Abstract

The Czech Republic has been a promising destination for foreign investors due to its locational advantages and tax-incentive policy. However, the profit-repatriation rate in the country is extremely high, which results in less capital being available for development. This paper studies the differences in profit-repatriation rates among FDI (foreign direct investment) firms in the Czech Republic after the appearance of tax-holiday incentives from 2008 to 2019. The precondition is to find the determinants of the repatriation rate of FDI firms, and the results show that the profit repatriation rate of FDI firms is positively affected by firm size and the liquidity of firms and negatively affected by investment opportunities and leverage. The paper divides FDI firms into several groups and examines the differences in repatriation rates between them before revealing the determinants of these differences. Firstly, there is no difference in profit repatriation between FDI firms with tax incentives and those without tax incentives. Next, we divide the FDI firms with tax incentives into two groups: those who still enjoy the tax incentives and those who no longer enjoy the tax incentives. The FDI firms with tax incentives that are in the tax-incentive period repatriate less than FDI firms with tax incentives that are not in the tax period any longer. The difference stems from the endowment effect, and three determinants that can reduce the repatriation rate of FDI firms that are no longer in the tax period are investment opportunities, leverage, and firm size.

Similar content being viewed by others

Introduction

Foreign direct investment is an important factor that can create many positive effects for host countries, including raising capital, job creation, tax contributions, technological transfer, and spillover effects. Therefore, host countries are now ready to provide generous investment incentives to attract foreign investors. One of the most common instruments is the tax holiday incentive, which gives FDI firms several tax advantages during a certain period. Foreign investors may consider it to be an important determinant of their location decision, in addition to the economic fundamentals of potential host countries (Klemm and Parys, 2012; Sabina and Eldin, 2022; Tobing and Jayadi, 2020). However, when investment incentives become more common and generous, investors may become more footloose and decide to move from one location to another location (Flamm, 1984; McLure Jr, 1999). This type of investor can be seen as rent-seeking, and certainly, hosting countries might be reluctant to welcome such rent-seekers. Because tax incentives are more popular among host countries than others, the main motivation of the paper is to examine the impact of tax incentives on the behavior of FDI firms. It is important to see whether tax incentives attract rent-seekers or long-term investors. Various papers confirm the important role of tax holidays in attracting FDI (Wilson, 1999; Klemm and Parys, 2012; Sabina and Eldin, 2022), but none examine the impact of tax incentives on the behavior of firms after coming to selected locations. Some papers have examined the impact of tax holidays on the performance of firms (Agliardi, 2002; Harris and Li, 2019); however, to the knowledge of the authors, no papers study the difference in the repatriation decisions of FDI firms in the presence or absence of tax holidays. If FDI firms decide to repatriate less of their profits and reinvest in host countries, they are less likely to be rent-seekers. This paper fills the above-mentioned research gap, and the authors expect that the paper will provide empirical evidence regarding the repatriation decisions of FDI firms after the appearance of tax holidays.

As FDI is a good source of development, countries may compete with one another by offering attractive tax incentives. However, from the perspective of host countries, these tax incentives have several costs, including administration fees, the inefficient allocation of capital, tax revenue losses, and more. Therefore, host countries, when they offer tax holiday incentives to welcome FDI, expect that the contributions of FDI firms that have received the tax incentives will be more than these costs. Thus, the paper puts forward an argument from the perspective of the host countries that FDI firms that receive tax holidays are expected to perform better than FDI firms that do not receive this incentive. Additionally, host countries not only expect better performance from FDI firms that recieve a tax holiday as compared to others but also expect such FDI firms to stay and create more value by reinvesting their profits and expanding their businesses. Thus, the first hypothesis of the paper is as follows: supported firms repatriate their profits to a lesser degree than non-supported firms.

Furthermore, tax holidays do not only play an important role in attracting foreign investors. They can directly or indirectly impact the performance and investment decisions of firms. Additionally, several papers have shown that firms have the motivation to invest more during the tax-holiday period (Agliardi, 2002; Azevedo et al. 2019; Lin, 2006). Therefore, we attempt to determine the difference in repatriation rates between FDI firms with the tax incentive that are still in the tax-holiday period and FDI firms with the tax incentive that are not in the tax-holiday period any longer. The second hypothesis of the paper is as follows: supported firms repatriate less profits during the tax-holiday period than after this period.

The paper focuses on the case of the Czech Republic to test the two hypotheses because this country is a common destination for FDI and, at the same time, the repatriation rate there is high. The repatriation rate, which can be presented by the ratio between dividend repatriation and GDP, is 5.739% in the Czech Republic (2019), which is higher than in most OECD countries (Annex A).

To test the two hypotheses, the paper divides FDI firms into two groups: those with and without tax-holiday incentives. Then, the FDI group with tax-holiday incentives is divided into two subgroups, specifically FDI firms that are still in the tax-holiday period and FDI firms that are no longer in the tax-holiday period. By using the Blinder-Oaxaca decomposition method, the first hypothesis is tested by comparing the first two groups, and the second hypothesis is tested by comparing the two subgroups. The paper not only points out the differences in repatriation rates between the groups and subgroups but also shows the determinants of the differences in repatriation rates among FDI groups. It helps to identify factors that can be used to reduce the repatriation rate. To do so, before testing the two hypotheses, it is also necessary to examine the impact of the determinants of the repatriation rate of FDI firms by applying a fixed-effects model with instrumental variables.

Generally, the paper finds that FDI firms that received the tax incentives and FDI firms that did not receive the tax incentives do not engage in different behavior in terms of repatriating their profits. However, among FDI firms with tax incentives, those that are still in the tax-incentive period repatriate less than those that are no longer in the tax-incentive period. The difference stems from the endowment effect between the two groups. Moreover, among the endowments, three determinants that reduce the repatriation rate of FDI firms that are no longer in the tax-incentive period are investment opportunity and leverage and firm size.

The paper is constructed as follows. Section 2 provides the background of the paper and develops the hypotheses. Section 3 describes the methodology used to solve the problem. It is followed by the Results and Discussions section, which reveals the main findings and implications of the paper in Section 4. The final section concludes the paper.

Background and hypothesis development

Theoretical background

This paper examines the behavior of foreign firms after the appearance of tax incentives offered by the host countries. The behavior is seen from the perspective of dividend-payout policy. There are two main issues here: why tax incentives are important and why FDI firms may behave differently after the appearance of tax incentives. The argument can be backed by two theories: the eclectic-paradigm and dividend theories.

The importance of tax can be seen based on the eclectic paradigm. The eclectic paradigm has been one of the leading theories of the development of multinational corporations (MNCs) and globalization (Dunning, 1988). Multinational corporations have ownership advantages (O; brand, rights skills, technology, or management skills) that create their competitive advantages over rivals, and they want to utilize them to establish production in a new location. This new location is attractive because of its location advantages (L), including geographical location, cheap workers and raw materials, tax incentives, or a lack of tariffs. Then, MNCs must consider the internalization advantages (I) to decide whether it is more profitable to produce a particular product in house or create a contract with a third party. Of the three OLI advantages, O and I are more likely to belong to MNCs, and only the L advantage is a tool that host countries can use to attract new foreign investors to their countries. Thus, the paper focuses on the L factor in the eclectic paradigm, more specifically the role of tax incentives offered by host countries. In the past, tax incentives have been underestimated as compared to other fundamental economic conditions of host countries. However, this factor is becoming more important as more and more papers highlight its role (Klemm and Parys, 2012; Sabina and Eldin, 2022; Wilson, 1999).

Next, the differences in dividend policy among firms are explained from the perspective of dividend theories. In dividend theories, there are two major types of financial decisions for firms: investment and financing decisions. After a company generates profits, it can decide to pay out or reinvest the profits, or it can decide to distribute the profits between reinvestment and payout dividends. The dividend policy can be stable (the stable dividend theory), which requires the dividend payout to be the same in every accounting period. According to Baker and Powell (2009), managers may believe that a stable dividend policy can lead to high share prices, and shareholders may expect a stable income source given their frequent consumption. From other perspectives, dividend payouts can be seen as residual or leftover earnings (the residual theory of dividends). This implies that the dividend amount should not be the main focus of corporations; rather, it is simply a leftover from net income and the retained earnings that are required to finance new investments (Brigham and Houston, 2004). In a perfect market, Miller and Modigliani (1961) argue in dividend-irrelevance theory, dividend policy is merely a way to manage the return of a firm’s cash flow and does not affect the value of a company. Shareholders should be indifferent to dividends, and therefore, the dividend policy of firms is irrelevant. However, the market is certainly not perfect. Therefore, the dividend-relevance theory states that dividend policy is relevant and must result from market imperfections. There are three major imperfections outlined in dividend-relevance theory, which are taxes, asymmetric information, and agency costs. This paper pays the most attention to the effect of taxes on the dividend decisions of firms. The theoretical framework for the effect of taxes on the dividend decisions of firms can be anchored by the tax preference theory. This theory holds that investors may have different expectations after the appearance of tax and, therefore, firms must change their dividend policies. Because the tax effect differs between different types of investors, the decision about dividend policy can affect the attractiveness of firms in the eyes of investors. Another theory that explains the behavior of firms is the agency theory. The managers of firms may behave in their own interests, rather than in the shareholders’ interests (Jensen and Meckling, 1976). They may decide to retain the earnings and use the money to do something else, rather than paying out dividends to shareholders. One motivation is that the managers may see a chance to gain additional profit from the current profits, rather than repatriating the profits to the shareholders, and then decide to reinvest in the host countries. One way to gain profit is to make use of the tax conditions in the investing countries. Overall, the theories show that the dividend policy of firms may be affected by several factors. This paper considers the tax conditions of the host countries. More specifically, the tax incentives offered by host countries can affect the dividend policies of firms (Brigham and Houston, 2004).

Hypothesis development

There is an argument that MNCs decide to invest in a specific location because of the strong economic fundamentals in that location (Dunning, 1993; Globerman and Shapiro, 2003, 1999 Blomström et al. 2003) and investment incentives are simply a minor determinant of FDI decisions. The primary motivations of MNCs include access to natural resources, market-seeking, efficiency-seeking, and strategic-asset-seeking. However, perspectives on the importance of investment incentives changed recently when various hosting countries began offering incentives to attract FDI. The most common incentive that developing countries offer is incentive schemes regarding tax holidays. Unlike other direct financial subsidies, tax holidays can affect operational decisions regarding FDI for several years. Given internationalization and regional integration, MNCs can set up international production and supply all clients from a single location. Therefore, locational advantages become relatively less important as compared to investment incentives, including tax holidays.

Various papers confirm the important role of tax holidays in attracting FDI. Wilson (1999) argues that given perfectly mobile capital, higher tax rates lead to a decrease in returns on capital at one location; then, the capital relocates. Therefore, using tax incentives to lower tax rates in one country can help attract FDI to that country. Klemm and Parys (2012) examine the impact of tax incentives on attracting FDI from 1985 to 2004 and conclude that lower corporate income tax and longer tax holidays have positive effects on FDI in Latin America and the Caribbean. Sabina and Eldin (2022) point out that tax policy is an important determinant of FDI in some Southeast European countries (studied in the 2000–2018 period), but the effect of the tax policy varies depending on the level of technology in the host countries. This suggests that a smaller difference in the level of technology between home and host countries may lead to lower importance on the part of tax incentives. Moreover, Sabina and Eldin (2022) argue that taxation affects the cost structures of FDI and, thus, investment decisions. Similarly, Tobing and Jayadi (2020) find a positive correlation between FDI inflow and tax holidays only in the long term in their study of Indonesia from 1975 to 2016. However, this relationship is not detected in the short term. From another viewpoint, tax incentives can be a signal from host countries to show a higher level of acceptance of foreign players in the markets (Munongo et al. 2017). Generally, the role of tax incentives is becoming more important as more countries use them to attract the attention of MNCs.

When they receive tax incentives, FDI firms are expected to perform better than those without investment incentives. The tax reduction achieved through a decrease in the user cost of capital makes investments increase (Klemm and Parys, 2012). Taxation may also affect the cost structure of investment of firms, and tax incentives are aimed at encouraging investment and economic growth (Sabina and Eldin, 2022). Therefore, FDI firms that receive tax incentives are expected to have more chances to earn high profits, and consequently, they are expected to reinvest their profits in host countries, rather than repatriating them to parent companies (Forti et al. 2015; Mrzygłód et al. 2021).

However, when investment incentives become more common and generous, investors may become more footloose and decide to move from one location to another location to earn more benefits (Flamm, 1984; McLure Jr, 1999). This type of motivation can be seen as rent-seeking. Certainly, no governments want to attract rent-seeking investors that only arrive to make use of policy privileges and do not have many positive impacts on the local economy. When a government offers tax holidays for specific MNCs, they expect that these MNCs will bring capital flow to the host country, create new jobs, transfer management and technological skills, and have other promising externalities (Moosa, 2002). Additionally, tax incentives have certain other costs, including administration fees, the inefficient allocation of capital, and tax revenue losses (Fowowe, 2011). Tiebout (1956) points out that the use of tax incentives involves the inefficient provision of public goods, which represents an expense. Certainly, when attracting and offering privileges to certain FDI firms, the host country expects that the benefits from these firms will outweigh the cost of offering the investment incentives. This can only happen when foreign firms, after receiving investment incentives, decide to remain and reinvest in the host countries. Otherwise, investment incentives may be not effective, and host countries may lose capital for accumulation and reinvestment, which may negatively affect capital flow for these countries (Akkermans, 2017).

Despite the importance of tax incentives, to the knowledge of the authors, existing papers only examine the impact of tax incentives on the location decisions of FDI firms. No papers empirically study the difference in repatriation decisions between FDI firms with and without tax incentives. Therefore, the authors of the paper argue that because tax holidays play an important role in the location decisions of FDI firms, host countries can expect that FDI firms that have received tax holidays will perform better than FDI firms that have not received these investment incentives and that, consequently, the former may reinvest their profits in host countries.

H1: Supported firms repatriate less profits than non-supported firms.

A variety of papers examine the effect of tax incentives on the performance of firms in general and FDI firms specifically. Harris and Li (2019) consider Chinese firms from 1998 to 2007 and conclude that assisted firms contribute to TFP (total factor productivity) growth more heavily than non-assisted firms. Huang (2015) studies the impact of tax policy on productivity in Taiwan from 2001 to 2008 and shows the positive and statistically significant influence of tax credits on the productivity of Taiwanese firms in the manufacturing sector. Czarnitzki et al. (2011) examine the link between tax credits and innovation activities among Canadian manufacturing firms from 1997 to 1999. The authors conclude that tax credits led to more innovation activities among Canadian firms during this period. Furthermore, Du et al. (2014) investigate the effect of tax and tariff policies on FDI spillovers in China and find that tax holidays enhance the positive externalities of FDI. Aghion et al. (2015) argue that industrial policies, including tax holidays, may encourage firms to be active in specific sectors and, therefore, it can complement competition and speed up innovation and economic growth. This paper uses a dataset of Chinese firms between 1998 and 2007 and shows that industrial policies, including tax holidays, foster competition and increase productivity growth. Nunn and Trefler (2010) suggest that tariff protection may create a “skill bias,” as firms may be pushed toward skill-intensive sectors. Consequently, there is a significant positive correlation between this “skill bias” and productivity growth on the part of firms and sectors. Generally, many papers favor the argument that tax incentives have a positive impact on the performance of firms.

As the main goal of any firm is to generate profit, if tax incentives create more earnings, firms may have an incentive to invest more and earn more profit. More specifically, firms are motivated to recognize revenue during the tax period, and they tend to exaggerate their expenses and losses in the following period to avoid higher tax rates (Lin 2006). Lin (2006) shows that firms increase their income accruals during the tax holiday period, which is consistent with income-shifting behavior. It implies that firms want to have more profits during the tax holiday period by accelerating their final goods, decreasing debt, reducing inventory, or delaying expensive inventory purchasing. Azevedo et al. (2019) show that tax holiday duration has a nonmonotonic effect on the timing of investment and that a long tax-holiday period boosts investment. Agliardi (2002) examines the reinvestment or disinvestment decisions of firms under the impact of tax systems. Agliardi (2002) proves that there are thresholds for reinvestment and disinvestment decisions and that profit tax is one important determinant. Fiscal policies play an ambiguous role, and an increase in profit tax leads to a decrease in the investment incentives of firms. This also implies that firms want to invest more during the period when the profit tax is low (the tax-holiday period). Azevedo et al. (2019) examine reinvestment and disinvestment flexibility under the impact of tax policy, which includes tax holidays. The authors argue that firms may agree not to divest during the tax holiday period and that a long tax holiday may speed up investment. These existing studies show that firms may want to reinvest during the tax holiday, but to the knowledge of the authors of this paper, no papers compare the investment behavior of FDI firms during and after the tax period. Thus, we argue that during the tax-holiday period, firms may want to reinvest their profits and thus gain more profit via the incentives. However, when the tax-holiday period ends, they may want to invest less, which leads to a higher repatriation rate.

H2: Supported firms repatriate less profits during the tax-holiday period than after this period.

The paper tests the two above hypotheses in the case of FDI firms in the Czech Republic because of the following reasons: the Czech Republic has been one of the most promising destinations for foreign investors, as a leading country in the V4 group, and the ratio of FDI stock to GDP has increased by six-fold since 1993 (Szabo, 2019). One of the reasons for this is that the Czech government has created favorable conditions to attract FDI in the form of both greenfield and brownfield investments. Furthermore, repatriated profits in the Czech Republic are high, as can be seen in Annex B. The ratio between dividend repatriation and the GDP of the Czech Republic stands in fifth place among OECD countries. For all these reasons, the repatriation rate for FDI firms after the appearance of tax holidays is worth studying.

One important point is that before examining the differences in the repatriation rate of FDI firms to investigate Hypotheses 1 and 2, it is necessary to identify the determinants of repatriation rates. In this regard, it helps to point out the factors that contribute to the differences in the repatriation rates of FDI firms. The size and age of firms are the most common determinants of dividend decisions. The agency theory shows that large and old firms are more likely to pay more dividends on average (Brawn and Šević, 2018; Forti et al. 2015). Age can be seen as representing the market strength and development of firms. A higher value for age means a longer period of competition and a better understanding of the host market (Mrzygłód et al. 2021), and such firms thus become more cash abundant. Another important factor is profitability, which can be represented by return on assets (ROA) or return on equity (ROE). This is the most obvious factor in this regard because only profitable firms are able to decide to repatriate or reinvest their profits (Fama and French, 2002; Jabbouri, 2016). Firms may increase their dividend payments when they have more profit to avoid retaining earnings. The next factor is investment opportunity (Boţoc and Pirtea, 2014; Faccio et al. 2001; Mitton, 2004), and it is clear that if firms see a profitable opportunity, they will be more likely to reinvest their profits to earn more in the future. Therefore, the repatriation rate will be lower. Finally, the paper examines the impact of the liquidity and leverage of firms on repatriation rates. These determinants are widely used in the literature. Various previous papers show a negative relationship between leverage and dividend payment, as firms with high levels of debt tend to lower their dividend payment and use cash to meet their debt obligations (Crutchley and Hansen, 1989; Gugler and Yurtoglu, 2003). Additionally, when firms plan to access credit markets, they tend to cut dividends to increase the confidence of their creditors and show a low agency cost for their debts (Mather and Peirson, 2006; Nini et al. 2009). In terms of liquidity, it is considered one of the most important factors in the repatriation rate because firms are unable to pay dividends if they are experiencing levels of cash liquidity that are too low. Therefore, various studies describe the relationship between firm liquidity and dividend payouts (DeAngelo et al. 2004; Deshmukh, 2003; Khang and King, 2006).

Generally, the paper examines the impact of age, size, liquidity, leverage, profitability, and investment opportunities on the repatriation rates of FDI firms. As these variables potentially affect the repatriation rate, they can lead to the differences in repatriation behaviors outlined in Hypothesis 1 and Hypothesis 2. The conceptual framework of this research project is as shown in Fig. 1.

The paper examines the impact of age, size, liquidity, leverage, profitability, and investment opportunities on the repatriation rates of FDI firms. As these variables potentially affect the repatriation rate, they can lead to the differences in repatriation behaviors outlined in Hypothesis 1 and Hypothesis 2.

Methodology

As can be seen in the conceptual framework, the two main hypotheses can be tested by using the Oaxaca-Blinder decomposition. However, before testing the hypotheses, it is necessary to identify the determinants of the repatriation decision. Otherwise, it is not possible to find the sources of the differences in dividend policy among FDI firms. The details are as follows:

The paper begins with a comparison of the mean difference in profit repatriation among groups by running a regression of profit repatriation on the dummy variables Support and Tax_period. This approach can provide initial findings regarding the differences among groups, but it is unable to show the components of these differences. Therefore, it is necessary to estimate the determinants of profit repatriation before examining the contributions of these determinants to these differences.

The main determinants of the repatriation rate of FDI firms in the Czech Republic are found by estimating the following equation:

where X is a set of the determinants of repatriation that have been used widely in the literature, including the Age and Size of firms (Al-Najjar and Kilincarslan, 2017; Brawn and Šević, 2018; Labhane, 2017; Mrzygłód, U. et al. 2021), Liquidity, Leverage, Profitability, and Investment Opportunities. ROA (return on assets) represents the profitability of firms, and Asset growth represents investment opportunities for FDI firms.

Equation 1 is estimated by applying the fixed-effects model with instrumental variables to the entire sample after using the Hausman test to reject the validity of the random-effects model (the Chi-square result of the Hausman test is 61.41, and the p-value is 0.000, which shows that the fixed-effects model is preferable in this case). The fixed-effects model allows a correlation between the error term and covariates, while the random-effects model strictly requires that there is no correlation between them. Therefore, the fixed-effects model is more realistic than the random-effects model. The fixed-effects model helps in resolving potential omitting-variables bias, which will be absorbed by \(\alpha _{{{\mathrm{i}}}}\). In this paper, \(\alpha _{{{\mathrm{i}}}}\) captures firm- and industry- (NACE) fixed effects; therefore, using the fixed effect model can help control for the heterogeneity of firms. The instrumental variables resolves the endogeneity problems created by using Liquidity and Leverage, as these two determinants that can affect repatriation rates and repatriation rates can affect these two factors as well (simultaneity). The paper uses the lag value of the two variables as instrumental variables because using lagged variables is a way to avoid simultaneity and resolve endogeneity (Reed, 2015). The paper investigates the validity of the instrumental variables by using Stock and Yogo criteria values. The results show that the instrumental variables are not weak (Annex C). Then, we run the regression on each sub-sample. First, the paper divides the entire sample into FDI firms that received tax incentives and FDI firms that did not receive tax incentives. Then, the group of FDI firms with tax incentives are divided into two sub-groups, specifically FDI firms that are in the tax-incentive period and FDI firms that are not in the tax-incentive period.

After that, we test the two main hypotheses by applying the Blinder-Oaxaca decomposition to panel data, which is based on the methodology of Kroger and Hartmann (2021). The decomposition with panel data shows group differences by levels and changes. The decomposition of levels shows the differences between groups at certain specific time points, while the decomposition of changes examines the differences between groups across time.

Decomposition of levels

The decomposition of levels can be applied to cross-sectional data at a specific time by using the original Kitagawa-Oaxaca-Blinder (KOB) decomposition. The outcome (Y) of groups A and B depends on covariates X as follows:

where l is group A or B, E(εi) = 0, and Cov (X,ɛ) = 0. Y is the repatriation rate, and X is the set of independent variables, as in Eq. 1. The KOB method decomposes the difference in the mean outcome of the two groups as follows:

It transforms to the following:

where

Et is the endowment effect, which explains the differences in the group’s characteristics at time t. Ct is the coefficient effect, which shows the differences in the coefficients at time t, and It is the interaction effect, which can be seen as an unexplained part of the mean difference between group A and group B. This decomposition is created from the viewpoint of group B when the endowment effect is weighted by the coefficients of group B and the coefficient effect is weighted by the endowment of group A. Et shows the expected change in the mean output of group B if group B has the same endowment as group A at time t, and Ct measures the expected change in the mean output of group B if it has the same coefficient as group A at time t.

Decomposition of changes

The decomposition of changes measures the change in the outcome difference between group A and group B across times t and s:

This change in gaps then can be decomposed into the following parts:

where

\({\Delta}{{{\mathrm{E}}}}\) shows that given the difference in the coefficient between groups A and B, the change in group output is explained by the endowment change within groups from time s and t. \({\Delta}{{{\mathrm{C}}}}\) shows that given the initial endowment difference between the groups at time s, the change in group output is explained by the coefficient change within a group from time s to time t. is an unexplained part of the output difference between groups A and B from time s to time t.

Note that when using panel data, the time-constant individual error term can be added to Eq. 2 as follows:

Then, there is another component of the difference between the time-constant individual error terms of groups A and B: \({\Delta}\alpha = {{{\mathrm{E}}}}\left( {\alpha ^{{{\mathrm{A}}}}} \right) - {{{\mathrm{E}}}}\left( {\alpha ^{{{\mathrm{B}}}}} \right)\). In the case of the random-effects model, the impact of \({\Delta}\alpha\) on the difference should be 0, as the consumption of the random-effects model is Cov(\(\alpha ^{{{\mathrm{l}}}},{{{\mathrm{X}}}}_{{{\mathrm{t}}}}^{{{\mathrm{l}}}}\)) = 0.

Data

The paper exploits the panel data derived from the financial statements of FDI firms in the Czech Republic from 2008 to 2019 using the CRIBIS database. The reason for using this period is that it is a 10-year period that covers the financial crisis period from 2008 to 2012 and it can fully capture the behavior of FDI firms over time. The total number of observations is 7669, which includes 3142 year-observations of FDI firms that received tax incentives when they began running a business in the Czech Republic and 4,527 year-observations of FDI firms that did not receive tax incentives when they started. The information about tax incentives has been collected manually from the Ministry of Trade and Investment. The dummy variable Support is constructed based on this information. It has a value of 0 for firms without tax incentives and 1 for firms with tax incentives. Additionally, this paper makes use of the information about the tax-incentive period for each FDI firm with a tax incentive to create the dummy variable Tax_period. For example, one firm received tax incentives from 2005 for 10 years; then, in 2017, it is not in the tax incentive period any longer, and the Tax_period dummy has a value of 0. This paper is the first to make use of this information in the Czech Republic. Among 3142 observations of FDI firms that have received tax incentives, 1555 year-observations are still in the tax-incentive period, and 1587 year-observations are not in the tax-incentive period any longer. This implies that one firm can be in the tax-incentive period in 2008, but then, in 2009, it may not be in the tax-incentive period any longer, because the tax period ends in 2008. The main reason for dividing the samples into groups instead of constructing an indicator for having tax incentives or not or still being in the tax-incentive period or not is because the duration of the tax-incentive period in the Czech Republic has changed from 2008 to 2019. Additionally, by dividing the samples into groups, the decomposition can be applied properly.

As the main purpose of the paper is to examine the profit repatriation rate of FDI firms in the Czech Republic, Y in Eq. 2 is the ratio of dividend to net earnings of FDI firm i at time t, and X is a set of independent variables. The constructions of these variables are shown in Table 1. The variables‘ description can be seen in Annex B. Other variables are calculated from the CRIBIS database, which includes information about the financial statements of firms in the Czech Republic. All variables are checked for stationarity via the Im-Pesaran-Shin unit root test for unbalanced panel data (see Annex D).

Results and discussion

Models 1 and 2 show the results of the regression of profit repatriation on the dummy variables Support and Tax_period, respectively (Table 2). The results of Model 1 imply that the mean difference in profit repatriation for supported and non-supported firms is 1.5305 and that it is not statistically significant. Therefore, there is no difference in repatriation behavior between these two groups. However, among firms that were supported when they began, there is a difference in profit repatriation between those that are still in the tax-incentive period and those that are not in the tax-incentive period any longer. Firms that are in the tax-incentive period repatriate less than firms that are not in the tax-incentive period. The coefficient is statistically significant at the 5% level. At this stage, Models 1 and 2 only compare the mean difference in profit repatriation among groups; they are unable to show the components of the differences. Therefore, this paper estimates the determinants of profit repatriation before examining the contributions of these determinants to the difference in repatriation.

Models 3 to 7 estimate the impacts of key determinants on the profit repatriation of FDI firms in the Czech Republic by using a fixed-effects model (Table 3). Model 3 shows that the profit repatriation of FDI firms depends on Leverage, Liquidity, Investment Opportunity, and Firm size. Liquidity and Firm size affect the profit-repatriation rate of FDI firms in the Czech Republic positively, while Leverage and Investment opportunities have negative impacts. More specifically, a 1% increase in the Liquidity of firms leads to a 0.1803% increase in the repatriation rate of FDI firms. This is equivalent to the results of Das (2017) and Jabbouri (2016) and confirms the importance of the liquidity of firms in the repatriation decisions of FDI firms in the Czech Republic. The positive and significant coefficient of Firm size implies that bigger firms tend to repatriate much more than smaller firms. Large firms are more mature and can access capital markets for financial sources more easily than small firms; thus, they are able to pay higher dividends. This is equivalent to the transaction cost theory (Holder et al. 1998; Koch and Shenoy, 1999). Moreover, a 1% increase in Leverage leads to a 0.1135% decrease in the repatriation rates of FDI firms. Firms with a higher level of debt pay fewer dividends (Faccio et al. 2001; Jabbouri, 2016). Higher debt may make firms riskier and more dependent on retained earnings (Hufft and Dufrene, 1996); thus, cash may be used to pay for debt rather than dividends. In terms of investment opportunities, the coefficient is negative and statistically significant, as in previous papers (Mitton, 2004; Mrzygłód et al. 2021; Porta et al. 2000). This suggests that if firms sense more profitable opportunities, they might want to reinvest and thus earn more profits rather than repatriate their profits as dividends. Put differently, investment opportunities can exhaust the cash resources that could be used to pay dividends (Faccio et al. 2001). The coefficients of Age and ROA are not statistically significant. This suggests that firm age and profitability do not influence repatriation rates among FDI firms in the Czech Republic.

We also run the estimation with four sub-samples, which are FDI firms with tax incentives, FDI firms without tax incentives, FDI firms with tax incentives that are still in the tax-incentive period, and FDI firms with tax incentives that are not in the tax-incentive period any longer, in Models 4 to 7, respectively. Models 4 and 5 are comparable because they are sub-samples of Model 1. Models 6 and 7 are comparable because they are sub-samples of Model 4 and FDI firms with tax incentives when they began are divided into two groups: firms in the tax-incentive period and firms not in the tax incentive period any longer.

Models 4 and 5 show that the profit repatriation of FDI firms with and without tax incentives when they began depends on various determinants. In the case of FDI firms with tax incentives when they began, the leverage, liquidity, investment opportunity, and size of firms are the significant determinants, while in the case of FDI firms without tax incentives, the determinants are age, leverage, liquidity, and investment opportunity.

Similarly, Models 6 and 7 show the various determinants of profit repatriation among FDI firms that were in the tax-incentive period and firms that were not in the tax-inventive period any longer. The decisions of the former depend on leverage, liquidity, investment opportunity, and firm size, and the decisions of the latter depend on liquidity, firm size, and investment opportunity.

Next, the paper applies the Blinder-Oaxaca method to decompose the difference in profit repatriation among firms. Firstly, the authors examine the difference between FDI firms with tax support and FDI firms without tax support when they began. Secondly, a similar approach is applied to FDI firms that are in the tax-incentive period and FDI firms that are not in the tax-incentive period. All these firms received tax incentives when they began, but some are not in this period any longer.

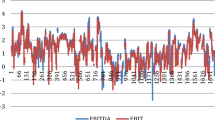

Table 4 shows the decomposition of profit repatriation into the composition of levels and the composition of changes. The paper takes 2008 as a reference year to compare with 2014 and 2018, as the differences in these years are the most visible (Fig. 2). The upper part of Table 4 shows the composition of levels, which considers the difference between firms in each year, 2008, 2014, and 2018, and the lower part shows the changes in these differences over the year. The results imply that there are no differences in repatriation decisions between supported and non-supported firms in terms of levels or changes.

The blue line is the average profit repatriation rate of FDI firms which are still in the tax incentive period and the orange line is the average profit repatriation rate of FDI firms which are no longer in the tax incentive period. The differences can be seen clearly in 2008, 2014 and 2018. Source: Authors.

The results from Table 4 disprove the first hypothesis and show that the repatriation rate of FDI firms with tax incentives is not significantly different from that of FDI firms without tax incentives. The behavior of these two groups in terms of profit repatriation is not different. In fact, many authors agree that tax incentives only play a minor role in the investment decisions of FDI firms. In some cases, tax incentives can negatively impact FDI inflows. For example, Klemm and Parys (2012) only find a positive impact on the part of tax holidays in Latin America and the Caribbean; the authors do not find such an impact in African countries. Hsu et al. (2019) use province-level data from 1998 to 2008 and cannot find a statistically significant relationship between tax-incentive policies and FDI inflow in China. Similarly, Fowowe (2011) also finds a negative link between tax incentives and FDI in Nigeria from 1970 onward. Another explanation for this result on our part is that many FDI firms in the Czech Republic do not receive tax holidays from the Czech government but do receive another kind of support directly from the European Union. Therefore, the benefits derived from tax holidays can offset the benefits of support from the EU, and consequently, unassisted firms decide to reinvest/repatriate at a similar rate as assisted ones.

However, the difference is detected between firms that are in the tax-incentive period and firms that are not in the tax-incentive period. Therefore, the second hypothesis is confirmed. Moreover, the difference occurs each year and does not change significantly over the years. This is why the coefficients in the lower section are not statistically significant. It implies that FDI firms that are in the tax-incentive period repatriate less than FDI firms that are not in the tax-incentive period and that the difference remains unchanged over the years.

This paper takes a further step and examines the reasons for the difference in repatriation behavior between FDI firms that are in the tax-incentive period and FDI firms that are not in the tax-incentive period. The Oaxaca-Blinder method decomposes the difference into three parts: endowments, coefficients, and the interaction between endowments and coefficients. The endowments part shows the differences in the mean Age, ROA, leverage, liquidity, investment opportunity, and size of FDI firms, while the coefficients part shows the differences in the coefficients, that is, the marginal effect of using these endowments. As the difference occurs but remains unchanged over the observed period, as shown in the lower part of Table 4, the authors treat the panel data as extended cross-sectional data to examine the impact of endowments, coefficients, and interactions.

The results in Table 5 show that FDI firms that are in the tax-incentive period repatriate 9.89% less than FDI firms that are not in the tax-incentive period. The first two rows of Table 5 show the average repatriation rates of FDI firms in the tax-incentive period and FDI firms not in the tax-incentive period. The endowment difference explains more than 50% of this difference in the repatriation rate (5.1754/9.8929 = 0.5227). It is statistically significant at the 0.1% level. About 50% of the difference in the repatriation rate is caused by the coefficients and interaction; however, the coefficients are not statistically significant. Therefore, in this case, we can only detect the impact of endowments.

The lower part of Table 5 shows the decomposition of endowments. The determinants that have the largest impacts are the Age of firms, Investment opportunity, Size of firms, and Liquidity. The positive sign means that if the gap in these variables between the two groups is reduced, then the repatriation gap is decreased and vice versa; the negative sign means that if the gap is reduced then the repatriation gap is increased. All the differences are expressed from the perspective of FDI firms that are not in the tax-incentive period. More specifically, Age contributes 45.28% of the variation (2.3434/5.1754 = 0.4528); Investment opportunity contributes 48.84% (2.5279/5.1754 = 0.4884) of the variation. Next is Leverage, with 27.92% (1.447/5.1754 = 0.2791), and Size, with −40.95% (−2.1191/5.1754 = −0.4995) of the variation. The contributions of ROA and Liquidity are not statistically significant. Therefore, the percentage of 48.84% for Investment Opportunities can be interpreted as follows: if the FDI firms that are not in the tax-incentive period have the same level of Investment Opportunities as FDI firms that are in the tax-incentive period, then the profit-repatriation rate can be reduced by 48.84%. Generally, the model shows that the difference in the repatriation rate can be reduced or increased, depending on the sign of coefficient, if the level of endowments for FDI firms that are not in the tax-incentive period reach the level of endowments for FDI firms that are in the tax-incentive period. Statistically, the repatriation rate of FDI firms that are not in the tax-incentive period can be decreased via Age, the Size of firms, Leverage, and Investment opportunities. However, in reality, it is not possible to affect the Age of a firm, as it increases every year and cannot be adjusted. Therefore, the three determinants that can be used to keep the repatriation rate low are Investment opportunity, Leverage, and the Size of firms.

Investment opportunity is proxied by asset growth, and the mean value of asset growth for FDI firms that are not in the tax-incentive period is lower than that for FDI firms that are in the tax-incentive period. Therefore, the former must increase the growth of their assets to reach the level of the latter, and this process will reduce their repatriation rate, as the relationship between investment opportunity and repatriation rates is negative (Model 7). Generally, these results imply that the investment opportunity for FDI firms that are in the tax-incentive period is higher as compared to others, which may stem directly from conditions regarding tax incentives or other determinants in the host countries, and that if FDI firms that are not in the tax-incentive period have the same opportunity, they will repatriate their profits less. Similarly, if the FDI firms that are no longer in the tax-incentive period can increase their leverage levels to that of FDI firms that are in the tax-incentive period, their repatriation rate will be lower.

Inversely, the sign of the Firm-size coefficient is negative, which means that if the FDI firms that are no longer in the tax incentive period have a size (measured by the logarithm of total assets) similar to that to FDI firms that are in the tax-incentive period, the difference in the repatriation rates between the groups will be increased. Foreign-direct-investment firms in the first group are smaller than FDI firms in the second group, and Model 7 shows that larger firms repatriate more of their profits.

Robustness check

We find that FDI firms that are in the tax-incentive period repatriate less than FDI firms that are no longer in the tax-incentive period. However, as an alternative explanation, the correlation may relate to the lifecycle of firms. In their early stages and during the tax-incentive period, firms have less or no profit to repatriate, and consequently, the repatriation rate is low. Then, when they enter the more stable stages after a few years (and may not be in the tax-incentive period any longer), they gain more profit and repatriate more. If this argument holds, the results of this paper are not robust, and the difference in repatriation rates between firms that are in the tax-incentive period and those that are not in the tax-incentive period may stem from the investment cycle. Therefore, this paper examines the impact of the lifecycle on the repatriation rate in the Czech Republic for firms that received tax incentives. The lifecycle is calculated using patterns regarding operating cash flow, investment cash flow, and financial cash flow. It is based on the methodology of Dickinson (2011). There are five stages: introduction, growth, mature, shakeout, and decline. We create an interaction term between the Tax_period and Stage variables and regress the repatriation rate on this interaction term. The Stage variable is a dummy variable. Then, we adds the Stage variable to Model 4 to test the impact of lifecycle on the repatriation rate of FDI firms with tax incentives. The results can be seen in Table 6.

In Model 8, the base is firms that are not in the tax-incentive period and are in Stage 1 of their lifecycle. Therefore, the coefficient of the interaction term Stage = 2*Tax_period = 1 indicates the difference in the repatriation rate between firms that are in the tax-incentive period and in Stage 2 of the lifecycle as compared to the base of the model. However, none of the coefficients are statistically significant. Therefore, the firm’s lifecycle and the tax-incentive period do not have a joint impact on repatriation rates. Turning to Model 9, the dummy variable Stage is not statistically significant, which implies that lifecycle does not correlate with repatriation rates. Models 8 and 9 show that the repatriation rate is not affected by firm lifecycle or the investment cycle in this case.

Additionally, as the period from 2008 to 2019 covers the global financial crisis, the paper examines the impact of this event. The period from 2008 to 2012 was the crisis period in the Czech Republic. The dummy variable crisis is created, which equals 0 for the year before 2012 and 1 from 2012 onward. Model 10 shows that the interaction term between Tax_period and Crisis is positive but not statistically significant. This implies that the financial crisis does not have any impact on the difference in repatriation rates between the two groups. Next, Model 11 is used to investigate the impact of the interaction term between Tax_period and Crisis with the presence of other control variables, and the model shows similar results. The coefficient of the interaction term is negative but statistically insignificant. Therefore, the difference in repatriation decisions between FDI firms in the tax-incentive period and FDI firms not in the tax-incentive period was not influenced by the financial crisis in the case of the Czech Republic.

Conclusion

This paper examines the repatriation rates of FDI firms in the Czech Republic from 2008 to 2019 by dividing FDI firms into groups: the FDI firms with tax-holiday incentives, FDI firms without tax-holiday incentives, FDI firms with tax-holiday incentives that are still in the tax-holiday period, and FDI firms with tax-holiday incentives that are no longer in the tax-holiday period. The first step was to identify the determinants of the repatriation rate of FDI firms in the Czech Republic. After applying a fixed-effects model with instrumental variables and a Oaxaca-Blinder decomposition, the results of the paper are as follows: the profit repatriation rate of FDI firms is positively affected by Liquidity and Firm Size and negatively affected by Investment Opportunities and Leverage. Next, there is no difference in profit repatriation between FDI firms with tax incentives and those without tax incentives. Finally, FDI firms that are in the tax-incentive period repatriate less than FDI firms that are no longer in the tax-incentive period, and the three determinants that can reduce the repatriation rate of FDI firms that are not in the tax-incentive period are Investment Opportunity, Leverage, and Firm Size.

This paper is unable to examine the difference in the repatriation rates of FDI firms in various tax-incentive-period stages. Further research should divide the tax period into smaller stages, for example, the first 2 years or the first 5 years. Understanding the behavior of FDI firms in different stages within the tax period might be useful.

The repatriation rates of FDI firms with tax incentives in the Czech Republic can be a good lesson for developing and transitioning countries. Foreign direct investment is still a significant capital flow that can help boost the economy of various host countries, and governments continue to use tax holidays as a tool to attract foreign investors. This implies that the situation is becoming more common around the world. Therefore, the repatriated profits of FDI firms in the Czech Republic during tax holidays could serve as a reference for the Czech government and other governments when they consider offering tax incentives to foreign investors. The policy implication is as follows: firstly, even though tax incentives can attract FDI, they are not a good tool via which to keep FDI firms reinvesting their profits in the Czech Republic, as there is no difference in the dividend policy between FDI firms with and without tax incentives. Secondly, as the factors that can help to reduce the repatriation rate of FDI firms that are no longer in the tax-holiday period are Investment Opportunity, Leverage, and the Size of Firms, the government might consider creating more investment opportunities and enhancing the financial market. Additionally, the government might consider providing more support for small and medium-sized firms.

Data availability

The paper makes use of the CRIBIS database, which is not publicly available. The link is https://www3.cribis.cz/login. It requires a subscription to log in.

References

Aghion BP, Cai J, Dewatripont M, Du L, Harrison A, Legros P (2015) Industrial policy and competition. American Economic Journal: Macroeconomics 7:1–32

Agliardi, E (2002). Taxation And Investment Decisions: A Real Options Approach. Australian Economic Papers, (1985)

Akkermans DHM (2017) Net profit flow per country from 1980 to 2009: The long-term effects of foreign direct investment. PLOS ONE 12:1–28. https://doi.org/10.1371/journal.pone.0179244

Al-Najjar B, Kilincarslan E (2017) Corporate dividend decisions and dividend smoothing. International Journal of Managerial Finance 13:304–331. https://doi.org/10.1108/IJMF-10-2016-0191

Azevedo A, Pereira PJ, Rodrigues A (2019) Foreign direct investment with tax holidays and policy uncertainty. International Journal of Finance & Economics 24:727–739. https://doi.org/10.1002/ijfe.1688

Baker, HK, & Powell, G (2009). Understanding Financial Management: A Practical Guide. John Wiley & Sons. Retrieved from https://books.google.cz/books?id=CAunuvnh91EC

Blomström, M, Kokko, A, & Mucchielli, J-L (2003). The Economics of Foreign Direct Investment Incentives. In H Herrmann & R Lipsey (Eds.), Foreign Direct Investment in the Real and Financial Sector of Industrial Countries (pp. 37–60). Berlin, Heidelberg: Springer Berlin Heidelberg

Boţoc C, Pirtea M (2014) Dividend payout-policy drivers: evidence from emerging countries. Emerging Markets Finance and Trade 50:95–112. https://doi.org/10.2753/REE1540-496X5004S407

Brawn DA, Šević A (2018) Firm size matters: Industry sector, firm age and volatility do too in determining which publicly-listed US firms pay a dividend. International Review of Financial Analysis 58:132–152. https://doi.org/10.1016/j.irfa.2018.05.002

Brigham, E, & Houston, J (2004). Fundamentals of Financial Management. South-Western, Ohio: Thomson

Crutchley CE, Hansen RS (1989) A Test of the Agency Theory of Managerial Ownership, Corporate Leverage, and Corporate Dividends. Financial Management 18:36–46. http://www.jstor.org/stable/3665795

Czarnitzki D, Hanel P, Miguel J (2011) Evaluating the impact of R & D tax credits on innovation: A microeconometric study on Canadian firms. Research Policy 40:217–229. https://doi.org/10.1016/j.respol.2010.09.017

Das S (2017) Firm characteristics and dividend policy in India. Transnational Corporations Review 0:1–11. https://doi.org/10.1080/19186444.2017.1362862

DeAngelo H, DeAngelo L, Skinner DJ (2004) Are dividends disappearing? Dividend concentration and the consolidation of earnings. Journal of Financial Economics 72:425–456. https://doi.org/10.1016/S0304-405X(03)00186-7

Deshmukh S (2003) Dividend initiations and asymmetric information: A hazard model. Financial Review 38:351–368. https://doi.org/10.1111/1540-6288.00050

Dickinson V (2011) Cash flow patterns as a proxy for firm life cycle. The Accounting Review 86:1969–1994. https://doi.org/10.2308/accr-10130

Du L, Harrison ANN, Jefferson G (2014) FDI spillovers and industrial policy: the role of tariffs and tax holidays. World Development 64:366–383. https://doi.org/10.1016/j.worlddev.2014.06.005

Dunning JH (1988) The eclectic paradigm of international production: a restatement and some possible extensions. Journal of International Business Studies 19:1–31

Dunning, JH (1993). Multinational enterprises and the global economy. Wokingham: Addison-Wesley Publishing Company

Faccio M, Lang LHP, Young L (2001) Dividends and expropriation. American Economic Review 91(1):54–78. https://doi.org/10.1257/aer.91.1.54

Fama EF, French KR (2002) Testing trade-off and pecking order predictions about dividends and debt. Review of Financial Studies 15:1–33. https://doi.org/10.1093/rfs/15.1.1

Flamm K (1984) The volatility of offshore investment. Journal of Development Economics 16:231–248. https://doi.org/10.1016/0304-3878(84)90076-2

Forti CAB, Peixoto FM, Alves DLE (2015) Determinant factors of dividend payments in Brazil *. Revista Contabilidade & Finanças 26:167–180. https://doi.org/10.1590/1808-057x201512260

Fowowe, B (2011). Financial liberalization in Sub‐Saharan Africa: What do we know? Journal of Economic Surveys, 27. https://doi.org/10.1111/j.1467-6419.2011.00689.x

Globerman S, Shapiro DM (1999) The impact of government policies on foreign direct investment: the Canadian experience. Journal of International Business Studies 30:513–532. http://www.jstor.org/stable/155463

Globerman S, Shapiro D (2003) Governance infrastructure and US foreign direct investment. Journal of International Business Studies 34:19–39. http://www.jstor.org/stable/3557137

Gugler K, Yurtoglu BB (2003) Corporate governance and dividend pay-out policy in Germany. European Economic Review 47:731–758. https://doi.org/10.1016/S0014-2921(02)00291-X

Harris R, Li S (2019) Government assistance and total factor productivity: firm-level evidence from China. Journal of Productivity Analysis 52:1–27. https://doi.org/10.1007/s11123-019-00559-4

Holder ME, Langrehr FW, Hexter JL (1998) Dividend policy determinants: an investigation of the influences of stakeholder theory. Financial Management 27:73–82

Hsu M, Lee J, Leon-Gonzalez R, Zhao Y (2019) Tax incentives and foreign direct investment in China. Applied Economics Letters 26:777–780. https://doi.org/10.1080/13504851.2018.1495817

Huang C (2015) Tax credits and total factor productivity: firm-level evidence from Taiwan. The Journal of Technology Transfer 40:932–947. https://doi.org/10.1007/s10961-014-9358-7

Hufft, EM, & Dufrene, U (1996). Small firm capital structure decisions: The effect of agency cost. United States Association for Small Business and Entrepreneurship

Jabbouri I (2016) Research in International Business and Finance Determinants of corporate dividend policy in emerging markets: Evidence from MENA stock markets. Research in International Business and Finance 37:283–298. https://doi.org/10.1016/j.ribaf.2016.01.018

Jensen MC, Meckling WH (1976) Theory of the firm: Managerial behavior, agency costs and ownershipstructure. Journal of Financial Economics 3:305–360

Khang K, King T-HD (2006) Does dividend policy relate to cross-sectional variation in information asymmetry? Evidence from returns to insider trades. Financial Management 35:71–94. https://doi.org/10.1111/j.1755-053X.2006.tb00160.x

Klemm A, Parys SVan (2012) Empirical evidence on the effects of tax incentives. International Tax and Public Finance 19:393–423. https://doi.org/10.1007/s10797-011-9194-8

Koch PD, Shenoy C (1999) The information content of dividend and capital structure policies. Financial Management 28:16–35

Kroger H, Hartmann J (2021) xtoaxaca - Extending the Kitagawa-Oaxaca-Blinder Decomposition Approach to Panel Data. The Stata Journal: Promoting Com- Munications on Statistics and Stata 21:360–410

Labhane NB (2017) Disappearing and reappearing dividends in emerging markets: evidence from Indian companies. Journal of Asia-Pacific Business 18:46–80. https://doi.org/10.1080/10599231.2017.1272996

Lin KZ (2006) The impact of tax holidays on earnings management: An empirical study of corporate reporting behavior in a developing-economy framework. The International Journal of Accounting 41:163–175. https://doi.org/10.1016/j.intacc.2006.04.006

Mather P, Peirson G (2006) Financial covenants in the markets for public and private debt. Accounting and Finance 46:285–307. https://doi.org/10.1111/j.1467-629X.2006.00168.x

McLure Jr, CE (1999). Tax Holidays and Investment Incentives; A Comparative Analysis. Bulletin for International Fiscal Documentation. Amsterdam

Miller MH, Modigliani F (1961) Dividend policy, growth, and the valuation of shares. The Journal of Business 34:411–433. http://www.jstor.org/stable/2351143

Mitton T (2004) Corporate governance and dividend policy in emerging markets. Emerging Markets Review 5:409–426. https://doi.org/10.1016/j.ememar.2004.05.003

Moosa, IA (2002). Foreign direct investment: theory, evidence, and practice / Imad A. Moosa. Palgrave Basingstoke

Mrzygłód U, Nowak S, Mosionek-Schweda M, Kwiatkowski JM (2021) What drives the dividend decisions in BRICS countries? Oeconomia Copernicana 12:593–629. https://doi.org/10.24136/oc.2021.020

Munongo S, Akanbi OA, Robinson Z (2017) Do tax incentives matter for investment? A literature review. Business And Economic Horizons 13:152–169

Nini G, Smith DC, Sufi A (2009) Creditor control rights and firm investment policy. Journal of Financial Economics 92:400–420. https://doi.org/10.1016/j.jfineco.2008.04.008

Nunn N, Trefler D (2010) The structure of tariffs and long-term growth. American Economic Journal: Macroeconomics 2:158–194. https://doi.org/10.1257/mac.2.4.158

Porta RL, Lopez-de-silanes F, Shleifer A, Vishny R (2000) Investor protection and corporate governance. Journal of Financial Economics 58:3–27

Reed WR (2015) On the practice of lagging variables to avoid simultaneity. Oxford Bulletin of Economics & Statistics 77:897–905. https://doi.org/10.1111/obes.12088

Sabina S, Eldin M (2022) How effective is tax policy in attracting foreign direct investments in transition countries. Central European Business Review 11:19–39. https://doi.org/10.18267/j.cebr.274

Szabo, S (2019). Foreign Direct Investment in the Czech Republic: A Visegrád Comparison. Retrieved from https://ideas.repec.org/p/euf/ecobri/042.html

Tiebout CM (1956) A pure theory of local expenditures. Journal of Political Economy 64:416–424. http://www.jstor.org/stable/1826343

Tobing S, Jayadi A (2020) Decentralization and tax holiday as strategies to boost foreign direct investment of Indonesia. Journal of Security and Sustainability Issues 10:460–471. https://doi.org/10.9770/jssi.2020.10.Oct(37)

Wilson JD (1999) Theories of tax competition. National Tax Journal 52:269–304. https://doi.org/10.1086/NTJ41789394

Acknowledgements

The authors are thankful to the Technology Agency of the Czech Republic, project No. TL03000319, and Tomas Bata University in Zlín, project No. RO/2022/04, for the financial support of this study.

Author information

Authors and Affiliations

Contributions

VHD: Conceptualization; Methodology; Software; Data curation; Investigation; Validation; Formal analysis; Writing - original draft; Visualization; Resources. DP: Conceptualization, Validation, Investigation, Resources. MD: Conceptualization, Resources

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Vu, D.H., Pavelková, D. & Damborský, M. Tax holidays and profit-repatriation rates for FDI firms: the case of the Czech Republic. Humanit Soc Sci Commun 10, 843 (2023). https://doi.org/10.1057/s41599-023-02369-4

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-02369-4