Abstract

Climate impacts on economic productivity indicate that climate change may threaten price stability. Here we apply fixed-effects regressions to over 27,000 observations of monthly consumer price indices worldwide to quantify the impacts of climate conditions on inflation. Higher temperatures increase food and headline inflation persistently over 12 months in both higher- and lower-income countries. Effects vary across seasons and regions depending on climatic norms, with further impacts from daily temperature variability and extreme precipitation. Evaluating these results under temperature increases projected for 2035 implies upwards pressures on food and headline inflation of 0.92-3.23 and 0.32-1.18 percentage-points per-year respectively on average globally (uncertainty range across emission scenarios, climate models and empirical specifications). Pressures are largest at low latitudes and show strong seasonality at high latitudes, peaking in summer. Finally, the 2022 extreme summer heat increased food inflation in Europe by 0.43-0.93 percentage-points which warming projected for 2035 would amplify by 30-50%.

Similar content being viewed by others

Introduction

The effects of climate change on the economy are becoming increasingly well understood. Key progress has been made using empirical methods to demonstrate impacts on labour productivity1, agricultural output2,3,4, energy demand5,6, and human health7,8 from historical weather fluctuations. The resulting consequences for macroeconomic production have also been quantified empirically, with non-linear impacts of average temperature9,10,11, temperature variability12, and various aspects of precipitation13 on aggregate economic output identified in historical data. The future changes in weather conditions expected due to greenhouse gas emissions imply considerable welfare losses when evaluated through both these micro-3,14,15 and macroeconomic impact channels10,11,16,17.

Despite these advances, weather impacts on inflation and, in particular, the implications for inflation risks under future climate change, remain understudied. Advancing this understanding is crucial to a comprehensive assessment of climate change risk because rising or unstable prices threaten economic18,19 and human welfare20,21 as well as political stability22. The 2021/2022 cost of living crisis provides an example of such implications, with estimates by the United Nations having suggested that an additional 71 million people may have fallen into poverty due to rapidly rising prices23. Moreover, the potential for climate change to impact inflation dynamics is of increasingly high-relevance for the conduct of monetary policy and for central banks’ ability to deliver on their price stability mandate in the future24,25,26. A comprehensive assessment of climatic risks on inflation is therefore an important element in guiding the mitigation and adaptation efforts of governments, as well as informing monetary policy concerning the risks posed by climate change.

Previous work in this area has used historical weather fluctuations to identify impacts on inflation from changes in average temperatures27,28,29,30, temperature variability30, as well as from annual precipitation31. However, assessments of the implications of these historical impacts under future climate change are lacking. Here, we provide a comprehensive assessment of the historical impacts on inflation from fluctuations in a wide range of weather conditions, while flexibly accounting for the heterogeneity of their impacts across seasons and regions given different baseline climatic and socio-economic conditions. Moreover, by combining our results with projections from physical climate models we are able to assess the implications of these impacts under the weather conditions projected with future climate change.

We combine measures of national exposure to different weather conditions, based on high-resolution data from the European Centre for Medium-range Weather Forecast Reanalysis version 5 (ERA5)32, with a dataset of monthly price indices for different aggregates of goods and services across 121 countries of the developed and developing world over the period 1996-2021 (see Supplementary Table S1 for summary statistics)33. As well as providing over 27,000 observations, the availability of monthly price indices allows a detailed assessment of the temporal dynamics of the response of inflation to weather shocks and the heterogeneity of such effects across seasons. Our empirical framework quantifies the plausibly causal effects of fluctuations in historical weather conditions on national, month-on-month inflation rates (measured as the change in the logarithm of consumer price indices (CPI)) by exploiting within-country variation using fixed-effects panel regression models. Country-fixed effects account for unobserved differences between regions such as baseline climate and inflation rates, while the use of year fixed effects accounts for contemporaneous global shocks to both variables such as El Nino events or global recessions. We further include country-month fixed effects to account for country-specific seasonality – a crucial step given the strong seasonal cycle in both monthly inflation and weather data. Furthermore, our baseline specification accounts for country-specific time trends to avoid spurious correlations arising from common trends. Consequently, our framework accounts for a wide variety of un-observed confounders, and our results stem from the deviations of weather conditions from their national and seasonal patterns which cannot be accounted for by global shocks or country-specific trends. Combined with the exogenous nature of weather fluctuations, these methodological choices strengthen confidence in a causal interpretation of our results34.

Results

Temperature increases cause nonlinear, persistent increases in food and headline inflation

We find a rich response of inflation in different price aggregates to fluctuations in a variety of weather conditions (see Supplementary Fig. S1, Tables S2 and S3). The strongest and most consistent signal arises from fluctuations in average monthly temperatures (Fig. 1 and Supplementary Fig. S1a & f). Impacts are strongest in the food price component (Fig. 1b and Supplementary Fig. S1f), indicative of a supply-side productivity shock given the considerable evidence for impacts on agricultural production from temperature2,4 and other weather fluctuations (Fig. 1a)35,36,37. Although larger in food prices, these impacts also translate into considerable effects on headline inflation (Fig. 1c). We find limited evidence for impacts on other price sub-components asides from weak evidence in the electricity sector (Supplementary Figs. S1 & S2).

a A schematic outline of the mechanisms via which temperature shocks may impact inflation via agricultural productivity and food prices. The results of fixed-effects panel regressions from over 27,000 observations of monthly price indices and weather fluctuations worldwide over the period 1996-2021 demonstrate persistent impacts on food (b) and headline (c) prices from a one-off increase in monthly average temperature. Lines indicate the cumulative marginal effects of a one-off 1 C increase in monthly temperature on month-on-month inflation rates, evaluated at different baseline temperatures (colour) reflecting the non-linearity of the response by baseline temperatures which differ across both seasons and regions (see methods for a specific explanation of the estimation of these marginal effects from the regression models). Error bars show the 95% confidence intervals having clustered standard errors by country. Full regression results are shown in Tables S2 & S3. Icons are obtained from Flaticon (https://www.flaticon.com/) using work from Febrian Hidayat, Vectors Tank and Freepik.

The response to average temperature is strongly non-linear, such that increases in hotter months and regions cause larger inflationary impacts (Fig. 1). Consequently, increases in average temperatures at high latitudes cause upwards inflationary pressures when occurring in the hottest month of the year, opposing downward pressures when occurring in colder months. By contrast, increases in average temperatures at lower latitudes cause upwards inflationary pressures all year round (Supplementary Fig. S3). These heterogeneities arise from the dependence of the impacts on baseline temperatures in the empirical model expressed through an interaction term (see methods), rather than explicit dependence on season or latitude, a distinguishing feature from previous work28. By using lagged weather variables, we further find that the impacts of a 1 C increase in monthly temperature on the price level persist across the entire 12 months following the initial shock (Fig. 1), causing a cumulative effect on food inflation of 0.17 percentage points over the following year (when occurring in country-months with a temperature of 25 C, under our central specification shown in column 1 of Supplementary Tables S4 & S5 and Fig. 1a). That is, the initial spike in inflation is not offset by a decline in prices over the following year.

The response of inflation to other weather variables

In addition to the impacts arising from average temperature changes, we also assess impacts from daily temperature variability (the standard deviation of daily temperatures within each month, see methods). We find significant upwards pressures on food and headline inflation from increased variability (Supplementary Tables S2 & S3, Fig. S1b & g), which depend on the magnitude of the seasonal temperature cycle, with larger impacts at lower latitudes where the seasonal cycle is less pronounced (Supplementary Fig. S3c). This reflects the same patterns of vulnerability as that identified to the impacts of daily variability on economic growth12. Impacts from variability persist over twelve months, although with increasingly large errors (Supplementary Fig. S1b & g).

With regards to precipitation, we assess exposure to monthly extremes using the Standardised Precipitation Evapotranspiration Index (SPEI, see methods for further details). Excess wet conditions cause upwards impacts on food and headline prices which persist over twelve months, independent of baseline climate conditions (Supplementary Table S2 & S3, Fig. S1c & h). Excess dry conditions have some significant upwards impacts when coinciding with hot months or regions, but these are generally less persistent or significant (Supplementary Fig. S1i). These results are qualitatively consistent under different SPEI timescales and thresholds (see Supplementary Fig. S4). We further consider the impacts of daily precipitation extremes (defined as population exposure to the grid-cell level relative exceedance of the 99th percentile, see methods Eq. 1 for further details) to assess potential heavy-precipitation impacts arising over shorter timescales such as flooding13. Statistically significant upwards pressures on headline inflation can be identified in hot months in the first month following the shock, but these impacts appear not to persist with insignificant cumulative impacts at further time-horizons (Supplementary Tables S2 & S3, Fig. S1e & j).

Robustness of the impact of temperature on inflation

In general, we find the strongest and most significant historical weather impacts on inflation from changes in average temperature. These effects are robust to a number of tests and alternative specifications, an overview of which is shown in Supplementary Tables S4 and S5 (the results of the robustness tests for all weather variables can be found in Supplementary Figs. S5–9). Such tests include using a dynamic panel specification to account for auto-correlations in inflation, for example, associated with inflation developments through the business cycle, using Driscoll-Kraay errors to account for cross-sectionally correlated errors, and including explicit controls for changes in monetary policy frameworks (Supplementary Tables S4 & S5 Columns 2-4, Figs. S5 & S6a–j)38. Moreover, we conduct tests in which we split our estimates based on national income (estimated from World Bank GDP and population data), as well as when normalising inflation data by its historical volatility. Doing so we find the effects of temperature increases to be consistent across both higher- and lower-income countries and when accounting for different historical inflation volatility (Supplementary Tables S4 & S5 Columns 5 & 6, Figs. S7 & S8).

The fact that fluctuations of average temperature cause equivalent impacts on inflation in high- and low-income countries suggests that historical adaptation to temperature increases via socioeconomic development has been limited. To further test whether adaptation can be seen in the historical period we alternatively define temperature shocks with respect to a moving average over the past 30 years rather than a static 1990–2021 average. This choice would reflect the fact that agents may adjust their expectations as long-term climatic conditions change. Empirical results using these temperature shocks provide very similar response functions (Fig. S6k–t). Moreover, Information Criteria do not provide strong evidence for using shocks defined in either way. Empirical models of impacts on headline inflation produce Bayesian Information Criteria (BIC) and Akaike Information Criteria (AIC) values of −146636 and −163551.5 when using shocks defined with a moving baseline, compared to −146638.8 and −163554.3 when defined with a fixed baseline. For impacts on food inflation the BIC and AIC show values of −105528.5 and −122443.7 for moving baseline shocks and −105526.7 and −122442 for shocks with a constant baseline. We interpret this as a lack of evidence for significant adjustment in the historical period.

In further tests we use an alternative price index dataset from the World Bank39, finding a qualitatively and quantitatively consistent response of food inflation (Supplementary Fig. S9). Estimates for headline inflation differ notably when using World Bank data, most likely due to the inclusion of imputed rents in the World Bank data which may bias estimates away from the effects on widely consumed goods (see Methods for further discussion).

Following the principle of parsimony, and since the magnitude of its impacts lie in the middle range of the other specifications, we use the simple specification of column 1 in Supplementary Tables S4 & S5 as our baseline for the rest of the paper. We nevertheless continue to discuss the robustness of our results to this choice and present a range of uncertainty arising from this choice of baseline empirical specification (see methods).

Future warming to amplify pressures on inflation

The empirical evidence for the historical impacts of weather shocks on inflation suggests that the ongoing warming and intensification of weather extremes and variability due to anthropogenic greenhouse gas emissions40 may have consequences for future inflation. To assess these consequences, we evaluate the empirical responses identified above for temperatures under projected future climate conditions. Future projections are taken from an ensemble of 21 bias-adjusted climate models from the Coupled Model Intercomparison Project Phase 6 (CMIP-6) under different emission forcing scenarios from the Shared Socioeconomic Pathways (SSP)41 (see methods for further details and comparison to the forcing scenarios considered by the Network for Greening the Financial System42). We focus on the role of average temperature due to the persistence of its impacts across income groups and price aggregates, as well as due to the stronger response of average temperatures to greenhouse gas forcing compared to other weather variables.

We consider the impacts we estimate using future climate projections as the effects of future weather conditions on inflation, which would occur (i) in the absence of historically un-precedented adaptation via socioeconomic development or adjustment to warmer climatic conditions, (ii) without a targeted monetary policy response, and (iii) abstracting from any possible interactions with macroeconomic developments. (i) Though we do not introduce explicit models of future adaptation, which could mitigate impacts from future climate change we note that several robustness tests account for historical adaptations, which may have evolved via socio-economic development or prolonged exposure to different climate conditions, or through adjustment to warmer climatic conditions (see above). The results suggest that historical adaptation to temperature increases through socio-economic development and adjustment to warmer climatic conditions has been limited. (ii) A monetary policy reaction aimed at limiting persistent impacts on inflation from long-term changes in average weather conditions is plausible. However, central banks usually pursue a medium-term orientation with respect to their price stability objective, which allows them to be patient when confronted with temporary shocks, such as the weather shocks that we identify historically (Fig. 1). (iii) We do not aim to forecast inflation or provide scenarios for it, which would require a range of assumptions on socioeconomic and macroeconomic developments as well as a suite of structural models (as for example, used in the context of the scenarios of the Network for Greening the Financial System42). Rather, we provide an assessment of the potential future exogenous pressure on inflation from future climate conditions, based on the causal relationships inferred with the empirical models, and assuming other socioeconomic factors such as demographic developments and changes in the consumption basket remain constant (principle of ceteris paribus). As such, these results should provide helpful guidance on the likely magnitude and range of exogenous pressures to which society will be exposed and to which monetary policy may have to respond (see also the discussion section).

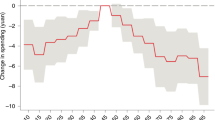

We find that the temperature conditions projected for 2035 under future warming imply upwards inflationary pressures across all of the world (Fig. 2a, b). In the global average, these effects constitute persistent upwards pressures on food inflation of 1.49±0.45 or 1.79±0.54 percentage-points per year (p.p.p.y.) respectively in a best- (SSP126) or worst-case (SSP585) emission scenario (uncertainty indicating the standard deviation across climate model projections). Pressures on headline inflation are approximately half as large, 0.76±0.23 or 0.91±0.28 p.p.p.y. under a best- or worst-case emission scenario (Fig. 2a, c). These results are qualitatively robust across empirical specifications, although impacts vary quantitatively dependent on this choice (shown in Supplementary Tables S4 & S5 row 5 and Figs. S10–12). Combining the uncertainty arising from empirical specification, emission scenario and range of climate model projections (see methods) results in a range of potential pressures on food inflation of 0.92-3.23 p.p.p.y. by 2035, and of 0.32-1.18 p.p.p.y. for headline inflation, on average across the world. These results therefore provide robust evidence that projected global warming would cause persistent upward exogenous pressures on inflation of considerable magnitudes already during the next few decades, independent of future emission trajectories and assuming ceteris paribus.

Maps of the pressure on annual national inflation in the food (a) and headline (b) price aggregates from the average weather conditions expected by 2035 under a high-emission scenario (SSP585) as estimated from the projections of CMIP-6 climate models. The annual pressure on inflation aggregated across world regions (population weighted), at different time periods under both a low (SSP126) and high (SSP585) emission scenario for food (c) and headline (d) price aggregates. Point estimates show the average, and error bars the standard deviation, of impacts as projected across the ensemble of 21 CMIP-6 climate models. Impacts are estimated accounting only for increasing average temperatures using the baseline empirical specification shown in column 1 of Supplementary Tables S4 & S5. Estimates reflect the exogenous pressure on inflation arising from future weather conditions in the absence of historically un-precedented adaptation, policy response, and abstracting from any possible interactions with macroeconomic developments (see text for discussion). Data on national administrative boundaries are obtained from the GADM database version 3.6 (https://gadm.org/).

Exogenous pressures on inflation from projected future temperature conditions are generally larger in the global south, with the largest pressures found across Africa and South America robustly across specifications (Fig. 2 & Supplementary Figs. S10–12). This occurs despite projected warming being greater at higher latitudes (Supplementary Fig. S13). This indicates that the heterogenous vulnerabilities to temperature increases due to different baseline temperature levels (as encoded in our empirical model shown in Eq. 3) outweigh heterogeneity in projected warming. Nevertheless, the magnitudes of pressures on inflation are also already considerable by 2035 across advanced economies, in the range of 1-2% on food inflation in North America and Europe under our baseline specification.

Beyond 2035 the magnitude of estimated pressures on inflation diverges strongly across emission scenarios (Fig. 2c, d), suggesting that decisive mitigation of greenhouse gases could substantially reduce them. By 2060, there is a strong and robust difference in the average global pressures on food inflation between the highest and lowest emission scenarios: 2.1 p.p.p.y. in our central estimate with a range of 1.6-3.8 across empirical specifications and climate models (Row 6 of Supplementary Tables S4 & S5). Under a best-case emission scenario, exogenous pressures on inflation are only marginally larger in 2060 than in 2035, but a worst-case emission scenario would cause pressures on food inflation exceeding 4 p.p.p.y. across large parts of the world (Fig. 2c, Supplementary Figs. S10–12c).

Although the empirical evidence indicates that adaptation to temperature shocks has been limited historically, we explore the potential of adaptation via adjustment to changing temperatures to reduce these future impacts. We do so by using empirical models in which temperature shocks are defined relative to a 30-year moving average rather than a constant baseline (Fig. S6k–t), and by evaluating potential impacts using future temperatures defined in this way. This method indicates that adaptation via adjustment could substantially reduce future impacts (Supplementary Fig. S14). In particular, in a low emission-scenario most impacts could be removed by adjustment once global temperatures stabilise (Supplementary Fig. S14c, d). However, in scenarios of un-mitigated warming, persistent impacts of considerable size remain despite introducing adjustment of this type which has not been observed historically (Supplementary Fig. S14).

The seasonality of pressures on inflation from future warming

The use of monthly CPI data allows us to further assess how the estimated pressures on inflation from future temperature conditions under projected climate change are distributed across the year. Concerning food inflation, these impacts are fairly constant across seasons at low latitudes but vary considerably across seasons in Northern mid-latitudes (20-40 N) where they can be more than twice as large in summer compared to winter (Fig. 3a). At the highest latitudes (>40 N) upwards pressure in summer contrasts downwards pressure in winter. This seasonal and spatial heterogeneity is robust across empirical specifications (Supplementary Figs. S15–S17), although accounting for different historical baseline inflation volatilities (column 6 of Supplementary Tables S4 & S5) introduces additional noise (Supplementary Fig. S17). Moreover, similar patterns are observed for headline inflation (Supplementary Figs. S18–S21).

a The pressures on monthly food inflation averaged across latitudinal bands estimated from the temperature conditions expected by 2035 under a high-emission scenario, as projected on average across the ensemble of CMIP-6 climate models. Impacts are estimated accounting only for increasing average temperatures. b The percentage change in the seasonal variability of food inflation under the pressures from future temperature conditions, estimated as the change in the standard deviation of the seasonal inflation cycle. c–f Country-specific examples of the pressures on the seasonal cycle of food inflation for the United States, Germany, Colombia and Kenya. Black curves show the historical average month-on-month percentage change in the food consumer price index (CPI) with blue error bars indicating the standard deviation across the years of the historical period (1996–2021). Red curves show this historical average plus the pressures estimated from the future weather conditions under projected warming, with the error bars indicating the standard deviation of projections across climate models. Estimates reflect the exogenous pressure on inflation arising from future weather conditions in the absence of historically un-precedented adaptation or policy response (see text for discussion). Data on national administrative boundaries are obtained from the GADM database version 3.6 (https://gadm.org/).

These heterogeneities arise from the dependence of the impacts on baseline temperatures as outlined in the empirical model (Eq. 3), rather than an explicit dependence on season or latitude. Large seasonal cycles of temperature at higher latitudes lead to stronger upward pressures in summer contrasting weak or downward pressures in winter, whereas less variable baseline temperatures throughout the year at low-latitudes result in fairly constant impacts across seasons. Projected temperature increases are typically stronger in winter than in summer in Northern mid-to-high latitudes (with the exception of Europe, Supplementary Fig. S13) indicating that most of the seasonality observed at high latitudes in Fig. 3 results from the distribution of baseline temperatures across seasons rather than differential warming between seasons (except in Europe, where more rapid warming in summer also contributes to these patterns).

These seasonally heterogenous pressures would cause alterations to the usual seasonal cycle of food inflation, resulting in an amplification of seasonal variability across most of the global south and the USA, and reductions in seasonal variability across most of Europe (excluding Spain) and the higher northern latitudes (Fig. 3b & Supplementary Fig. S15–21b). A reduction in seasonal variability arises when the strongest upwards pressures occur in months with historically lower inflation rates, as compared to other months (as shown in the case of Germany in Fig. 3d).

Amplified impacts from unpredictable heat extremes

In addition to shifting average conditions, climate change is also altering the intensity and frequency of unpredictable hot extremes which may pose additional short-term risks to inflation. The summer heat extreme in Europe in 2022 is a prominent example in which combined heat and drought had wide-spread impacts on agricultural and economic activity. These effects likely added to inflationary pressures in Europe, but the magnitude of their contribution has so far been difficult to assess, particularly in the context of other pressures from the Russian invasion of Ukraine and the aftermath of the Covid-19 pandemic. Combining our empirical results with estimates of monthly temperatures in June, July and August of 2022 (from the ERA5 reanalysis of historical observations), we estimate that the anomalous heat over these three months alone caused a cumulative annual impact of 0.67 percentage-points (0.43–0.93 across empirical specifications) on food inflation and 0.34 percentage-points (0.18–0.41) on headline inflation in Europe, with larger impacts across Southern Europe (Fig. 4a, see Supplementary Figs. S22–S24 for results using other empirical specifications).

The cumulative annual impacts on food (a) and headline (b) inflation from the observed temperatures of June, July and August of 2022 across Europe. (c, d) Regionally aggregated (using a population weighting) impacts from the historical 2022 summer temperatures, as well as those impacts which would result from an equivalent summer if amplified by future warming as projected by CMIP-6 climate models (see methods) under future emission scenarios specified by the SSPs. Point estimates and error bars show the mean and standard deviation of impacts across climate models. Data on national administrative boundaries are obtained from the GADM database version 3.6 (https://gadm.org/).

Future climate change will amplify the magnitude of such heat extremes, thereby also amplifying their potential impact on inflation. To assess such effects, we make use of the fact that climate change will alter the distribution of future summer temperatures predominantly by shifting their mean43,44. We therefore add the future summer warming projected to occur from 2022 onwards in the CMIP-6 projections to the historical temperatures realised in 2022, and re-evaluate their impact using our empirical response functions (see methods for further details). This approach suggests that if amplified by future warming, an equivalent extreme summer (i.e., in the upper tail of the shifted temperature distribution) would – ceteris paribus - cause impacts on food inflation in Europe of 1.0 percentage-points (0.6–1.6, uncertainty range across climate models and empirical specifications) in 2035 under a high-emission scenario, or of 0.9 percentage-points (0.5–1.4) under a low-emission scenario (Fig. 4c). These constitute an amplification of the impacts of extreme heat on inflation in Europe by 30–50% due to climate change already by 2035. By 2060, the amplification of such extreme impacts would diverge under different emission scenarios, remaining at 1.1 percentage-points (0.6–1.8) under the most optimistic scenario compared to 1.8 percentage-points (1.0–3.2) under the most pessimistic scenario of emission mitigation, an amplification of nearly 200%. These results highlight the short-term risks to inflation posed by unpredictable heat extremes which are already occurring under present climatic conditions, and which will be amplified by future warming.

Discussion

This work has identified a number of weather variables with significant historical impacts on headline and food inflation globally (Supplementary Fig. S1), but limitations persist in providing a comprehensive relationship between weather conditions and inflation. For example, the fact that we do not find such significant or consistent impacts of precipitation changes on food prices may be surprising given the clear sensitivity of agricultural productivity to precipitation36. However, precipitation changes exhibit a higher spatial variability than temperature34 and the use of national-level data may therefore be a limiting factor in our ability to accurately detect such effects should they exist. The development of consistent datasets of consumer prices at higher spatial resolutions, such as for sub-national regions may reduce these issues to the extent that local prices reflect local production. To the extent that local prices reflect imported production, assessments of spill-overs via trade45 or pressures arising through global commodity prices may provide further interesting insights.

Second, our empirical results refer predominantly to food and headline inflation, whereas we find a limited response of other price aggregates to weather changes. However, the strong response of electricity demand to temperature5,6 suggests that impacts on electricity prices are plausible. Indeed, we find that electricity prices show some consistent and persistent response to temperature increases (Supplementary Fig. S1k), but with much larger uncertainty which precludes statements of significance at conventional levels. Lesser data availability for this more detailed price aggregate as well as complex and heterogeneous electricity price-setting practices may contribute to these large errors. However, as electricity supply is increasingly met with renewable sources, the price sensitivity to weather may change. A detailed analysis of electricity and other price aggregates may be a fruitful avenue of future work.

Compared to previous literature, our empirical results are similar to those of Mukherjee29 in identifying persistent impacts of temperature increases in both developed and developing countries. Moreover, they are similar to those of Faccia et al.28 in identifying that temperature increases in hot seasons cause the largest and most significant upwards pressures on food inflation. Our approach is qualitatively different to Faccia et al.28 in that it models the heterogeneity across seasons and regions using interactions of the temperature shocks with baseline temperatures rather than assessing shocks in specifically defined seasons. Faccia et al. find contemporaneous impacts of 0.38%-points on food inflation from a 1.5 C quarterly summer temperature increase. Evaluating the regression coefficients pertaining to average temperatures in our central model (shown in Column 1 of Supplementary Table S2) at the baseline temperature observed in our dataset on the three hottest months of the year on average across countries (23.5 C), and given a 1.5 C temperature increase, indicates an impact of 0.17%-points. Given that our data are monthly, we must further consider a temperature shock, which persists across all three months of a quarter to compare to Faccia et al., implying an impact of 0.49%-points which is closely consistent. The slightly larger estimates we obtain may result from the use of more granular climate data (monthly vs quarterly) which likely limits attenuation of the impact signal.

The implications of our empirical results under future temperature conditions are considerable regarding societal welfare in general and price stability in particular: our results suggest that climate change is likely to alter inflation seasonality, increase inflation volatility, inflation heterogeneity and place persistent pressures on inflation levels.

In our empirical results we find upward pressures on food and headline inflation from higher-than-normal temperatures, especially when occurring in hot months and countries. This implies short-term rises in inflation from exceptionally hot periods such as that experienced in Europe in the summer of 2022 (Fig. 4a, b). With the intensity of hot extremes and their impacts on inflation being amplified with continuing climatic change (Fig. 4c, d), while being unpredictable in the medium- to longer-term, this relationship is set to increase inflation volatility. This in turn may pose challenges to inflation forecasting and monetary policy, likely increasing the difficulty of identifying temporary supply shocks and disentangling them from more persistent drivers.

We find that the inflationary impact of temperature shocks depends on the baseline climatic conditions. At the same time, future climate change implies different warming levels depending on the season and latitude. Taken together, this implies that temperature shocks under future climate change would both amplify inflation heterogeneity (Fig. 2) and alter the seasonality of inflation within individual countries (Fig. 3b). Inflation heterogeneity poses challenges in monetary union areas such as the euro area, where larger inflationary pressures from climate change in southern Europe (Fig. 2 & 4) may increase inflation differentials, making the calibration of a single monetary policy more difficult46. Moreover, heterogeneous effects on inflation within an economic union such as the EU could exacerbate pre-existing welfare discrepancies, which can fuel anti-EU sentiment47. In addition, an altered inflation seasonality could pose additional challenges to inflation forecasting, which may however be (partially) mitigated through the development of weather-dependent forecasts for production48 and inflation49.

Finally, evaluating our empirical results under future temperature conditions suggests that – ceteris paribus - persistent upward pressures on annual food inflation of 1-3 percentage-points per-year could result from temperatures projected for 2035 (Fig. 2c). In addition, we test for adaptation via socio-economic development (Supplementary Fig. S8, Table S4 & S5 column 5), prolonged exposure to higher temperatures (Fig. 1 and all other empirical specifications), and adjustment to gradual warming (Supplementary Fig. S6k–t), with results suggesting that these forms of historical adaptation have been very limited (see earlier discussion). It should however be noted that our estimates assume constancy in other factors which may be important for future developments of inflation such as general macroeconomic developments and structural changes in the economy. Our estimates should therefore be understood as the likely exogenous pressure on inflation from future climate conditions based on the causal relationships inferred from the empirical models, in the absence of unprecedented adaptation. More persistent upward inflationary pressures from increasing temperatures under a changing climate would have important implications for monetary policy, as it would render the identification of drivers of inflation more difficult when relying on traditionally used models, and also risk the de-anchoring of inflation expectations. As a result, central banks may need to make monetary policy decisions also in response to weather and climate shocks, as in such a situation weather and climate shocks can no longer be considered temporary. Moreover, persistent upward pressures on inflation may have adverse effects on purchasing power, often with regressive distributional effects and potential impacts on social cohesion50, as well as inefficiency costs due to nominal rigidities and adverse interactions with taxation50. Overall, these results strongly highlight the importance for central banks and macroeconomic modelling in general to consider future climate change in their macroeconomic assessment and forecasting tools.

Future adaptation to climate change through unprecedented technological changes – which we do not explicitly model - offers an opportunity to limit pressures on inflation in a changing climate. For example, planned adoption of space cooling could limit heat stress impacts on labour productivity and crop switching could limit agricultural productivity losses, two major channels of impacts with potential relevance to inflation. Exploring the possibility for historically un-precedented adaptation to reduce impacts via adjustment to changes in long-term climate conditions indicates that it could do so substantially (Supplementary Fig. S14). However, without considerable mitigation of greenhouse gas emissions pressures on inflation would remain persistent and sizeable, even when accounting for such adaptation which goes beyond what has been observed historically. The efficacy and opportunity costs of the necessary investments in these adaptations also remain largely unknown and therefore present an important avenue for further research on the scope to limit the risks to inflation from a warming climate and intensifying heat extremes.

Methods

Inflation data

Data on national-level inflation of different price aggregates are obtained from a dataset developed by reference33 (see the Supplementary Methods for further information). The data used here constitute monthly, non-seasonally adjusted prices at different levels of aggregation. Data are available for 121 countries with varying temporal coverage from 1996-2021. The countries included cover most of the developed world (minus Australia and New Zealand where monthly data are not available), as well as large parts of the developing world. Coverage across South America and Africa is good, but large gaps exist in South East Asia where detailed information on price aggregates at monthly timescales are not available. Month-on-month inflation rates are used as the main dependent variable, estimated as the first difference in the logarithm of consumer price indices (CPI).

In a robustness test conducted in Fig. S9, we alternatively use monthly inflation data from the World Bank cross-country database on inflation39. Differences in the aggregation procedures exist and are documented extensively in reference33. Two important differences are the inclusion of imputed rents in some headline inflation indices in the World Bank data and differences in the aggregation of food (see Supplementary Methods for further details). We use the data compiled by reference33 as our main specification because the inclusion of imputed rents may bias estimates away from the impacts on widely consumed goods. In those countries where imputed rents are incorporated, they typically have a large weight, but there are many indices that do not incorporate them, notably including all European countries using the Harmonised Index of Consumer Prices. We find that the impacts on food inflation from mean temperature are qualitatively and quantitatively consistent when using World Bank data, Fig. S9. The response of headline inflation differs considerably, likely due to the inconsistent inclusion of imputed rents in headline inflation in the World Bank data.

Climate data

The primary source of climate data for this study is the ERA-5 reanalysis of historical observations32. ERA-5 combines satellite and in-situ observations with state-of-the-art assimilation and modelling techniques to provide estimates of climate variables with global coverage and at 6-hourly resolution. Daily 2 m air temperature and surface precipitation rates for the years 1990-2021 are used as well as monthly average temperature for the months of June, July and August in 2022 for use in Fig. 4. All data from ERA-5 is obtained on a regular 0.25-by-0.25-degree grid for the years 1990-2021. For the estimates of SPEI, we follow the literature51 in using monthly mean temperature and monthly precipitation totals from the Climate Research Unit (CRU) TS v4.05 for the years 1901-2021. This data is obtained at the same resolution and on the same grid as ERA-5.

Weather variables

Monthly, m, averages, \({\bar{T}}_{x,m}\), and standard deviations, \({\widetilde{T}}_{x,m}\), of daily ERA-5 temperatures are calculated at the grid cell, \(x\), level. Moreover, the relative exceedance of certain high precipitation thresholds, \({T}_{x}\), are calculated according to

where \({P}_{x,d}\) are daily precipitation totals, \(H\) the Heavide step function and \({D}_{m}\) the number of days in a given month. Following reference13, we use the 99th percentile of the distribution of historical daily rainfall to set thresholds locally (1990-2021).

Standardised Precipitation Evapotranspiration Indices (SPEI) are calculated following the methods of reference51, applying their publicly available code to monthly temperature and precipitation data from CRU TS v4.05. The SPEI calculation is based on a physical model of moisture balance and considers contributions to dry or wet conditions from both temperature and precipitation. It is a widely used tool to flexibly compare dry and wet conditions across countries. Moreover, its flexible estimation over different timescales allows exploration of different impact-relevant timescales. We estimate SPEI at one, two-, three-, six- and twelve-month timescales to flexibly assess the impacts of shocks across these timescales.

Spatial aggregation

We use gridded population estimates from the History database of the Global Environment (HYDE)52 to estimate national-level exposure to changes in these climate variables. The data are provided at 0.25-by-0.25-degree resolution by the Inter-Sectoral Impact Model Intercomparison Project (ISIMIP). Monthly average temperature, temperature variability and the measure of daily precipitation extremes are aggregated to the national level using a population weighted average. In this weighting we also account for the proportion of grid-cells falling within a given administrative unit, estimated by evenly distributing 100 points within each grid-cell and estimating the proportion which fall within the given administrative unit. Given these weightings, \({w}_{x,n},\) for all \({{{{{{\boldsymbol{N}}}}}}}_{{{{{{\boldsymbol{x}}}}}}}\) grid-cells falling at least partially within the administrative boundary of a country, \(c\), this weighted average reads:

for monthly average temperature for example. The equivalent procedure applies for temperature variability and the measure of daily precipitation extremes.

For SPEI, we first estimate binary variables indicating whether a grid cell is experiencing conditions which exceed a certain level of dry or wet (indicated as SPEI < and SPEI>, respectively in Eq. 3). We choose thresholds of one, one-point-five, two and two-point-five deviations to flexibly assess the exceedance of different thresholds. We then apply the same spatial aggregation procedure as outlined in Eq. 2 to estimate the proportion of population exposed to these excessively wet or dry conditions. By calculating the grid-cell level exceedance of certain SPEI thresholds and aggregating the proportion of national population exposed to these excess wet or dry conditions, we aim to limit the issue of spatially averaging over opposing effects. This is particularly relevant for precipitation given its larger spatial variability34.

The magnitude of the temperature seasonal cycle, \({\hat{T}}_{c}\) is estimated as the difference between the maximum and minimum national monthly temperatures within a given year, which is then averaged over the historical period (1990-2021) before use in the regression models. Deviations of average temperature, \(d{\bar{{{{T}}}}}_{{{{c}}}{{{,}}}{{{m}}}}\), and temperature variability, d\({\widetilde{T}}_{c,m}\), from their historical average (1990-2021) over the same calendar month are also calculated for use as dependent variables. This choice is intended to reflect the impact of deviations of monthly climate conditions from their historical seasonal patterns, following the intuition that the economy is well adapted to historical weather patterns from which deviations are a source of potential impacts. We note that the use of country-month fixed effects in the empirical model (see next section), results in an equivalent differencing process for the other independent variables.

Empirical framework for estimation of causal effects

The combination of price and climate data results in 27,340 country-month observations across 121 countries. We then apply fixed-effects panel regression models to identify the causal effects of changes in weather variables on national level inflation. Month-on-month national level inflation rates, \({dlCP}{I}_{c,m}\) are the dependent variable. Deviations of average temperature are included with an interaction with the average temperature level, whereas deviations of temperature variability are included with an interaction with the magnitude of the seasonal temperature cycle, following the heterogeneities identified in previous studies on the impacts of climate conditions on growth12. The interaction with the average temperature level introduces a heterogeneity in the response to temperature shocks across both geographical locations and seasons, based on the prevailing temperature of those regions and seasons. This choice follows previous literature which finds larger impacts on inflation in hotter seasons28, and larger impacts on different economic factors in hotter regions1,2,10,11. Daily precipitation extremes are included with an interaction with the monthly average temperature level (having also tested alternative interactions with the monthly share of annual precipitation). Both positive (excess wet) and negative (excess dry) SPEI threshold exceedance are used. For the former we find no significant effect of interactions with the monthly average temperature level or the monthly share of annual precipitation and as a result include no interactions in our main specification. For the latter we find a significant effect of an interaction with monthly average temperature level and therefore include this in our main specification. We include all weather variables simultaneously to ensure that any effects we identify occur independently of one another and are therefore additive12,34. Each weather variable is included with 11 lags in addition to the contemporaneous term, to assess the delayed effects of monthly weather shocks over the course of the following year and in particular whether they are recovered or persist over this time frame.

Our baseline specification includes country, \({\mu }_{c}\), date, \({\eta }_{t},\) and country-month, \({\pi }_{c,m},\) fixed effects, in addition to country specific linear time-trends, \({\gamma }_{c}y\). Country fixed effects account for unobserved differences between regions such as baseline climate and inflation rates, while the use of date fixed effects accounts for contemporaneous global shocks to both variables such as El Nino events or global recessions. The inclusion of country-month fixed effects accounts for country specific seasonality – a crucial step given the strong seasonal cycle in both monthly inflation and weather data. This constitutes an additionally conservative step by ignoring inflation impacts which could repeatedly occur seasonally due to seasonal weather patterns. This ensures that our results only estimate the impacts of deviations from normal seasonal conditions. Finally, our baseline specification accounts for country specific time trends to avoid spurious correlations arising from common trends. This is important given the presence of strong warming trends in the historical period which could cause spurious correlations to inflation changes. Interestingly, we find that accounting for these linear trends enhances the magnitude of estimated effects, suggesting that it indeed assists in removing estimation biases. Estimates without linear time trends are nevertheless qualitatively and quantitatively similar. The regression model of the baseline specification then reads:

where \(t\) is the date in terms of a given year and month and \({\varepsilon }_{c,t}\) is the country-date residual error. Note that here \(t\) refers to the date i.e., the month of a specific year, whereas m refers to all general occurrences of a particular month, and y refers to the particular year. In our baseline specification, errors are clustered by country. Coefficients \(\alpha\) and \(\beta\) describe the common impact across countries and months of a 1-unit increase in each independent variable on month-on-month inflation rates and are shown in Tables S2 and S3.

In alternative robustness tests we estimate a dynamic model in which we also include 11 lags of the inflation rates, \({dlCP}{I}_{c,t}\) to account for serial correlations due to for example business cycles (Supplementary Tables S4 & S5 Column 2, Fig. S5), account for cross-sectionally correlated and heteroskedastic errors using Driscoll Kraay errors38 (Supplementary Tables S4 & S5 Column 3, Fig. S5), and test an inflation database provided by the World Bank (Supplementary Tables S4 & S5 Column 7 Fig. S9). Moreover, in an additional robustness test we include controls for transitions in monetary policy using data from the Comprehensive Monetary Policy Framework project53. We use the data in its most granular form (32 classifications of monetary policy frameworks) introducing dummy variables in the regression for each potential framework. Our results are qualitatively and quantitatively robust to these additional controls (Supplementary Tables S4 & S5 Column 4, Fig. S6a–j). Furthermore, we also estimate models in which we include additional interactions of each climate variable with a binary term indicating whether a given country has above or below median national income per capita (based on world bank estimates of GDP and population, see Supplementary Tables S4 & S5 Column 5, Fig. S8), and also when normalising monthly inflation rates by their interannual standard deviation to account for differing baseline inflation volatilities (see Supplementary Tables S4 & S5 Column 6, Fig. S7). These robustness tests of our main results are summarised in Supplementary Tables S3 and S4 of the supplementary information.

We do not include further controls for variables which affect inflation such as employment and economic output for a number of reasons. First, important aspects of their effects which are linked to business cycles are already accounted for by the use of a dynamic panel with lagged inflation as independent variables, as used in similar contexts with global panels28. Second, such data is not available at the monthly resolution used here for most countries in our panel. Third, including such control variables could only alter our results if they were correlated with the weather variables. Given the strong a-priori assumption of exogeneity between weather and these variables, the presence of such correlations would indicate that these control variables are themselves impacted by the weather variables. Therefore, any alteration to our results when including these variables would not alter our main interpretation but rather indicate that these variables (employment/output) are a mediating variable through which weather impacts inflation. While such mechanistic insights may be interesting, due to data availability they are beyond the scope of our manuscript which primarily aims to understand the overall impacts of climate variables on inflation.

Cumulative marginal effects

In Fig. 1 and a number of supplementary figures we display the results of the empirical models by plotting the cumulative marginal effects of each climate variable. These cumulative marginal effects reflect the theoretical cumulative impact on prices from a 1-unit climate shock. These effects are estimated by summing the lagged coefficients (shown in Eq. (3)) which are relevant to a particular climate variable. Moreover, because of the use of interaction terms, the coefficient pertaining to the interaction term must be multiplied by a chosen value of the moderating variable of the interaction. For example, in Fig. 1 the cumulative marginal effects, \({ME}\), of average temperature are plotted, having been calculated as follows:

Calculating the cumulative marginal effects therefore requires an evaluation of the coefficients at a particular baseline temperature, and their summation over the different lags. In Fig. 1, these marginal effects are plotted when evaluating the above summation over different numbers of lags, from 0 to 11 months after the initial shock. We show results having evaluated Eq. (4) at the temperatures observed at the lower and upper quartiles and median of the distribution of country-month temperatures present in our data. We conduct equivalent procedures for estimating and plotting the cumulative marginal effects for the other climate variables in the Supplementary Figs. S1, S2 & S4–S9.

Climate model data

Daily 2-m temperature and precipitation totals are taken from 21 climate models participating in CMIP-6 under the most pessimistic (SSP-RCP8.5, referred to as SSP585 in the main text) and most optimistic (SSP-RCP2.6, referred to as SSP126) greenhouse gas emission scenario from 2015-2100. SSP126 provides approximately equivalent emission forcing as the orderly and dis-orderly transition scenarios provided by the Network for Greening the Financial System (NGFS), with an average end-of-century global temperature change of 1.7 C. SSP585 provides stronger emission forcing (4.9 C end-of-century global temperature change) than the hot-house world scenario from NGFS (3.2 C end-of-century temperature change). While considered by some as un-realistic54, RCP8.5 tracks recent emissions well and is arguably likely to provide a good estimation of emission forcing up until mid-century based on current (2020) policies55. The data have been bias-adjusted and statistically downscaled to a common half-degree grid to reflect the historical distribution of daily temperature and precipitation of the W5E5 dataset (WATCH Forcing Data Methodology applied to the ERA5 data) using the trend-preserving method developed by ISIMIP56,57.

Estimating impacts from projected future warming

We evaluate the hypothetical impact on inflation which future weather conditions under projected climate change would cause given our empirical models. We note the important distinction that these are not projections of future inflation, but simply an evaluation of this particular mechanism via which climate conditions effect inflation under future conditions. Important factors including demographic developments, changes in the consumption basket, and fiscal and monetary policies are purposefully held fixed (although we note that our empirical results are strongly robust to changes in the regime of monetary policy, Supplementary Fig. S6a–j; also see the discussion included in the main part of the manuscript).

To do so, we evaluate the first terms pertaining to monthly average temperatures of Eq. 3 under future temperature conditions. That is, we calculate future monthly average national temperatures from the CMIP-6 models (using a population weighting equivalent to that used with the historical data), \({\bar{T}}_{c,y > 2020,m}\), as well as their deviations from the 1990-2021 average, \(\Delta {\bar{T}}_{c,y > 2020,m}\), and then apply these to the first terms of Eq. 3 to calculate the impacts on inflation:

Note that in practice, \(m-L\), may need to refer to a month in the preceding year. These impacts are then averaged over 30-year periods centered on the future period in question (usually 2035 or 2060). These impacts at the country-month level are then either summed over the year to provide estimates of annual impacts on inflation as in Fig. 2 or presented at the monthly level as in Fig. 3. This procedure is conducted separately for each of the 21 climate models in the CMIP-6 ensemble, from which the mean and standard deviation are presented as central estimates and errors.

In Fig. 4 we assess the impacts of the 2022 extreme summer heat in Europe using ERA-5 estimates of monthly temperatures in June, July and August. In this case, the total impacts on inflation from those three summer months are estimated using the temperature levels in those months, \({\bar{T}}_{c,m}\), their deviation from the historical (1990-2021) average, \(\Delta {\bar{T}}_{c,m}\), and the relevant terms from Eq. 3 pertaining to average temperature impacts:

As such, these impacts reflect the estimated effects on net inflation from June 2022 to August 2023 from the three months of temperature in June, July and August of 2022.

We further assess how the impacts from such extremes could be amplified under future warming. To do so, we evaluate the future warming occurring between 2022 and 2035 or 2060 in each summer month in each country (using the difference between 30-year averages of temperature centered on 2022 and 2035 or 2060 in each climate model and emission scenario). This additional month-specific warming is then added to the historically observed 2022 summer temperatures, and the impacts on inflation evaluated as before using Eq. 6. This approach assumes that future warming will shift the mean of the distribution of possible summer temperatures and does not account for the potential role of changing temperature variability in altering the intensity of future temperature extremes. However, evidence for a role of temperature variability in enhancing extremes at monthly time-scales is limited43,44.

When presenting estimated inflationary impacts under projected future climate, we also present country-level impacts aggregated to larger spatial regions. In Figs. 2 and 4 we do so using a population weighted average (using World Bank estimates of national level population in 2017) to reflect the human exposure to future inflationary pressures. In Fig. 3a and S3d we take binned averages across latitudinal zones to convey the relationship between latitude and the seasonality of inflation response and impacts. Countries are considered part of a latitudinal zone if their centroid falls within the zone’s boundaries, and in this context, we use an average without population weighting to reflect the nature of the relationship between latitude and impacts rather than to reflect the average human exposure to impacts.

Uncertainty in estimated impacts from future weather conditions under projected warming arises from a combination of factors, including the choice of empirical specification, the range of climate model projections, as well as future emission scenarios if their differences are not explicitly compared. In Figs. 2–4 we show projection estimates for a particular empirical specification, showing the range of projections across climate models and emission scenarios visually. In the text, we discuss the robustness of these figures to the use of different empirical specifications (results of which are shown in the Supplementary Information Figs. S10–S24), and report estimates of projected impacts with an uncertainty range accounting for these contributing factors. This uncertainty range spans the lowest projection across the empirical specifications shown in columns 1-7 of Supplementary Tables S4 & S5 (and emission scenario unless explicitly comparing their differences) combined with the lower range of climate model projections (the mean minus one standard deviation of impacts across climate models), and the largest projection across empirical specifications combined with the higher range of climate model projections (the mean plus one standard deviation of impacts across climate models). This framework provides a transparent assessment of uncertainty across a range of factors.

Data availability

ERA-5 climate data are publicly available at https://www.ecmwf.int/en/forecasts/datasets/reanalysis-datasets/era5, and raw data is available for 10 of the bias-adjusted climate models from the ISIMIP repository at: https://data.isimip.org/. Raw data on price indices was taken from a forthcoming publicly available dataset developed by ref. 33. All processed climate data and anonymised inflation data (until publication of the inflation data-set by ref. 33) necessary for replication of our analysis is publicly available at: https://doi.org/10.5281/zenodo.10183679. Source data required only for reproducing the main figures is also available at the same repository.

Code availability

All code used for the replication of our analysis is publicly available at: https://doi.org/10.5281/zenodo.10183679.

References

Dasgupta, S. et al. Effects of climate change on combined labour productivity and supply: an empirical, multi-model study. Lancet Planet. Health 5, e455–e465 (2021).

de Lima, C. Z. et al. Heat stress on agricultural workers exacerbates crop impacts of climate change. Environ. Res. Lett. 16, 044020 (2021).

Moore, F. C., Baldos, U., Hertel, T. & Diaz, D. New science of climate change impacts on agriculture implies higher social cost of carbon. Nat. Commun. 8, 1–9 (2017).

Moore, F. C., Baldos, U. L. C. & Hertel, T. Economic impacts of climate change on agriculture: a comparison of process-based and statistical yield models. Environ. Res. Lett. 12, 065008 (2017).

Auffhammer, M., Baylis, P. & Hausman, C. H. Climate change is projected to have severe impacts on the frequency and intensity of peak electricity demand across the United States. Proc. Natl. Acad. Sci. 114, 1886–1891 (2017).

Wenz, L., Levermann, A. & Auffhammer, M. North–south polarization of European electricity consumption under future warming. Proc. Natl. Acad. Sci. 114, E7910–E7918 (2017).

Song, X. et al. Impact of ambient temperature on morbidity and mortality: an overview of reviews. Sci. Total Environ. 586, 241–254 (2017).

Guo, Y. et al. Temperature variability and mortality: a multi-country study. Environ. Health Perspect. 124, 1554–1559 (2016).

Dell, M., Jones, B. F. & Olken, B. A. Temperature shocks and economic growth: Evidence from the last half century. Am. Econ. J. Macroecon. 4, 66–95 (2012).

Burke, M., Hsiang, S. M. & Miguel, E. Global non-linear effect of temperature on economic production. Nature 527, 235–239 (2015).

Kalkuhl, M. & Wenz, L. The impact of climate conditions on economic production. Evidence from a global panel of regions. J. Environ. Econ. Manag. 103, 102360 (2020).

Kotz, M., Wenz, L., Stechemesser, A., Kalkuhl, M. & Levermann, A. Day-to-day temperature variability reduces economic growth. Nat. Clim. Change 11, 319–325 (2021).

Kotz, M., Levermann, A. & Wenz, L. The effect of rainfall changes on economic production. Nature 601, 223–227 (2022).

Bressler, R. D. The mortality cost of carbon. Nat. Commun. 12, 1–12 (2021).

Rode, A. et al. Estimating a social cost of carbon for global energy consumption. Nature 598, 308–314 (2021).

Burke, M., Davis, W. M. & Diffenbaugh, N. S. Large potential reduction in economic damages under UN mitigation targets. Nature 557, 549–553 (2018).

Moore, F. C. & Diaz, D. B. Temperature impacts on economic growth warrant stringent mitigation policy. Nat. Clim. Change 5, 127–131 (2015).

Dotsey, M. & Ireland, P. The welfare cost of inflation in general equilibrium. J. Monet. Econ. 37, 29–47 (1996).

Chu, A. C. & Lai, C.-C. Money and the welfare cost of inflation in an R&D growth model. J. Money Credit Bank 45, 233–249 (2013).

Gazdar, H. & Mallah, H. B. Inflation and food security in Pakistan: Impact and coping strategies. IDS Bull 44, 31–37 (2013).

Nord, M., Coleman-Jensen, A. & Gregory, C. Prevalence of US food insecurity is related to changes in unemployment, inflation, and the price of food. (2014).

Abaidoo, R. & Agyapong, E. K. Commodity price volatility, inflation uncertainty and political stability. Int. Rev. Econ. 1–31 (2022).

Molina, G. G., Montoya-Aguirre, M., and Ortiz-Juarez, E. Addressing the cost-of-living crisis in developing countries: Poverty and vulnerability projections and policy responses. U. N. High-Level Polit. Forum Sustain. Dev. HLPF (2022).

Bolton, P. et al. The green swan. BIS Books (2020).

Boneva, L., Ferrucci, G. & Mongelli, F. P. To be or not to be “green”: how can monetary policy react to climate change? ECB Occas. Pap. (2021).

Drudi, F. et al. Climate change and monetary policy in the euro area. (2021).

Parker, M. The impact of disasters on inflation. Econ. Disasters Clim. Change 2, 21–48 (2018).

Faccia, D., Parker, M. & Stracca, L. Feeling the heat: extreme temperatures and price stability. ECB Work. Pap. Ser. (2021).

Mukherjee, K. & Ouattara, B. Climate and monetary policy: do temperature shocks lead to inflationary pressures? Clim. Change 167, 1–21 (2021).

Ciccarelli, M., Kuik, F. & Hernández, C. M. The asymmetric effects of weather shocks on euro area inflation. ECB Work. Pap. Ser., (2023).

Moessner, R. Effects of Precipitation on Food Consumer Price Inflation. (2022).

Hersbach, H. et al. The ERA5 global reanalysis. Q. J. R. Meteorol. Soc. 146, 1999–2049 (2020).

Osbat, C., Parker, M. & Franceschi, E. Navigating the global inflation surge: Rising tide or choppy wake? ECB Mimeo (2024).

Auffhammer, M., Hsiang, S. M., Schlenker, W. & Sobel, A. Using weather data and climate model output in economic analyses of climate change. Rev. Environ. Econ. Policy (2020).

Wheeler, T. R., Craufurd, P. Q., Ellis, R. H., Porter, J. R. & Prasad, P. V. Temperature variability and the yield of annual crops. Agric. Ecosyst. Environ. 82, 159–167 (2000).

Liang, X.-Z. et al. Determining climate effects on US total agricultural productivity. Proc. Natl. Acad. Sci. 114, E2285–E2292 (2017).

Damania, R. The economics of water scarcity and variability. Oxf. Rev. Econ. Policy 36, 24–44 (2020).

Driscoll, J. C. & Kraay, A. C. Consistent covariance matrix estimation with spatially dependent panel data. Rev. Econ. Stat. 80, 549–560 (1998).

Ha, J., Kose, M. A. & Ohnsorge, F. One-stop source: A global database of inflation. J. Int. Money Finance 102896 (2023).

Arias, P. et al. Climate Change 2021: The Physical Science Basis. Contribution of Working Group14 I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Technical Summary. (2021).

Riahi, K. et al. The shared socioeconomic pathways and their energy, land use, and greenhouse gas emissions implications: an overview. Glob. Environ. Change 42, 153–168 (2017).

NGFS. NGFS Climate Scenarios for Central Banks and Supervisors. (2021).

Lenton, T. M., Dakos, V., Bathiany, S. & Scheffer, M. Observed trends in the magnitude and persistence of monthly temperature variability. Sci. Rep. 7, 1–10 (2017).

van der Wiel, K. & Bintanja, R. Contribution of climatic changes in mean and variability to monthly temperature and precipitation extremes. Commun. Earth Environ. 2, 1–11 (2021).

Kuhla, K., Willner, S. N., Otto, C., Wenz, L. & Levermann, A. Future heat stress to reduce people’s purchasing power. PloS One 16, e0251210 (2021).

Consolo, A., Koester, G., Nickel, C., Porqueddu, M. & Smets, F. The Need for an Inflation Buffer in the Ecb’s Price Stability Objective–the Role of Nominal Rigidities and Inflation Differentials. ECB Occas. Pap. (2021).

Kuhn, T., Van Elsas, E., Hakhverdian, A. & van der Brug, W. An ever wider gap in an ever closer union: Rising inequalities and euroscepticism in 12 West European democracies, 1975–2009. Socio-Econ. Rev. 14, 27–45 (2016).

Iizumi, T. et al. Prediction of seasonal climate-induced variations in global food production. Nat. Clim. Change 3, 904–908 (2013).

Vidal-Quadras Costa, I., Saez Moreno, M., Kuik, F. & Osbat, C. Forecasting food inflation with climate and commodities data using a non linear model. forthcoming.

Cecioni, M. et al. The Ecb’s Price Stability Framework: Past Experience, and Current and Future Challenges. (2021).

Vicente-Serrano, S. M., Beguería, S. & López-Moreno, J. I. A multiscalar drought index sensitive to global warming: the standardized precipitation evapotranspiration index. J. Clim. 23, 1696–1718 (2010).

Klein Goldewijk, K., Beusen, A., Van Drecht, G. & De Vos, M. The HYDE 3.1 spatially explicit database of human-induced global land-use change over the past 12,000 years. Glob. Ecol. Biogeogr. 20, 73–86 (2011).

Cobham, D. Monetary policy frameworks since Bretton Woods, across the world and its regions. World Its Reg. Sept. 12 2022 (2022).

Hausfather, Z. & Peters, G. P. Emissions–the ‘business as usual’story is misleading. Nature 577, 618–620 (2020).

Schwalm, C. R., Glendon, S. & Duffy, P. B. RCP8. 5 tracks cumulative CO2 emissions. Proc. Natl. Acad. Sci. 117, 19656–19657 (2020).

Cucchi, M. et al. WFDE5: bias-adjusted ERA5 reanalysis data for impact studies. Earth Syst. Sci. Data 12, 2097–2120 (2020).

Lange, S. Trend-preserving bias adjustment and statistical downscaling with ISIMIP3BASD (v1. 0). Geosci. Model Dev. 12, 3055–3070 (2019).

Acknowledgements

We gratefully acknowledge the work of Miles Parker and Chiara Osbat in collecting the data on consumer price indices and providing it to us prior to its publication. We also thank them both for insightful feedback on early versions of the manuscript. MK gratefully acknowledges funding from the Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH on behalf of the Government of the Federal Republic of Germany and Federal Ministry for Economic Cooperation and Development (BMZ). Part of the work for this paper was also conducted during a joint project procured by the European Central Bank. We note that the views expressed are those of the authors and should not be reported as representing the views of the European Central Bank (ECB) or the Eurosystem.

Author information

Authors and Affiliations

Contributions

M.K. designed the weather variables, empirical approach, the use of physical climate models, conducted all analyses, produced all figures and lead the writing of the manuscript. F.K. proposed the collaboration, contributed to the design of the weather variables and the empirical approach as well as the interpretation of the results and writing of the manuscript. E.L. contributed to the design of the weather variables and the empirical approach as well as the interpretation of the results and writing of the manuscript. C.N. gave feedback on results and contributed to the writing of the manuscript.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Communications Earth & Environment thanks Simon Dikau and the other, anonymous, reviewer(s) for their contribution to the peer review of this work. Primary Handling Editors: Alessandro Rubino and Clare Davis. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Kotz, M., Kuik, F., Lis, E. et al. Global warming and heat extremes to enhance inflationary pressures. Commun Earth Environ 5, 116 (2024). https://doi.org/10.1038/s43247-023-01173-x

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s43247-023-01173-x

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.