Abstract

Advanced digitalization and financial technology have of recent times become among the most crucial tools. Data mining and sentiment analysis have revealed the importance of digitalization in modern times. This study examines the influence of Google search activity on the volatility of digital assets. We analyzed six digital asset prices for Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple from the Coinmarketcap database. We used tweets on Twitter to survey users’ sentiment by using the Twitter search Application Programming Interface and Google trend search from web searches, news searches, and YouTube searches data using RStudio software. The study spanned 1 September 2019 to 31 January 2020 and employed the Vector Autoregression (VAR) approach for analysis. The VAR estimation revealed that Google search variables have significantly influenced the volatility of Bitcoin, Ethereum, Litecoin, and Ripple, as supported by the Granger causality test and impulse response function. The results of this study could be useful for investors and policymakers in drawing up strategies to reduce market volatility. These results should thus be useful to investors in developing profitable investment strategies to mitigate the impact of market turbulence.

Similar content being viewed by others

Introduction

Key advances in digitalization have made social media a common platform for individuals and public to express their opinions on specific issues. Public views are the users’ perspectives on particular topics, products, brands, issues or policies (Lippmann, 2017). A study by Alkhatib et al. (2020) stated that government policies and businesses could also be significantly influenced by views of individual netizens on related issues. They found that the government and businesses monitor overall views of the community to gauge their perspectives on current policies, products or events.

The theory of behavioural science have identified some characteristics of individuals and the environment that may be related with their innate behaviour. The theory also includes behavioural theory and psychology in conventional economic and financial elements to explain investor decisions. Among the earliest researchers to develop the financial behaviour theory were Kahneman and Tversky (1979) and Thaler (1980). Based on financial behaviour theory, Nouri et al. (2017) stated that buying and selling shares was due to internal factors and external psychological factors. Khajavi and Ghasemi (2006) also added that financial behaviour theory covers various aspects of psychology and social sciences. Some studies (Ding et al. 2020; Kraaijeveld and De Smedt, 2020; Reis and Pinho, 2020; Anastasiou et al. 2021) also indicated that user sentiment may have an impact on the individual’s behaviour and decision-making. Additionally, one of the primary reasons for price fluctuation in digital assets markets was due to external factors. Admittedly, by the middle of 2017, the majority of digital assets had undergone significant price changesFootnote 1 and at the same time, user reaction on TwitterFootnote 2 and other social media platforms, as well as Google searchesFootnote 3 for digital assets, all rose simultaneously.

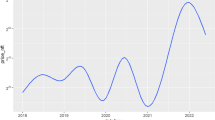

Figure 1 and Fig. 2 illustrate Bitcoin volatility and trend in Google data respectively on the keywords “Bitcoin”, from January 2017 until February 2020. They mostly showed similar patterns between Bitcoin volatility and search activity, especially at the end of 2017. Preis et al. (2013) also pointed out that Google search activity and the stock market price had positive correlation, especially before the stock market crash. An almost similar scenario occurred in the Bitcoin market which recorded a surge in searches in the web, news, and YouTube related to Bitcoin prior to the fall in its price. We highlighted the Bitcoin market in this study since the currency accounts for almost 50 percent of the top 100 Cryptocurrency1 and can thus influence the price of other such currencies in the same way as changes in the price of Bitcoin (Vidal-Tomás and Ibañez, 2018; Hajam et al. 2021). Further, users’ sentiment on the Twitter platform also exerts significant influence on the digital asset market. Several studies (Garcia et al. 2014; Garcia et al. 2015; Steinert and Herff, 2018; Shen et al. 2019; Philippas et al. 2019; Kraaijeveld and De Smedt, 2020; Öztürk and Bilgiç, 2021; Suardi et al. 2022) have already proven the impacts of users’ sentiment on the digital assets market. In addition to their findings, several studies (Garcia et al. 2014; Garcia et al. 2015; Li et al., 2021) have emphasized the combined significance of Google search activity and Twitter as useful indicators to investor sentiment.

Bitcoin volatility.

Google trend data.

As evident from the graph above, news and YouTube searches on digital assets show a very similar pattern to the digital asset market. Moreover, users tend to browse through various Google search platforms to gather sufficient information. In consequence, the objective of our study will be to examine the search effects of web, news, and YouTube on the volatility of digital assets. The study identified six digital assets, namely Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple, with the highest market capitalization in 2019Footnote 4. Together these assets comprised 71 percent of the market capitalization in the economy in 2019Footnote 5. In consequence, we may evaluate the impact of these searches on digital assets volatility and identify the sources that may have significant influence. In this way investors and policymakers may acquire a better understanding of the importance of user sentiment and Google searches in the digital assets market. For example, the USD currency captured almost 70 percent of Bitcoin transactions in 2020Footnote 6; such, the findings of this study may be highly beneficial to the United States policymakers and also to other policymakers who welcome the use of digital assets in their transactions. This finding is in line with Huerta et al. (2021), who noted that such analysis was particularly helpful to national policymakers, since they will have a better understanding of users’ attention and accordingly create a suitable framework to solve future issues. In addition, investors can formulate a profitable investment strategy through understanding the relationship between Google trend data and the digital assets market (Chuffart, 2022; Siriopoulos et al. 2021). This study utilized the RapidMiner software to obtain real-time data from the Twitter developers. In this way not a single tweet was missed over the 5-month tweet collection period. Data were thus gathered over a short time period. Consistent with the majority of earlier studies (Feng Mai et al. 2018; Steinert and Herff, 2018; Shen et al. 2019; Kraaijeveld and De Smedt, 2020;) the study analyzed sentiment data from Twitter over the course of only 2–3 months. This paper starts with an introduction in section one and continues with the literature review in section two and on to the methodology in section three. The empirical findings are given in section four with the discussion presented in section five, and the conclusion in section six.

Literature review

Many researchers have conducted studies related to behavioural science theory. For example, Subrahmanyam (2008), Dowling et al. (2009) and Lodhi (2014) studied internal factors, including the investor’s personality and psychological nature. Khajavi and Ghasemi (2006) examined the theory of financial behaviour covering various aspects of psychology and social sciences, contrary to the efficient market hypothesis. Studies that neglect users’ behaviour in the rational pricing model may result in less accurate estimation of securities performance (Baker and Wurgler, 2006). Financial behaviour can also be used to explain the irrational behaviour of investors (Anastasiou et al. 2021). The aspect on sentiment may illustrate price discrepancies due to stock price changes away from the initial price (Reis and Pinho, 2020). Consequently, investor behaviour may be one of the factors that influence the stock price movement. However, the Efficient Market Hypothesis (EMH) theory contends that stock market prices accurately reflect all relevant information and indicate signals for resource allocation (Fama, 1970). Despite the spread of new information to the public, the stock price will return to normal without experiencing any market shocks. Ding et al. (2020) admittedly claimed that in a real-world scenario, investors tend to overreact to a bad incident that may exert an immediate impact on the financial market in the short term and neglect historical stock price data. Furthermore, Kraaijeveld and De Smedt (2020) emphasized that the EMH theory pays little attention to the perspective of users’ behaviour. Additionally, Bourghelle et al. (2022) noted that users’ behaviour is a non-fundamental variable and it frequently exerts an impact on their investment decision although separate from the economic aspects of the market.

Further, the behavioural financial theory reveals the irrational behaviour of investors and indicates that their investment decisions are not always rational. Some studies (Liu and Tsyvinski, 2018; Katsiampa et al. 2019; Chang et al. 2021; Chuffart, 2022; Aslanidis et al. 2022; Pinto-Gutiérrez et al. 2022) discovered a strong relationship between Google trend data and volatility and return of digital assets. These findings were also supported by the real situation that occurred in 2017 as illustrated in Fig. 1 and Fig. 2. The price of Bitcoin in December 16, 2017 was $19, 345.49, at the same time the Google search activity related to Bitcoin reached the peak level of popularity. However, the Fama French 3-factor model does not incorporate the importance of users’ attention. It is an asset pricing model that was developed on the capital asset pricing model (CAPM) by including size risk and value risk elements to the market risk factors. The analysis of the financial market volatility is hence inaccurate when the behavioural factor is not included in the model.

Recently, human autobiographical memory was shown to influence issues related to investment decisions. For example, the development of social networking sites opens up opportunities for behavioural science studies to easily access or obtain user data. Behaviour science and social network studies demonstrate a correlation between digital currency and Twitter (Steinert and Herff, 2018). In addition, conventional media platforms, namely television, magazines, or newspapers, use social media to rapidly spread information to readers (Araya et al. 2017). In addition, during the Covid-19 pandemic, Twitter was the platform for users to obtain information and make predictions on Bitcoin (Kaminski, 2014; Ozturk and Bilgic, 2021) the stock market (Bollen et al. 2011; Zhang et al. 2011; Mittal and Goel, 2012; Rao and Srivastava, 2012; Si et al. 2013; Sprenger et al. 2014), election results (Bermingham and Smeaton, 2011; Sprenger et al. 2014), and health and risk factors (Huerta et al. 2021; Lee et al. 2022).

Kristoufek (2013) and Yu et al. (2019) studied Bitcoin prices using Google trends and Wikipedia. Kristoufek (2013) found a two-way relationship whereas Yu et al. (2019) discovered that Google search was considered a source of information compared to Wikipedia, which does not provide new information, but only general information. Papadamou et al. (2022) further added that the number of searches gathered from the Google trend data can be considered as the overall population’s behaviour for a particular search, and such searches were proven useful in evaluating investor behaviour. Other studies found that Twitter and Google searches produced significant contributions to the volatility of Bitcoin prices (Garcia et al. 2015) but contradicted the results of Han et al. (2019), in which Google search showed more significant relationship with the price of Bitcoin than that in Twitter. Both studies used a number of tweets and were Google-themed, and this difference may be due to obviating user sentiment on Twitter as opposed to other researchers (Kim et al. 2016; Deng et al. 2017; Kim et al. 2017; Mai et al. 2018; Steinert and Herff, 2018; Wolk, 2019).

Most past studies only focused on Google search in measuring the effectiveness of the digital assets market (Zhang et al. 2018; Katsiampa et al. 2019; Aslanidis et al. 2022; Chang et al. 2021; Chuffart, 2022; Zhang et al. 2021; Pinto-Gutiérrez et al. 2022; Süssmuth, 2022; Smales, 2022; Tripathi et al. 2022). In particular, Chuffart (2022) demonstrated that Google search is a solid indicator of the correlation between digital assets and provides useful information for portfolio management. He further added that Google search activity could explain the significant changes in the correlation dynamics between digital assets especially the bubble burst in 2017. However, none of the studies focused on news and YouTube search indicators related to digital assets. We know that users rely on Google search and browse other aspects to get complete comprehensive information. This study has contributed to the narrowing of knowledge gaps on the implications of searches in the websites, news, and YouTube for digital assets and the volatility of their prices. The platforms provide significant sources for identifying the impact of price volatility due to digital asset.

Methodology

The methodology is divided into several stages. The first step involved data collection wherein six digital assets were focused on: Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple, which together accounted for 71 percent of the market capitalization of 100 digital assets. The digital asset price data were sourced from coinmarketcap.com. This study also sourced user tweets on Twitter for digital assets using the Twitter search Application Programming Interface (API). We collated Twitter data that included usernames, hashtags, tweets, and some retweets. We used RapidMiner software to collect the 160 data per day for each digital asset by using the keywords ‘Bitcoin’, ‘Bitcoin Cash’, ‘Ethereum’, ‘Ethereum Classic’, ‘Litecoin’, and ‘Ripple’. In addition, data related to web search, news search, and YouTube search based on these keywords were sourced from Google Trend data using RStudio software. The data have value that range from 0 to 100. A value of 100 indicates peak popularity for the search term and the reverse for 0 value. Daily data were collated between 1 September 2019 and 31 January 2020.

The second step was computing the volatility for stated digital assets and cleaning the collected tweets. Starting with market data for digital assets, we used the price of Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple Pi,t to calculate the return, as shown in Eq. (1):

The variance of digital asset returns was then estimated using the generalized autoregressive conditional heteroskedasticity (GARCH) approach in this study. The following are the conditional mean and variance specifications:

Where, Returni,t is the current digital asset rate of return (i = 1,2,3,4,5,6) at time t. Next, Returni,t-1 refers to the past digital assets rate of return for Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple, and εi,t is an error term. The parameters of x > 0, α ≥ 0, β ≥ 0, and ηi,t are independent and similar random variables distributed with zero mean and unit variance. The hi,t is the matrix co-variances. The error terms act normally, and maximum likelihood is used to estimate parameters. Subsequently, the compiled tweets were then processed to remove any noise components. In this study, user sentiments were analyzed using the Valence Aware Dictionary for Sentiment Reasoning (VADER) (Hutto and Gilbert, 2014). This dictionary is useful for deciphering some punctuation, symbols, and numbers in tweets. Our study used the VADER dictionary to clean the data, as demonstrated by Öztürk and Bilgiç (2021). Tweets were cleaned up from all types of punctuations, except #, $, @, ‘, ’, !, “, ?, ., and webpage links. Additionally, all uppercase letters were changed to lowercase.

The third phase of this study comprised sentiment analyses on the cleaned tweets. The VADER approach is a lexicon and rule-based sentiment analysis and its specifically trained, and appropriate for sentiments expressed on Twitter (Elbagir and Jing, 2019; Kraaijeveld and De Smedt, 2020). Valencia et al. (2019) stated that VADER has several additional advantages, and it is particularly useful for analyzing tweet content and extracting sentiment values from emotions, emojis, punctuation, use of grammar, slang, and acronyms compared to machine learning techniques. Moreover, VADER can produce three types of sentiment which are positive sentiment, neutral sentiment, and negative sentiment. Further, VADER was used to estimate the compound score. Based on this, each tweet gathered for the study was divided into three sentiment categories. A tweet with a score of −1 was categorized as a negative sentiment, whereas a tweet with a score of +1 was classified as a positive sentiment. Hutto and Gilbert (2014) also indicated that compound scores of ≥0.05 show positive sentiments, while neutral sentiments ranged between >−0.05 and <0.05, and ≤−0.05 for negative sentiments. This range of scores was also employed in earlier studies that used the VADER dictionary (Kraaijeveld and De Smedt, 2020; Öztürk and Bilgiç, 2021; Suardi et al. 2022). The total number of positive, neutral, and negative sentiments were counted and categorized into daily tweet datasets individually after the sentiment analysis was complete. The Python softwareFootnote 7 was used for the cleaning process and sentiment analysis.

In the fourth step, the datasets for digital assets were organized independently. The variables in this study had to be renormalized since the sentiment and Google trend data were highly volatile compared with other variables. The Z-transformation was used to standardize all of the time series: Zt = (Xt−μx)/σx, where μx and σx are defined as the mean and standard deviation of each time series, respectively. Due to the equal scale and variance of all the data, researchers were able to quantify the effects of the changes in numerical analysis (Garcia et al. 2015). Before proceeding with the VAR analysis, this study adopted the Augmented Dickey Fuller (ADF) to assess each time series stationary properties (Fuller, 2009). The null hypothesis of the Augmented Dickey–Fuller t-test is 0 Ho θ = (i.e., the data need to be differenced to make it stationary) versus the alternative hypothesis of 0: H1 θ < (i.e., the data is stationary and doesn’t need to be differenced). All variables have to be tested using ADF, and if rejected by the null hypothesis, the data is considered stationary and significant at level I(0).

Finally, to investigate the implication of Google searches on the volatility of digital assets, a VAR method was employed in the following form:

where a is a vector of constant white noise innovations while εi,t is an independent vector. Yi,t is the vector y of variable volatility for Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple. Xi,t-j represents the vector that contains different variables, such as web search, news search, YouTube search, positive sentiment, neutral sentiment, and negative sentiment. The lag selection was based on the Schwarz Criterion (SC), the Akaike Information Criterion (AIC), and the Hannan-Quinn (HQ) Criterion. However, the suggested lag for Bitcoin and Ripple has an autocorrelation problem. To solve this problem, other lags were chosen, namely lag 3 for Bitcoin and lag 2 for Ripple. In addition, lag 1 was chosen for Bitcoin Cash, Ethereum, Ethereum Classic, and Litecoin based on the lag selection criteria SC, AIC, and HQ. With this VAR model, this study subsequently performed a linear Granger causality test (Granger, 1969). The Granger causality test is written as follows for a linear system:

This research has carried out the Impulse Response Function (IRF) analysis, which is a fundamental method in a VAR model (Dizaji, 2019; Siriopoulos et al. 2021). IRF shows how the digital assets volatility response to a shock in web search, news search, YouTube search, positive sentiment, negative sentiment, neutral sentiment, and volatility. In IRF, the vertical line represents the magnitude of response to shocks and the horizontal line indicates the period after the initial shock. The dotted lines represent 95% confidence intervals, whereas the solid lines depict the impulse response. When the horizontal line falls between confidence bands, the impulse response is not statistically significant. On the other hand, the ordering of variable could affect the IRF findings. Dizaji (2019) proposed that the ordering of variables should adhere to economic theory. These were mostly exogenous variables to endogenous variables. Google trend and sentiment variables were placed as the first and second variables being the most exogenous variables in our model. Volatility variables come next in the Cholesky ordering, after the first and second variables. Hence, volatility is the most endogenous variable in the VAR system. Subsequently, a diagnostic test of the estimated VAR model was conducted separately utilizing the inverse roots of the AR characteristic polynomial (VAR stability) and the VAR residual serial correlation Lagrange Multiplier (LM) test for digital assets datasets.

Empirical results

Table 1 reports the mean, median, maximum, minimum, standard deviation (Std. Dev) and skewness for the variables of volatility, web search, news search, YouTube search, positive sentiment, negative sentiment, and neutral sentiment for digital assets such as Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin and Ripple. The news search and neutral sentiment (web search and positive sentiment) of Bitcoin (Ethereum) shows a higher mean compared to other digital assets of the period. Furthermore, YouTube search of Litecoin (volatility and negative sentiment of Ripple) has a markedly greater mean than other digital assets. Besides, Bitcoin datasets describe that positive sentiment and neutral sentiment are negatively skewed and other variables are positively skewed. Among the variables, only neutral sentiment (positive sentiment) in Ethereum (Ripple) datasets is skewed negatively. Conversely, all the variables in Bitcoin Cash, Ethereum Classic, and Litecoin are skewed positively. The standard deviation values of all variables for all digital assets shows the value of one (1) due to all time series being standardized using the Z-transformationFootnote 8.

Table 2 shows the unit root test results for the variables of volatility, web search, news search, YouTube search, positive sentiment, negative sentiment, and neutral sentiment for digital assets such as Bitcoin, Bitcoin cash, Ethereum, Ethereum classic, Litecoin, and Ripple by using the ADF method in the categories of intercepts, trends and intercepts. All variables in the Ethereum and Ripple datasets stationarity showed 1% significance level. For Bitcoin, Bitcoin Cash, Ethereum Classic, and Litecoin, all variables are stationary at the same level as Ethereum and Ripple, but the volatility is stationary at the 5 and 10% significance levels. Specifically, the volatility of Bitcoin and Bitcoin Cash is stationary at 5% (intercept) and 10% (trend and intercept) significance levels respectively. In addition, the volatility of Ethereum Classic and Litecoin is stationary at a 5% (intercept and trend and intercept) significance level.

VAR estimation

Table 3 presents the findings of the VAR models, with the coefficient estimates in Panel A and the Granger causality results in Panel B. According to the results of the VAR estimation of Bitcoin, web search influences Bitcoin volatility, with a significant positive at lag 1 and a significant negative at lag 2 at the 1 and 10% significance levels, respectively. These results were value added by the Granger causality results, indicating that the null hypothesis was successfully rejected thus designating that web search does not Granger cause volatility at the 1% significance level. The mix of positive and negative relationships at lags between user attention and the Bitcoin market is highly fluctuating due to Bitcoin price (Chen et al. 2020). Furthermore, Hasan (2022) pointed out that the reaction of the Bitcoin market towards user attention and sentiment was more in line with temporary sentiment shocks. This analysis also discovered that news searches had significantly affected volatility at lag 2 with 5% significance level. This observation proved that a rise in news search led to an increase in volatility on the 2nd day. The Granger causality test also revealed that news search resulted in Granger volatility to be significant at 10% level. Although, YouTube impact volatility was significantly positive in panel A, the result however was not supported by Granger causality findings in panel B.

The VAR estimation for Bitcoin Cash revealed that volatility is influenced by own shock only and is not influenced by other variables in the model. It may happen since Bitcoin cash is less popular than Bitcoin, and investors are more familiar with Bitcoin in the world of digital assets. Consequently, most of the previous studies (Polasik et al. 2015; Garcia et al. 2015; Kim et al. 2016; Kim et al. 2017; Mai et al. 2018) only focused on Bitcoin in their analyses due to similar reasons. Besides, Ethereum volatility is significantly affected by web search at lag 1 with 1% significance level. These findings are supported by the Granger causality results at 1% significance level, as shown in panel B of Table 3. Moreover, the VAR estimation of Ethereum Classic illustrates that web search impacts Ethereum Classic volatility, with a significant positive at lag 1 at the 10% significance level. These findings were supported by the Granger causality results at the 10% significance level. Further, positive sentiment (negative sentiment) influences Ethereum Classic volatility significantly and negatively (positive) at lag 1 with 5% (1%) significance level. The Granger causality test has explained that positive sentiment and negative sentiment can be very useful in predicting future volatility at the 5 and 1% significance levels, respectively. Subsequently, Litecoin volatility was affected significantly and positively by web search and negative sentiment at lag 1 with 1% significance level. These outcomes were value added by the Granger causality test in panel B at the 1% significance level. Meanwhile, the VAR estimation for Ripple described that web search have a significant positive impact on Ripple volatility at lag 1 with 1% significance level. In addition, YouTube search affects Ripple volatility, with a significant positive at lag 1 and a significant negative at lag 2 with 5 and 1% significance levels, respectively. The Granger causality results in panel B also revealed that the null hypothesis was rejected indicating that web search and YouTube search does not Granger cause volatility at the 5 and 1% significance levels, respectively. Even though, news searches influence Ripple volatility significantly in panel A but the results are not supported by the Granger causality test in panel B.

Impulse response function

Figure 3 illustrates the impulse response of Bitcoin volatility when an innovation of other variables operates over the next 15-day period. We identified that shock in web search and news search triggered a gradual increase in volatility. One unit shock in the standard deviation of the web search (news search) influences Bitcoin volatility positively and significantly from day 1 until day 7 (day 3 until day 9). In addition, the IRF findings are in agreement with the VAR estimation results, which describe that Bitcoin volatility responds more towards Google search variables than Twitter sentiment variables. Our results are consistent with some studies (Aalborg et al. 2019; Zhang et al. 2018; Shen et al. 2019; Yu et al. 2019), which indicated that the Google trend has a significant impact on Bitcoin markets. This is a crucial finding since an investor searching for Bitcoin information on the internet may become motivated to invest in Bitcoin, producing a cause-and-effect relationship with Bitcoin volatility. Further, the response of Bitcoin volatility to any shock resulting from the variables of YouTube search, positive sentiment, neutral sentiment, and negative sentiment was not significant. Conversely, one unit shock in the standard deviation of the volatility affects Bitcoin volatility positively and significantly from day 1 until day 7.

Impulse response function of bitcoin.

The impulse response of Bitcoin Cash volatility to shock in other variables that took place over the next 15 days (period) is shown in Fig. 4. The IRFs of Bitcoin Cash volatility are only significant towards shock coming from news search and volatility. One unit shock in the standard deviation of the news search influences the Bitcoin Cash volatility slightly positively and significantly from day 1 until day 6. Furthermore, volatility response was significantly positive from own shock from day 1 until day 11. These findings are quite consistent with VAR results in that Bitcoin Cash volatility is only significant towards its own shock.

Impulse response function of bitcoin cash. Note: Y-axis and X-axis represent response standard deviation (s.d) and period.

Figure 5 depicts the impulse response of Ethereum volatility to shock in other variables throughout the course of the following 15 days (period). IRF analysis showed that it responded positively to web search shock from day 1 until day 5, which is consistent with VAR estimation. The volatility response was positively significant towards own shock from day 1 until day 7. In comparison, the response of Ethereum volatility towards shock coming from variables of YouTube search, news search, positive sentiment, neutral sentiment, and negative sentiment was not significant.

Impulse response function of ethereum. Note: Y-axis and X-axis represent response standard deviation (s.d) and period.

The impulse response of Ethereum Classic volatility to shocks in other variables throughout the course of the next 15 days (period) is illustrated in Fig. 6. The volatility is only significant towards shock coming from negative sentiment and volatility. The response was significant for the negative sentiment which shows that one unit shock in the standard deviation of the negative sentiment influences volatility positively and significantly from day 1 until day 10 which is in line with VAR findings.

Impulse response function of ethereum classic. Note: Y-axis and X-axis represent response standard deviation (s.d) and period.

Figure 7 describes the impulse response of Litecoin volatility to shocks in other variables that occurred over the next 15-day period. We observed that shock in web search and negative sentiment influenced volatility. One unit shock in the standard deviation of the web search (negative sentiment) affects Litecoin volatility positively and significantly from day 1 until day 9 (day 1 until day 8) as similarly shown by VAR estimation. Subsequently, volatility impact was shown positively significant on own shock from day 1 until day 8.

Impulse response function of litecoin. Note: Y-axis and X-axis represent response standard deviation (s.d) and period.

Figure 8 illustrates the Ripple volatility impulse response to shocks in other variables throughout the course of the subsequent 15 days (period). Ripple volatility responded positively to web search (YouTube search) shock from day 1 until day 4 (day 3) in agreement with VAR estimation. In addition, volatility reacts positively significantly towards own (negative sentiment) shock from day 1 until day 4 (day 3) whereas the response towards shock coming from other variables was not significant.

Impulse response function of ripple. Note: Y-axis and X-axis represent response standard deviation (s.d) and period.

Diagnostic tests

VAR residual serial correlation LM test

Table 4 shows the VAR residual serial correlation LM test for Bitcoin, Bitcoin cash, Ethereum, Ethereum classic, Litecoin, and Ripple. The test revealed that the VAR estimation has no serial correlation relationship with all digital assets.

Inverse roots of AR characteristic polynomial

Figure 9 illustrates the inverse roots of the AR characteristics polynomial for Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple. The VAR stability findings showed that all the points were inside the circle and the absolute values of Eigenvalue were <1 (1) for all digital assets. As a result, the computed VAR model was stable and satisfactory according to the diagnostic criteria.

Inverse roots of AR characteristic polynomial.

Discussion

This study examines the implication of Google search activity which comprises web search, news search, and YouTube search on digital assets’ volatility. The empirical findings provide evidence that the volatility of digital assets such as Bitcoin, Ethereum, Litecoin, and Ripple is influenced by the Google search variables compared with sentiment indicators. As an explanation, the volatility of Bitcoin was influenced by shock arising from web search and news search, whereas the volatility of Ethereum and Litecoin was affected by web search, and Ripple react to shock coming from web search and YouTube search. These results are in line with some studies (Urquhart, 2018; Katsiampa et al. 2019; Lin, 2020; Aslanidis et al. 2022; Chuffart, 2022; Chang et al. 2021; Li et al. 2021; Rutkowska and Kliber, 2021; Zhang et al. 2021; Pinto-Gutiérrez et al. 2022; Süssmuth, 2022; Smales, 2022; Tripathi et al. 2022) that highlight the importance of Google trend in digital assets markets. However, past studies generally focused on Google trend data and they did not consider the importance of separate searches such as web search, news search, and YouTube and relate these with digital assets markets. By perusing this enquiry, we obtained a clear view of how digital asset markets reacted to search activity.

In addition, digital assets such as Ethereum Classic and Litecoin only responded to Twitter sentiment among the six digital assets. The literature review showed us that the influence of Google search variables is superior to Twitter sentiment toward digital assets’ volatility. These results become value-added as per Steinert and Herff (2018) statement, which suggested a relationship between digital assets and social media under the concept of behavioural science. In addition, these findings are also in line with behavioural finance theory, which indicates that psychological and sentiment factors do have an important impact on investment decisions (Kraaijeveld and De Smedt, 2020).

Admittedly, policymakers can benefit from such analyses, especially in understanding the importance of Google search activity and in identifying the actual causes of digital assets volatility. This statement is supported by Huerta et al. (2021), who indicated that policymakers needed to discover the real reasons for financial market fluctuation in order to stabilize it through implementing the suitable steps. In addition, Chuffart (2022) stated that Google searches are known to be a valuable predictor for cryptocurrencies and are able to provide profitable information for portfolio management. Alternatively, during market crisis, the investor or portfolio manager can consider Bitcoin Cash as a safe-haven asset since it receives insignificant effect from Google search and Twitter sentiment variables. At the same time, an investor can undertake web search (Bitcoin, Ethereum, Litecoin, Ripple), news search (Bitcoin), and YouTube search (Ripple) before deciding on investment, especially in times of market turbulence. In consequence, investors can avoid loss and formulate promising investment strategies.

Conclusion

In our empirical analysis, we measured the implication of Google searches on digital assets’ volatility. The user attention measured by the Google trend significantly affects digital assets markets compared with user sentiment on Twitter. Google search activity is a significant factor influencing the decision of investors to buy or sell digital assets. Nowadays, an investor can easily obtain and gather enlightening information from Google search and, at the same time, make an investment decision. To the best of our knowledge, this paper documents the important indication regarding the impact of Google search activities such as news search, web search, and YouTube search separately on digital assets. As such, we may assist a policymaker in the US in encouraging the use of digital assets to develop strategies to lessen digital assets price volatility. Furthermore, during times of market turmoil, investors can be assisted in decision-making after observing the relationship between Google search variables and digital assets prices. The users’ observation can also be used to predict stock market’s volatility such as in S&P 500, Nikkei 225, and FTSE 100. The limitation of this study is that we only analysed the six digital asset prices of Bitcoin, Bitcoin Cash, Ethereum, Ethereum Classic, Litecoin, and Ripple from the coinmarketcap database, although there are many other digital assets in the market.

Data availability

Data for digital assets price were collated from Coinmarketcap which is available in a publicly accessible repository as the following link: https://coinmarketcap.com or Cryptocurrency Prices, Charts And Market Capitalizations | CoinMarketCap. Data for user tweets on Twitter was sourced using the Twitter search Application Programming Interface (API). Data for Google trend was collected using RStudio software. Both data are included in this published article (and its supplementary information files).

Notes

The variables in this study had to be renormalized because the sentiment and Google trend data were highly volatile compared with other variables. The Z-transformation was used to standardize all the time series: Zt = (Xt−μx)/σx, where μx and σx are defined as the mean and standard deviation of each time series, respectively. Due to the equal scale and variance of all the data, researcher were able to quantify the effects of the changes in numerical analysis (Garcia et al. 2015).

References

Aalborg HA, Molnár P, De Vries JE (2019) What can explain the price, volatility and trading volume of Bitcoin? Finance Res Lett 29:255–265. https://doi.org/10.1016/j.frl.2018.08.010

AlKhatib M, El Barachi M, AleAhmad A, Oroumchian F, Shaalan K (2020) A sentiment reporting framework for major city events: case study on the China-United States trade war. J Clean Prod 264:121426–121439. https://doi.org/10.1016/j.jclepro.2020.121426

Anastasiou D, Ballis A, Drakos K (2021) Cryptocurrencies’ price crash risk and crisis sentiment. Financ Res Lett 42:101928–101933. https://doi.org/10.1016/j.frl.2021.101928

Araya V, Quezada M, Poblete B, Parra D (2017) Gaining historical and international relations insights from social media: spatio-temporal real-world news analysis using Twitter. EPJ Data Sci 6(25):1–35. https://doi.org/10.1140/epjds/s13688-017-0122-8

Aslanidis N, Bariviera AF, López Ó (2022) The link between Bitcoin and Google trends attention. Finance Res Lett 47:102654–102662. https://doi.org/10.1016/j.frl.2021.102654

Baker M, Wurgler J (2006) Investor sentiment and the cross-section of stock returns. J Finance 61(4):1645–1680. https://doi.org/10.1111/j.1540-6261.2006.00885.x

Bermingham A, Smeaton AF (2011) On using Twitter to monitor political sentiment and predict election results. Proceedings of the workshop on sentiment analysis where AI meets psychology, AFLNP, 2011

Bollen J, Huina M, Xiaojun Z (2011) Twitter mood predicts the stock market. J Comput Sci 2(1):1–8. https://doi.org/10.1016/j.jocs.2010.12.007

Bourghelle D, Jawadi F, Rozin P (2022) Do collective emotions drive Bitcoin volatility? A triple regime-switching vector approach. J Econ Behav Organ 196(2):294–306. https://doi.org/10.1016/j.jebo.2022.01.026

Chang CY, Lo CC, Cheng JC, Chen TL, Chi LY, Chen CC (2021) Relationship between Bitcoin exchange rate and other financial indexes in time series. Math Probl Eng 8842877:1–9. https://doi.org/10.1155/2021/8842877

Chen C, Liu L, Zhao N (2020) Fear sentiment, uncertainty, and Bitcoin price dynamics: the case of COVID-19. Emerg Mark Finance Trade 56(10):2298–2309. https://doi.org/10.4324/9781003214687-12

Chuffart T (2022) Interest in Cryptocurrencies predicts conditional correlation dynamics. Finance Res Lett 46:102239–102246. https://doi.org/10.1016/j.frl.2021.102239

Deng S, Sinha AP, Zhao H (2017) Adapting sentiment lexicons to domain-specific social media texts. Decis Support Syst 94:65–76. https://doi.org/10.1016/j.dss.2016.11.001

Dizaji FS (2019) Trade openness, political institutions, and military spending (evidence from lifting Iran’s sanctions). Empir Econ 57(6):2013–2041. https://doi.org/10.1007/s00181-018-1528-2

Ding D, Guan C, Chan CML, Liu W (2020) Building stock market resilience through digital transformation: using Google trends to analyze the impact of COVID-19 pandemic. Front Bus Res China 14(21):1–21. https://doi.org/10.1186/s11782-020-00089-z. 3

Dowling NA, Corney T, Hoiles L (2009) Financial management practices and money attitudes as determinants of financial problem and dissatisfaction in young male Australian workers. J Financ Couns Plan 20(2):5–13. https://ssrn.com/abstract=2222945

Elbagir S, Jing Y (2019) Language Toolkit and VADER sentiment. Proc Int Multi Confer Eng Comp Scient 0958:12–16

Fama EF (1970) Efficient capital markets: a review of theory and empirical work. J Finance 25(2):383–417. https://www.jstor.org/stable/2325486

Feng M, Zhe S, Qing B, Xin W, Roger HL, Chiang (2018) How does social media impact Bitcoin value? A test of the silent majority hypothesis. J Manag Inf Syst 35(1):19–52. https://doi.org/10.1080/07421222.2018.1440774

Fuller WA (2009) Introd statist time series. John Wiley and Sons, New York

Garcia D, Tessone CJ, Mavrodiev P, Perony N (2014) The digital traces of bubbles: feedback cycles between socio-economic signals in the Bitcoin economy. J R Soc Interface 11(99):1–8. https://doi.org/10.1098/rsif.2014.0623

Garcia D, Schweitzer F, Garcia D (2015) Social signals and algorithmic trading of Bitcoin. R Soc Open Sci 2(9):1–19. https://doi.org/10.1098/rsos.150288

Granger C (1969) Investigating casual relations by econometric models and cross-spectral methods. Econometrica 37(3):424–438. https://doi.org/10.2307/1912791

Han WP, Youngjoo L (2019) How are Twitter activities related to top Cryptocurrencies’ performance? Evidence from social media network and sentiment analysis. Drustvena Istrazivanja 28(3):435–460. https://doi.org/10.5559/di.28.3.04

Hajam AB, Dilip K, Shiljas K (2021) Investor attention and herding in the Cryptocurrency market during the COVID-19 pandemic. Appl Finance Lett 10:67–77. https://doi.org/10.24135/afl.v10i.448

Hasan MT (2022) The sum of all SCARES COVID-19 sentiment and asset return. Q Rev Econ Finance 86:332–346. https://doi.org/10.1016/j.qref.2022.08.005

Hutto CJ, Gilbert E (2014) VADER: a parsimonious rule-based model for sentiment analysis of social media text. Proceedings of the 8th international conference on weblogs and social media, ICWSM, 2014

Huerta DT, Hawkins JB, Brownstein JS, Hswen Y (2021) Exploring discussions of health and risk and public sentiment in Massachusetts during COVID-19 pandemic mandate implementation: a Twitter analysis. SSM -Popul Health 15:100851–100860. https://doi.org/10.1016/j.ssmph.2021.100851-100860

Kahneman D, Tversky A (1979) Prospect theory: an analysis of decision under risk. Econometrica 47(2):263–291. https://doi.org/10.2307/1914185

Kaminski J (2014) Nowcasting the Bitcoin market with Twitter signals. Social and information networks. arXiv. https://doi.org/10.48550/arXiv.1406.7577

Katsiampa P, Moutsianas K, Urquhart A (2019) Information demand and Cryptocurrency market activity. Econ Lett 185:108714–108726. https://doi.org/10.1016/j.econlet.2019.108714

Khajavi S, Ghasemi M (2006) Efficient market hypothesis and behavioral finance. J. Financial Res 7(20):49–69. 64

Kim YB, Kim JG, Kim W, Im JH, Kim TH, Kang SJ, Kim CH (2016) Predicting fluctuations in Cryptocurrency transactions based on user comments and replies. PLoS One 11(8):1–17. https://doi.org/10.1371/journal.pone.0161197. 65

Kim Y, Bin LJ, Park N, Choo J, Kim JH, Kim CH (2017) When Bitcoin encounters information in an online forum: using text mining to analyse user opinions and predict value fluctuation. PLoS One 12(5):1–14. https://doi.org/10.1371/journal.pone.0177630

Kristoufek L (2013) Bitcoin meets Google trends and Wikipedia: quantifying the relationship between phenomena of the internet era. Sci Rep 3:1–7. https://doi.org/10.1038/srep03415

Kraaijeveld O, De Smedt J (2020) The predictive power of public Twitter sentiment for forecasting Cryptocurrency prices. J Int Financial Mark I 65:101188–101199. https://doi.org/10.1016/j.intfin.2020.101188.76

Lee JY, Yang YS, Ghauri PN, Park BI (2022) The impact of social media and digital platforms experience on SME international orientation: the moderating role of COVID-19 pandemic. J Int Manag 28(4):100950–100971. https://doi.org/10.1016/j.intman.2022

Li Y, Goodell JW, Shen D (2021) Comparing search-engine and social-media attentions in finance research: Evidence from cryptocurrencies. Int Rev Econ Finance 75:723–746

Lippmann W (2017) Public Opinion. Transaction, New Brunswick and London

Li X, Wang CA (2017) The technology and economic determinants of Cryptocurrency exchange rates: the case of Bitcoin. Decis Support Syst 95:49–60. https://doi.org/10.1016/j.dss.2016.12.001

Liu Y, Tsyvinski A (2018) Risks returns cryptocurrency. Technical report: National Bureau of Economic Research, Cambridge. https://doi.org/10.3386/w24877

Lin ZY (2020) Investor attention and Cryptocurrency performance. Fin Res Lett 40:101702–101711. https://doi.org/10.1016/j.frl.2020.101702

Lodhi S (2014) Factors influencing individual investor behavior: an empirical study of city Karachi. IOSR-JBM 16(2):68–76. https://doi.org/10.9790/487X-16236876

Mai F, Shan Z, Bai Q, Wang X, Chiang RHL (2018) How does social media impact Bitcoin value? A test of the silent majority hypothesis. J Manag Inf Syst 35(1):19–52. https://doi.org/10.1080/07421222.2018.1440774

Mittal A, Goel A (2012) Stock prediction using Twitter sentiment analysis. Int J Sci Res Sci Eng Technol 7(4):265–270. https://doi.org/10.32628/CSEIT217475

Nouri A, Motamedi S, Soltani M (2017) Empirical analysis of the financial behavior of investors with brand approach (case study: Tehran stock exchange). Sci. Ann. Econ. Bus 64(1):97–121. https://doi.org/10.1515/saeb-2017-0007

Öztürk SS, Bilgiç ME (2021) Twitter & Bitcoin: are the most influential accounts really influential? Appl Econ Lett 29(11):1001–1004. https://doi.org/10.1080/13504851.2021.1904104

Papadamou S, Koulis A, Kyriakopoulos C, Fassas AP (2022) Cannabis stocks returns: the role of liquidity and investors’ attention via Google metrics. Int J Financ Stud 10(1):1–11. https://doi.org/10.3390/ijfs10010007

Philippas D, Rjiba H, Guesmi K, Goutte S (2019) Media attention and Bitcoin prices. Fin Res Lett 30:37–43. https://doi.org/10.1016/j.frl.2019.03.031

Pinto-Gutiérrez C, Gaitán S, Jaramillo D, Velasquez S (2022) The NFT hype: what draws attention to non-fungible tokens? Mathematics 10(3):335–348. https://doi.org/10.3390/math1003033

Polasik M, Piotrowska AI, Wisniewski TP, Kotkowski R, Lightfoot G (2015) Price fluctuations and the use of Bitcoin: an empirical inquiry. Int J Electron Commer 20(1):9–49. https://doi.org/10.1080/10864415.2016.1061413

Preis T, Moat HS, Eugene SH (2013) Quantifying trading behavior in financial markets using Google trends. Sci Rep 3:1–6. https://doi.org/10.1038/screp01684

Rao T, Srivastava S (2012) Analyzing stock market movements using Twitter sentiment analysis. International conference on advances in social networks analysis and mining. IEEE

Reis PMN, Pinho C (2020) COVID-19 and investor sentiment influence on the US and European countries sector returns. Invest Manag Financial Innov 17(3):373–386. https://doi.org/10.21511/imfi.17(3).2020.28

Rutkowska A, Kliber A (2021) Say anything you want about me if you spell my name right: the effect of internet searches on financial market. Cent Eur J Oper 29(2):633–664. https://doi.org/10.1007/s10100-019-00665-6

Shen D, Urquhart A, Wang P (2019) Does Twitter predict Bitcoin? Econ Lett 174:118–122. https://doi.org/10.1016/j.econlet.2018.11.007

Si J, Mukherjee A, Liu B, Li Q, Li H, Deng X (2013) Exploiting topic based Twitter sentiment for stock prediction. Annu Meeting Assoc Comput Linguist 2(2011):24–29. https://aclanthology.org/P13-2005

Siriopoulos C, Svingou A, Dandu J (2021) Lessons for Euro markets from the first wave of COVID-19. Invest Manag Financial Innov 18(1):285–298. https://doi.org/10.21511/imfi.18(1).2021.24

Smales LA (2022) Investor attention and cryptocurrency price crash risk: a quantile regression approach. Stud Econ Fin 39(3):490–505. https://doi.org/10.1108/SEF-09-2021-0371

Sprenger TO, Tumasjan A, Sandner PG, Welpe IM (2014) Tweets and trades: the information content of stock microblogs. Eur Financ Manag 20(5):926–957. https://doi.org/10.1111/j.1468-036X.2013.12007.x

Steinert L, Herff C (2018) Predicting altcoin returns using social media. PLoS One 13(12):1–12. https://doi.org/10.1371/journal.pone.0208119

Subrahmanyam A (2008) Behavioural finance: a review and synthesis. Eur Financ Manag 14(1):12–29. https://doi.org/10.1111/j.1468-036X.2007.00415.x

Suardi S, Rasel AR, Liu B (2022) On the predictive power of tweet sentiments and attention on Bitcoin. Int Rev Econ Fin 79:289–301. https://doi.org/10.1016/j.iref.2022.02.017

Süssmuth B (2022) The mutual predictability of Bitcoin and web search dynamics. J Forecast 41(3):435–454. https://doi.org/10.1002/for.2819

Thaler R (1980) Toward a positive theory of consumer choice. J Econ Behav Organ 1(1):39–60. https://doi.org/10.1016/0167-2681(80)90051-7

Tripathi A, Dixit A, Vipul (2022) Liquidity commonality in the cryptocurrency market. Appl Econ 54(15):1727–1741. https://doi.org/10.1080/00036846.2021.1982128

Urquhart A (2018) What causes the attention of Bitcoin? Econ Lett 166:40–44. https://doi.org/10.1016/j.econlet.2018.02.017

Valencia F, Gómez-Espinosa A, Valdés-Aguirre B (2019) Price movement prediction of Cryptocurrencies using sentiment analysis and machine learning. Entropy 21(6):589–601. https://doi.org/10.3390/e21060589

Vidal-Tomás D, Ibañez A(2018) Semi-strong efficiency of Bitcoin Fin Res Lett 27:259–265https://doi.org/10.1016/j.frl.2018.03.013

Wołk K (2019) Advanced social media sentiment analysis for short-term cryptocurrency price prediction. Expert Syst 37(2):1–16. https://doi.org/10.1111/exsy.12493

Yu JH, Kang J, Park S (2019) Information availability and return volatility in the Bitcoin market: analysing differences of user opinion and interest. Inf Process Manag 56(3):721–732. https://doi.org/10.1016/j.ipm.2018.12.002

Zhang X, Fuehres H, Gloor PA (2011) Predicting stock market indicators through Twitter “I hope it is not as bad as I fear. Procedia Soc Behav Sci 26(2007):55–62. https://doi.org/10.1016/j.sbspro.2011.10.562

Zhang W, Wang P, Li X, Shen D (2018) Quantifying the cross-correlations between online searches and Bitcoin market. Phys A Stat Mech Appl 509:657–672. https://doi.org/10.1016/j.physa.2018.06.073

Zhang X, Lu F, Tao R, Wang S (2021) The time-varying causal relationship between the Bitcoin market and internet attention. Financial Innov 7(66):5083–5102. https://doi.org/10.1186/s40854-021-00275-9

Acknowledgements

This research was funded by the “Yayasan Tun Ismail Ali (YTI-UKM) Endowed Chair” under the grant EP-2018-009 and “The APC was funded by the Faculty of Economics and Management, Universiti Kebangsaan Malaysia”.

Author information

Authors and Affiliations

Contributions

All authors participated in designing the research and were involved in subsequent revisions. The first author was involved in the gathering, analysing, and interpreting of data for the task. Together with the second author, they drafted the initial manuscript. The first, second, third and fourth author contributed significantly to the idea and design of the study, revision of the work for significant intellectual content, and final approval of the version to be published.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Said, F.F., Somasuntharam, R.S., Yaakub, M.R. et al. Impact of Google searches and social media on digital assets’ volatility. Humanit Soc Sci Commun 10, 885 (2023). https://doi.org/10.1057/s41599-023-02400-8

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-02400-8