Abstract

Many countries have recently announced the ambition to reach net-zero emissions targets. Here we explore the climate and energy transition impacts of the following strategies using the IMAGE integrated assessment model: 1) implementing the pledged 2030 targets and net-zero targets, 2) aligning the 2030 emission targets with the net-zero targets, 3) broadening the coalition of net-zero countries, and 4) strengthening the net-zero pledges by bringing them forward in time. The results illustrate that each step could accelerate the low-carbon transition by building on existing elements in international climate policy. Our study shows that the gap between a continuation of current emission trends and a Paris-aligned 1.5 °C target can be reduced by about 90% by 2100. This provides a pathway to bring the Paris Agreement climate goals within reach.

Similar content being viewed by others

Introduction

To meet its overall climate objective of keeping global temperature increase well below 2 °C, and preferably 1.5°C, the Paris Agreement has designed a process of cycles of country-level pledges on near- and longer-term emission reduction targets and strategies1. In 2020 and 2021, many countries have indeed renewed their 2030 pledges as part of their Nationally Determined Contributions (NDCs)2,3,4 and announced or formally submitted long-term net-zero emission targets5,6,7. The net-zero emission targets form a crucial step forward in international climate policy, but as noticed in the literature, there are considerable differences between them6,8,9. Some of the announced net-zero emission targets form part of a detailed emissions reduction strategy; others only constitute a single announcement. Moreover, the announcements differ in coverage—focusing on all greenhouse gases (GHG) or only on CO2 emissions. Still, the announced net-zero targets constitute a major development—with many countries accepting their responsibility in climate action and providing the first long-term pathway of emission reductions at the global level. In fact, Meinshausen et al.7 recently concluded that, if implemented, countries’ current net-zero emission targets would more-or-less lead to stabilizing the global mean temperature increase just below 2 °C. As part of the 2023 global stocktake, the critical question is how to build upon the current pledges to implement the Paris Agreement’s overall goals. Additionally, only limited studies have provided information on what impacts such a transition will have on sectoral emissions and energy systems10,11. This study provides a way forward based on four propositions that could align current pledges with the Paris Agreement climate goals by (1) implementing the current net-zero pledges, (2) aligning the NDCs with the net-zero pledges by implementing the net-zero targets on a linear path from 2022 onwards (Table 1), to provide confidence that the net-zero targets can be met, (3) broadening the net-zero pledges to all countries in line with those already announced by similar countries, and (4) strengthening all commitments, by bringing the net-zero target year forward by five years for all regions, to further close the gap between national efforts and global goals.

For this, we have developed a set of scenarios to illustrate the impact of our propositions. All scenarios have been developed using the IMAGE integrated assessment model12, one of the models also used to create the recent set of scenarios used by IPCC. Translating the announced targets into emission reduction strategies is critical for real-world impact, highlighting the relevance of our propositions. Rogelj et al. emphasized earlier that for several countries, the targets have not yet been substantiated8. Model-based scenario analysis using global, but especially national models can help materialize this step (implementing)13,14,15,16,17,18. Here, using the IMAGE integrated assessment model, we show energy and land-use pathways consistent with the net-zero targets (see Methods and Supplementary Notes) and the more ambitious scenarios. The subsequent step of aligning the NDC with the net-zero targets is critical to provide a low-cost path to the long-term goals and avoid high cumulative emissions in the short term. The broadening step offers a clear pathway to close the emission gap between current policies and the Paris goals11,19. Finally, the strengthening step explores the climate and energy transition impacts of hastening the implementation of net-zero targets.

We compare the results of the analysis to (1) the latest NDCs and announced net-zero pledges (NDCs and net-zero targets) and (2) the analysis of currently implemented policies, that have only been done to a limited extent beforehand10. In many countries, there is still an implementation gap between the reductions pledged in the NDCs and the expected outcomes of implemented climate policies20,21,22. Therefore, we are presenting also regional results, based on commitments of countries within the selected regions (Organization for Economic Co-operation and Development (OECD) region, non-OECD region where countries have a net-zero target, and non-OECD region where countries do not have any type of announced target). We also compare the results to a least-cost pathway consistent with the 1.5 °C climate target. We use the current policies scenario of IMAGE as a starting point for our cost-optimal implementation of abatement options that bring emissions towards the NDC and net-zero target pledges, and finally, the 1.5 °C target. The current policies scenario is based on the latest inventory of current policies, as described in previous literature20,21.

Results

Scenario analysis to inform the global stocktake

Table 1 provides an overview of the scenarios to explore the impact of our propositions. The aligning scenario assumes direct implementation of a cost-optimal pathway towards the net-zero targets starting from 2022, avoiding the delay of some of the NDCs. An exception is made for countries with a net-zero year more than 40 years in the future—where the NDC emission pathway is used until 2030 (based on the lowest emission level achieved by either current policies or the NDC). The broadening strategy assigns net-zero targets to all countries. For this, we used an observed relationship between the income level of IMAGE regions, as measured by their 2020 gross domestic product (GDP) per capita, and their announced net-zero year (Supplementary Table 1 and Supplementary Fig. 1): on average, high-income countries have announced earlier net-zero years than low-income countries. This is consistent with the historical responsibility and capability of high-income countries. It should be noted that several countries have announced net-zero CO2 emissions targets, while most countries announced net-zero GHG targets. However, for some countries, it is unclear whether the net-zero target refers to CO2 or GHGs, and their assumed coverage is based on earlier analysis5,23 (Supplementary Table 1). Our assumptions on countries with unclear coverage are optimistic, assuming a GHG neutrality target for China, India, and South Korea, consistent with recent literature5,7,11,17,24. However, China’s and India’s GHG coverage is ultimately unclear25 and it is important to acknowledge that a part of scientific literature assumes that coverage of China’s targets specifically, only includes CO226,27. The distinction between CO2 neutrality and GHG neutrality for these major emitters can have a major impact on climate calculations28 and the energy transition29. To make the CO2 and GHG net-zero targets comparable, we assumed a 15-year delay (range 10-20 years) in reaching full GHG net-zero levels (compared to CO2) that is observed at the global scale, based on an assessment of cost-effective 1.5 °C and 2 °C scenarios from a selection of integrated assessment models13, as well as the recent IPCC AR6 report30 (see also text in Supplementary Table 1); this is only to derive a single relationship—and in reality, the years of reaching net-zero CO2 and GHG can differ based on the national emission sources.

Impact on emission trajectories and temperature projections

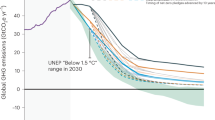

The outcomes for the global GHG emission trajectories and temperature increase are indicated in Fig. 1a, b. If countries only implement current policies, emissions are projected to increase further up to 2030. The illustrative extensions of both the current policies (CurPol) and the NDC scenario reach a global mean temperature increase of 3.5 °C (2.6–4.7 °C with a 66% probability). If all NDCs were fully implemented, emissions would stabilize in 2030. The difference between the CurPol and NDC scenarios is often referred to as the implementation gap. The extrapolation of this scenario would reduce total cumulative emissions by about 25% compared to CurPol but still lead to about 2.8 °C warming (2.1–3.9 °C with a 66% probability). The net-zero targets announced mostly between 2020 and 2022 form a critical step forward, as also reported by Meinshausen7. Assuming implementation of the NDCs, implementing the net-zero targets in IMAGE leads to 1.9 °C (1.4–2.6 oC with a 66% probability) increase in global mean temperature, consistent with recent literature7,19. Global emissions do not reach net zero as about half the countries (representing 25% of global emissions) have not announced net-zero targets. As can also be seen, the trajectory via the NDC targets is not yet aligned with the net-zero goals. If countries aligned the NDCs with the net-zero goals, the temperature increase would be 1.75 °C (1.4–2.5 oC with a 66% probability) due to the lower cumulative emissions between now, 2030 (NDCs) and the net-zero target years. Such an alignment of the short-term policy implementation and NDC targets with the long-term net-zero targets is also attractive to reach the global net-zero goal cost-efficiently, seeing as emissions trajectories implied by NDC and net-zero targets of G20 members highlight discrepancies between short-term policy implementation, NDC targets and long-term net-zero targets4,31. The next critical step is broadening the targets to all countries. Such a scenario can be regarded as aligned with the ambition to stay well below 2 °C (ending up at 1.6 °C; 1.1–2.2 °C with a 66% probability), achieving global GHG neutrality by 2070. Strengthening the pledges by five years does not hasten the neutrality year but does project a lower temperature increase of 1.55 °C (1–2.1 °C with a 66% probability), due to slightly lower cumulative emissions.

Global GHG emission projections (a), global mean temperature increase in 2100 (b), and probabilities of temperature increase (bars) and peak warming (dots) (c) for the current policies (CurPol), NDC, net-zero (NZ), the aligned (NZ-Al), broadened (NZ-Br), and strengthened (NZ-Str) net-zero scenarios, and the existing IMAGE 1.5 °C scenario. The bars in c represent the probability of temperature increase located between the values presented in each scenario’s x-axis. All non-CO2 gases considered in the calculations for a (CH4, N2O, HFCs, PFCs, and SF6) are aggregated into CO2eq values according to the 100-year Global Warming Potentials in the IPCC AR6 report.

Regional and sectoral implications

The detailed impacts of the steps of implementing, aligning, and broadening the NDC and net-zero targets are shown in Fig. 2. Implementing the NDCs (compared to current policies) mainly achieves further emission reductions in the OECD region (Fig. 2a). The first big step is the net-zero implementation step via the net-zero scenario. Here, emissions reductions are achieved in both OECD and non-OECD regions (Fig. 2a, b). In fact, the additional reduction in the non-OECD region is substantially larger given its larger share in total emissions and the fact that the NDC scenario is more ambitious in most OECD countries (Supplementary Table 2). Implementing the net-zero scenarios has a substantial impact on land-use emissions for all regions as well, as afforestation, reforestation, and deforestation (ARD) activities reduce agriculture, forestry, and other land-use (AFOLU) emissions in all regions, reaching negative emissions in the two separate non-OECD regions.

GHG emission reductions (shaded columns) and GHG emission levels per sector and scenario for the OECD region (a), non-OECD region with net-zero targets (b), and non-OECD region without a net-zero target (c) in 2050.

The next step is aligning the 2030 NDCs with the net-zero targets. This impacts OECD and non-OECD regions but can further reduce emissions by 2050 in non-OECD countries by about 20% (Fig. 2b). It should be noted that the alignment step mostly impacts cumulative emissions (and so the 2050 emission impact is less important). The broadening step has the strongest impact on the non-OECD region without an announced target yet, reducing emissions in 2050 by almost 70% (Fig. 2c). It should be noted that in the model calculation, the increasing level of ambition of the scenarios also impacts other regions, given the impact of policies on technology development rates and depletion dynamics. This leads to a slight increase in emissions in the OECD and non-OECD region while moving from the net-zero and the aligned net-zero to the aligned net-zero and broadened net-zero scenarios respectively, mostly as a result of increased competition for bioenergy (and consequences for bioenergy with carbon capture and storage (BECCS)), the impacts on technology development and fossil fuel prices.

The OECD region achieves GHG neutrality between 2045 and 2050 under all net-zero scenarios (Fig. 3a–c and Supplementary Fig. 2a–d), as most of the individual countries within the region have a net-zero GHG target year in 2050, the exception being Turkey and Mexico. Emission levels almost reach their respective 1.5 °C scenario by the end of the century, mainly driven by negative emissions in the AFOLU and electricity sectors after 2040. For the non-OECD region with a net-zero target, GHG neutrality is achieved in 2070 (Fig. 3d–f); aligning the NDCs with net-zero targets accelerates reaching net-zero from 2070 to 2060, and emissions peak earlier and lower (Supplementary Fig. 2e). This is facilitated by a rapid decline in energy supply emissions. As mentioned in the discussion in Fig. 2 results above, the enhanced policy implementation (in the form of an economy-wide carbon tax), also impacts other regions. Climate policies, carbon tax, and mitigation pathways that are applied in the scenarios have a notable impact on technology development and learning rates, renewable technology cost reductions, or reversely, fossil fuel technology cost increases on a global level. This impact can be seen while moving from the CurPol to the NZ scenario (Fig. 3g, h), where non-OECD countries with no net-zero target still take advantage of reduced renewable technology costs, leading to a notable decrease in electricity emissions. The broadening scenario greatly impacts emission projections of the non-OECD region with no net-zero targets: increasing emissions under the NZ and NZ-Al scenarios are now converted into a declining emissions pathway that reaches net-zero by around 2060 (Fig. 3g–i and Supplementary Fig. 2). This is mainly induced by a sharp drop in emissions from power supply. This pattern is similar to the other regions. In contrast to the OECD region, the final emissions level is not close to its 1.5 oC scenario. Finally, the strengthening scenario, as seen above, has marginal effects on emission levels. This, in connection with the results presented in Fig. 3 and Supplementary Fig. 2, implies that a broadening and strengthening of ambition is not enough to meet 1.5 oC. Setting the region on a 1.5 °C pathway requires substantial negative emissions to return the temperature to a 1.5 °C warming level (in conjunction with negative emissions in the other regions’ 1.5 °C scenario). A straightforward net-zero GHG target for the region is not enough to help materialize these required deep negative emissions. Still, both a short- and long-term acceleration of the transition to zero and, subsequently, negative emissions in the energy supply sector is critical. It is noteworthy that while the region does not have a net-zero target under the NZ scenario, it benefits from the region’s NDC targets, particularly from technology learning and reducing renewables costs in the IMAGE model, leading to a substantial decrease in emissions compared to its CurPol scenario.

Development of GHG emission projections over time by sector, for OECD (a–c), non-OECD with a net-zero target (d–f), and non-OECD without a net-zero target (g–i) regions, for the CurPol, NZ, and NZ-Br scenarios. All non-CO2 gases considered in the calculations for this figure (CH4, N2O, HFCs, PFCs, and SF6) are aggregated into CO2eq values according to the 100-year Global Warming Potentials in the IPCC AR6 report.

The AFOLU and electricity sectors contribute most to emission reductions and negative emissions after reaching net zero. The electricity sector decarbonizes on average around 2040, with the industry sector achieving the same 20 years later. Buildings and transport, while being able to reduce emissions throughout the century, can never decarbonize fully. The residual emission sources in all regions and scenarios are almost exclusively non-CO2 gases, with reductions in the sector happening at an extremely low pace. We do not take the Global Methane Pledge of COP26 into account, which would achieve a 30% reduction in CH4 emissions by 2030 and most likely would have enduring effects throughout the rest of the century.

Translation of the targets into actual mitigation strategies by model-based scenarios can also assist in their implementation. While global models (such as presented here) can provide initial insights, net-zero pathways must be translated into mitigation strategies mostly using national models (or a combination thereof—as shown earlier). The scenarios shown here implement mitigation measures based on cost optimization. It should be noted that other strategies exist that might emphasize other measures, such as lifestyle changes or specific measures that are easier to implement32, as feasibility concerns might not always be aligned with cost considerations. The results show that, in any case, an important contribution will come from the electricity and AFOLU sectors that go negative first. Additionally, transport and industry can reach almost zero emissions in the NZ and NZ-Al scenarios for OECD and non-OECD with a net-zero target. The broadening and strengthening scenarios achieve comparable results on a global level.

Transformations in energy use

As expected, based on the previous results, the primary energy consumption development over time is similar for all mitigation scenarios for the OECD region (Fig. 4a–c and Supplementary Fig. 3a–c). Consumption remains at relatively the same levels throughout the century. Fossil fuel consumption percentage drops substantially with remaining fossil fuel use coupled with carbon capture and storage (CCS) (other scenarios emphasizing a larger role for renewables could lead to lower fossil fuel levels). At the same time, the uptake of low-carbon sources increases substantially, driven mostly by solar, wind, modern biomass, and BECCS. The contribution of modern biomass and BECCS is relatively more important for the OECD region compared to both non-OECD ones (25% of total primary energy consumption by the end of the century).

Development of substituted primary energy consumption projections over time, for OECD (a–c), non-OECD with a net-zero target (d–f), and non-OECD without a net-zero target (g–i) regions, for the CurPol, NZ, and NZ-Br scenarios. Trad.Bio (traditional biomass) in the IMAGE model includes charcoal, fuelwood, crop residue, and dung. Mod.Bio (modern biomass) includes all liquid biofuels (ethanol, diesel, methanol), as well as wood pellets.

Traditional fossil fuel use is also phased out considerably in the non-OECD region with a net-zero target, from 81% in 2015 to between 16-21% across all net-zero scenarios by the end of the century (Fig. 4d–f and Supplementary Fig. 3e–g). Residual fossil production is coupled with CCS to a higher extent than in the OECD region—up to 65% of total fossil production compared to approximately 50% in the OECD. The extensive modern biomass and BECCS use seen in the OECD region is replaced with nuclear and wind (12% and 24% of total primary energy consumption by 2100 respectively) and particularly solar (36%). The decrease in primary energy production when moving from the CurPol to net-zero scenarios is attributed to the substantial decrease in absolute final energy consumption in all net-zero scenarios for this region (as seen in Supplementary Fig. 4f), compared to the other regions. Combined with the increased electrification in power supply, industry, and transport, especially in China and India, the widespread use of fossil fuels, especially the extraction and use of coal and, to a lesser extent, natural gas in these 2 regions is replaced by more efficient sources of energy, with the remaining fossil sources coupled with CCS, leading to overall lower primary energy production in the region.

By broadening and strengthening the net-zero targets to countries without a net-zero target, fossil fuel use without CCS is almost eliminated, while it was projected to increase in all types under the NZ and NZ-Al scenarios (Fig. 4g–i and Supplementary Fig. 3i–k). Additionally, total primary energy production is slightly reduced compared to the region’s 1.5 oC scenario. This is a result of low negative emissions in the power supply sector compared to the 1.5 °C pathway, as BECCS and fossil fuel coupled with CCS use remain limited in our net-zero scenarios for this region. Primary energy production from solar sources is by far the biggest contributor by the end of the century in the region, comprising 42–51% of the total by 2100.

A decrease in primary energy is also observed in the non-OECD region without a net-zero target, but it is not as noticeable in absolute terms. The replacement of fossil fuel sources (mostly natural gas and oil) with renewable alternatives (solar, biomass, and BECCS) can be seen in Fig. 4g–i.

Discussion

We have shown that while the national net-zero targets are an important step forward in the current negotiations, our propositions could bring the emissions levels closer to those consistent with the 1.5 °C goal. Under the broadened net-zero scenario, GHG neutrality is reached around 2070, based on immediately implementing the net-zero targets, aligning the NDCs, and providing targets to all countries. Moving the net-zero targets forward by five years, while providing some marginal improvements in terms of temperature increase, does not have a noticeable effect on emission levels or energy indicators. However, some additional effort would still be required to close the last 10% of the emissions gap to the 1.5 oC target. This signifies that even a broadened and strengthened scenario that assumes a net-zero target for all countries, built upon already relatively optimistic assumptions (as presented in the section ‘Scenario analysis to inform the global stocktake’), and also allows overshoot, is not consistent with the Paris Agreement targets. This inconsistency has also been explored in literature28. Deeper mitigation in the first half of the century—similar to the 1.5 °C scenario—is required, which translates to faster decoupling from fossil fuel use without CCS, higher renewables deployment, and increased energy efficiency. It should be noted that the current illustrations of the results rely on the technology assumptions of the IMAGE model, but this is less so for the actual emission trends. Other models or scenario assumptions can be used to identify pathways with higher or lower reliance on carbon dioxide removal (CDR) technologies. In the IMAGE results, most emission reductions are achieved via an extensive phase-out of traditional fossil fuels and parallel fuel shifts to renewables. However, the persistence of non-CO2 gases and some hard-to-abate CO2 sectors and the limitations in short-term emission reductions might make use of CDR technologies necessary33. The scenarios are implemented for total GHG emission reductions, which do not prioritize individual GHG reduction, but use a region-specific carbon tax to implement the respective net-zero pathways. Thus, the scenarios are agnostic about specific climate ambitions other than the overall goal of net-zero GHGs and do not include non-climate socio-economic or other aspects. Even under our optimistic GHG assumptions, it is more cost-effective in our model to prioritize CO2 removal via land sinks or BECCS instead of focusing on non-CO2 reductions—although a reduction in CH4 emissions from the oil and gas sector is achieved in the non-OECD regions in our net-zero scenarios. In recent work relating to hard-to-abate sectors, it was also established that reduction of non-CO2 GHGs is most effective via specific targeted measures, either via demand-side changes (less meat consumption, lower calorie intake, and less food waste), or technology changes (shift toward cultured meat and measures to reduce non-CO2 emissions from agriculture), rather than a universal carbon tax33. It should be noted that for stabilizing temperature, reaching CO2 neutrality in combination with non-CO2 reductions is sufficient. GHG neutrality (that is achieved later) leads to a decrease in global temperature.

Political and social realities or feasibilities are not explicitly considered here, as our scenarios present cost-optimal mitigation pathways within the conditions set. International collaboration and national focus and policy are of paramount importance in shaping net-zero mitigation strategies. Still, they must be translated into mitigation strategies mostly using national models, as global models cannot provide the granularity of input required for developing national mitigation strategies. Additionally, demand-side mitigation will be a major driver of emission reductions in the medium- to long-term future, mostly through lifestyle changes (increased use of public transport, dietary changes etc.) and the availability of possible new CDR technologies.

Methods

The IMAGE integrated assessment model

IMAGE is an integrated assessment model framework that simulates global and regional environmental consequences of changes in human activities34,35,36,37 (see also Supplementary Methods). The model is a simulation model, i.e., changes in model variables are calculated on the basis of the information from the previous time step. The model includes a detailed description of the energy and land-use system and simulates most of the socio-economic parameters for 26 regions (Supplementary Table 1). The model has been designed to analyze large-scale and long-term interactions between human development and the natural environment and to identify response strategies to global environmental change based on the assessment of options for mitigation and adaption12. While IMAGE includes a slightly adapted version of the MAGICC 6.0 climate model, our temperature outcomes are estimated using the climate model MAGICC 7.5.3, which calculates climate impacts based on the radiative forcing of an ensemble of greenhouse gases (see also Supplementary Methods).

Global warming potentials and climate forcers

The individual non-CO2 GHGs that were considered in our calculations of emission projections were methane (CH4), nitrous oxide (N2O), hydrofluorocarbons, perfluorocarbons, and sulfur hexafluoride (HFCs, PFCs, and SF6, aggregated as F-gases for this study). All non-CO2 gases are aggregated into CO2e values according to the 100-year Global Warming Potentials (GWP) in the IPCC AR6 report. While we acknowledge the importance of separating between short- and long-lived climate forcers (SLCFs and LLCFs)28,38,39,40,41, the use of GWP-100 metrics is a common practice in current international policies, thus used in this work as well for consistency with national communications and scientific literature7,11,42. While a separation between SLCFs and LLCFs would have a modest impact on the end-of-century temperature increase and mitigation cost results43, it would have a more substantial impact in reducing global mean temperature in the short term. Such a separation would potentially avoid overshooting of 1.5 °C or 2 oC targets, and, most importantly, would lead to a change in the overall timing of emission reductions, e.g., a slower rate of temperature change in the short term, allowing for easier adaptation by both human society and natural ecosystems38,40,44.

Our temperature outcomes are calculated via the MAGICC model, which considers the forcing impact of an ensemble of gases provided to it (in our case 23 different gases), leading to the reported temperature increase probabilities and mean temperature results. Thus, our temperature outcomes are independent of the GWPs used in our calculations of GHG emission projections.

Scenario development

The CurPol scenario of IMAGE was derived from the original SSP2 baseline by introducing explicit policy measures and is reported in detail in Roelfsema et al.20,21. More specifically, we used a modeling protocol21, updated from Roelfsema et al.20, including a detailed spreadsheet listing policies by country to implement current policies in the IMAGE model. The CurPol scenario also considers the short-term (2020–2025) economic projections updated to include the implications of the COVID-19 pandemic, including changes in sectoral activity45,46. In our NDC and mitigation scenarios, we assume a cost-optimal achievement of the NDC and net-zero emission target levels respectively via a regionally differentiated carbon price in all regions. The carbon price is implemented from 2021 onwards to reach the 2030 net-zero targets, following a cost-optimal pathway.

The CurPol and NDC scenarios are defined up to 2030. To illustrate the possible long-term effect of continuing a similar effort, van Soest et al.47 proposed extrapolating the equivalent carbon price in 2030 using an annual increase equal to the GDP growth rate of the different regions up to 2100. The equivalent carbon price represents the value of carbon that would yield the same marginal emissions reduction as the current or NDC policies in a region. If a region has a zero-carbon price while implementing its NDC in 2030, an initial minimum carbon price in 2031 of 1 $/tCO2 was assumed.

All the calculations are performed on the level of the 26 IMAGE regions and aggregated in post-processing to the OECD and non-OECD regions as presented in Supplementary Table 1. For more information on the scenarios used see also Supplementary Notes.

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

The data that support the findings of this study are available on GitHub.

Code availability

The code for the IMAGE 3.2 model is not publicly available at this moment, but the development of an open-source python-based code is underway. The IMAGE 3.2 model is documented on the common integrated assessment model documentation. The IMAGE 3.2 model is also documented on its website. The Python script used to generate the figures can be found on GitHub.

References

UNFCCC. Adoption of the Paris Agreement. https://unfccc.int/resource/docs/2015/cop21/eng/l09r01.pdf (UNFCCC, 2015).

UNFCCC. Communication of Long-term Strategies | UNFCCC. https://unfccc.int/process/the-paris-agreement/long-term-strategies (UNFCCC, 2022).

UNFCCC. Nationally Determined Contributions Registry | UNFCCC. https://unfccc.int/NDCREG (UNFCCC, 2022).

Den Elzen, M. G. J. et al. Updated nationally determined contributions collectively raise ambition levels but need strengthening further to keep Paris goals within reach. Mitig. Adapt. Strateg. Glob. Chang. 27, 1–29 (2022).

Höhne, N. et al. Wave of net zero emission targets opens window to meeting the Paris Agreement. Nat. Clim. Chang. 11, 820–822 (2021).

Hale, T. et al. Assessing the rapidly-emerging landscape of net zero targets. Clim. Policy 22, 18–29 (2022).

Meinshausen, M. et al. Realization of Paris Agreement pledges may limit warming just below 2 °C. Nature 604, 304–309 (2022).

Rogelj, J., Geden, O., Cowie, A. & Reisinger, A. Net-zero emissions targets are vague: three ways to fix. Nature 591, 365–368 (2021).

Climate Watch. Net-Zero Tracker. https://www.climatewatchdata.org/net-zero-tracker (2022).

Keramidas, K., Vázquez, D., Ramirez, S., Rincon, D. & Los Santos, R. Global Energy and Climate Outlook 2021: Advancing Towards Climate Neutrality Taking sTock of Climate Policy Pledges after COP26 and the Corresponding Energy-economy Implications. European Commission, Joint Research Centre (JRC) (2021).

Iyer, G. et al. Ratcheting of climate pledges needed to limit peak global warming. Nat. Clim. Chang. 1–7. https://doi.org/10.1038/s41558-022-01508-0 (2022).

van Vuuren, D. P. et al. Energy, land-use and greenhouse gas emissions trajectories under a green growth paradigm. Glob. Environ. Chang. 42, 237–250 (2017).

van Soest, H. L., den Elzen, M. G. J. & van Vuuren, D. P. Net-zero emission targets for major emitting countries consistent with the Paris Agreement. Nat. Commun. 12, 1–9 (2021).

Riahi, K. et al. Cost and attainability of meeting stringent climate targets without overshoot. Nat. Clim. Chang. 11, 1063–1069 (2021).

European Commission. A Clean Planet for All—A European Strategic Long-term Vision for A Prosperous, Modern, Competitive and Climate Neutral Economy. (European Commission, 2018).

US Department of State. The Long-Term Strategy of the United States. Pathways to Net-Zero Greenhouse Gas Emissions by 2050. (US Department of State, 2021).

He, J. et al. Towards carbon neutrality: a study on China’s long-term low-carbon transition pathways and strategies. Environ. Sci. Ecotechnol. 9, 100134 (2022).

Dafnomilis, I., den Elzen, M. & van Vuuren, D. P. Achieving net-zero emissions targets: an analysis of long-term scenarios using an integrated assessment model. Ann. N. Y. Acad. Sci. 1522, 98–108 (2023).

United Nations Environment Programme. Emissions Gap Report 2021. https://www.unep.org/resources/emissions-gap-report-2021 (United Nations Environment Programme, 2021).

Roelfsema, M. et al. Taking stock of national climate policies to evaluate implementation of the Paris Agreement. Nat. Commun. 11, 1–12 (2020).

Roelfsema, M. et al. Developing scenarios in the context of the Paris Agreement and application in the integrated assessment model IMAGE: a framework for bridging the policy-modelling divide. Environ. Sci. Policy 135, 104–116 (2022).

Nascimento, L. et al. Greenhouse gas mitigation scenarios for major emitting countries. Greenhouse gas mitigation scenarios for major emitting countries. Analysis of current climate policies and mitigation commitments: 2021 update. http://newclimate.org/publications/ (2021).

Climate Action Tracker. CAT Net Zero Target Evaluations. https://climateactiontracker.org/global/cat-net-zero-target-evaluations/.

Zeng, N. et al. The Chinese carbon-neutral goal: challenges and prospects. Adv. Atmos. Sci. 2022 398 39, 1229–1238 (2022).

United Nations Environment Programme. Emissions Gap Report 2022. https://www.unep.org/resources/emissions-gap-report-2022 (United Nations Environment Programme, 2022).

Chen, J., Cui, H., Xu, Y. & Ge, Q. Long-term temperature and sea-level rise stabilization before and beyond 2100: estimating the additional climate mitigation contribution from China’s recent 2060 carbon neutrality pledge. Environ. Res. Lett. 16, 074032 (2021).

Li, L. et al. Mitigation of China’s carbon neutrality to global warming. Nat. Commun. 13, 1–7 (2022).

Tanaka, K. & O’Neill, B. C. The Paris Agreement zero-emissions goal is not always consistent with the 1.5 °C and 2 °C temperature targets. Nat. Clim. Chang. 8, 319–324 (2018).

Xiong, W., Tanaka, K., Ciais, P. & Yan, L. Evaluating China’s Role in achieving the 1.5 °C target of the Paris agreement. Energies 15, 6002 (2022).

Shukla, P. R. et al. IPCC 2022: Summary for Policymakers. In: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. www.ipcc.ch; https://doi.org/10.1017/9781009157926.001 (2022).

Nascimento, L. et al. Greenhouse Gas Mitigation Scenarios for Major Emitting Countries. Analysis of Current Climate Policies and Mitigation Commitments: 2022 Update. NewClimate Institute. (2022).

Van Vuuren, D. P. et al. Alternative pathways to the 1.5 °C target reduce the need for negative emission technologies. Nat. Clim. Chang. 8, 391–397 (2018).

Edelenbosch, O. Y. et al. Mitigating Greenhouse Gas Emissions in Hard-to-abate Sectors. PBL Netherlands Environmental Assessment Agency, The Hague (2022).

Stehfest, E., van Vuuren, D. P., Kram, T. & Bouwman, L. Integrated Assessment of Global Environmental Change with IMAGE 3.0.PBL Netherlands Environmental Assessment Agency, The Hague (2014).

Doelman, J. C. et al. Afforestation for climate change mitigation: potentials, risks and trade-offs. Glob. Chang. Biol. 26, 1576–1591 (2020).

Hof, A. F. et al. Regional energy diversity and sovereignty in different 2 °C and 1.5 °C pathways. Energy 239, 122197 (2022).

van Vuuren, D. P. et al. The 2021 SSP scenarios of the IMAGE 3.2 model. EarthArXiv preprint (2021).

Allen, M. R. et al. Indicate separate contributions of long-lived and short-lived greenhouse gases in emission targets. npj Clim. Atmos. Sci. 5, 1–4 (2022).

McKeough, P. A case for ensuring reductions in CO2 emissions are given priority over reductions in CH4 emissions in the near term. Clim. Chang. 174, 1–16 (2022).

Shoemaker, J. K., Schrag, D. P., Molina, M. J. & Ramanathan, V. What role for short-lived climate pollutants in mitigation policy? Science (80-.). 342, 1323–1324 (2013).

Denison, S., Forster, P. M. & Smith, C. J. Guidance on emissions metrics for nationally determined contributions under the Paris Agreement. Environ. Res. Lett. 14, 124002 (2019).

IPCC. Climate Change 2022: Mitigation of Climate Change. Working Group III contribution to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. https://www.ipcc.ch/site/assets/uploads/2018/05/uncertainty-guidance-note.pdf (IPCC, 2022).

Van Den Berg, M., Hof, A. F., Van Vliet, J. & Van Vuuren, D. P. Impact of the choice of emission metric on greenhouse gas abatement and costs. Environ. Res. Lett. 10, 024001 (2015).

Harmsen, M. et al. Taking some heat off the NDCs? The limited potential of additional short-lived climate forcers’ mitigation. Clim. Change 163, 1443–1461 (2020).

Dafnomilis, I. et al. Exploring the Impact of the COVID-19 Pandemic on Global Emission Projections-assessment of Green Versus Non-green Recovery. http://newclimate.org/publications/ (2020).

Dafnomilis, I. et al. Targeted green recovery measures in a post-COVID-19 world enable the energy transition. Front. Clim. 4, 91 (2022).

van Soest, H. L. et al. Global roll-out of comprehensive policy measures may aid in bridging emissions gap. Nat. Commun. 12, 1–10 (2021).

Acknowledgements

This work was supported by the European Union’s Horizon 2020 research and innovation program (grant agreement no. 821471: ENGAGE; grant agreement no. 821124: NAVIGATE).

Author information

Authors and Affiliations

Contributions

I.D., M.d.E., and D.v.V. designed the study. I.D. led the scenario development and implementation, analysis of results, and writing of the manuscript. M.d.E. and D.v.V. contributed to the analysis, interpretation, and discussion of the results and the writing of the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Communications Earth & Environment thanks the anonymous reviewers for their contribution to the peer review of this work. Primary handling editors: Heike Langenberg. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Dafnomilis, I., den Elzen, M. & van Vuuren, D. Paris targets within reach by aligning, broadening and strengthening net-zero pledges. Commun Earth Environ 5, 48 (2024). https://doi.org/10.1038/s43247-023-01184-8

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s43247-023-01184-8

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.