Abstract

Under the dual carbon goals in China, the transition to a net-zero carbon economy requires massive amounts of capital, which must be provided and facilitated by financial institutions. Yet, there are no unified, publicly available disclosures of the investment carbon footprint of Chinese financial institutions, leaving them facing great climate-related risks. Here we demonstrate that the aggregated financed emissions show an upward trend from 2015, and the investment portfolios are more exposed to carbon-intensive assets, based on the equity portfolios of China’s 105 fund firms. We further explore the decarbonization potential for fund firms and show that sustainability-aware fund firms are characterized by financed emission reductions and carbon efficiency gains. To fulfill sustainable investing, China’s institutional investors should focus on investment allocations shifting to high-tech sectors and target the improvement of self-reported carbon emissions.

Similar content being viewed by others

Introduction

The current emission pledge to the Paris Agreement appears insufficient to hold the global average temperature increase below 1.5 °C1,2. The transition to net-zero is a strategic imperative for the financial sector, with trillions in capital that are aligned towards meeting the Paris Agreement3,4. Under the commitment, some financial institutions (i.e., insurers, asset managers, and fund firms) are competing to showcase their green ambitions and committing to align their portfolios with 1.5 °C based on a decarbonization trajectory by 20505. As the world’s largest CO2 emitter6, the Chinese government has committed itself to achieve peak carbon emissions before 2030 and carbon neutrality before 20607. Capital markets, particularly environmental, social and governance (ESG) investing, have become an important force in supporting carbon neutrality strategies. Consequently, Chinese financial institutions as active participants in sustainable investing, facilitated and supported the flow of trillion dollars in ESG capital to mitigate climate change.

Financial institutions that want to align their financial flows with sustainable ESG investing, need to assess their investment carbon footprint accurately8. This footprint is multidimensional and spans all factors in ESG, we only focus on the environmental factor in this paper. Partnership for Carbon Accounting Financials (PCAF) and Task Force on Climate-related Financial Disclosures (TCFD) have provided standardized guidance on calculating and tracking carbon footprint embodied in investment activities year over year, and comparing these with the targeted goals9,10. ESG investing has gained popularity in the Chinese mutual fund markets over the past decade, which places greater demands on environmental information disclosure11. China has also made efforts to decarbonize within its booming economy via a package of low-carbon development policies, including improved climate-related and environmental information disclosure12,13. As the largest institutional investors in the stock market, Chinese fund firms offer an important route towards investing in the equity markets to achieve carbon neutrality goals14. And some of the investors have started to pay attention to their investment portfolios and disclosed their carbon footprints voluntarily15,16. However, the impact of this action will likely remain marginal as long as lawmakers do not supplement compulsory reporting standards. There is, to date, no unified regulatory canvas for China’s financial institutions to impose a strict framework for reporting investment carbon footprint.

Financial institutions’ ability to make a comprehensive assessment of portfolios’ climate profiles relies on being able to analyze trustworthy corporate disclosures of carbon emissions. This is a notoriously complicated task because of the dearth of firm-level CO2 emissions data and even generating self-reporting bias8,17. The firm-level carbon disclosures concentrated in Europe, North America, and other developed countries18,19 such as the compulsory mandate for annual disclosure of GHG emissions in the UK20. Developing countries, have little commitment to carbon mitigation and disclosure21,22. In addition, it is well accepted that Scope1 emissions can’t sufficiently draw the full picture of investment carbon footprint, and Scope 3 embodied in the supply chain should also be focused on. However, the main issue is that the overarching account of Scope 3 emissions is quite hard to assess.

The all above points imply that China’s financial institutions remain largely in the dark when it comes to accurately measuring the carbon footprint of their investment portfolios. In this study, we only focused on Scope 1 and Scope 2 emissions and used methodologies introduced by TCFD to study the equity portfolios of 105 Chinese public fund firms over the period from 2010 to 2020. We first accounted for and analyzed the trends in financed emissions and carbon intensities of the fund firms’ investment portfolios. The study also revealed the drivers of financed emissions to help identify key exposures to carbon-related risks and potentials for carbon reductions. It can guide in embedding ESG principles into institutional investors’ portfolio decarbonization strategies and provide compelling insights for policymakers and investors.

Results

Trends in the carbon footprints of 105 fund firms’ equity portfolios

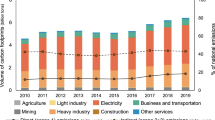

Figure 1 shows the trends in total financed emissions embodied in the equity portfolios of China’s 105 fund firms, as shown in Eq. (1). Overall, it presents a fluctuating trend from 2010 to 2015, which dramatically increased from 100.26 million tons (Mt) in 2010 to a high point of 183.11 Mt in 2012, and then decreased to 87.21 Mt in 2015. After 2015, total financed emissions suffered a steady rise, reaching a second peak of 168.40 Mt in 2018 (Supplementary Table 2). There then, the total volume declined slightly and stabilized at the level of 159.00 Mt in 2020. Zhang et al. calculated embodied carbon emissions in equity portfolios of the leading asset managers and found that there are prominent differences in the volume of financed emissions of different asset managers23. There has been a rapid increase in financed emissions for most Chinese asset managers, which is related to the investment structure. They were from the investment firms themselves rather than environmentalists, and their financed emissions were more concentrated in carbon-intensive sectors like Electricity, Gas and Water. However, foreign asset managers are building portfolios aligned with climate change goals with financed emissions and carbon intensities declining over the past decades. Europe, the world’s leading economic region having committed to carbon neutrality with the best legal system, has not only set limits on the total carbon emissions for its member states but also mandatorily required financial institutions to report climate-related disclosures24. Similarly, the oscillating fluctuations in the financed emissions of Chinese fund firms were mainly influenced by carbon-intensive sectors, which accounted for approximately 80% of the total financed emissions. Financed emissions of Electricity, Gas and Water sector contributed the most with a consistent ratio of ~50% of the total financed emissions. Notably, it largely contributed to the peak of total financed emissions in 2012 and then dropped from 113.12 Mt in 2012 to 42.80 Mt in 2015. Similarly, financed emissions of Metal Smelting decreased by 48.03%, reaching a low point of 9.75 Mt in 2015. Overall, fund firms adjusted portfolios based on macroeconomic conditions. China stimulated the construction of basic industrial facilities such as electricity and steel prior to 2012 in response to the shock of the financial crisis, which pulled up total financed emissions. The ongoing impact of the global macroeconomy from 2012 to 2015, causing weak demand in traditionally carbon-intensive products, triggered the withdrawal of capital from these sectors.

a Total financed emissions by sectors. The gray line represents the financed emissions of Top 10 Chinese fund firms. The pink shade represents the sum of financed emissions except for six carbon-intensive sectors. b Trends in Top 10 fund firms’ financed emissions (FF represents fund firm). In the panel, the thick lines in the thick gray box denote the interquartile range and the median, and the thin lines outside the box denote the maximum and minimum values. The point inside the box represents specific values of financed emissions of Top 10 fund firms. c Top 10 fund firms financed emissions by carbon-intensive sectors in 2010, 2015, and 2020. See detailed results in Supplementary Table 3.

Total financed emissions were mainly contributed by the Top 10 Chinese fund firms, altogether 88.77 Mt in 2020, accounting for 55.83% of total volume. The overall trend of the Top 10 firms remained consistently rising but showed varied degrees of growth. Fund 8 with 6.90 Mt of financed emissions in 2020, increased by 3.10 times compared to 2010, and Fund 5 and Fund 1 increased by 2.98 times and 0.98 times, respectively. From the perspective of the drivers of financed emissions, we analyzed the Top 10 fund firms at the carbon-intensive sectoral level. On the whole, financed emissions increased in almost all carbon-intensive sectors, including Electricity, Gas, and Water as well as Metal Smelting being the two drivers that played a notable role in promoting the growth of financed emissions. Specifically, Electricity, Gas and Water was the largest contributor to financed emissions, with a possible reason for this being that they continued to occupy an irreplaceable position in investment portfolios. Notably, Fund 1 was responsible for 9.57 Mt financed emissions from Electricity, Gas, and Water in 2020, resulting in 72.77% of its financed emissions and increased by 2.61 times compared to 2010. Similarly, Fund 5’s rapid growth in financed emissions was also driven by Electricity, Gas, and Water, which increased from 0.08 Mt in 2010 to 5.62 Mt in 2020. In addition, Fund 2 reached 10.71 Mt of financed emissions in 2020, of which Metals Smelting contributed the most with a ratio of 30.01%. Financed emissions from Metals Smelting in Fund 8 and Fund 9 increased by 1.57 Mt and 0.96 Mt, accounting for 24.79% and 25.22% in 2020, respectively.

The effects of carbon exposure on financed emissions

The metric Weighted Average Carbon Intensity (WACI) indicates a portfolios’ exposure to carbon-intensive assets9, which can be used for evaluating carbon-related risks. Additionally, Carbon Emissions to Revenue Intensity (CERI) measures total financed emissions divided by economic activity, with higher values indicating more efficiency. Overall, the average WACI for 105 fund firms showed a fluctuating downward trend, with two peaks at 624.76 tonnes CO2 M$-1 in 2012 and 577.45 tonnes CO2 M$−1 in 2018.

Most of the fund firms visibly reduced their holdings in carbon-intensive sectors, and mainly concentrated on Coal Mining and Electricity, Gas, and Water. Fossil fuel divestments could be presumably attributed to Chinese fund firms having started to allocate their capital in socially responsible ways. The average WACI of the Top 10 fund firms was slightly above the overall average WACI and each fund firm showed varied degrees of decline (Fig. 2a). Specifically, Fund 4 decreased most over the period, from 635.40 tonnes CO2 M$−1 in 2010 to 282.25 tonnes CO2 M$−1 in 2020. This was ascribed to the reduction in share of investment in Coal Mining (−4.66%) and Electricity, Gas, and Water (−0.80%), with only 6.87% of capital distributed in carbon-intensive sectors (Fig. 3a). In a similar vein, Fund 10 decreased from 685.14 tonnes CO2 M$−1 in 2010 to 361.29 tonnes CO2 M$−1 in 2020, which was mainly divesting from Petroleum Processing and Coking (−0.73%) as well as Raw Chemical Materials and Chemical Products (−7.42%).

a Trends in Top 10 fund firms’ Weighted Average Carbon Intensity (WACI). b Trends in Top 10 fund firms’ Carbon Emissions to Revenue Intensity (CERI). The red and blue lines indicate the average WACI (CERI) of all Chinese fund firms and the average WACI (CERI) of the Top 10 fund firms, respectively. See detailed results in Supplementary Table 2. In each panel, the thick lines in the thick gray box denote the interquartile range and the median, and the thin lines outside the box denote the maximum and minimum values. The points inside the box represent specific values of WACI (CERI) of Top 10 fund firms.

The variation of the average CERI shows a bimodal structure overall (Fig. 2b), rising from 356.49 tonnes CO2 M$−1 in 2010 to the first peak of 654.36 tonnes CO2 M$−1 in 2012, and then decreasing to 415.07 tonnes CO2 M$−1 in 2015. From 2016 to 2020, the average CERI reached the second peak in 2018 (608.06 tonnes CO2 M$−1) and then entered a continuously downward trend, reaching 493.42 tonnes CO2 M$−1 in 2020. The trend of average CERI of Top 10 fund firms remained largely consistent with the overall, whereas it maintained a continuously upward trend since 2016 and reached 673.86 tonnes CO2 M$−1 in 2020. For most of the fund firms, the share of revenue in carbon-intensive sectors was low (Fig. 3b), such as Electricity, Gas, and Water with the highest financed emissions but underperformed in revenue over the last decade. Furthermore, all the Top 10 fund firms displayed decreases in their shares of revenue in carbon-intensive sectors. Fund 5’s share of revenue in carbon-intensive sectors fell from 33.51% in 2010 to 12.08% in 2020, with a decrease of 21.43%, mainly due to the reductions in Coal Mining (−11.31%) and Metal Smelting (−14.71%). Similarly, both Fund 3 and Fund 4 showed decreases in Coal Mining (2.76% and 4.03%, respectively) and Metals Smelting (6.82% and 7.28%, respectively). In addition, it can be seen that the shares of revenue in Petroleum Processing and Coking, Nonmetal Products as well as Electricity, Gas, and Water were quite low and investees in these sectors had seen their profit margins shrink due to the contraction in both energy demand and the decarbonization process.

Carbon reduction potential for fund firms

Financed emissions can predict the future trend of portfolios’ carbon footprints. Between 2010 and 2020, there has been an increase in financed emissions for the vast majority of fund firms, while some fall, indicating a clear tendency to reduce emissions. In terms of carbon intensity indicators, the rise in financed emissions is accompanied by a fall in WACI and CERI. In particular, they tended to invest less in heavy industries such as Electricity, Gas and Water and Metal Smelting, and divested some of their lower-yielding holdings, indicating a degree of divestment from carbon-intensive assets. In addition, some fund firms have seen their financed emissions fall while their carbon intensities have risen, suggesting that there is a risk of greenwashing as the carbon exposure of their portfolios has not shrunk distinctly. In this study, it can be observed that there are heterogeneities among Chinese fund firms. Therefore, we further classify them into three categories based on the trend of the financed emissions and carbon intensities from 2016 to 2020 (Fig. 4), and select one as a representative case study, respectively.

The orange line shows the trends in Carbon Emissions to Revenue Intensity. Each row of the graph represents a fund firm owning the same characteristics. a–c show the trends of carbon footprints of the representative fund firms - Fund A, Fund B, and Fund C. d–f represent the trends in carbon intensities (Weighted Average Carbon Intensity and Carbon Emissions to Revenue Intensity) of Fund A, Fund B, and Fund C, respectively.

Fund a maintained a consistently upward trend in financed emissions over this period, at an annual growth of 72.45%. Financed emissions embodied in carbon-intensive sectors are important drivers. It can be also observed that with the rise of financed emissions in Metals Smelting, it drove financed emissions of Fund a from 0.01 Mt in 2015 to 0.07 Mt in 2020. Two highly carbon-intensive sectors—Metals Smelting and Electricity, Gas, and Water—accounted for about 70% of its financed emissions since 2018. In terms of the carbon intensities, both WACI and CERI showed a consistently increasing trend over this period (22.05% and 74.70%, respectively). With the continued growth in financed emissions and large exposure to carbon-intensive assets, there is no clear roadmap toward decarbonizing portfolios for this category of fund firms, which demands further attention.

Fund b with financed emissions and the carbon intensities were all in a downward trend. More specifically, the sectors—Electricity, Gas and Water, and Raw Chemical Materials and Chemical Products, made a great reduction during this period, which were the main factors contributing to the decline of financed emissions. Both the WACI and CERI declined from 474.98 tonnes CO2 M$−1 to 163.38 tonnes CO2 M$−1, and 576.34 tonnes CO2 M$−1 to 224.22 tonnes CO2 M$−1, respectively. Fund b made a huge reduction of investment in major carbon-intensive sectors such as Electricity, Gas and Water (−88.40%), Metals Smelting (−78.50%) and Nonmetal products (−67.60%), and shifted extensively to electronic and telecommunications equipment ( + 8.26%) as well as electric equipment and machinery ( + 0.06%). Electronic and telecommunications equipment, as a representative of the high-tech sector, is characterized by low carbon intensity and high energy efficiency25, which plays a critical role in achieving investment portfolio decarbonization.

Fund c was clearly characterized by an upward trend in financed emissions and a downward trend in carbon intensities. While Electricity, Gas, and Water kept dominating over the period, Metals Smelting was the main factor for the increase in financed emissions, contributing to 32.93% of its financed emissions in 2020. It performed well on two carbon intensities indicators, which suggested the fund firm’s great potential for carbon reductions and carbon efficiency gains. Accordingly, the WACI declined considerably by 63.31%, and CERI decreased by 35.84%. There were great increases in shares of investment in electric equipment and machinery (7.93%) and electronic and telecommunications equipment (4.64%), while divesting from Petroleum Processing and Coking (−0.30%) and Electricity, Gas and Water (−2.33%). This shift from traditional high-emitting sectors to high-tech sectors has not only resulted in reducing financed emissions effectively, but also improved the risk exposure of their portfolios.

Data validation and limitation

Financial institutions’ ability to make comprehensive assessments of companies’ climate profiles relies on trustworthy corporate disclosures of carbon emissions. Corporate carbon emissions are a key input in climate-related metrics. The uncertainty of estimating financial institutions′ investment carbon footprints is mainly caused by the reliability of carbon emissions data for investee companies. Currently, we used an industry average approach based on input-output tables to estimate firm-level carbon emissions, which brought great uncertainty into the study. The firms in China that are mandatory to disclose carbon information account for a very small proportion, while most fall within the scope of voluntary disclosure owing to corporate social responsibility26. For example, only 211 listed companies actively disclosed their carbon footprint in 2020, accounting for 5.1% of all listed companies27.

To test the reliability of the data, we compared the estimated results with the currently disclosed data on corporate carbon emissions. This study covers 56 high carbon-emitting listed companies in China28, releasing a total of about 5.1 billion tonnes in 2021 (over 40% of China’s total carbon emissions and 75% of the total emissions in the Top 100 fund firms), with electricity, cement, and steel being the main three sectors. The gaps in electricity, cement, and iron sectors between the self-reported firms’ carbon emissions data and those calculated by the accounting methodology in this paper are 22.21%, −85.82%, and −34.21%, respectively (Fig. 5). Specifically, after excluding some exceptional values, the uncertainty ranges for electricity, cement, and iron sectors are (−69.52%, 119.49%), (−85.82%, −56.08%) and (−99.80%, 16.90%). The exceptions are mainly distributed in the electricity sector, in which the companies’ renewable energy development strategies are the main causes of uncertainty. For example, some renewable energy companies focus on hydropower generation, and their carbon emissions are much lower than those of the traditional thermal power generation sector. The industry average method ignores the heterogeneity of corporate energy transition strategies between industries. In the future, we will further divide the power industry into renewable and traditional sectors in order to improve the accuracy of the calculation.

The boxplots show the minimum, maximum, first quartile, the median, the third quartile. In each panel, the thick lines in the thick box denote the interquartile range and the median, and the thin lines outside the box denote the maximum and minimum values. The point outside the box represents specific values of carbon emissions of high carbon-emitting listed companies in each sector. Carbon emissions based on estimated and self-reported data in a Electricity sector, b Cement sector, c Iron sector.

In this study, we only accounted for Scope 1 and Scope 2 emissions, without the consideration of Scope 3 emissions. PCAF recommended investors account for the Scope 3 emissions of the investee company when Scope 3 emissions are necessary, as only focusing on Scope 1 and Scope 2 emissions will not provide the full picture of the company’s carbon-related risks. Some researchers have undertaken to assess Scope 3 emissions for specific industries and corporates, which used the input–output analysis methodology to measure carbon emissions29,30. They found that indirect emissions are substantial and growing, especially in the industry sectors (in which Scope 3 emissions were most important) and buildings (in which Scope 3 emissions were twice as high as direct emissions). Although Scope 3 emissions are widely known to be important, they are not well understood and rarely estimated, and there is little motivation or science-based technical methods in current carbon footprint protocols.

Carbon emissions embodied in investments are allocated to the financial institutions based on the proportional share of investment in the investee. This attribution assumes that institutional investors are only responsible for part of carbon footprints, as many emissions from the up- or downstream of the value chain can’t be attributed to institutional investors alone. Therefore, the economic Input-Output life Cycle Assessment (EIO-LCA) for measuring investment carbon footprint could cause this risk of double counting. Teubler and Kühlert applied the 100/50/0 attribution rule to Scope 1, Scope 2, and Scope 3 emissions for calculating investment carbon footprint31. In this study, we used PCAF’s method including corporate Scope 1 and Scope 2 emissions based on a 100% attribution factor, and for Scope 3, a more accurate attribution rule is needed in future research but will be likely based on an analysis of the portfolio’s distribution of energy producers and consumers.

Discussion

Institutional investors face a moment of truth about their commitment to environmental, social, and governance (ESG) factors. Many large institutional investors have publicly committed themselves to integrate ESG factors into their investing. Yet it’s clear that many investors have struggled to convert their commitment into practice. The ESG investment in China has entered a phase of accelerated development, but the AUM of ESG assets still lag behind those in other major markets worldwide, with less than one-sixth of the European market and one-tenth of the US market, respectively32,33. Institutional investors’ ESG investments rely on accurate environmental information disclosure, however, the absence of a standardized framework has hindered institutional investors from socially responsible investing.

This study accounted for the financed emissions and carbon intensities of Chinese fund firms, explored the drivers of financed emissions, and identified potential carbon-related risks from a dynamic perspective. We found that Chinese fund firms, as the largest institutional market participants, had maintained a continuously increase trend of total financed emissions from 2015 and reached 159 Mt in 2020. In addition, the Top 10 fund firms were the main contributors, responsible for about 70% of total financed emissions. Considering the entire portfolio universe, we found that Chinese fund firms held large shares of carbon-intensive assets with high exposure to carbon-related risks. Therefore, the focus should be put on the leading fund firms, who need to follow the lead of their international counterparts in setting specific phased carbon neutrality targets to decarbonize their portfolios as soon as possible. We further found that while exposures to carbon-related risks had remained on a declining trend, portfolios still remained dominated by carbon-intensive assets. In general, Chinese fund firms have been accelerating the launch of ESG-themed products in recent years, with investment portfolios shifting from traditional carbon-intensive assets to green and low-carbon ones. Regulated by the “carbon peak and carbon neutrality” target, the green transition will bring about tremendous investment opportunities as well as social and environmental benefits. Fund firms can increase socially responsible investments within their portfolio by reconsidering carbon-intensive sectors, which are exposed to material carbon-related risks. Additionally, fund firms can focus on growing sectors like renewable energy or companies bringing an innovative approach to traditional industries. Fund firms also can set ESG scores for investees based on a well-estimated accounting system, and then allocate more capital to companies with high ESG scores.

This paper further explored the heterogeneity of trends in carbon indicators of fund firms, with a view to improving their investment portfolios to achieve long-term decarbonization goals. Firstly, fund firms that have shown a consistent increase in both financed emissions and carbon intensities are likely to face greater carbon-related risks and pressure to reduce emissions in the future, due to their large holdings of carbon-intensive sectors. Therefore, these firms should pull out of an ever-wider range of carbon-intensive assets and tilt their portfolios towards the companies flagged as environmentally friendly. Secondly, fund firms with both declining financed emissions and carbon intensities indicate a trend toward decarbonization of their portfolios. Such firms should therefore play a leading role in decarbonizing their portfolios, and take on the social responsibility to run their own businesses in a sustainable manner that further increases the rigor and transparency of carbon disclosure. Besides, they should set green transition routes, such as divesting from fossil fuels. Finally, funds characterized by rising financed emissions but declining carbon intensities indicate their investments are still dominated by carbon-intensive assets, while the future trend will be satisfactory. They need to reduce carbon-related risk exposures on the one hand, and achieve incremental decarbonization by setting up their portfolios to adjust to lower carbon-intensive assets on the other hand.

Methods

Scope boundary and corporate carbon emissions

The Greenhouse Gas Accounting System (GHG Protocol) provides the standard for measuring direct and indirect carbon emissions, which are further catergorized by three scopes—Scope 1, Scope 2, and Scope 3. Scope 1 is direct carbon emissions that occur from production activities by the company34. Scope 2 is indirect carbon emissions from the generation of purchased or acquired electricity. Scope 3 is all other indirect carbon emissions that occur in the value chain of the company. The GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard categorizes Scope 3 emissions into 15 categories, and investment portfolios are precisely under Scope 3 Category 15 (investments).

In this study, we only focus on investees’ Scope 1 and Scope 2 emissions, due to the data unavailability and uncertainty of Scope 3 emissions. We use average-data method to evaluate Chinese corporate carbon emissions, shown in Eq. (1). The method uses revenue data combined with environmentally-extended input-output (EEIO) data to estimate the Scope 1 and Scope 2 emissions, which is specifical for firm-level CO2 emissions unavailable10. The formula is as follows:

Where Eit is Scope 1 and Scope 2 carbon emissions of company i in year t. Rit is total revenue of a company i in year t. Cjt indicates the sector j’s carbon emissions in year t. Ojt represents total output of sector j in year t.

Investment Carbon Metrics

Scientifically sound evaluation methods for calculating carbon footprint of investment have been sufficiently developed and standardized. Initial methods for assessing the climate impact of investments were developed and tested in open network initiatives, such as the PCAF, which was an industry-led initiative to enable financial institutions to consistently measure and disclose the GHG emissions financed by their loans and investments35,36. TCFD made some progress on the basis of PCAF, and provided guidance on calculating GHG for certain financial products, such as private equity investment funds, green bonds and so on. Nearly 4000 organizations around the world have declared the support for the TCFD and over 615 institutional investors with more than $60 trillion in assets under management took on TCFD’s guidance to disclose their climate-related information37. In this study, we applied the TCFD framework to account for financed emissions and related carbon intensity indicators of equity portfolios; the equations can be expressed as (2) to (4).

The financed emissions are calculated by multiplying share of investment by carbon emissions of investees. Where Ft is the financed emissions of the portfolio in year t. Iit is the market value of the invested company i in year t. Mt indicates the total market value held by the investor in year t. The metric can clearly show the financed emissions and changing trends intuitively, but can’t be used to compare with other portfolios.

Where WACIt refers to the metric Weighted Average Carbon Intensity of portfolios in year t, expressed in tonnes CO2 (M$ sales)−1. By normalizing financed emissions, it can compare portfolios of different sizes, in addition to simple calculation and easy understanding.

Where CERIt refers to Carbon Emissions to Revenue Intensity and can be used to measure the productivity of the investees, expressed in tonnes CO2 (M$ revenue)−1. It is used for comparison between portfolios of different sizes. The disadvantages of this equation are relatively complex and difficult to understand.

Data collection and processing

There were 155 public fund firms released by China Securities Regulatory Commission38. Fund firms whose equity portfolios did not figure in the S&P Capital IQ Pro database, were excluded. Then the sample data was 105 fund firms over the period from 2010 to 2020, as China has supported a series of incentives to encourage and back green financial development39. In addition, the majority of the invested objects are Chinese-listed companies, so the study only focuses on the invested companies that are headquartered in China.

The economic output data are sourced from the Global Trade Analysis Project database (GTAP), which is updated at a four-year interval and is available in 2011 (GTAP9), 2014 (GTAP10), and 2017 (GTAP11). The Scope 1 emissions are from the CEADs database, which covers 42 sectors and provides a full picture of historical country-level emissions by energy types. Scope 2 emissions are based on the GTAP-E database, which contains detailed energy consumption from the electricity sector. To fill the data gap in intervening years, we used data from the neighboring year to replace it. For example, data from 2011 is also used for the years 2010, 2012, and 2013. All equity portfolios and related financial data are collected from the S&P Capital IQ Pro database (The equity portfolio of financial institutions refers to the shareholdings of listed companies, and the data is updated quarterly.). The S&P Capital IQ database also provides detailed financial information on listed companies, including the total revenue, market value, Standard Industrial Classification codes (SIC codes), and headquarters location.

To maintain the sectoral consistency of GTAP and IEA databases, we aggregated into 28 sectors and divided them into carbon-intensive and non-carbon-intensive sectors (shown in Supplementary Table 1). Each invested firm was assigned a SIC four-digit code to determine which sector it belonged to. For the regional scale, we distinguished the headquarters of invested companies based on their country-level distribution.

Data availability

All the data are available at https://github.com/lareina678/Carbon-footprints-of-Chinese-fund-firms-equity-portf.git.

References

Luderer, G. et al. Residual fossil CO2 emissions in 1.5–2 °C pathways. Nat. Clim. Change 8, 626–633 (2018).

Peters, G. P. et al. Key indicators to track current progress and future ambition of the Paris Agreement. Nat. Clim. Change 7, 118–122 (2017).

Zhao, X., Liu, C. & Yang, M. The effects of environmental regulation on China’s total factor productivity: an empirical study of carbon-intensive industries. J. Clean. Prod. 179, 325–334 (2018).

Babcock, A., He, A. & Ramani, V. Building investor trust in net zero. J. Appl. Corp. Finance 34, 52–59 (2022).

Bolton, P., Kacperczyk, M. & Samama, F. Net-zero carbon portfolio alignment. Financial Anal. J. 78, 19–33 (2022).

Shan, Y. et al. China’s CO2 emission accounts 1997–2015. Sci. Data 5, 1–14 (2018).

Shao, L. et al. Carbon emission imbalances and the structural paths of Chinese regions. Appl. Energy 215, 396–404 (2018).

Anquetin, T., Coqueret, G., Tavin, B. & Welgryn, L. Scopes of carbon emissions and their impact on green portfolios. Econ. Model. 115, 105951 (2022).

Task Force on Climate-related Financial Disclosures. Implementing the recommendations of the task force on climate-related financial disclosure. (2017).

Partnership for Carbon Accounting Financials. The Global GHG Accounting and Reporting Standard for the Financial Industry https://carbonaccountingfinancials.com/standard#the-global-ghg-accounting-and-reporting-standard-for-the-financial-industry. (2020).

Zhang, N., Zhang, Y. & Zong, Z. Fund ESG performance and downside risk: evidence from China. Int. Rev. Financial Anal. 86, 102526 (2023).

Tang, W.-Q., Meng, B. & Wu, L.-B. The impact of regulatory and financial discrimination on China’s low-carbon development: considering firm heterogeneity. Adv. Clim. Change Res. 11, 72–84 (2020).

Meng, F., Su, B., Thomson, E., Zhou, D. & Zhou, P. Measuring China’s regional energy and carbon emission efficiency with DEA models: a survey. Appl. Energy 183, 1–21 (2016).

Ji, X., Zhang, Y., Mirza, N., Umar, M. & Rizvi, S. K. A. The impact of carbon neutrality on the investment performance: evidence from the equity mutual funds in BRICS. J. Environ. Manage. 297, 113228 (2021).

Gentzoglanis, A. Corporate social responsibility and financial networks as a surrogate for regulation. J. Sustain. Finance Invest. 9, 214–225 (2019).

Chen, X., Weber, O., Song, X. & Li, L. Do greener funds perform better? An analysis of open-end equity funds in China. J. Sustain. Finance Invest. 13, 387–405 (2023).

Wang, G., Li, S. & Yang, L. Research on the pathway of green financial system to implement the realization of China’s carbon neutrality target. Int. J. Environ. Res. Public Health 19, 2451 (2022).

Cheng, C., Ren, X., Dong, K., Dong, X. & Wang, Z. How does technological innovation mitigate CO2 emissions in OECD countries? Heterogeneous analysis using panel quantile regression. J. Environ. Manage. 280, 111818 (2021).

Ren, X., Cheng, C., Wang, Z. & Yan, C. Spillover and dynamic effects of energy transition and economic growth on carbon dioxide emissions for the European Union: a dynamic spatial panel model. Sustain. Dev. 29, 228–242 (2021).

Downar, B., Ernstberger, J., Reichelstein, S., Schwenen, S. & Zaklan, A. The impact of carbon disclosure mandates on emissions and financial operating performance. Rev. Account. Stud. 26, 1137–1175 (2021).

Kuo, L., Yu, H.-C. & Chang, B.-G. The signals of green governance on mitigation of climate change–evidence from Chinese firms. Int. J. Clim. Change Strateg. Manag. 26, 1137–1175 (2015).

Grauel, J. & Gotthardt, D. The relevance of national contexts for carbon disclosure decisions of stock-listed companies: a multilevel analysis. J. Clean. Prod. 133, 1204–1217 (2016).

Zhang, Z., Li, J. & Guan, D. Value chain carbon footprints of Chinese listed companies. Nat. Commun. 14, 2794 (2023).

Mésonnier, J.-S. & Nguyen, B. Showing off cleaner hands: mandatory climate-related disclosure by financial institutions and the financing of fossil energy. Available at SSRN https://doi.org/10.2139/ssrn.3733781 (2020).

Zheng, J. et al. The slowdown in China’s carbon emissions growth in the new phase of economic development. One Earth 1, 240–253 (2019).

Li, H. et al. The motivations of Chinese firms in response to the Carbon Disclosure Project. Environ. Sci. Pollut. Res. 26, 27792–27807 (2019).

SynTao Green Finance. Analysis Report on Climate-related Disclosures of A-share Listed Companies. (2021).

Carbon Rating Report of China’s Listed Companies https://www.eco.gov.cn/news_info/54114.html (2021).

Wei, P., Li, Y. & Zhang, Y. Corporate green bonds and carbon performance: An economic input–output life cycle assessment model‐based analysis. Bus. Strategy Environ.; https://doi.org/10.1002/bse.3267 (2022).

Hertwich, E. G. & Wood, R. The growing importance of scope 3 greenhouse gas emissions from industry. Environ. Res. Lett. 13, 104013 (2018).

Teubler, J. & Kühlert, M. Financial carbon footprint: calculating banks’ scope 3 emissions of assets and loans. European Council for an Energy Efficient Economy. https://nbn-resolving.org/urn:nbn:de:bsz:wup4-opus-75872 (2020).

Investment Company Institute. A Review of Trends and Activities in the Investment Company Industry (2021).

European Securities and Markets Authority. Performance and Costs of EU Retail Investment Products (2022).

Bhatia, P. et al. Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011).

Linthorst, G. & Schenke, M. Platform Carbon Accounting Financials (PCAF) report 2018., (2018).

Linthorst, G. & Schenke, M. Platform Carbon Accounting Financials (PCAF) report 2019., (2019).

Task Force on Climate-related Financial Disclosures. Task Force on Climate-related Financial Disclosures Overview (2022).

China Securities Regulatory Commission. List of Public Fund Management Firms (in Chinese) http://www.csrc.gov.cn/csrc/c101900/c1029657/content.shtml (2022).

Jin, J. & Han, L. Assessment of Chinese green funds: Performance and industry allocation. J. Clean. Prod. 171, 1084–1093 (2018).

Acknowledgements

We acknowledge supports from National Natural Science Foundation of China (7221101088).

Author information

Authors and Affiliations

Contributions

X.Y, and J.L.W. conceived the original idea and designed the research. J.L.W. wrote the relevant processing codes and drafted the initial manuscript. D.B.G. was responsible for writing methods and collecting the raw data. Z.K.Z. and J.L.W. analyzed the results and created the figures. Z.K.Z. and D.B.C. commented on the discussion. All the authors contributed to writing the manuscript and discussed the results at all stages.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Communications Earth & Environment thanks Yuning Gao and the other, anonymous, reviewer(s) for their contribution to the peer review of this work. Primary Handling Editors: Pallav Purohit and Clare Davis. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Wang, J., Guan, D., Zhang, Z. et al. Carbon footprints of the equity portfolios of Chinese fund firms. Commun Earth Environ 4, 296 (2023). https://doi.org/10.1038/s43247-023-00926-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s43247-023-00926-y

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.