Abstract

Climate change mitigation generally require rapid decarbonization in the power sector, including phase-out of fossil fuel-fired generators. Given recent technological developments, co-firing of hydrogen or ammonia, could help decarbonize fossil-based generators, but little is known about how its effects would play out globally. Here, we explore this topic using an energy system model. The results indicate that hydrogen co-firing occurs solely in stringent mitigation like 1.5 °C scenarios, where around half of existing coal and gas power capacity can be retrofitted for hydrogen co-firing, reducing stranded capacity, mainly in the Organization for Economic Co-operation and Development (OECD) countries and Asia. However, electricity supply from co-firing generators is limited to about 1% of total electricity generation, because hydrogen co-firing is mainly used as a backup option to balance the variable renewable energies. The incremental fuel cost of hydrogen results in lower capacity factor of hydrogen co-fired generators, whereas low-carbon hydrogen contributes to reducing emission cost associated with carbon pricing. While hydrogen co-firing may play a role in balancing intermittency of variable renewable energies, it will not seriously delay the phase-out of fossil-based generators.

Similar content being viewed by others

Introduction

The Paris Agreement set climate goals of a temperature increase well below 2 °C and to pursue efforts for below 1.5 °C. The corresponding mitigation pathways require huge and rapid reduction of CO2 emissions from the energy sector; in particular, the power sector needs to be decarbonized rapidly in the coming decades1,2,3. Given the recent trends and future expectation of decreasing costs for solar photovoltaic (PV) and wind power4,5, mitigation strategies proposed for power system decarbonization generally involve upscaling of low-carbon electricity, especially renewable sources replacing fossil fuel-fired generators6,7. Such mitigation scenarios generally involve phase-out and retirement of fossil fuel-fired powerplants before their expected lifetime, resulting in stranded assets8,9,10. Although carbon capture and storage (CCS) would facilitate fossil fuel-fired power generation under the low emissions scenarios, CCS-based electricity generation is limited in the mitigation scenarios of the Intergovernmental Panel on Climate Change Sixth Assessment Report (IPCC AR6), with a median value <10% in 205011 due to several barriers, such as incremental capital costs and energy penalties12,13.

Hydrogen is expected to contribute to deep decarbonization, replacing fossil fuels in sectors that are hard to decarbonize, such as long-distance transport and some industry sectors14,15,16. Meanwhile for the power sector, flexible generators that integrate variable renewable energies (VREs), such as gas-fired generators, will be difficult to decarbonize17. However, previous studies have not intensively focused on application of hydrogen to power sector decarbonization. Hydrogen co-firing, including hydrogen-based energy carriers such as ammonia, could be an option of CO2 emissions abatement from fossil fuel-fired generators as long as the necessary hydrogen is generated from low-carbon sources, such as renewable electricity and biomass18,19. In addition, hydrogen could potentially contribute to VRE integration as a seasonal storage option for electricity20,21. Given the recent decreases in costs of solar PV and wind power generators and the expectation of increasing low-carbon hydrogen supply through electrolysis4,5, hydrogen co-firing may be an option for power system decarbonization.

Hydrogen is a secondary energy carrier that is obtained from various energy sources. Therefore, its role has been assessed using energy system models and integrated assessment models (IAMs), which cover both energy supply and demand sectors, as well as power system models. Nevertheless, as only a few studies have assessed hydrogen use in the power sector, there are still several knowledge gaps associated with the potential role of hydrogen. First, previous studies have mainly focused on hydrogen co-firing only with natural gas-fired generators and with a limited regional coverage. Öberg et al.18 used a power system model for European countries and found that hydrogen co-firing is limited benefit in natural gas powerplant, even in a stringent mitigation scenario. Bui et al.22 evaluated the CO2 emission intensity of hydrogen-based generators and indicated that it can contribute to decarbonizing natural gas generators such as CCS. In national model intercomparison studies for Europe and the US, some models have included hydrogen-based energy carriers, concluding that hydrogen is mainly used in high-density transport fuels and high-temperature industrial processes, whereas its use in the power sector is limited23,24. Although these studies have provided insights into the role of hydrogen, the potential of hydrogen co-firing at the global level, including at coal and at gas powerplants, is not yet well understood. Second, although retrofitting fossil-fueled generators with hydrogen co-firing can theoretically reduce stranded asset risks, little is known about such effects. Because global coal power generation is currently still rising, especially in Asian countries25, stranded asset risk can be a significant issue in these regions10,26,27. Although previous studies have assessed the effect of retrofitting coal powerplant with carbon capture and biomass co-firing28,29, the potential impact of hydrogen co-firing on avoiding stranded asset risks has not yet to be explored.

Against these backgrounds, the question of whether hydrogen co-firing could reduce the transition risks associated with the phase-out of fossil-fueled generators and stranded assets arises. As described in the International Energy Agency (IEA) Net-Zero report30, hydrogen co-firing could theoretically lead to continued use of existing coal- and natural gas-based assets under the energy system transition scenario. The Group of Seven (G7) Climate, Energy and Environment Ministers’ Communiqué of April 202331, acknowledges the roles of hydrogen and ammonia in the power sector towards net-zero emissions, although their impacts have not been explored. To clarify this research question, we develop a global energy system model with high temporal resolution with a variety of technology options, including hydrogen co-firing. In this study, we explore the potential role of hydrogen co-firing on decarbonization of the global energy system.

Quantitative scenario assessment is conducted using the Asia-Pacific Integrated Model (AIM)-Technology, which is a global bottom-up energy system model. Although hydrogen production and use in the final energy sectors have been modeled in previous studies14,32, there are three major advancements associated with hydrogen applications in the power sector to address the research question of this study. First, gas- and coal-fired power generators with hydrogen co-firing are represented to assess their roles in global mitigation scenarios. It is assumed that both hydrogen and ammonia can be co-fired for these generators (hereafter, hydrogen co-firing is defined as including both hydrogen and ammonia). Since the operating conditions of co-fired generators are determined endogenously in the model similar to other fossil fuel-fired generators, hydrogen co-fired generators can play a dual role in complementing the intermittency of VRE and serving as base or middle-load generators. Additional investments required for hydrogen co-fired generators, which vary with the hydrogen mix rate, are assumed based on the literature18. Second, the model is updated to represent the retrofitting of existing fossil fuel-fired generators with hydrogen co-firing and carbon capture technologies. Consequently, a technology retrofit is endogenously determined in the model, based on the additional investment required for the retrofit, the changes in energy and emissions performances, and the remaining lifetime of the upgraded plant. To quantify the amount of stranded assets in the mitigation scenarios, existing and planned coal and gas powerplant information is obtained from the literatures33,34. Third, to consider the seasonal variation in electricity demand and supply from VREs, the intra-annual temporal resolution is improved in this model. As previous studies assessing seasonal storage modeled monthly power supply and demand profiles35,36, the AIM-Technology in this study also contains 12 representative days corresponding to one per month and 24 h per day. More details about these changes are presented in the Methods section.

Multiple scenarios are prepared to assess the outcomes of hydrogen co-firing in various mitigation pathways and technology portfolios. The emissions pathways are based on carbon budgets by 2100 of 500, 700, 1000 and 1400 gigatonnes (Gt) -CO237. In the 500 Gt-CO2 scenario, which is compatible with the 1.5 °C goal, energy-related CO2 emissions are reduced to nearly net zero by 205014. Scenarios are also classified based on technology availability to explore conditions of hydrogen co-firing. The Default scenario is based on the default model setting with no any additional constraints or parameter changes. The H2-optimistic (H2Opt) scenario considers the drastic cost reductions for electrolyzer and solar and wind power, which are expected to enhance hydrogen co-firing. The Limited-CCS (LimCCS) scenario, where geological storage and bioenergy supply are constrained to 4 Gt-CO2 per year and 100 exajoule (EJ) per year, respectively, is assessed because it requires stringent residual emissions reductions and associated increases of carbon prices14. The H2Opt+ scenario is a what-if scenario with the most optimistic conditions for hydrogen co-firing. In addition to the conditions in the H2Opt and LimCCS cases, the H2Opt+ scenario includes higher cost assumptions for battery storage and no new construction of seasonal storage. The No-Cofire (NoCOF) scenario is assessed as a reference wherein hydrogen co-firing with fossil fuel-fired powerplants is not available. Sensitivity scenarios are also analyzed for various socio-economic conditions. More details about the assumptions of these scenarios are provided in the Methods.

Results

Hydrogen consumption in the power sector

Upscaling of low-carbon electricity, particularly solar and wind power, is commonly observed across all mitigation scenarios and regions (Fig. 1a, Supplementary Fig. 1). Consequently, CO2 emissions from energy supply sectors fall rapidly and range around −5 to 5 Gt–CO2 in 2050 under all the mitigation scenarios, while residual emissions from energy demand sectors account for around 5–15 Gt–CO2 in 2050 (Supplementary Fig. 2a, Supplementary Fig. 3). Carbon prices range from around 150 US $ per t-CO2 or higher by 2050, reaching 300–600 US $ per t-CO2 in the 500 Gt–CO2 scenarios, where energy-related CO2 emissions decreases to nearly net zero in 2050 (Supplementary Fig. 2b). Cumulative mitigation cost increases with increasing mitigation stringency, ranging around 0.9–1.1% of gross domestic product (GDP) in the 500 Gt–CO2 scenarios (Supplementary Fig. 4).

a Power generation in the 500, 700, 1000 and 1400 Gt–CO2 scenarios with Default technology. Results for other scenarios are shown in Supplementary Fig. 1. b Power generation from fossil fuel-fired generators (including hydrogen co-firing and carbon capture and storage [CCS]). Right bar plots illustrate the power generation from fossil fuels in 2050 as obtained from the Intergovernmental Panel on Climate Change Sixth Assessment Report (IPCC AR6) Scenario Database82 for each climate category (C1–C3). “n” denotes the number of available scenarios in each category. c, d Hydrogen co-firing as a share of total power generation in 2030 and 2050 in the world, and Asia, Latin America, Middle East and Africa, the Organization for Economic Co-operation and Development (OECD) and Europa (EU), and Reforming Economies, respectively. Results for other scenarios are shown in Supplementary Fig. 7. e Hydrogen co-firing as a share of fossil fuel-based power generation relative to carbon prices, excluding No-Cofire (NoCOF) cases.

A phase-out of fossil fuels in the power sector is generally observed across all mitigation scenarios, even when hydrogen co-firing is available. Power generation from fossil fuel-fired generators, which includes hydrogen co-firing, decreases rapidly, accounting for around <20 EJ per year by 2050 (Fig. 1b). These values are similar to the ranges obtained from the corresponding mitigation scenarios of the IPCC-AR6. A trend of decreasing fossil fuel use is also observed in the total primary energy supply across all regions (Supplementary Fig. 5). Although total power generation from fossil fuel-based generators decreases, stringent mitigation scenarios may employ hydrogen co-firing. In the 500 Gt–CO2 scenarios excluding the NoCOF scenarios, power generation from hydrogen co-fired generators reaches around 2–6 EJ per year in 2050, equivalent to around 30–90% of total fossil fuel-fired power generation (Supplementary Fig. 6). Nevertheless, the share of power generation associated with hydrogen co-firing is negligible compared to total power generation, accounting for <1% in 2050, including that for sensitivity scenarios with various technological and socio-economic conditions (Fig. 1c). Furthermore, in scenario with carbon budgets >1000 Gt–CO2, diffusion of hydrogen co-firing is very low, even for H2Opt+. In 2030, hydrogen co-firing is observed in the LimCCS, H2Opt, and H2Opt+ cases reaching ~2–4 EJ per year in the stringent mitigation scenarios, while hydrogen co-firing implementation is absent or very limited in the Default cases. Relative to the global average, the share of hydrogen co-firing in total power generation rises in the Organization for Economic Co-operation and Development (OECD) and Asian countries, followed by the Middle East and Africa; however, the contributions of hydrogen co-firing to total power generation remain limited, reaching 2–3% in each region (Fig. 1d).

Mitigation stringency is a driver of hydrogen co-firing, as this process is implemented when carbon prices exceed about 200 US $ per t-CO2 in the H2Opt, H2Opt+ and LimCCS cases, whereas it occurs in the Default scenarios at the carbon prices >300 US$ per t-CO2 (Fig. 1e). As hydrogen production depends on low-carbon electricity in these scenarios (Supplementary Fig. 8), hydrogen co-firing is an effective method to reduce CO2 emissions from energy supply sectors at such high carbon prices. Consequently, hydrogen co-firing of fossil fuel-based generators contributes to reducing CO2 emissions intensity, accounting for around 0.075 t-CO2 per GJ in the 500 H2Opt scenario and 0.1 t-CO2 per GJ in the 500 NoCOF scenario (Supplementary Fig. 9).

In addition to hydrogen utilization in the power sector, hydrogen and hydrogen-based energy carriers, including ammonia and synthetic hydrocarbons, also help reduce emissions in the final energy demand sectors (Supplementary Fig. 10). The main consumer of hydrogen is the transport sector, followed by other energy demand sectors (Supplementary Fig. 11). In comparison, hydrogen consumption in the power sector is relatively small.

Capacity factor of hydrogen co-fired generators

Although the impact of hydrogen co-firing on total electricity generation is limited, the capacity of hydrogen co-fired generators scales up rapidly, especially under stringent mitigation scenarios (Fig. 2a). In particular, in the 500 H2Opt, 500 H2Opt+ and 500-LimCCS scenarios, the capacity of hydrogen co-fired generators increases to more than half of total fossil fuel-fired powerplants in 2050, reaching about 2000, 5000, and 4000 gigawatts (GW), respectively (Fig. 2b). In these scenarios, around half of capacity for both coal- and gas-fired generators is equipped with hydrogen co-firing technology. It should be noted that the power capacity values in this study are larger than those in the IPCC-AR6 scenarios, as shown in Fig. 2b, because the AIM-Technology model has detailed time resolution, which results in a large requirement for back-up capacity for VRE intermittency. Despite the increase in hydrogen co-firing capacity, the annual average capacity factor of hydrogen co-fired powerplant is much lower than under today’s conditions, accounting for <30% and 5% of gas and coal generators, respectively (Fig. 2c). This difference arises because fossil fuel-fired generators with hydrogen co-firing are used as a backup source for balancing VRE intermittency, especially under stringent mitigation scenarios, resulting in these generators operating for only a few hours per year (Supplementary Fig. 13). In seasons when power generation from VRE is abundant, direct use of electricity from VREs is a more efficient option rather than converting the electricity into hydrogen due to conversion losses in the electrolysis and hydrogen-to-power conversion processes. In contrast, fossil fuel-fired generators with CCS have a higher capacity factor than hydrogen co-firing in 2050, reaching up to 70% and 30% for gas and coal, respectively. Nevertheless, the contribution of CCS plants to total power generation remains limited due to their cost penalty.

a Capacity of electricity generators from fossil fuels including hydrogen co-firing in the 500 and 1000 Gt–CO2 scenarios with H2-Optimistic (H2Opt) conditions. Results for other scenarios are shown in Supplementary Fig. 12. b Capacities of total fossil fuel-fired generators and hydrogen co-firing in 2030 and 2050 across various climate and technology scenarios. Right bar plots illustrate the capacity of total fossil fuel-fired generators in 2050 in the Intergovernmental Panel on Climate Change Sixth Assessment Report (IPCC AR6). “n” denotes the number of available scenarios in each category. c Annual average capacity factors of coal- and gas-fired generators in 2030 and 2050.

Role of hydrogen in seasonal storage

While the power supply from hydrogen co-fired generators is limited in terms of total annual power generation, its contribution to balancing the seasonal variability of electricity supply is notable, especially under stringent mitigation scenarios (Supplementary Figs. 13, 14). Figure 3a compares the annual power supply provided by various seasonal storage options. While pumped hydro energy storage (PHES) for seasonal balancing (S-PHES) and compressed air energy storage (CAES) are commonly used and effective seasonal storage options across mitigation scenarios in 2050, the contribution of hydrogen co-firing varies with the stringency of mitigation as well as technological conditions associated with hydrogen. In 2050, the collective power supply from S-PHES and CAES reaches around 0.5 EJ per year with little difference among scenarios, as these technologies are cost-effective options for addressing VRE integration despite their limited potential38. In contrast, the role of hydrogen co-fired generators on seasonal power storage is limited under 1000 Gt–CO2 and higher scenario, even in the H2Opt+ cases. Nevertheless, the power supply from hydrogen co-firing exceeds those of S-PHES and CAES in the 500 and 700 Gt–CO2 scenarios. Hydrogen co-firing also has an impact on battery storage capacity with respect to short-term variability (Supplementary Fig. 15); however, it would not reduce the importance of battery as a short-term storage option, because the difference in battery capacity between the default and NoCOF scenarios is relatively small.

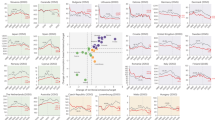

a Electricity supply from seasonal storage technologies. Dotted line denotes those from pumped-hydro electricity storage (PHES) and compressed air electricity storage (CAES). b Curtailment of generated electricity relative to the share of VREs in power generation. Bubble size represents the amount of power generation with hydrogen co-firing.

The role of hydrogen co-firing as seasonal storage is highlighted by the reduced curtailment of excess VRE supply (Fig. 3b). While curtailment of electricity increases across all scenarios as the VRE share of power generation increases, reaching ~10 EJ per year, the amount curtailment is almost halved under the H2Opt, H2Opt+, and LimCCS cases relative to the Default and NoCOF cases, at 3–7 EJ per year.

Impacts on stranded capacity of fossil fuel-fired generators

As the mitigation scenarios require rapid emissions reductions in the near-term, stranded coal capacity in 2030 reaches 1500 GW in the NoCOF cases, equivalent to about two thirds of existing coal capacity (Fig. 4a, b), which is roughly comparable with previous reported values26. Stranded capacity is observed mainly in Asia, especially for coal-fired generators, followed by OECD countries, the Middle East and Africa (Fig. 4c), due to the near-term greater capacity of coal- and gas-fired generators (Supplementary Fig. 18). In 2050, stranded coal capacity falls to ~500 GW, accounting for around one third of total existing capacity, due to the retirement of existing capacity. Stranded capacity is lower for gas-fired generators than coal-fired plants, accounting for around 500 GW and 100 GW in 2030 and 2050, respectively.

a Capacity of fossil fuel-fired generators in the 500 Gt–CO2 scenarios. Results for other scenarios are shown in Supplementary Fig. 16. b Unused power capacities of coal- and gas-fired generators. c Unused coal and gas power capacities by region for the 500 Gt-CO2 scenarios in Asia, Latin America, Middle East and Africa, the Organization for Economic Co-operation and Development (OECD) and Europa (EU), and Reforming Economies. Results for other scenarios are shown in Supplementary Fig. 17.

Hydrogen co-firing can reduce the amount of stranded capacity of coal- and gas-fired generators under some mitigation scenarios, but is not always cost-effective. Stranded coal capacity is reduced by about 200 GW in the H2Opt and H2Opt+ cases, meaning that it is nearly halved in 2050, whereas the impact on gas-fired generators is much smaller. In contrast, stranded coal and gas capacities in the Default and LimCCS cases do not discernably differ from the NoCOF case. This pattern emerges because fossil fuel-fired generators without co-firing, especially gas-fired powerplants, are an effective option for backup power to support VRE integration39. Although hydrogen co-firing can replace this backup capacity and thereby reduce associated emissions, its impact on stranded capacity is limited.

Cost implications of hydrogen application in the power sector

The limited potential of hydrogen co-firing in the global power systems is mainly due to the cost penalty of hydrogen relative to other low-carbon generators. Figure 5a presents a comparison of the levelized cost of electricity (LCOE) across major power generators while considering the effect of carbon prices. Hydrogen co-fired generators generally have much higher LCOE than generators without co-firing under moderate mitigation scenarios because hydrogen is more costly to produce than fossil fuels, at around 30–40 US$ per GJ (Supplementary Fig. 19). Differences in LCOE between generators with and without co-firing narrow under stringent mitigation scenarios. In particular, in the H2Opt and H2Opt+ cases, the LCOE of hydrogen co-fired generators is similar to or lower than the value for generators without co-firing.

a Levelized cost of electricity (LCOE) comparison among different power generation technologies in 2050 with a 10% discount rate, including the effect of the carbon price penalty on CO2 emissions. Integration cost is not included. b LCOE decomposition in 2050 for the 500 and 1000 Gt–CO2 scenarios. Results for other scenarios are shown in Supplementary Fig. 20.

Such variation in LCOE among scenarios derive mainly from heterogeneity in fuel and emissions cost compositions (Fig. 5b). While hydrogen co-firing is generally associated with increases fuel costs and capital costs under the most mitigation scenarios, these changes can be offset by reduced emissions costs associated with higher carbon prices under stringent mitigation scenarios. Specifically, for the H2Opt and H2Opt+ cases, LCOE of hydrogen co-fired generators is similar to that without co-firing due to the fuel cost reduction relative to Default cases. Nevertheless, hydrogen co-firing is generally more costly than other low-carbon generators, such as solar PV, even if the cost of hydrogen falls substantially. Therefore, the contribution of hydrogen co-fired generators to total power generation is limited, and they are employed only as backup capacity for VREs due to their high variable costs40.

Discussion

According to the scenario assessment with various assumptions about mitigation stringency and the technology portfolio, the impact of hydrogen co-firing on prolonging fossil fuel-based power generation is limited. Even in the H2Opt+ scenario in this study, which was designed as a what-if scenario that assumes the most optimistic condition for hydrogen co-firing, the share of hydrogen co-firing accounts for <1% of global total power generation in 2050. The hydrogen co-firing results differ among regions; the share of hydrogen co-firing is larger in OECD countries and Asia because of the greater risks of stranded capacity. Nevertheless, the impact of hydrogen co-firing is limited even in these regions, as the share of hydrogen co-firing reaches 2–3% at most. Although expansion of hydrogen co-fired generator capacity is observed for both coal and gas, the contributions of these changes to total power generation are small, because the hydrogen co-fired generators mainly used as a back-up option for VRE intermittency. It is due to greater cost penalty associated with hydrogen production, relative to the direct use of generated electricity from renewables or energy penalty of CCS implementation. Although hydrogen cost reduction may enhance hydrogen co-firing, the phase-out of fossil fuel-fired generators is a robust trend in the deep decarbonization scenario. These results suggest that the transition risks of fossil fuel-based power infrastructure must be considered when developing climate and energy strategies, even when hydrogen co-firing becomes technically feasible.

Despite the limited impacts on total power generation, the results of this study clarify the potential roles of hydrogen in deep decarbonization. While previous studies have mainly highlighted the role of hydrogen utilization in energy demand sectors that are difficult to decarbonize14,15,23, such as long-distance transport and high-temperature industrial processes, this study demonstrates that low-carbon hydrogen can contribute to power sector decarbonization specifically in the form of flexible generators to account for the seasonal intermittency of VREs. Nevertheless, our results underscore that hydrogen co-fired generators have a minor influence on the power generation mix. This is attributed to the presence of other cost-effective options for integrating VRE, including PHES and CAES, battery storage, and curtailment. Because seasonal electricity storage with hydrogen is a relatively expensive option for VRE integration, the development and deployment of various technological options, rather than depending solely on hydrogen, will be essential.

Although we confirmed the potential roles of hydrogen co-firing in power system decarbonization, an absence of hydrogen co-firing would have no substantial impact, as net zero emissions are accomplished in the NoCOF scenarios without extensive mitigation cost increases. In contrast, limited availability of CCS and biomass substantially increases mitigation costs, as shown in the LimCCS cases. This difference occurs because alternative decarbonization options to hydrogen co-firing exist for the power sector, such as the direct use of VREs and CCS. In contrast to the power sector, hydrogen use in the hard-to-decarbonize sectors of transport and industry could play an essential role14. In this regard, energy strategies to support hydrogen penetration should be based on a holistic approach that prioritizes the effective use of hydrogen.

Some limitation of caveats on the interpretation of our results should be noted. First, as national energy strategies generally involve ensuring energy security as well as economic and environmental aims, countries still maintain fossil fuel reserves today. Because hydrogen and hydrogen-based carriers are relatively easier to store than other low-carbon sources, such as solar- and wind-based electricity, hydrogen use in the power sector can be a practical option for energy security purposes. Second, as this study is based on single model assessment, it would be useful to employ other models with different structures, such as different temporal resolutions. In addition, although this study indicates that extensive wind power generation exceed the power generated by solar PV in 2050, which is consistent with recent scenario assessments using the Global Change Analysis Model (GCAM) and Model for Energy Supply Strategy Alternatives and their General Environmental Impact (MESSAGEix)41,42, expectations of increased solar PV are growing given recent developments. Although the model choice and structure can affect the quantitative result of power generation to some extent, such as the requirement for seasonal storage and solar PV expansion, the findings of a limited role of hydrogen co-firing on decarbonization is likely to be robust, because the cost disadvantage of hydrogen co-firing would not be greatly affected by the choice of model. Third, solar- and wind-based electricity systems would be more vulnerable to extreme conditions, such as extreme weather events and natural disasters. Under such extremes conditions, a backup power supply provided by hydrogen is an attractive option.

Methods

Energy system model

Quantitative analysis of scenarios was conducted using AIM-Technology which is a global bottom-up energy system model14,32. In this model, the operating conditions of several energy technologies, including both energy supply and demand sectors, are determined through linear programming to minimize total energy system cost. The total energy system costs include the annualized initial costs of technologies, energy, operating and emissions costs, which are subject to exogenous energy service demand. Technological parameters including energy efficiency and cost parameters, energy service demands, and several constraints such as primary energy resources are provided to the model as exogenous parameters. Quantitative information about energy demand, energy supply, CO2 emissions and sequestration, energy system costs, and carbon prices are calculated and output from the model. In the energy supply sector, several primary and secondary energy sources, including fossil fuels, nuclear, renewables and hydrogen, are converted to electricity. The power sector uses a dispatch module with a 1 h temporal resolution for representative days. The operating conditions of the power generator are determined under a cost-minimizing framework. Therefore, the capacity factor of flexible generators, including hydrogen co-fired generators, is determined endogenously in this model. In terms of hydrogen generation, hydrogen production from fossil fuels, biomass, and electrolysis is modeled. The mathematical equations, parameter settings and further detailed information have been reported in Oshiro et al.14.

In this study, gas- and coal-fired power generators employing hydrogen co-firing were added to the model. Incremental investment in hydrogen co-firing for both new construction and retrofitting was assumed based on an existing study18 as summarized in Supplementary Table 1. Because a higher hydrogen mix rate requires additional investment for upgrading of the combustion chamber as well as hydrogen tank, incremental costs of hydrogen co-firing varied with hydrogen mix rate. We assumed that both hydrogen and ammonia could be co-fired in both coal- and gas-fired generators. In the context of cost minimization, the hydrogen mix rate was internally determined in the model within 0–100%, with a 100% mix indicating exclusive hydrogen combustion.

In addition, the model was updated to represent retrofitting of existing fossil fuel-fired generators with hydrogen co-firing and carbon capture. In the updated model, a technology retrofit is endogenously determined based on the incremental cost for the retrofit, as summarized in Supplementary Table 1, and on a cost minimizing framework. The annualized incremental cost is calculated based on the remaining lifetime of the upgraded plant. The mathematical equations for technology retrofitting are summarized in the Supplementary Note 1. To quantify stranded assets in the mitigation scenarios, information about existing and planned coal and gas powerplant was obtained from the Global Coal Plant Tracker33 and the Global Gas Plant Tracker34. Planned powerplants included those under construction or in the permitting processes. To incorporate recent trends in solar PV and wind power capacity expansion, the calibration period for solar and wind capacity has been extended to 2027, based on the IEA’s estimates43.

To account for the seasonal variation in electricity demand and supply from VREs, the intra-annual temporal resolution was improved in this model version to include 12 representative days, corresponding to one for each month, and 24 h per day, whereas the previous model used two typical days to represent year, corresponding to summer and winter14. Due to tradeoffs between the model temporal resolution and computational resource requirements44, there have been few presentations of the intra-annual temporal resolution in the IAMs. Recently, some IAMs have modeled the seasonal specific electricity supply and demand profiles explicitly39,45, or soft-linked the IAMs and detailed power system models46,47,48. By contrast, detailed power and energy system models, such as The Integrated MARKAL-EFOM System (TIMES), present a more detailed temporal resolution for four seasons or for each month49,50,51. Although there are several methods to reduce the time resolution for power system analysis52,53, the representative day approach for each season or month offers a clear advantage in assessing seasonal storage effects, as it represents seasonal specific supply and demand conditions. Because the 2–3-season average approach is insufficient to capture the duration curves of solar and wind54, and several studies assessing electricity storage modeled monthly power supply and demand profiles35,36,55, the updated model contains 12 representative days, one for each month, and 24 h per day. In addition, four representative days, when the power output from VRE generators is at its lowest in each quarter of the year, were selected based on historical weather observations between 2006 and 2015, obtained from of the Modern-Era Retrospective analysis for Research and Applications Version 2 (MERRA-2)56,57 to consider the impacts of VRE intermittency due to weather conditions. For each representative day, typical regional monthly electricity demand profiles were determined from the literature58,59. VRE potential and hourly output in each month were also estimated based on the literature60,61. PHES and CAES were introduced as new technologies that can compete with hydrogen co-firing as seasonal storage options. Their technological potentials were assumed based on the literature62,63. Technological parameter assumptions for these technologies are summarized in Supplementary Table 2.

There are various methods for model evaluation of process-based IAMs64. Model intercomparison has been conducted with a number of IAMs1,65, and some of the models have included model documentation66,67. In some studies, historical simulations68,69 and diagnostic studies70,71 have been conducted. For the AIM-Technology model, detailed model documentation, including mathematical equations and parameter assumptions, is available72. Model intercomparisons have been conducted for national studies73,74,75. A recent study using the AIM-Technology-Global model presented a comparison with the IPCC-AR6 scenario32.

Based on the simulation results of energy system models, several indicators were calculated to clarify the potential role of hydrogen co-firing. First, the stranded capacity of powerplants was estimated as unused capacity through a target year, in accordance with previous research76. Second, as a cost indicator for comparison among power generation technologies, LCOE was calculated based on a 10% discount rate.

Scenarios

Multiple scenarios were modeled to assess the condition of hydrogen co-firing under various mitigation pathways and technology portfolios (Supplementary Table 3). The emissions pathways used in this study were based on carbon budgets by 2100 of 500, 700, 1000 and 1400 Gt–CO237. The 500 Gt–CO2 scenario corresponds to the 1.5 °C goal of the Paris Agreement, and energy-related CO2 emissions reach nearly zero in 2050. Emissions reduction begins from 2024 in all mitigation scenarios, aligning with the historical emissions trend up to 202377.

Scenarios were also classified based on technology availability and assumptions to explore the potential of hydrogen co-firing. The Default case was based on the model’s default settings, in which hydrogen co-firing is available, and no additional constraint or parameter changes were imposed. The H2Opt case considered a dramatic cost reduction for hydrogen electrolyzer and solar and wind power, which could enhance hydrogen co-firing by lowering the production cost of hydrogen. The costs of solar and wind power in the H2Opt case were based on the International Renewable Energy Agency (IRENA) estimates78,79. Electrolyzer cost in the H2Opt case was based on the IEA Net-Zero report30. The cost assumptions on these technologies are summarized in Supplementary Fig. 21. Furthermore, additional technological conditions were included to elucidate the possible role of hydrogen utilization in the power sector. In addition, because limited CCS and bioenergy could lead to stringent reductions of residual emissions and associated increases in carbon prices14, the LimCCS scenario was prepared. In this scenario, geological storage of captured CO2 and bioenergy supply are limited to 4 Gt-CO2 per year and 100 EJ per year, respectively, based on the literature6. In the LimCCS case, electrolyzer and renewable energy costs are the same as in the H2Opt case. The H2Opt+ scenario was designed as a what-if scenario assuming the most optimistic conditions for hydrogen co-firing. In addition to the conditions imposed in the H2Opt case, this scenario includes higher battery cost assumptions and no new construction of seasonal storage (CAES an PHES). Also, the same limitations on CCS and bioenergy that occur in the LimCCS case were imposed in the H2Opt+ case. The NoCOF scenario was assessed as a reference scenario for comparison with other scenarios, wherein hydrogen co-firing of fossil fuel-fired powerplants is not available. In this scenario, the technology cost assumptions are the same as in the Default scenario. In these main scenarios, the socioeconomic conditions were equivalent to the assumptions of Shared Socioeconomic Pathway (SSP) 280.

In addition to these main scenarios, sensitivity scenarios were analyzed to evaluate several uncertainties associated with socio-economic conditions. Although the main scenarios in this study used SSP2 assumptions, SSP1 and SSP3 assumptions were also assessed as sensitivity cases for the 500 H2Opt because the recent IAM-based studies generally included socio-economic uncertainties among SSP 1–342,81. The results of these sensitivity analyses are summarized in the Supplementary Figures.

IPCC AR6 scenario data

For comparison between our results and the IPCC AR6 scenario data, the World v.1.1 dataset of the AR6 scenario data was used82. The categories C1, C2, and C3 were used for comparison, as they were essentially consistent with the range of climate scenarios of this study. C1 limits the temperature increase to 1.5 °C with no or limited overshoot with 50% likelihood. C2 limits 1.5 °C in 2100 with 50% likelihood after a high overshoot. C3 limits peak warming to 2 °C in this century with 67% likelihood.

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

The scenario data generated in this study have been deposited in the Zenodo repository under accession code https://doi.org/10.5281/zenodo.10457307.

Code availability

The source code used for scenario data analysis and figure production is provided in the GitHub repository (https://github.com/kenoshiro/H2cofire; https://doi.org/10.5281/zenodo.10602980). The source code of the AIM-Technology model is available at the GitHub repository (https://github.com/KUAtmos/AIMTechnology_core; https://doi.org/10.5281/zenodo.8401421).

References

Krey, V., Luderer, G., Clarke, L. & Kriegler, E. Getting from here to there—energy technology transformation pathways in the EMF27 scenarios. Clim. Change 123, 369–382 (2014).

Rogelj, J. et al. Energy system transformations for limiting end-of-century warming to below 1.5 °C. Nat. Clim. Change 5, 519–527 (2015).

Bistline, J. E. T. & Blanford, G. J. The role of the power sector in net-zero energy systems. Energy Clim. Change 2, 100045 (2021).

IRENA. Renewable Power Generation Costs in 2021. https://www.irena.org/publications/2022/Jul/Renewable-Power-Generation-Costs-in-2021 (2022).

Creutzig, F., Agoston, P., Goldschmidt, J. C., Luderer, G., Nemet, G. & Pietzcker, R. C. The underestimated potential of solar energy to mitigate climate change. Nat. Energy 2, 17140 (2017).

Luderer, G. et al. Impact of declining renewable energy costs on electrification in low-emission scenarios. Nat. Energy 7, 32–42 (2022).

Riahi, K. et al. Mitigation pathways compatible with long-term goals. In: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change (eds Shukla P. R. et al.) 295–408 (Cambridge University Press, 2022).

Edwards, M. R. et al. Quantifying the regional stranded asset risks from new coal plants under 1.5 °C. Environ. Res. Lett. 17, 024029 (2022).

Fofrich, R. et al. Early retirement of power plants in climate mitigation scenarios. Environ. Res. Lett. 15, 094064 (2020).

Johnson, N., Krey, V., McCollum, D. L., Rao, S., Riahi, K. & Rogelj, J. Stranded on a low-carbon planet: implications of climate policy for the phase-out of coal-based power plants. Technol. Forecast. Soc. Change 90, 89–102 (2015).

Clarke L. et al. Energy systems. In Climate Change 2022: Mitigation of Climate Change (eds Shukla P. R. et al.) 511–598 (Cambridge University Press, 2022).

Bui, M. et al. Carbon capture and storage (CCS): the way forward. Energy Environ. Sci. 11, 1062–1176 (2018).

Rubin, E. S., Davison, J. E. & Herzog, H. J. The cost of CO2 capture and storage. Int. J. Greenh. Gas. Control 40, 378–400 (2015).

Oshiro, K. & Fujimori, S. Role of hydrogen-based energy carriers as an alternative option to reduce residual emissions associated with mid-century decarbonization goals. Appl. Energy 313, 118803 (2022).

Odenweller, A., Ueckerdt, F., Nemet, G. F., Jensterle, M. & Luderer, G. Probabilistic feasibility space of scaling up green hydrogen supply. Nat. Energy 7, 854–865 (2022).

van Ruijven, B., van Vuuren, D. P. & de Vries, B. The potential role of hydrogen in energy systems with and without climate policy. Int. J. Hydrog. Energy 32, 1655–1672 (2007).

Davis, S. J. et al. Net-zero emissions energy systems. Science 360, eaas9793 (2018).

Öberg, S., Odenberger, M. & Johnsson, F. Exploring the competitiveness of hydrogen-fueled gas turbines in future energy systems. Int. J. Hydrog. Energy 47, 624–644 (2022).

IEA. The Future of Hydrogen Seizing Today’s Opportunities. https://www.iea.org/reports/the-future-of-hydrogen (2019).

Gabrielli, P., Poluzzi, A., Kramer, G. J., Spiers, C., Mazzotti, M. & Gazzani, M. Seasonal energy storage for zero-emissions multi-energy systems via underground hydrogen storage. Renew. Sustain. Energy Rev. 121, 109629 (2020).

Dowling, J. A. et al. Role of long-duration energy storage in variable renewable electricity systems. Joule 4, 1907–1928 (2020).

Bui, M., Sunny, N. & Mac Dowell, N. The prospects of flexible natural gas-fired CCGT within a green taxonomy. iScience 26, 107382 (2023).

Rodrigues, R. et al. Narrative-driven alternative roads to achieve mid-century CO2 net neutrality in Europe. Energy 239, 121908 (2022).

Browning, M. et al. Net-zero CO2 by 2050 scenarios for the United States in the energy modeling forum 37 study. Energy Clim. Change 4, 100104 (2023).

IEA. Tracking Clean Energy Progress 2023. https://www.iea.org/reports/tracking-clean-energy-progress-2023 (2023).

Cui, R. Y. et al. Quantifying operational lifetimes for coal power plants under the Paris goals. Nat. Commun. 10, 4759 (2019).

Jakob, M. et al. The future of coal in a carbon-constrained climate. Nat. Clim. Change 10, 704–707 (2020).

Fan, J.-L. et al. Co-firing plants with retrofitted carbon capture and storage for power-sector emissions mitigation. Nat. Clim. Change 13, 807–815 (2023).

Lu, Y., Cohen, F., Smith, S. M. & Pfeiffer, A. Plant conversions and abatement technologies cannot prevent stranding of power plant assets in 2 °C scenarios. Nat. Commun. 13, 806 (2022).

IEA. Net Zero by 2050 A Roadmap for the Global Energy Sector. https://www.iea.org/reports/net-zero-by-2050 (2021).

G7. G7 Climate, Energy and Environment Ministers’ Communiqué. https://www.env.go.jp/content/000127828.pdf (2023).

Oshiro, K., Fujimori, S., Hasegawa, T., Asayama, S., Shiraki, H. & Takahashi, K. Alternative, but expensive, energy transition scenario featuring carbon capture and utilization can preserve existing energy demand technologies. One Earth 6, 872–883 (2023).

GEM. Global Coal Plant Tracker (GEM, 2022).

GEM. Global Gas Plant Tracker (GEM, 2022).

Sánchez-Pérez, P. A., Staadecker, M., Szinai, J., Kurtz, S. & Hidalgo-Gonzalez, P. Effect of modeled time horizon on quantifying the need for long-duration storage. Appl. Energy 317, 119022 (2022).

He, G., Lin, J., Sifuentes, F., Liu, X., Abhyankar, N. & Phadke, A. Rapid cost decrease of renewables and storage accelerates the decarbonization of China’s power system. Nat. Commun. 11, 2486 (2020).

Fujimori, S., Oshiro, K., Hasegawa, T., Takakura, J. & Ueda, K. Climate change mitigation costs reduction caused by socioeconomic-technological transitions. npj. Clim. Action 2, 9 (2023).

Schmidt, O., Melchior, S., Hawkes, A. & Staffell, I. Projecting the future levelized cost of electricity storage technologies. Joule 3, 81–100 (2019).

Pietzcker, R. C. et al. System integration of wind and solar power in integrated assessment models: a cross-model evaluation of new approaches. Energy Econ. 64, 583–599 (2017).

Jenkins, J. D., Luke, M. & Thernstrom, S. Getting to zero carbon emissions in the electric power sector. Joule 2, 2498–2510 (2018).

Iyer, G. et al. Ratcheting of climate pledges needed to limit peak global warming. Nat. Clim. Change 12, 1129–1135 (2022).

Guo, F. et al. Implications of intercontinental renewable electricity trade for energy systems and emissions. Nat. Energy 7, 1144–1156 (2022).

IEA. Renewables 2022. https://www.iea.org/reports/renewables-2022 (2022).

Frew, B. A. & Jacobson, M. Z. Temporal and spatial tradeoffs in power system modeling with assumptions about storage: an application of the POWER model. Energy 117, 198–213 (2016).

Després, J., Mima, S., Kitous, A., Criqui, P., Hadjsaid, N. & Noirot, I. Storage as a flexibility option in power systems with high shares of variable renewable energy sources: a POLES-based analysis. Energy Econ. 64, 638–650 (2017).

Brinkerink, M., Zakeri, B., Huppmann, D., Glynn, J., Ó Gallachóir, B. & Deane, P. Assessing global climate change mitigation scenarios from a power system perspective using a novel multi-model framework. Environ. Model. Softw. 150, 105336 (2022).

Gong, C. C. et al. Bidirectional coupling of the long-term integrated assessment model regional model of investments and development (REMIND) v3.0.0 with the hourly power sector model dispatch and investment evaluation tool with endogenous renewables (DIETER) v1.0.2. Geosci. Model Dev. 16, 4977–5033 (2023).

Fujimori, S., Oshiro, K., Shiraki, H. & Hasegawa, T. Energy transformation cost for the Japanese mid-century strategy. Nat. Commun. 10, 4737 (2019).

Deane, J. P., Chiodi, A., Gargiulo, M. & Ó Gallachóir, B. P. Soft-linking of a power systems model to an energy systems model. Energy 42, 303–312 (2012).

Johnston, J., Henriquez-Auba, R., Maluenda, B. & Fripp, M. Switch 2.0: a modern platform for planning high-renewable power systems. SoftwareX 10, 100251 (2019).

Gaur, A. S., Das, P., Jain, A., Bhakar, R. & Mathur, J. Long-term energy system planning considering short-term operational constraints. Energy Strategy Rev. 26, 100383 (2019).

Bistline, J. E. T. The importance of temporal resolution in modeling deep decarbonization of the electric power sector. Environ. Res. Lett. 16, 084005 (2021).

Pfenninger, S. Dealing with multiple decades of hourly wind and PV time series in energy models: a comparison of methods to reduce time resolution and the planning implications of inter-annual variability. Appl. Energy 197, 1–13 (2017).

Blanford, G. J., Merrick, J. H., Bistline, J. E. & Young D. T. Simulating annual variation in load, wind, and solar by representative hour selection. Energy J. 39, 189–212 (2018).

Mileva, A., Johnston, J., Nelson, J. H. & Kammen, D. M. Power system balancing for deep decarbonization of the electricity sector. Appl. Energy 162, 1001–1009 (2016).

Global Modeling and Assimilation Office (GMAO). MERRA-2 tavg1_2d_rad_Nx: 2d,1-Hourly,Time-Averaged,Single-Level, Assimilation,Radiation Diagnostics V5.12.4. https://doi.org/10.5067/Q9QMY5PBNV1T (2015).

Global Modeling and Assimilation Office (GMAO). MERRA-2 tavg1_2d_slv_Nx: 2d,1-Hourly,Time-averaged,Single-level,Assimilation,Single-level Diagnostics V5.12.4. https://doi.org/10.5067/RKPHT8KC1Y1T (2015).

Brinkerink M., Deane P. PLEXOS-World 2015 V6 edn (Harvard Dataverse, 2020).

Castillo, V. Z., Boer, H.-S. D., Muñoz, R. M., Gernaat, D. E. H. J., Benders, R. & van Vuuren, D. Future global electricity demand load curves. Energy 258, 124741 (2022).

Pfenninger, S. & Staffell, I. Long-term patterns of European PV output using 30 years of validated hourly reanalysis and satellite data. Energy 114, 1251–1265 (2016).

Staffell, I. & Pfenninger, S. Using bias-corrected reanalysis to simulate current and future wind power output. Energy 114, 1224–1239 (2016).

Stocks, M., Stocks, R., Lu, B., Cheng, C. & Blakers, A. Global atlas of closed-loop pumped hydro energy storage. Joule 5, 270–284 (2021).

Aghahosseini, A. & Breyer, C. Assessment of geological resource potential for compressed air energy storage in global electricity supply. Energy Convers. Manag. 169, 161–173 (2018).

Wilson, C. et al. Evaluating process-based integrated assessment models of climate change mitigation. Clim.Change 166, 3 (2021).

Riahi, K. et al. Cost and attainability of meeting stringent climate targets without overshoot. Nat. Clim. Change 11, 1063–1069 (2021).

Calvin, K. et al. GCAM v5.1: representing the linkages between energy, water, land, climate and economic systems. Geosci. Model Dev. 12, 677–698 (2019).

Baumstark, L. et al. REMIND2.1: transformation and innovation dynamics of the energy-economic system within climate and sustainability limits. Geosci. Model Dev. 14, 6571–6603 (2021).

Fujimori, S., Dai, H., Masui, T. & Matsuoka, Y. Global energy model hindcasting. Energy 114, 293–301 (2016).

Snyder, A. C., Link, R. P. & Calvin, K. V. Evaluation of integrated assessment model hindcast experiments: a case study of the GCAM 3.0 land use module. Geosci. Model Dev. 10, 4307–4319 (2017).

Kriegler, E. et al. Diagnostic indicators for integrated assessment models of climate policy. Technol. Forecast. Soc. Change 90, 45–61 (2015).

Harmsen, M. et al. Integrated assessment model diagnostics: key indicators and model evolution. Environ. Res. Lett. 16, 054046 (2021).

Oshiro K. AIM-Technology Model. https://kenoshiro.github.io/AIM-Technology-doc/ (2021).

Oshiro, K. et al. Mid-century emission pathways in Japan associated with the global 2 °C goal: national and global models’ assessments based on carbon budgets. Clim. Change 162, 1913–1927 (2019).

Krey, V. et al. Looking under the hood: a comparison of techno-economic assumptions across national and global integrated assessment models. Energy 172, 1254–1267 (2019).

Sugiyama, M. et al. EMF 35 JMIP study for Japan’s long-term climate and energy policy: scenario designs and key findings. Sustain. Sci. 16, 355–374 (2021).

Oshiro, K. & Fujimori, S. Stranded investment associated with rapid energy system changes under the mid-century strategy in Japan. Sustain. Sci. 16, 477–487 (2020).

Friedlingstein, P. et al. Global carbon budget 2023. Earth Syst. Sci. Data 15, 5301–5369 (2023).

IRENA. Future of Solar Photovoltaic: Deployment, Investment, Technology, Grid Integration and Socio-Economic Aspects (International Renewable Energy Agency, 2019).

IRENA. Future of Wind: Deployment, Investment, Technology, Grid Integration and Socio-Economic Aspects (International Renewable Energy Agency, 2019).

Riahi, K. et al. The shared socioeconomic pathways and their energy, land use and greenhouse gas emissions implications: an overview. Glob. Environ. Change 42, 153–168 (2017).

Gambhir, A. et al. Near-term transition and longer-term physical climate risks of greenhouse gas emissions pathways. Nat. Clim. Change 12, 88–96 (2022).

Byers, E. et al. AR6 Scenarios Database Hosted by IIASA. https://data.ece.iiasa.ac.at/ar6/#/login?redirect=%2Fworkspaces (2022).

Acknowledgements

K.O. and S.F. acknowledge support from the Environment Research and Technology Development Fund (JPMEERF20211001) of the Environmental Restoration and Conservation Agency provided by the Ministry of Environment of Japan, JSPS KAKENHI Grant Number JP23K04087, and the Sumitomo Electric Industries Group CSR Foundation.

Author information

Authors and Affiliations

Contributions

K.O. designed the research. K.O. and S.F. contributed to scenario design and interpretation of the results. K.O. developed the model, conducted the analysis, created the figures, and wrote the first draft of the paper. K.O. and S.F. contributed to the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Communications thanks the anonymous, reviewer(s) for their contribution to the peer review of this work. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Oshiro, K., Fujimori, S. Limited impact of hydrogen co-firing on prolonging fossil-based power generation under low emissions scenarios. Nat Commun 15, 1778 (2024). https://doi.org/10.1038/s41467-024-46101-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s41467-024-46101-5

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.