Abstract

Corporate social responsibility (CSR) could be an effective risk-alleviating tool for companies. However, an important issue is whether CSR plays a risk-alleviating role in large negative shocks such as the COVID-19 pandemic. This study investigated the impact of corporate social responsibility on stock performance in China during the COVID-19 pandemic, focusing on the differing effects of strategic and responsive CSR. By analysing daily data on newly confirmed COVID-19 cases and the stock performance of A-share listed companies during the lockdown period in 2020, we find that CSR can significantly mitigate the negative effects of the pandemic on stock returns and recovery. Specifically, responsive CSR has a significant short-term moderating effect, whereas strategic CSR has a significant long-term moderating effect. The moderating effects of CSR are more pronounced among non-state-owned firms, firms with lower financial leverage, and large companies. These findings suggest that companies can reduce short- and long-term risks by strategically using responsive and strategic CSR in response to negative shocks in global economies.

Similar content being viewed by others

Introduction

At the beginning of 2020, the COVID-19 outbreak triggered enormous and heterogeneous shocks in the global economy. This has resulted in considerable uncertainty and substantial disruptions to capital markets (Ding et al. 2021; Yi et al. 2021), especially stock markets (Boubaker et al. 2022; Buertey et al. 2024; Jin et al. 2023; Khanchel et al. 2024; Tian et al. 2022). Due to its cause, scope, and severity, the consequences motivate research on the factors shaping firms’ responses to COVID-19. Corporate social responsibility (CSR), as an important risk mitigation tool, has been proven that it can significantly improve corporate performance (Deng et al. 2022; Eccles et al. 2012; Khan et al. 2023; Michelon et al. 2013; Úbeda-García et al. 2021). However, few studies have examined how CSR affects corporate stock performance (CSP) during the COVID-19 pandemic and the effects of heterogeneous CSR on CSP. This study aims to provide an innovative perspective on the effects of overall and specific CSRs, namely strategic and responsive CSR, on CSP during the COVID-19 pandemic in China.

Due to the pandemic and public health concerns, capital markets are at systematic risk, which can affect corporate financial performance (CFP) (Ferriani and Natoli, 2021; Zhai et al. 2022). From January to May 2020, the Standard & Poor’s (S&P) 500 Index witnessed a 34% drop from its peak to its trough. Similarly, the stock markets in Brazil, Hong Kong, Italy, and Japan experienced remarkable declines of 46, 25, 41, and 31%, respectively. In addition, the volatility of individual stock returns during this period was even greater (Ding et al. 2021; Wang, 2011). Studies indicate that CSR is essential in alleviating the negative impacts of emergency events on firms (Shiu and Yang, 2017; Yang et al. 2019; Choi and Jung, 2022). According to Havlinova and Kukacka (2023), the fundamental principle of CSR aims to maximise corporate shareholders’ profits and improve social well-being through responsible corporate activities that go beyond business purposes and legal requirements. This CSR belief is based on the idea that companies that incorporate business ethics into their daily operations can positively impact societal development and the environment.

As a risk-management tool, CSR can positively influence stakeholder groups, protect firms from negative publicity, positively shape customer identification, and indirectly enhance CSP. Specifically, CSR alleviates the negative effects of COVID-19 on CSP through three channels: reputation effects (Archimi et al. 2018; Minor and Morgan 2011; Park et al. 2014), immunisation effects (Carroll et al. 2012; Epstein et al. 2010; Liang and Renneboog 2017), and sustainable development effects (Chang et al. 2022; Gao and Kil-Soek Han 2022; Jeong et al. 2018; Mithani, 2017; Ratajczak and Szutowski 2016). For example, Khan et al. (2023) found that corporate donations, as an important context for CSR, help build a good image and reputation for all parties involved, such as stakeholders and customers, to improve CSP. While the overwhelming literature supports the significant effects of CSR on CSP, it remains unclear whether CSR can fulfil the same role in the particular context of the COVID-19 pandemic, especially concerning specific dimensions of CSR, such as strategic CSR and responsive CSR and their impact on CSP during different periods.

However, research on the COVID-19 crisis has yet to examine the prevalence of CSR activities. Moreover, existing studies have not explored the impact of these activities (responsive versus strategic) on stock returns or how CSR alleviates the negative effects of COVID-19 on CSP. The relationship between CSR and CSP is more complicated than suggested in many previous studies. This complexity underlies our study, which extends the scope of existing research on the relationship between CSR and CSP, particularly during the COVID-19 pandemic. This study fills this research gap by investigating the role of CSR in the context of the COVID-19 impact on CSP in the Chinese stock market.

Employing daily data on newly confirmed COVID-19 cases and the CSP of A-share listed companies during the 2020 lockdown period in China, we constructed regressions with the interaction term of CSR and COVID-19 to illustrate the moderating effects of CSR on CSP during the COVID-19 pandemic. Empirically, we found that the COVID-19 outbreak had a significant negative impact on CSP; however, overall, CSR mitigated the inhibitory effects of COVID-19. Generally, responsive CSR significantly mitigates the negative influence of COVID-19 on CSP in the short term, whereas strategic CSR mitigates this negative influence in the long term.

This study makes three important contributions to the literature. First, we extend research on the factors influencing the relationship between public health shocks and CSP. Existing studies illustrate the direct effect of public health shocks on CSP (Donadelli et al. 2017; Schell et al. 2020; Zhang et al. 2021). This study investigates the significant moderating effect of heterogeneous CSR on this relationship and explores the influence mechanism of CSR on the relationship between public health events and CSP. Second, we examine the impact of CSR on CSP from the new perspective of heterogeneous CSR, whereas existing studies have only examined the effect of overall CSR on CSP. This study explores the risk management functions of different types of CSR and deepens the literature on CSR and CSP (Benabou and Tirole, 2010; Oikonomou et al. 2012; Lins et al. 2017; Krueger et al. 2021). Third, we examine the heterogeneous effects of responsive and strategic CSR on CSP among different types of companies during the COVID-19 pandemic and find that strategic CSR has a more intense and profound impact on CSP in the post-epidemic era.

The remainder of the paper is structured as follows: Section 2 reviews the literature and presents some theoretical hypotheses. Section 3 introduces the data, variables, and methodology. Section 4 presents the empirical results and a heterogeneous analysis. Finally, Section 5 presents the main findings and their implications.

Literature review and hypothesis development

The Roles of CSR in the effect of COVID-19 on corporate stock performance

Studies have shown that public health crises or pandemics pose a heavy economic burden on financial markets, often leading to stock market crashes (Donadelli et al. 2017; Schell et al. 2020). COVID-19 has led to significant global declines in stock markets, with high levels of market volatility (Zhang et al. 2021). Pandemic-related news, such as lockdowns and case counts, influences investor sentiment and leads to abrupt market movements (Zaremba and Czapkiewicz 2020; Zhou and Zhou 2022). Overall, the COVID-19 pandemic has had a significant negative impact on stock markets. For instance, Baker et al. (2020) showed that 18 markets fluctuated by 2.5% or more daily in the 22 trading days following the outbreak of COVID-19 on 24th February 2020. Facing a pandemic such as COVID-19, companies need to react to shocks and avoid stock price fluctuation risk. Therefore, many scholars have focused on the role of CSR in CSP (Benabou and Tirole 2010; Oikonomou et al. 2012; Lins et al. 2017; Krueger et al. 2021).

CSR refers to a company’s efforts to contribute to society beyond its financial interests. This concept has gained significant importance in business, with companies recognising the benefits of incorporating social and environmental considerations into their practices. CSR has evolved over the years and is now used as a risk management tool, allowing companies to identify potential risks and opportunities and take proactive steps to mitigate risks and seize opportunities. Implementing CSR practices can help companies reduce financial, operational, environmental, and social risks. Companies engage in CSR for a variety of reasons, driven by both ethical considerations and strategic business motives, such as ethical and moral obligations (Carroll 1999), reputation and brand building (Sen and Bhattacharya 2001), employee engagement and retention (Turker 2009), risk management and stakeholder relations (Tokoro 2007), competitive advantage (Porter and Kramer 2006), innovation and business opportunities (Hart and Milstein 2003), investor relations and access to capital (Eccles et al. 2012), regulatory compliance and license to operate (Bansal and Roth 2000), and so on. Therefore, if socially responsible firms commit to a high standard of transparency and engage in less bad news hoarding, they have a lower stock crash risk. However, if managers engage in CSR to cover up bad news and divert shareholder scrutiny, CSR is associated with a higher stock crash risk (Kim et al. 2014).

Recent CSR studies have highlighted the benefits of CSR as an insurance mechanism for risk management. Kim et al. (2021) show that by using option-implied volatility, CSR can serve as an effective insurance mechanism for firms. Similarly, Carroll and Shabana (2010) suggested that CSR can be a powerful tool for risk management by helping companies identify and mitigate potential risks. Chollet and Sandwidi (2018) demonstrate that good CSR performance reduces financial risks and reinforces a company’s commitment to good governance and environmental practices. In addition, Chen et al. (2018) find that firms can use CSR engagement to adjust their business strategies and reduce operational uncertainty. Finally, Karwowski and Raulinajtys-Grzybek (2021) confirmed that companies can use CSR actions to mitigate environmental, social, governance (ESG), and reputational risks. In addition, Ding et al. (2021) assessed how pre-existing levels of CSR activities shaped stock prices during the pandemic and found that CSR enhanced the resiliency of stock prices to COVID-19 by strengthening loyalty and bonds among key stakeholders. Zhai et al. (2022) found that firms with strong engagement in CSR activities, such as corporate donations, before the pandemic experienced fewer negative impacts than those with no or weak CSR activities, indicating that CSR can function as insurance and alleviate the negative effects of COVID-19 on stock performance. However, whether CSR can mitigate the negative shock of public health events such as COVID-19 is still unclear.

The COVID-19 pandemic underscores the critical role of CSR in cushioning firms against market turbulence. Through the channels of reputation, immunisation, and sustainable development effects, CSR emerges as a conduit for risk management and a strategic asset in enhancing CSP amidst such crises. First, in the face of COVID-19, companies with robust CSR commitments leverage their reputational capital to fortify stakeholder trust and loyalty, which is vital during uncertain times. A reputation built on ethical integrity, environmental stewardship, and community welfare translates into tangible financial valuations, with investors often attributing premiums to the stocks of socially responsible firms. Empirical evidence corroborates this finding, demonstrating a significant positive link between comprehensive CSR endeavours and stock market resilience (Archimi et al. 2018; Minor and Morgan 2011; Park et al. 2014), an attribute particularly invaluable during pandemic-induced market fluctuations.

Second, the immunisation effect suggests that companies with strong CSR practices can better weather negative events, such as environmental disasters or public emergencies, without experiencing significant declines in stock prices. This is because investors perceive these companies as better prepared to manage risks and mitigate negative impacts, which can help insulate them from market volatility. The immunisation effect is particularly noticeable in industries sensitive to environmental and social issues. For instance, in sectors such as energy and manufacturing, companies with strong environmental policies may face fewer regulatory penalties and public backlash, thereby protecting their stock values from sudden drops (Carroll et al. 2012; Epstein et al. 2010; Liang and Renneboog 2017).

Third, CSR-oriented firms are adept at aligning with sustainable development trajectories and seizing long-term growth vistas that have accelerated the COVID-19 pandemic in many ways. The shift towards sustainability, whether through low-carbon initiatives or resilient supply chains, presents fertile ground for value creation, driving investor confidence and stock performance over time. The innovation and forward-thinking inherent in sustainable practices position these firms advantageously in the market, a factor increasingly recognised by investors in the current context (Chang et al. 2022; Gao and Kil-Soek Han 2022; Jeong et al. 2018; Mithani 2017; Ratajczak and Szutowski 2016).

In summary, the interplay between CSR and CSP, particularly during COVID-19, is intricate and multifaceted. While reputation, immunisation, and sustainable development collectively underscore CSR’s pivotal role of CSR in stock performance resilience, it is imperative to acknowledge the variability of these impacts across industries and regions. Thus, a discerning analysis is essential to fully comprehend and leverage CSR’s potential of CSR to navigate the economic repercussions of the pandemic. Based on the above, we propose the following hypothesis:

H1: General CSR activities can mitigate the negative impacts of COVID-19 on CSP.

Responsive CSR and strategic CSR

CSR is an important risk management tool that profoundly impacts all aspects of corporate performance. However, there are different types of CSR, and as research has intensified, studies have begun to focus on how these types can affect corporate performance. The earliest classification of CSR into responsive CSR and strategic CSR was introduced by Carroll (1979) and was later renamed accommodating and proactive CSR. From an environmental perspective, Henriques and Sadorsky (1999) suggested that responsive CSR involves complying with environmental standards, whereas strategic CSR involves striving to be environmental leaders. Carroll (2004) expanded the idea of responsive CSR, which he saw as related to economic, legal, ethical, and philanthropic responsibilities. Luo (2006) provided even more extensive descriptions, defining responsive CSR as related to ethical codes, organisational credibility, and philanthropic contributions, and strategic CSR as related to resource accommodation, collaboration and knowledge transfer, local partnerships, and participation. Existing studies have focused on the overall effect of CSR on CSP. For instance, Tsai and Wu (2022) explore the relationship between CSR and stock performance and find that the financial returns generated by various CSR dimensions differ during a financial crisis. Havlinova and Kukacka (2023) analyse the impact of CSR on stock performance after the global financial crisis and suggest that companies should strategically implement socially responsible initiatives to boost stock prices through the CSR channel. However, no studies have examined the effects of distinct CSR categories on CSP, such as responsive and strategic CSR.

Porter and Kramer (2006, 2011) proposed the most recent and popular distinction between responsive and strategic CSR. They argue that responsive CSR is a short-term, compliance-oriented concept based on traditional social responsibility, involving corporate citizenship and reducing harm to society. In contrast, strategic CSR involves responsible activities that are part of the business strategy, including investing in long-term innovative resources, focusing on social and economic value creation, and strengthening competitive advantages by solving social problems (Rhee et al. 2021). According to Porter and Kramer (2011), strategic CSR has three key features: motivation, relationships, and investment. As Bohas and Poussing (2016) suggest, strategic CSR is the most comprehensive implementation of CSR with the highest level of commitment, as opposed to limited implementation with the lowest level of commitment for responsive CSR. However, CSR heterogeneity is regarded as a “black box” in the literature, and as a result, there is limited research on how different CSR activities affect CSP. Based on the literature, the impact of responsive CSR on CSP is short-term and temporary, whereas the impact of strategic CSR is primarily long-term and sustained (Bansal et al. 2015; Sakunasingha et al. 2018; Rameshwar et al. 2020).

In the context of the COVID-19 pandemic, the interplay between CSR and CSP has garnered considerable interest. The pandemic has underscored the importance of CSR, particularly responsive (actions taken in direct response to societal needs) and strategic CSR (aligned with a company’s business strategies). Previous research indicates that firms that quickly engage in responsive CSR activities, such as donating toward COVID-19 relief efforts or providing resources to affected communities, see an immediate positive reaction in their stock performance. This is attributed to the “halo effect,” in which companies perceived as doing good gain a more favourable view from investors and consumers alike (Khan et al. 2023; Zhai et al. 2022). In addition, studies suggest that responsive CSR activities help firms mitigate the risks associated with a pandemic. Firms actively involved in CSR were often viewed as more resilient, potentially cushioning their stock prices from the severe downturns seen in companies less engaged in CSR (Deng et al. 2022; Khan et al. 2023; Kim et al. 2021; Úbeda-García et al. 2021). Furthermore, the literature highlights that responsive CSR leads to enhanced loyalty and support from stakeholders, including customers, employees, and suppliers, which positively impacts stock performance. This support was crucial during the pandemic when companies faced unprecedented operational and supply chain challenges (Archimi et al. 2018; Boubaker et al. 2022; Turker, 2009).

Strategic CSR, ingrained in a company’s core business strategy, contributes to long-term value creation. Firms with a strong foundation in strategic CSR before the pandemic were better positioned to navigate the crisis, reflecting more stable and sometimes increasing stock price trends (Bansal et al. 2015; Michelon et al. 2013; Rameshwar et al. 2020). In addition, investors tend to favour companies with robust strategic CSR policies and view them as better long-term investments. During the COVID-19 pandemic, these companies are often seen as having more adaptable and resilient traits that investors highly value during uncertain times, leading to more stable or positive stock price movements (Bohas and Poussing 2016; Deng et al. 2022; Yang et al. 2021). Moreover, the literature indicates that companies focusing on strategic CSR are more innovative and competitive during the pandemic. Their commitment to sustainability and ethical practices drove them to find new solutions to pandemic-related challenges, often leading to operational efficiency and new market opportunities and positively influencing their stock performance (Havlinova and Kukacka 2023; Rhee et al. 2021).

Both responsive and strategic CSR played pivotal roles in COVID-19, influencing CSP. While responsive CSR offers immediate benefits and risk mitigation, strategic CSR provides long-term value and stability. Companies that effectively integrated both approaches in their response to the pandemic were generally perceived favourably by the market, as reflected in their stock performance. According to the CSR attribute distinction theory, our main hypotheses are as follows:

H2: In the short term, responsive CSR significantly impacts stock performance, as indicated by stock returns.

H3: In the long term, strategic CSR significantly impacts stock performance, as indicated by the recovery of stock returns.

Methods

Data

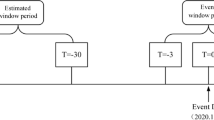

The sample of this study consists of four data sources: One is the data on COVID-19 cases retrieved from the National Health Commission from 3rd February 2020 to 10th April 2020. Because Wuhan was locked down on 23rd January 2020, 3rd February 2020 was the first trading day after the holidays of the Chinese Spring Festival. Wuhan was unlocked on 8th April 2020, and China’s economy gradually recovered from the pandemic. Therefore, our sample’s data on pandemic cases lasted 10 weeks, from 3rd February 2020 (the sixth week of 2020) to 10th April 2020 (the fifteenth week of 2020). The other includes data on stock prices and corporate characteristics, including corporate financial characteristics, which are all from the China Stock Market & Accounting Research Database (CSMAR), a famous and popular database covering most of the data on the Chinese stock market and public companies. The other is the data on corporate donations during COVID-19 in China from 3rd February 2020 to 10th April 2020, which was released on the China Association of Public Companies website. The fourth source of data is from the Rankings CSR Ratings (RKS) database, which is an authoritative third-party rating agency for corporate social responsibility in China committed to providing objective and scientific corporate responsibility rating information for responsible investors, responsible consumers, and the public; it is also popularly used by many scholars to investigate China’s corporate socially responsible behaviour.

Our original sample covers China’s listed companies on the Shanghai and Shenzhen Stock Exchanges in 2020. Considering the different characteristics of financial and non-financial companies, we deleted companies in the financial industry and then covered the remaining 18 industries in major categories. Considering there are big differences among manufacturing industries, we also classified the manufacturing industry into 31 sub-industries by two-digit middle-class codes based on the Guidelines for the Industry Classification of Listed Companies issued by the China Securities Regulatory Commission, so there are 48 industries (including sub-industries for manufacturing companies) with 3680 companies in our sample. Furthermore, we deleted sample data with the main variables omitted, resulting in 3572 companies. Finally, we matched the data from the above four sources and winsorised the data at 1% on both sides, leaving 33215 firm-week observations in the basic regression. In addition, to investigate corporate recovery from COVID-19, we also extend our data period to 2019 and the second half of 2020; due to the observation loss in calculating the measure of stock return recovery, we have 33165 observations for the stock return recovery regression.

Model

Our basic model specifications are as follows:

Where i, j, and t denote firm, industry, and week respectively. The dependent variable, \({{WkRtn} \% }_{i,t}\), is the Adjusted weekly stock return of firm i from the last trading day in week t-1 to the last trading day in week t. \({{RtnRecovery}}_{i}\) is the weekly stock return recovery for firm i comparing with its in the following 6 months. \({{LogCOVID}19}_{{t}}\) represents the COVID-19 cases in week t. \({{\boldsymbol{CSR}}^{\prime} }_{i}\) includes measures of \({{CSR}}_{i}\), \({{StrategicCSR}}_{i}\), \({{ResponsiveCSR}}_{i}\). \(\mathop{\sum }\nolimits_{m=1}^{k}{\beta }_{m}{X}_{m,i,{pre}2020}\) represents the effects of k firm-level control variables. To account for any unobservable characteristics that may be omitted in the model, we also include industry and time fixed effects (\({\delta }_{j,t}\)). We estimate equations by using OLS with robust standard errors clustered at the firm level.

Variable measurements

Weekly Stock Return(\({{{WkRtn}} \% }_{{{i}},{{t}}}\))

It is calculated by the Adjusted weekly stock return(Minus the corresponding Market return) of firm i from the last trading day in week t-1 to the last trading day in week t.

Weekly Stock Return Recovery(\({{{RtnRecovery}}}_{{{i}}}\))

It is calculated by the change of average weekly stock return(adjusted by market return) during COVID-19 comparing with that in the following 6 months, then scaled by 3 months average weekly stock return before COVID-19.

COVID-19(\({{{LogCOVID}}{{19}}}_{{{t}}}\))

It is calculated by the log of newly confirmed COVID-19 cases in week t.

CSR includes measures of \({{CSR}}_{i}\) \({{StrategicCSR}}_{i}\), \({{ResponsiveCSR}}_{i}\). \({{StrategicCSR}}_{i}\) indicates whether firm i disclosed CSR reports prior to the epidemic. \({{ResponsiveCSR}}_{i}\) indicates whether firm i donated during the epidemic. \({{CSR\_total}}_{i}\) is used to measure whether firm i has fulfilled its social corporate responsibility before or during the epidemic.

Control Variables

Consistent with the existing literature, we employ we employ a set of firm-level control variables, including firm age (Age), firm size (Size), total debt ratio (Leverage), return on asset (ROA), cash holding (Cash), market-to-book ratio (MtB), growth rate (Growth), ownership (SOE). The detailed definitions for the variables above can be seen in the Appendix.

Results

Descriptive statistics of main variables and correlation analysis

Table 1 presents the descriptive statistics of the main variables. The mean value of WkRtn% is 0.436 with a standard deviation of 7.360, indicating a significant difference in weekly stock returns among the sample companies. The mean value of RtnRecovery% is 4.974, with a standard deviation of 14.922, indicating significant differences in stock return recovery among the sample companies. The mean value of LogCovid19 was 7.140, and its standard deviation was 1.905, suggesting that COVID-19 cases vary during the sample period. The mean value of CSR is 0.444 with a standard deviation of 0.497; the mean value of StrategicCSR is 0.258 with a standard deviation of 0.438; and the mean value of CSR is 0.193 with a standard deviation of 0.395, indicating significant differences in CSR, StrategicCSR, and ResponsiveCSR among the sample companies. The descriptive statistics results of the main control variables are consistent with those of existing studies.

Table 2 presents the results of the correlation analysis of the main variables, which shows that the absolute values of the relative coefficients are below 0.5 (except for the correlations among CSR, strategic CSR, and responsive CSR), suggesting no multicollinearity problem between the variables. Furthermore, the value of the VIF test for all variables is much less than 10, as shown in Table 3, which also suggests no multicollinearity problem.

Regression analysis

Table 4 illustrates the regression analysis of the moderating effect of total CSR on a firm’s stock returns after controlling for other firm characteristics and industry- and time-fixed effects. This indicates the significant negative impact of the COVID-19 shock and the positive impact of CSR on stock returns. The results of the interactive items of COVID-19 and CSR indicated that the moderating effect of CSR significantly alleviated the passive influence of COVID-19 by changing the coefficient from negative to positive.

Table 5 shows the heterogeneity of the CSR. The interactive item in Column 3 is significant but not in Column 2. This implies that the moderating effect of CSR affected stock returns through responsive CSR (Column 2) rather than strategic CSR (Column 3) during the COVID-19 pandemic.

Furthermore, Table 6 shows that in the long term, COVID-19 and CSR played opposite roles in the recovery of stock returns (Column 1). Similarly, the interactive item in column 1 is significant, indicating that CSR has an important moderating effect on the recovery of stock returns. However, the heterogeneity of CSR in the recovery of stock returns is quite different from that of stock returns. In contrast to Tables 5, 6 indicates that strategic CSR (Column 2) has a significant moderating effect, denoted by the coefficient of the interactive items, rather than responsive CSR (Column 3). This proves that long-term strategic CSR is much more crucial than short-term responsive CSR for an enterprise’s stock performance to recover from the COVID-19 crisis.

Robustness analysis

The results in Table 7 are inconsistent with those in Tables 4, 5. Columns 1 and 3 show the significant negative impact of the COVID-19 shock on daily stock returns. Still, the coefficients of the interactive terms of the COVID-19 shock and CSR indicators are significantly positive (0.061 and 0.134, respectively). This finding indicates that total and responsive CSR have notable moderating effects on daily stock returns. Although the coefficient of the interactive term in Column (2) is significantly negative (-0.032), the negative impact of the COVID-19 shock (−2.356) is significantly reduced by strategic CSR.

Similarly, Table 8 verifies the conclusions drawn from Tables 4 and 7. Both general and strategic CSR (Columns 1 and 2 in Table 8) have more significant and stronger moderating effects on daily stock return recovery than responsive CSR (Column 3 in Table 8). This implies that, in the long run, firms’ stock returns can recover more effectively from the COVID-19 shock through strategic CSR behaviours.

Sub-sample analysis

To investigate the heterogeneous moderating effects of CSR on stock returns, we divide all listed companies into groups according to different categories, such as ownership, industry, and firm size.

Ownership: SOE VS Non-SOE

Tables 9, 10 show that CSR had a greater impact on the stocks of non-state-owned companies. As public entities, state-owned companies have a certain sociality. Investors naturally believe that state-owned companies should take on social responsibility. However, the public has lower expectations of non-state-owned companies. Therefore, state-owned companies’ CSR activities do not significantly influence their stock returns (see Columns 1, 2, and 3 of Tables 9, 10). However, non-state-owned companies’ general and responsive CSR has an important moderating effect on stock returns (see Columns 4 and 6 in Table 9). In the long run, general and strategic CSR significantly impact the stock return recovery of non-state-owned companies (Columns 4 and 5 in Table 10).

Financial leverage: lower risk VS higher risk

Tables 11, 12 show that CSR has a greater impact on companies with lower financial leverage. Companies with lower financial leverage have much lower risk when faced with public health emergencies and events. During the COVID-19 pandemic, these companies did not need to engage in CSR behaviours but still benefited. The empirical results show that CSR has no significant effect on stock returns or recovery (see Columns 1 and 4 in Tables 11, 12). However, responsive CSR contributes to the stock returns of companies with lower financial leverage in the short run (Column 6 in Table 12), and strategic CSRs contribute to the stock return recovery of companies with lower financial leverage in the long run (Column 5 in Table 12).

Firm size: large companies VS small companies

Table 13 shows that general CSR does not impact large or small companies’ stock returns (Columns 1 and 4). Still, responsive and strategic CSRs significantly impact large companies’ stock returns (Columns 2 and 3). However, for a long time, only strategic CSR significantly moderated the stock return recovery of large companies (Column 2 in Table 14). People usually pay more attention to corporate reputation, corporate culture, corporate news, and corporate images of large companies than small companies. These large companies should take on more social responsibilities and set good societal examples. Thus, CSR affects large companies more than it affects small companies.

Conclusions and discussions

This study examines the moderating impact of heterogeneous CSR on CSP and CSP recovery during the COVID-19 pandemic in China. Our findings indicate that the COVID-19 outbreak significantly negatively impacts firms’ stock returns and recovery. However, CSR mitigated the inhibitory effects of COVID-19. Our research shows that responsive CSR significantly mitigates the negative influence of COVID-19 on stock returns in the short term, whereas strategic CSR does not have a significant impact. However, in the long run, strategic CSR notably accelerated the recovery of stock returns compared to responsive CSR. Additionally, the moderating effects of CSR are more significant for the stock returns and recovery of non-state-owned, non-medical, and non-Hubei firms. These results suggest that CSR is an effective risk-mitigation tool that can significantly reduce the negative impact of emergent public events on CSP. Hence, companies can take immediate responsive CSR actions to mitigate negative shocks to stock returns when emergent public events occur. However, in the long run, corporations must take active strategic CSR actions to recover more quickly from the shocks of emergent public events.

These findings have important implications for companies. First, CSR could be treated as a cost-enhancing behaviour because doing CSR is usually much more expensive but without foreseeable benefits. However, our results indicate that CSR, as an effective risk-mediation pool, could help companies eliminate stock price crashes and recover quickly. Therefore, companies can firmly believe that conducting CSR is beneficial, especially in bringing long-term strategic benefits to themselves. Second, although CSR can benefit companies, they must be aware of the heterogeneity of CSR behaviour. Corporate social responsibility can provide long-term benefits to enterprises. When facing sudden negative events, companies must implement responsive CSR to alleviate short-term negative impacts. Third, it is necessary for companies to vigorously disclose corporate social responsibility information so that such a positive corporate image can be more easily known to their stakeholders and help improve corporate reputation, which is vital for companies to mitigate risks. Finally, companies undertaking more social responsibility will help them establish good relationships with the government and obtain more sustainable development projects from the government, especially for non-state-owned companies.

Our study provides new findings on the effects of heterogeneous CSR behaviours on corporate stock returns. This study has some limitations that need to be investigated further in the future. First, there is no consensus in the literature on measuring corporate strategic social responsibility and responsive social responsibility. This study used donations made by companies in response to COVID-19 as a measure of corporate responsive social responsibility and long-term corporate CSR to measure strategic social responsibility. Although the proposed measure is logical and reasonable, it lacks accuracy. Therefore, how to accurately measure corporate strategic and responsive social responsibility needs to be explored in the future. Second, the roles that strategic corporate social responsibility and responsive corporate social responsibility behaviours will play in mitigating negative shocks in the future still need to be further verified.

Data availability

Data are available upon requests.

References

Archimi CS, Reynaud E, Yasin HM, Bhatti ZA (2018) How perceived corporate social responsibility affects employee cynicism: The mediating role of organizational trust. J Bus Ethics 151(4):907–921

Bansal P, Jiang GF, Jung JC (2015) Managing responsibly in tough economic times: strategic and tactical csr during the 2008–2009 global recession. Long Range Plan 48(2):69–79

Bansal P, Roth K (2000) Why companies go green: A model of ecological responsiveness. Acad Manag J 43(4):717–736

Benabou R, Tirole J (2010) Individual and corporate social responsibility. Economica 77:1–19

Bohas A, Poussing N (2016) An empirical exploration of the role of strategic and responsive corporate social responsibility in the adoption of different green IT strategies. J Clean Prod 122:240–251

Boubaker S, Liu Z, Zhan Y (2022) Customer relationships, corporate social responsibility, and stock price reaction: Lessons from China during health crisis times. Financ Res Lett 47:102699

Buertey S, Chu TT, Thompson EK (2024) An empirical study on the cushioning effect of corporate social responsibility on the negative impact of COVID-19 on firm performance. Corp Soc Responsibility Environ Manag 31(2):1364–1379

Carroll AB (1979) A three-dimensional conceptual model of corporate performance. Acad Manag Rev 4:497–505

Carroll AB (1999) Corporate social responsibility: Evolution of a definitional construct. Bus Soc 38(3):268–295

Carroll AB (2004) Managing ethically with global stakeholders: A present and future challenge. Acad Manag Executive 18:114–120

Carroll AB, Shabana KM (2010) The business case for corporate social responsibility: A review of concepts, research and practice. Int J Manag Rev 12(1):85–105

Carroll AB, Zhang H, Zhang J (2012) The construct validity of corporate social responsibility and its association with corporate reputation. J Bus Ethics 111(2):187–201

Chang X, Fu K, Jin Y, Liem PF (2022) Sustainable Finance: ESG/CSR, Firm Value, and Investment Returns*. Asia Pac J Financ Stud 51:325–371

Chen RCY, Hung SW, Lee CH (2018) Corporate social responsibility and firm idiosyncratic risk in different market states. Corp Soc Responsib Environ Manag 25:642–658

Choi C, Jung H (2022) COVID-19’s impacts on the Korean stock market. Appl Econ Lett 29(11):974–978

Chollet P, Sandwidi BW (2018) CSR engagement and financial risk: A virtuous circle? International evidence. Glob Financ J 38:65–81

Deng B, Ji L, Liu Z (2022) The effect of strategic corporate social responsibility on financial performance: Evidence from China. Emerg Mark Financ Trade 58(6):1726–1739

Ding W, Levine R, Lin C, Xie W (2021) Corporate immunity to the COVID-19 pandemic. J Financ Econ 141(2):802–830

Donadelli M, Kizys R, Riedel M (2017) Dangerous infectious diseases: Bad news for main street, good news for wall street? J Financ Mark 35:84–103

Eccles RG, Ioannou I, Serafeim G (2012) The impact of corporate sustainability on organizational processes and performance. Manag Sci 60(11):2835–2857

Epstein MJ, Buhovac AR, Yuthas K (2010) Implementing corporate social responsibility: Lessons learned from the front line. J Corp Account Financ 21(3):15–24

Ferriani F, Natoli F (2021) ESG risks in times of Covid-19. Appl Econ Lett 28(18):1537–1541

Gao Y, Kil-Seok Han KS (2022) Managerial overconfidence, CSR and firm value. Asia-Pac J Account Econ 29(6):1600–1618

Hart SL, Milstein MB (2003) Creating sustainable value. Acad Manag Perspect 17(2):56–67

Havlinova A, Kukacka J (2023) Corporate social responsibility and stock prices after the financial crisis: The role of strategic CSR activities. J Bus Ethics 182:223–242

Henriques I, Sadorsky P (1999) The relationship between environmental commitment and managerial perceptions of stakeholder importance. Acad Manag J 42:87–99

Jeong KH, Jeong SW, Lee WJ et al. (2018) Permanency of CSR activities and firm value. J Bus Ethics 152:207–223

Jin C, Cong Z, Dan Z, Zhang T (2023) COVID-19, CSR, and performance of listed tourism companies. Financ Res Lett 57:104217

Karwowski M, Raulinajtys-Grzybek M (2021) The application of corporate social responsibility (CSR) actions for mitigation of environmental, social, corporate governance (ESG) and reputational risk in integrated reports. Corp Soc Responsib Environ Manag 28:1270–1284

Khan I, Jia M, Lei X, Niu R, Khan J, Tong Z (2023) Corporate social responsibility and firm performance. Total Qual Manag Bus Excell 34(5-6):672–691

Khanchel I, Lassoued N, Gargouri R (2024) Have corporate social responsibility strategies mattered during the pandemic: Symbolic CSR versus substantive CSR. Corp Soc Res Environ Manag 31(2):1380–1398

Kim S, Lee G, Kang H-G (2021) Risk management and corporate social responsibility. Strategic Manag J 42:202–230

Kim Y, Li H, Li S (2014) Corporate social responsibility and stock price crash risk. J Bank Financ 43:1–13

Krueger P, Zacharias S, Tang DY, Rui, Z (2021) The Effects of Mandatory ESG Disclosure Around the World. European Corporate Governance Institute—Finance Working Paper No. 754/2021, Swiss Finance Institute Research Paper No. 21–44. Available online: https://doi.org/10.2139/ssrn.3832745 (accessed on 19 October 2021)

Liang H, Renneboog L (2017) On the foundations of corporate social responsibility. J Financ 72(2):853–910

Lins KV, Servaes H, Tamayo A (2017) Social capital, trust, and firm performance: the value of corporate social responsibility during the financial crisis. J Financ 72:1785–1824

Luo Y (2006) Political behavior, social responsibility, and perceived corruption: A structuration perspective. J Int Bus Stud 37:747–766

Michelon G, Boesso G, Kumar K (2013) Examining the link between strategic corporate social responsibility and company performance: An analysis of the best corporate citizens. Corp Soc Responsib Environ Manag 20(2):81–94

Minor D, Morgan J (2011) CSR as reputation insurance: PRIMUM NON NOCERE. Calif Manag Rev 53(3):40–59

Mithani MA (2017) Innovation and CSR - do they go well together? Long. Range Plan. 50(6):699–711

Oikonomou I, Brooks C, Pavelin S (2012) The impact of corporate social performance on financial risk and utility: A longitudinal analysis. Financ Manag 41:483–515

Park J, Lee H, Kim C (2014) Corporate social responsibilities, consumer trust and corporate reputation: South Korean consumers’ perspectives. J Bus Res 67(3):295–302

Porter ME, Kramer MR (2006) Strategy and society. Harv Bus Rev 84(12):78–92

Porter ME, Kramer MR (2011) Creating shared value: How to reinvent capitalism. Harv Bus Rev 89:62–77

Rameshwar R, Saha R, Sanyal SN (2020) Strategic corporate social responsibility, capabilities, and opportunities: Empirical substantiation and futuristic implications. Corp Soc Responsib Environ Manag 27(6):2816–2830

Ratajczak P, Szutowski D (2016) Exploring the relationship between CSR and innovation. Sustain Acc Manag Policy J 7(2):295–318

Rhee YP, Park C, Petersen B (2021) The effect of local stakeholder pressures on responsive and strategic CSR activities. Bus Soc 60(3):582–613

Sakunasingha B, Jiraporn P, Uyar A (2018) Which CSR activities are more consequential? Evidence from the Great Recession. Financ Res Lett 27:1–8

Schell D, Wang M, Huynh TLD (2020) This time is indeed different: A study on global market reactions to public health crisis. J Behav Exp Financ 27:100349

Sen S, Bhattacharya CB (2001) Does doing good always lead to doing better? Consumer reactions to corporate social responsibility. J Mark Res 38(2):225–243

Shiu Y, Yang S (2017) Does engagement in corporate social responsibility provide strategic insurance-like effects? Strategic Manag J 38(2):455–470

Tian J, Wang X, Wei Y (2022) Does CSR performance improve corporate immunity to the COVID-19 pandemic? Evidence from China’s stock market. Front Public Health 10:956521

Tokoro N (2007) Stakeholders and corporate social responsibility (CSR): A new perspective on the structure of relationships. Asian Bus Manag 6:143–162

Tsai HJ, Wu Y (2022) Changes in corporate social responsibility and stock performance. J Bus Ethics 178:735–755

Turker D (2009) Measuring corporate social responsibility: A scale development study. J Bus Ethics 85(4):411–427

Úbeda-García M, Claver-Cortés E, Marco-Lajara B, Zaragoza-Sáez P (2021) Corporate social responsibility and firm performance in the hotel industry. The mediating role of green human resource management and environmental outcomes. J Bus Res 123:57–69

Wang YG (2011) Corporate social responsibility and stock performance—evidence from Taiwan. Mod Econ 2(05):788

Yang S, Chang A, Chen Y, Shiu Y (2019) Can country trade flows benefit from improved corporate social responsibility ratings? Econ Model. 80:192–201

Yang Z, Su H, Sun W (2021) Can strategic corporate social responsibility drive corporate innovation? South Afr J Bus Manag 52(1):a2577

Yi Y, Zhang Z, Yan Y (2021) Kindness is rewarded! The impact of corporate social responsibility on Chinese market reactions to the COVID-19 pandemic. Econ Lett 208:110066

Zaremba A, Czapkiewicz A (2020) Is Bitcoin a hedge or safe haven for currencies? An intraday analysis during COVID-19. Res Int Bus Financ 54:101295

Zhai H, Xiao M, Chan KC, Liu Q (2022) Physical proximity, corporate social responsibility, and the impact of negative investor sentiment on stock returns: Evidence from COVID‐19 in China. Int Rev Financ 22(2):308–314

Zhang D, Hu M, Ji Q (2021) Financial markets under the global pandemic of COVID-19. Financ Res Lett 36:101528

Zhou D, Zhou R (2022) ESG performance and stock price volatility in public health crisis: Evidence from COVID-19 pandemic. Int J Environ Res Public Health 19:202

Acknowledgements

This study is supported by the National Social Science Fund of China (23FGLB032) and the Shanghai Social Science Foundation (2022ZJB006). We also thank Mr. Dezheng Huo for the financial support.

Author information

Authors and Affiliations

Contributions

Yunhe Li conceptualized, designed and supervised the study. Xinyi Shen collected thedata and performed the data analysis. Fang Zhang coordinated and supervised the study.Yunhe Li and Fang Zhang drafted the manuscript. All authors substantially contributedto the article and approved the submitted version. These authors contributed equally to this work.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Li, Y., Shen, X. & Zhang, F. The effects of heterogeneous CSR on corporate stock performance: evidence from COVID-19 pandemic in China. Humanit Soc Sci Commun 11, 499 (2024). https://doi.org/10.1057/s41599-024-03001-9

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-03001-9