Abstract

The promise of novel plant-based meat alternatives (PBMAs) to lessen the health and environmental impacts of meat consumption ultimately depend on market acceptance and the extent to which they displace meat in consumers’ diets. We use household scanner data to provide an in-depth analysis of consumers’ PBMA buying behaviors. PBMAs buyers tend to be young, single, female, college educated, employed, higher income, and non-white. About 20% of consumers purchased a PBMA at least once, and 12% purchased a PBMA on multiple occasions. About 2.79% of households only purchased PBMAs. About 86% of PBMA buyers also bought ground meat; however, PBMA buyers spent about 13% less on ground meat. Interestingly, after a household’s first PBMA purchase, ground meat consumption did not fall. The number of households buying a PBMA for the first time fell over the two year period studied, despite the increase in market share in the ground meat market.

Similar content being viewed by others

Introduction

In recent years, concerns have increased around the health and environmental impacts of meat consumption1,2,3,4,5,6,7,8. Encouraging dietary change toward more plant-based diets has been proposed to reduce dietary-related land-use, water use, and greenhouse gas emissions1,2,9,10. From a public health perspective, substitution to a plant based diet has been estimated to lower the risk of chronic diseases and mortality11,12,13,14. Despite encouragement for dietary change, consumer demand for meat remains high and is growing15. Moreover, there is little public support for policies to tax foods based on health or environmental outcomes16. The current dilemma faced by the industry and policymakers is between persistently high meat demand and a lack of political support for policies that would curb meat consumption. A potential solution is to invest in innovative plant-based meat alternatives (PBMA) that have the potential to induce consumers to willingly transition away from animal to plant-based diets17,18,19,20,21. Novel PBMAs use ingredients such as soy, wheat, pea, and heme to mimic the sensory characteristics and macronutrients of meat.

Interest in PMBAs also stems from potential environmental benefits. Several studies have suggested that reducing meat consumption in favor of a more plant-based diet will lead to better environmental outcomes, which include, reducing greenhouse gas (GHG) emissions, land use, and water use relative to conventional beef production3,17,18,22,23. However, for these environmental benefits to be realized, consumers must be willing to choose PBMAs over meat options. At this point, much remains unknown about consumer purchase behaviors surrounding PBMAs.

What is known about consumer preferences for PBMAs is primarily limited to hypothetical stated preference surveys16,24,25,26,27, industry and interest groups reports28,29, and analysis of retail scanner data that aggregates over thousands of consumers30. Analysis of household scanner data has only recently been undertaken31. These previous studies have estimated market shares for PBMAs that range from 30% to less than 1%. These estimates depended on how the market is defined (e.g., ground products vs. all beef vs. all meat), the data source used (e.g., stated preference survey vs. retail scanner data), and the unit of measurement (e.g., share of quantities sold or share of sales)16,26,27,28,29,30,32,33. Most estimates of retail scanner data put the dollar market share of PBMA out of all meat sales at less than 1%, a figure that grew rapidly from 2019–2021, but that appears to have stalled in 202228,30. Analysis using scanner data has suggested low repeat purchases of PBMAs and that PBMAs are not a substitute for beef or pork31.

Some studies have analyzed the demographic characteristics of PBMA buyers16,24,25,26,31,32,34,35. These studies found that PBMA consumers are more likely to be younger, higher income, female, more educated, politically liberal, residing in urban areas, and with young children16,24,25,26,31,32,34,35. These prior studies also identified key consumer beliefs associated with PBMA consumption, such as, following a vegetarian or vegan diet, concerns for the environmental impact of meat production, health concerns of meat consumption, and more concern for animal welfare16,24,25,26,36,37,38.

The primary objective of this study is to determine dynamics of the PBMA market and consumer characteristics of PBMA consumers using household scanner data spanning the two year period of November 2018 to November 2020. These rich transaction-level data help inform a number of key unresolved questions about the demand for PBMAs. What are the drivers of PBMA purchases? We expect that demand for PBMAs is stable and growing if consumers are particularly concerned for the environmental impacts of meat production and animal welfare, while being satisfied with the taste of PBMAs. If instead, however, novelty is a key driver, high initial sales may be followed by stagnation in sales, once the novelty of the PBMA products has worn off. Insights into this matter can be explored by determining the extent which PBMA sales are coming from repeat vs. new household purchases. Another key question is the extent to which consumers are substituting away from meat toward PBMAs, in which case the new products are likely to hamper meat demand. Also, if sales of PBMAs are coming from households who do not primarily purchase much meat, the rising market share of PBMAs could be explained by an expansion of the market. Finally, what are the characteristics of people who buy PBMAs? Knowledge of such information can help identify target markets and provide insights into the trajectory of sales.

Results

Market share

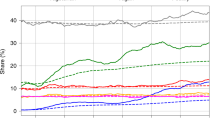

Out of sales for all ground meat products, the PBMA expenditure share averaged 5.91% from November 2018 to November 2020 (Fig. 1). The PBMA expenditure share gradually increased over the two year span, reaching a peak of 8.40% in October of 2020, nearly double the initial 4.22% share in November of 2018. The average PBMA expenditure experienced a sharp but brief decline after the onset of the COVID-19 pandemic in March and April of 2020 but then recovered in May of 2020 (Supplementary Fig. 1).

Plant-based meat alternative share of total expenditures on ground meat products.

General household behavior

Over the two year period 7,761 (19.92%) households purchased a PBMA at least once, while 31,205 (80.08%) households did not purchase a PBMA over this time (Fig. 2). Among the full sample of consumers, 12.03% of households bought PBMAs on multiple occasions (Supplementary Table 2). Among households who purchased a PBMA at least once, 60.15% made a repeat purchase, meaning 39.85% of PBMA buyers tried the product only once.

Overview of household consumption behavior.

In the full sample of households, a small fraction 1,089 (2.79%) avoided ground meat entirely and only purchased PBMAs (Fig. 2). Of consumers who bought a PBMA, 14.51% did not purchase ground meat. Most households (85.97%) that purchased a PBMA also purchased ground meat at some point in the two year span; however, as will soon be noted, PBMA buyers tended to spend less on ground meat than non-PBMA buyers.

Demographic analysis of household behavior and market analysis

Table 1 shows that a larger share of households with a younger head (< 35) were more likely to make a PBMA purchase than middle age (35–64) and older households (65 +). A significantly higher share of single female households purchased a PBMA than married or single male households. Additionally, a higher share of households that have an employed or college educated household head purchased a PBMA. Significant differences were also observed among income groups, revealing households with an income of $100,000 or greater were more likely to purchase a PBMA than middle income ($45,000-$99,999) or lower income (< $45,000) households. A larger share of African-American and other minority households purchased a PBMA than white households. Also, larger share of households with children purchased a PBMA than households without children.

A majority of consumers did not purchase PBMAs at all. Non-PBMA buyers were more likely to be older (65 +), married or single males, not college educated, not employed, lower income (< 45,000), white, and without children, rather than younger (< 35) or middle age (35–64), single females, college educated, employed, middle ($45,000–$99,999) or high income (> $100,000), non-white racially, and without children.

About 12% of households (6,670), purchased both ground meat and PBMAs over the two year period. A higher share of dual-purchasing households is younger (< 35), married or single females, college educated, employed, high income (> $100,000), African American, Hispanic, and with children present, relative to dual-purchasing households that are middle age (35–64) and older (65 +), single males, non-college educated, unemployed, low (< $45,000) or middle income ($45,000–$99,999), white or other race, non-Hispanic, and without children present. Among the sample of PBMA buyers, a majority purchased both PBMA and ground meat, but a higher share of households with more members (≥ 2), married, not college educated, high income (> $100,000), African-American, and with children present, purchased both PBMAs and ground meat relative households that were smaller (< 2), unmarried, college educated, lower (< $45,000) or middle income ($45,000–$99,999), white or other race, and without children present.

Some households (1087) did not purchase any ground meat (Fig. 2). This group has a higher share of households that are younger (< 35), with one member, single males, college educated, employed, a minority that is not African-American, and without children, relative to households that are middle age (35–64) and older (65 +), with more than one member, single females or married, non-college educated, unemployed, white or African American, and with children present. In the sample limited to PBMA buyers, a higher share of households with one member, single male heads, college educated, low income (< $45,000), of a minority that is not African American, and without children present only purchased PBMAs relative to households with more than one member, single females or married, not college educated, middle ($45,000–$99,999) or high income (> $100,000), white or African-American, and with children present.

A higher share of households that are younger (< 35), single females, college educated, employed, higher income (> $100,00), African-American and other minorities, and with children present made repeat purchases of PBMAs, relative to households that are middle age (35–64) and older (65 +), single males or married, non-college educated, unemployed, low (< $45,000) or middle income ($45,000–$99,999), white, and without children present. Among the sample of PBMA purchasing households, there were few significant differences among demographic groups in repeat-purchase behavior.

The average household in the full sample purchased 1.53 PBMA units (or 0.01 per week) over the two year span (Table 2; Supplementary Fig. 2). Looking only at PBMA purchasing households, 7.69 units on average were purchased in two years (or 0.07 per week). Among all households, two-year expenditures on PBMAs were $6.78 ($0.07/week) and was $34.04 (or $0.33/week) for households who purchased at least one PBMA. By contrast, households spent $112.74 over the two year period on ground meat ($1.08/week). For households who purchased a PBMA, they spent $97.78 on ground meat ($0.94/week).

The time-series nature of the data permits an investigation of purchase behavior before and after the first observed purchase of PBMAs. The average PBMA purchasing household bought more ground beef units (0.02) and spent more on ground beef ($0.50) after their first PBMA purchase then they did prior to their first PBMA purchase. New entrants into the PBMA market declined over the period (Supplementary Fig. 5) despite the fact that even at the period’s end, 80.08% had not purchased a PBMA. The week in which the highest number of households entered was the initial week of the study period in November 11, 2018.

Significant differences between demographic groups were observed with regards to PBMA units purchased and expenditures (Table 3). In the full sample, the households that purchased the most PBMA units and had the highest expenditures were younger (< 35), single males, college educated, employed, high income (> $100,000), and African-American compared to households that are middle age (45–64) or older (65 +), single females or married, not college educated, unemployed, low (< $45,000) or middle income ($45,000-$99,999), and white or another minority race. Among the sample including only PBMA buyers, single males purchased more units and had higher expenditure than females.

The number of ground meat units purchased was significantly lower among PBMA buyers (15.43) than the full sample (15.95), which resulted in significantly lower total expenditure on ground meat options (Table 2) among PBMA buyers compared to non-buyers. The average ground meat units and expenditure purchased by a buyer in the market was fairly constant across the two year span with a spike during the early stages of the COVID-19 pandemic in March of 2020 (Supplementary Fig. 3; Supplementary Fig. 4).

Households that are middle age (35–64), have more members (≥ 2), married, not college educated, employed, high income (> $100,000), white, not Hispanic, and have children present purchased and spent more on ground meat than households that are younger (< 35) or older (65 +), less members (< 2), single males or females, college educated, unemployed, low (< $45,000) or middle ($45,000–$99,999) income, minority race, Hispanic, and without children present (Table 4). Among the sample limited to PBMA buyers, households that are middle age (35–64), have more members, married, not college educated, employed, high income (> $100,000), non-Hispanic, and with children present purchased more ground meat units and had higher expenditure on average than households that are younger (< 35) or older (65 +), have less members, single males or females, college educated, unemployed, low (< $45,000) or middle ($45,000–$99,999) income, Hispanic, and without children present. One primary difference is that African-American households purchased the most units, but white households had the highest expenditure. Similar patterns are observed for the weekly household average expenditure and purchases of ground meat where households that are middle age (35–64), larger, married, not college educated, employed, higher income (> $100,000), white, non-Hispanic, and with children present had the highest weekly expenditures and units purchased.

Potential implications of COVID-19

Additionally, we analyzed if the potential effects of the COVID-19 pandemic on the units purchased and expenditures on ground meats and PBMAs among the full sample of households and PBMA buyers (Supplementary Table 3). We observed that among both the full sample and PBMA buyers that purchases of ground meats and PBMAs significantly increased after the beginning of the COVID-19 pandemic.

Discussion and conclusions

This study sought to provide a deeper understanding of the market for PBMAs. From November 2018 to November 2020, expenditure shares for PBMAs, out of the ground meat market, increased from 4.22 to 6.29%. Expenditure shares declined sharply in the early stages of the COVID-19 pandemic in March and April of 2020 but quickly recovered. Our expenditure share estimates are larger than previous analysis, likely due to the fact that we limited our analysis to ground products28,30,33,39.

Another objective of our study was to identify consumer segments of PBMA purchasers by behavior. We identified that a sizable portion of ground meat consuming households purchased PBMAs, and that among PBMA purchasers, repeat-purchasing behavior was common (60.15%) but not universal. Novelty seeking was also prevalent (39.85%), indicating a sizable portion of households were potentially not satisfied with the developments in PBMAs. A vast majority of PBMA purchasing households bought ground meat options in addition to selecting some PBMAs. However, it is important to note that on average, PBMA purchasing households purchased fewer units and spent less on ground meat than households that only purchased ground meat options. Our evidence suggests that entering the PBMA market does not deter ground meat purchasing households from purchasing ground meat, as weekly units purchased and expenditure on ground meat products increased on average after the purchase of the first PBMA. These results show that PBMAs largely to do not deter meat demand amongst purchasing households and that rising PBMA market shares are not necessarily indicative of an expanding market since most purchasers of the products also purchase meats.

Similar previous studies from stated preference surveys, we identify that consumers of PBMAs are more likely to be younger (< 35), higher income (> $100,000), female, college educated, and of non-white minority racially16,24,25,26,34,35. Our additional contributions include the finding that repeat-purchasing of PBMAs was prevalent, especially among households with a younger (< 35), employed, and college educated head. Despite the prevalence of repeat-buying among PBMA buyers, a majority of households that purchased PBMAs bought both ground meat and PBMAs, which is consistent with Zhao et al. (2022) indicating that PBMAs may be complementary to beef. This phenomenon of continuing ground meat purchases provides some evidence that PMBAs are not leading to substitution away from ground meat options17,18,19,20. The high prevalence of novelty seeking behavior also shows that PBMAs are not leading to substitution away from meats after purchasing PBMAs. This finding also suggests additional evidence that even though interest and market share have increased surrounding PBMAs, that meat markets and their supply chain are not significantly affected by the PBMA market40.

Our additional insight into consumer segments is observing differences in household expenditures on PBMAs and ground meats. We found that younger (< 35), single male, college educated, employed, high income (> $100,000), and African-American households on average had the highest weekly expenditures of PBMAs. When considering only buyers of PBMAs we observe few significant differences between households in expenditure other than in marital status, which potentially indicates that households that are purchasers of PBMA exhibit similar preferences across demographic groups. This is not true of ground meat purchasers, where many significant differences occurred in patterns of expenditure. Households with more members, higher income, married, and with children present income had the highest expenditure.

Finally, we also identified that the COVID-19 pandemic had a significant effect on the units purchased and household expenditure of ground meats and PBMAs. We observed that households on average, purchased more units of both ground meats and PBMAs after the beginning of the COVID-19 pandemic. These results are consistent with general estimates on food and grocery spending, which indicate that expenditures and volumes of food purchased at home increased drastically at the onset of the COVID-19 pandemic41.

PMBA sales grew from November 2018 to November 2020. However, some recent reports have suggested declining sales42. Our results foreshadow this decline in sales with the sizable portion of households engaging in novelty seeking behavior as well as the general trend of declining market entry amongst households. A particularly interesting finding is that few significant differences were measured in mean purchases and expenditures of PBMAs between purchasing households, which indicates that demographic differences are not evident among buyers of PBMAs indicating they may have similar preference structures. Despite the increase in market share and repeat-purchases among PBMA purchasing households, entering the PBMA market did not decrease household purchases of ground meat. Future research can include insight into important product characteristics consumers consider when purchasing PBMAs. Another interesting segment of this market is food away from home. Despite reports of declining sales multiple restaurant chains, such as, Kentucky Fried Chicken (KFC) have recently introduced meatless chicken nuggets43, which indicate that food service providers still see PBMAs as viable products. This market is still in its infancy and will likely substantially evolve in time.

Many questions still remain with respect to PBMAs. One primary issue are the questions surrounding the healthiness of the new novel PBMAs for long term human health, despite having similar macronutrient values to the beef options they are simulating44,45,46. It is also unclear as to the effects of the novel PBMAs on the environment. The companies producing the products have released favorable life cycle analyses regarding these products17,18. Despite the favorable life cycle analysis results, some have estimated suggest that changes in the prices of PBMAs do little to affect the beef supply chain, thus potentially only inducing minor environmental and climate benefits40.

Methods

Data

This study utilizes the Information Resources, Inc. (IRI) household scanner panel dataset. Households who made at least one meat or PBMA purchase from November 2018 to November 2020 were included. The resulting data set consists of individual-transaction data from 38,966 households. Each entry in the dataset is recorded at a universal product code (UPC) level. The dataset includes UPCs of the primary categories of beef, poultry, seafood, pork, PBMAs, turkey, etc. Each UPC code is attached to a product description which includes characteristics such as the brand, processing method, packaging, and size. Additionally, each UPC represents a specific set of product characteristics which include the brand, type of meat, fat content, weight, etc. We aggregated purchases to the weekly level, implying 104 weeks of observations for each of the 38,966 households.

The PBMAs did not include non-patty or non-ground substitutes such as sausage link substitutes. The PBMAs studied resemble ground meat products and are theoretically the closest substitute. Thus, we restricted analysis to purchases of ground meat options (ground beef, ground chicken, ground turkey, or ground/crumble/patty), and PBMA patties and burgers. The ground meat products include categories of ground beef, beef burgers, ground turkey, turkey burgers, ground chicken, soy burgers, and newer forms of PBMAs. The total number of transactions in the dataset are 505,262 consisting of 439 UPCs. The UPCs that remained in the dataset were those were purchased on 50 or more occasions in the span of the dataset. Many UPCs that were purchased on 50 or less occasions were unclear as to what the products specifically were, and thus were not considered for this analysis.

In addition to product characteristics, the demographics of each household are known. The demographics considered are the age of the household head (young (< 35), middle age (35–64), old (65 +)), the number of individuals in the household, marital status (married, single female, single male), education level (college degree or not), employment status (employed or not), income level (low (< $45,000), middle ($45,000-$99,999), high (> $100,000)), race (white, African-American, other races), Hispanic, and the presence of children. Due to the nature of the data, some household entries contain characteristics of both a female and male head of household. In these cases, the female characteristics are considered as the primary characteristics when a female household head is present due to the fact that a majority of primary shoppers in household are females47. Female characteristics were used when applicable for the age of the household head, and the education level as the other demographic characteristics were used to describe the household in general without taking into account the specific heads of household. Supplementary table 1 details the household demographic breakdown.

After identifying the relevant demographics and UPCs we aggregate the products using indicator variables for ground beef, turkey, chicken, and PBMAs. We aggregate the purchases for each of these product types for each individual household for each week over the span of two years. These aggregations formulate a dataset of 38,966 households that purchased at least one of the UPCs in the product categories of ground beef, turkey, chicken, and PBMAs. Next, we identified the households who purchased at least one PBMA over the span of the dataset, which added up to 7761 households.

Data analysis

Our first market analysis is the expenditure share of PBMAs relative to other ground meats over the two year span of the dataset. We estimate the expenditure share by taking the sum of dollars spent on a particular ground meat option in a given week and divided that by the total expenditure on ground meat and PBMAs in a given week. Additionally, we estimate the market expenditures and units purchased for ground meats and PBMAs by taking the total expenditure and units purchased in a given week and divide that by the number of households who purchased a product in that specific week.

Next we estimate an overview of purchasing behavior by both the full sample and PBMA consumers estimating the share of PBMA buyers, the share of households that purchased PBMAs on more than one occasion, the share of households that did not purchase ground meat, the share of households who only purchased ground meat and no PBMAs, and the share of households who purchased both ground meat and PBMAs. We estimate the share of households that purchased PBMAs by denoting a household as a buyer if they purchased at least one PBMA over the span of two years. This provides the smaller subset of the sample of PBMA buyers. The share of households who made repeat purchases is estimated by examining if a household if made purchases of PBMAs on multiple occasions in the dataset. If they did make multiple purchases they were assigned an indicator variable for engaging in habit forming behavior. Next, we estimated the share of households that did not purchase ground meat. These estimates were calculated by assigning a dummy variable to a household that purchased at least 1 one ground meat item over the span of the dataset. If they received a “0” for this indicator they were included in the share that did purchase ground meat. Using the indicator variable for ground meat buyers and PBMA buyers, we also estimate the share of households who purchased ground meat only, and the share of households that purchased both ground meat and PBMAs.

After estimating the overall shares of household behaviors, we estimate the average aggregate number of units purchased, average number of weekly units purchased, average total expenditure, and average weekly expenditure for both PBMAs and ground meat. We estimate the number of units purchased by calculating the sum of units of ground meat and PBMAs purchased by a household. The weekly units are estimated by dividing the total number of units purchased by the 104 weeks of data collection. The same process is repeated for the ground meat and PBMA expenditures.

The final metric is to estimate if ground meat units and expenditures changed after the household entered the PBMA market by making their first purchase. We estimate the average weekly consumption of ground meat products by first finding the week that a household made their first purchase of a PBMA. Next we took the sum of ground meat units and expenditure on ground meat products before and after the first purchase occurred. After taking the sum of units and expenditures, we divide the sums by the number of weeks before and after the first purchase. The averages are then compared in a paired t-test to examine if purchasing patterns changed amongst households after the first PBMA purchase.

After the estimating the general behavioral overview of the households in the market, we analyzed the consumer segments and purchasing patterns by demographic groups. First we estimated the consumer segments, which were the share of PBMA buyers, the habit forming buyers who purchased on more than one occasion, the share of households who did not purchase PBMAs, the share of households who purchased both ground meat and PBMAs, and the share of households that did not purchase ground meat. To test the differences a chi-squared test was used where the null hypothesis is that no association is detectable between the binary outcome variable and the demographics.

Next, we estimated the demographic differences for the aggregate and weekly number of units purchased and expenditures for both ground meat options and PBMAs. Due to these variables being continuous outcomes, we employed an analysis of variance (ANOVA) test with a null hypothesis that the difference in means between demographic groups for these metrics were equal to 0.

The final metric we estimated was if household purchases and expenditures of ground meats and PBMAs after the beginning of the COVID-19 pandemic. We estimated the average number of units purchased and expenditures prior to March 1, 2020 and after. This date was chosen as it resembled the month in which the early stages of the economic disruptions from COVID-19 began in the food sector41. We tested the differences in the averages with a paired t-test before and after the beginning of the pandemic.

We confirm that all methods were carried out in accordance with the relevant guidelines from Information Resources Inc. (IRI) and Purdue University. Due to the nature of the data the approval to conduct research with this data was given by a signed contract with Information Resources Inc. (IRI). All respondents give consent to Information Resources Inc.

Data availability

Due to contractual obligations with Information Resources, Inc. (IRI), we are not at liberty to share the data.

References

Clark, M. A., Springmann, M., Hill, J. & Tilman, D. Multiple health and environmental impacts of foods. Proc. Natl. Acad. Sci. U. S. A. 116, 23357–23362 (2019).

Clark, M. & Tilman, D. Comparative analysis of environmental impacts of agricultural production systems, agricultural input efficiency, and food choice. Environ. Res. Lett. 12, 064016 (2017).

de Vries, M. & de Boer, I. J. M. Comparing environmental impacts for livestock products: A review of life cycle assessments. Livest. Sci. 128, 1–11 (2010).

Sanchez-Sabate, R. & Sabaté, J. Consumer attitudes towards environmental concerns of meat consumption: A systematic review. Int. J. Environ. Res. Public Health 16, 1220 (2019).

Mazac, R. et al. Incorporation of novel foods in European diets can reduce global warming potential, water use and land use by over 80%. Nat. Food 3, 286–293 (2022).

Tuninetti, M., Ridolfi, L. & Laio, F. Compliance with EAT-Lancet dietary guidelines would reduce global water footprint but increase it for 40% of the world population. Nat. Food 3, 143–151 (2022).

Sun, Z. et al. Dietary change in high-income nations alone can lead to substantial double climate dividend. Nat. Food 3, 29–27 (2022).

Parlasca, M. C. & Qaim, M. Meat consumption and sustainability. Annu. Rev. Resour. Econ. 14, 1–25 (2022).

Heller, M. C., Willits-Smith, A., Meyer, R., Keoleian, G. A. & Rose, D. Greenhouse gas emissions and energy use associated with production of individual self-selected US diets. Environ. Res. Lett. 13, 044004 (2018).

Eshel, G., Shepon, A., Makov, T. & Milo, R. Land, irrigation water, greenhouse gas, and reactive nitrogen burdens of meat, eggs, and dairy production in the United States. Proc. Natl. Acad. Sci. U. S. A. 111, 11996–12001 (2014).

Fehér, A., Gazdecki, M., Véha, M., Szakály, M. & Szakály, Z. A comprehensive review of the benefits of and the barriers to the switch to a plant-based diet. Sustainability 12, 1–18 (2020).

Godfray, H. C. J. et al. Meat consumption, health, and the environment. Science 361, 6399 (2018).

Zheng, Y. et al. Association of changes in red meat consumption with total and cause specific mortality among US women and men: Two prospective cohort studies. BMJ 365, l2110 (2019).

Springmann, M., Godfray, H. C. J., Rayner, M. & Scarborough, P. Analysis and valuation of the health and climate change cobenefits of dietary change. Proc. Natl. Acad. Sci. U. S. A. 113, 4146–4151 (2016).

Lusk, J. L. & Tonsor, G. T. Supply and demand indices and their welfare implications. Q Open 1, 1–22 (2021).

Van Loo, E. J., Caputo, V. & Lusk, J. L. Consumer preferences for farm-raised meat, lab-grown meat, and plant-based meat alternatives: Does information or brand matter?. Food Policy 95, 101931 (2020).

Beyond Meat. Beyond Meat. https://www.beyondmeat.com/ (2021).

Impossible Foods. Impossible. https://impossiblefoods.com/ (2021).

Bandoim, L. Fungi-Based Meat Wants To Be Your Meatless Monday Dinner (Forbes, 2021).

Safran Foer, J. The End of Meat is Here (The New York Times, 2020).

Stanton, C. Restaurants Saved 700K Animals with Plant-based Offerings Last Year. More Options are Coming in 2022 (USA TODAY, 2022).

Aiking, H. Future protein supply. Trends Food Sci. Technol. 22, 112–120 (2011).

Herrero, M. et al. Livestock and the environment: What have we learned in the past decade?. Ann. Rev. Environ. Resour. 40, 177–202 (2015).

Bryant, C., Szejda, K., Parekh, N., Desphande, V. & Tse, B. A survey of consumer perceptions of plant-based and clean meat in the USA, India, and China. Front. Sustain. Food Syst. 3, 1–11 (2019).

Carlsson, F., Kataria, M. & Lampi, E. How much does it take? Willingness to switch to meat substitutes. vol. 2473 https://ideas.repec.org/p/hhs/gunwpe/0798.html (2021).

Slade, P. If you build it, will they eat it? Consumer preferences for plant-based and cultured meat burgers. Appetite https://doi.org/10.1016/j.appet.2018.02.030 (2018).

Tonsor, G. T. Meat Demand Monitor - February 2022. https://www.agmanager.info/livestock-meat/meat-demand/monthly-meat-demand-monitor-survey-data/monthly-meat-demand-monitor-14 (2022).

IRI. Protein & performance. 1–12 (2020).

Reorink, A.-M. September brought continued gains for meat alternative sales. The Shelby Report https://www.theshelbyreport.com/2020/11/11/september-continued-gains-meat-alternative-sales/ (2020).

Zhao, S., Wang, L., Hu, W. & Zheng, Y. Meet the meatless: Demand for new generation plant-based meat alternatives. Appl. Econ. Perspect. Policy https://doi.org/10.1002/aepp.13232 (2022).

Cuffey, J., Chenarides, L., Li, W. & Zhao, S. Consumer Spending Patterns for Plant-Based Meat Alternatives. Appl. Econ. Perspect. Policy https://doi.org/10.1002/aepp.13280 (2022).

Tonsor, G. T., Lusk, J. L. & Schroeder, T. C. Market potential of new plant-based protein alternatives: Insights from four US consumer experiments. Appl. Econ. Perspect. Policy https://doi.org/10.1002/aepp.13253 (2022).

Good Food Institute. U.S. retail market data for the plant-based industry. https://gfi.org/marketresearch/ (2021).

Onwezen, M. C., Bouwman, E. P., Reinders, M. J. & Dagevos, H. A systematic review on consumer acceptance of alternative proteins: Pulses, algae, insects, plant-based meat alternatives, and cultured meat. Appetite 159, 105058 (2021).

T. Tonsor, G. & L. Lusk, J. Impact of new plant-based protein alternatives on U.S. Beef Demand. https://www.agmanager.info/livestock-meat/meat-demand/meat-demand-research-studies/impact-new-plant-based-protein-0 (2021).

Michel, F., Hartmann, C. & Siegrist, M. Consumers’ associations, perceptions and acceptance of meat and plant-based meat alternatives. Food Qual. Prefer. 87, 104063 (2021).

Circus, V. E. & Robison, R. Exploring perceptions of sustainable proteins and meat attachment. Br. Food J. 121, 533–545 (2019).

Hwang, J., You, J., Moon, J. & Jeong, J. Factors affecting consumers’ alternative meats buying intentions: Plant-based meat alternative and cultured meat. Sustainability 12, 5662 (2020).

IRI. IRI CPG Demand Index. https://indices.iriworldwide.com/covid19/?i=0 (2021).

Lusk, J., Blaustein-Rejto, D., Shah, S. & Tonsor, G. T. Impact of plant-based meat alternatives on cattle inventories and greenhouse gas emissions. Environ. Res. Lett. 17, 024035 (2022).

USDA ERS. Food and Consumers. https://www.ers.usda.gov/covid-19/food-and-consumers/#spending (2022).

Watson, E. IRI: US retail sales of refrigerated plant-based meat − 3.1% YoY in Q3 as Beyond meat predicts slower sales. Food Navigator (2021).

Valinsky, J. KFC’s new menu item tastes like chicken (but isn’t). CNN Business2 https://www.cnn.com/2022/01/04/business/kfc-beyond-fried-chicken-launch/index.html (2022).

Hu, F. B., Otis, B. O. & McCarthy, G. Can plant-based meat alternatives be part of a healthy and sustainable diet?. JAMA - J. Am. Med. Assoc. 322, 1547–1548 (2019).

Rubio, N. R., Xiang, N. & Kaplan, D. L. Plant-based and cell-based approaches to meat production. Nat. Commun. 11, 1–11 (2020).

Toh, D. W., Kiat, A. S. R. V. & Henry, C. J. Unknown impacts of plant-based meat alternatives on long-term health. Nat. Food 3, 90–91 (2022).

Schaeffer, K. Among U.S. couples, women do more cooking and grocery shopping than men. Pew Research Center. https://www.pewresearch.org/fact-tank/2019/09/24/among-u-s-couples-women-do-more-cooking-and-grocery-shopping-than-men/ (2019).

Author information

Authors and Affiliations

Contributions

Z.T.N. contributed to the drafting, writing, and editing of the manuscript, conducted the data analysis, interpreted the data, and aided in data acquisition. J.L.L contributed to the writing and editing of the manuscript, data acquisition, and supervised the data analysis and interpretation. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Neuhofer, Z.T., Lusk, J.L. Most plant-based meat alternative buyers also buy meat: an analysis of household demographics, habit formation, and buying behavior among meat alternative buyers. Sci Rep 12, 13062 (2022). https://doi.org/10.1038/s41598-022-16996-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s41598-022-16996-5

This article is cited by

-

Microbial community structure of plant-based meat alternatives

npj Science of Food (2024)

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.