Abstract

Electric vehicle batteries contain many internationally sourced critical minerals. Seeking a stable mineral supply, the US Inflation Reduction Act sets a market-value-based target for battery critical mineral content. In 2027, for an electric vehicle to be tax-credit eligible, 80% of the market value of critical minerals in its battery must be sourced domestically or from US free-trade partners. We determined that the target may be achievable for fully electric vehicles with nickel cobalt aluminium cathode batteries, but achieving the target with lithium iron phosphate and nickel cobalt manganese batteries would be challenging. We also note that a mass-based target could avoid some of the challenges posed by a market-value target, such as volatile market prices. We further conclude that the approach the Act has taken ignores the environmental effects of mining, non-critical minerals supply, support for recycling and definitions that avoid gamesmanship.

Similar content being viewed by others

Main

Electric vehicles (EVs) are central to plans to mitigate greenhouse gas (GHG) emissions from the transportation sector. In August 2022, President Biden signed the Inflation Reduction Act (IRA), which provides tax credits for eligible EVs and aims to spur their adoption. One criterion for an EV to be eligible for a tax credit is that after 31 December 2026, 80% of the market value of the critical minerals in its battery be ‘extracted or processed in the United States’ or any of the 20 free-trade countries (FTCs) with whom the United States holds a free-trade agreement. Minerals recovered from recycling in North America also count towards the 80% target. This 80% target, meant to enhance the security of mineral supply, and therefore energy security for vehicle electrification, is challenging because relevant minerals such as cobalt and manganese are overwhelmingly extracted outside US borders.

Furthermore, the IRA’s market-value-based target does not address several key issues that would increase the sustainability of EV batteries1,2 and enhance the security of mineral supply. First, the infrastructure and technology for EV battery recycling will not be ready by 2027 to return critical minerals from spent batteries to the supply chain in time to help meet this target, which will leave battery makers to lean on virgin mineral supplies3. Moreover, the market value of recycled minerals may be less than that of virgin minerals4, disincentivizing use of recycled minerals even when they become available because manufacturers will more easily meet the IRA targets with expensive virgin minerals. Policies and incentives that follow the IRA should accelerate and expand existing efforts to establish a domestic battery recycling network and support ongoing development of battery recycling technology. Second, there is no explicit provision to evaluate the environmental effects of different mineral sources, including recovering minerals from geothermal brines5, from coal6 or other unconventional sources, from the ocean7,8, from spent electronics9 and from virgin mineral mining, which poses a significant environmental quality threat10,11,12. The effects on overall air, water and soil quality—along with GHG emissions—of minerals acquisition will be essential to predict and monitor to avoid burden shifting as the United States aims to decarbonize light-duty vehicles.

Nonetheless, it is important to evaluate the feasibility of the IRA’s target as it stands for multiple lithium-ion battery chemistries used in fully electric battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). We evaluate the target for three BEV battery chemistries: nickel manganese cobalt (NMC) (current majority in the market), nickel cobalt aluminium (NCA) (currently used by Tesla) and lithium iron phosphate (LFP) (Tesla S3 and Ford F150 will use this chemistry)13. In our analysis, we average the compositions of four NMC batteries: NMC111, NMC532, NMC622 and NMC811. We consider only the critical minerals in the IRA’s Section 45c(6): aluminium, cobalt, graphite (natural and synthetic), lithium, manganese and nickel. We summarize the mass and market-value contributions by mineral for BEV (Supplementary Tables 2G and 11D, respectively) and PHEV battery chemistries (Supplementary Tables 3G and 12D, respectively). In BEV NMC batteries, the dominant market-value contributor was cobalt (48%) (Supplementary Table 11F). Aluminium contributed over 60% to the market value of critical minerals in LFP batteries. Nickel was the majority contributor (49%) to the market value of NCA BEV batteries.

We considered two scenarios for provision of these minerals. First, in the ‘maximum availability’ scenario, we assume the United States imports all available supply of each mineral from FTCs14. This scenario is unlikely because FTCs do not trade exclusively with the United States. In the second scenario (‘baseline imports’), we reduced the amount of minerals from FTCs to match historical import levels. Both scenarios account for US production and for the use of critical minerals in other industries (Supplementary Table 4A–F). Minerals obtained from recycling in North America are also allowable under the IRA. Accordingly, we included secondary production of nickel and aluminium from scrap and waste materials from other industries (Supplementary Table 7A,B,M,N). Neither mineral-availability scenario includes minerals stemming from EV lithium-ion battery recycling because it is not yet at an industrial scale in the United States. Supplementary Table 0A lists additional assumptions adopted in creating the scenarios.

Critically, the IRA specifies minerals must be extracted or processed in the United States or an FTC. Therefore, minerals could be imported from a non-FTC country to the United States or an FTC and processed in a way that would meet IRA requirements. This introduces the possibility of gamesmanship that could reduce mineral and energy security and worsen the environmental effects of producing EV batteries. For example, the United States imported 2,618 t of lithium mineral (between lithium hydroxide and lithium carbonate imports) in 201915. Of that, 59% came from Argentina, a non-FTC country that does not offer the labour and environmental protections the United States requires of FTC partners. If the United States processed this imported Argentinian lithium and used it in batteries, the cars that contain these batteries would be tax-credit eligible. Our analysis did not account for this scenario because it does not reduce the mineral security and environmental quality risks associated with international supply chains. To achieve the aims of the IRA, guidance should be provided regarding what constitutes processing and what allowable sources are for the minerals that would be processed in the United States or an FTC.

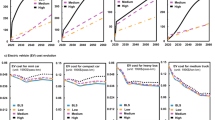

Figure 1a displays the number of BEV batteries that meet the 80% IRA target assuming only a single chemistry is used for all batteries16. Nearly universally, not enough batteries meet this criterion to satisfy projected BEV demand. The one exception is when critical minerals in NCA batteries are at their low market value and mineral availability is high. Meeting the IRA targets for BEVs is therefore extraordinarily challenging.

a, Market-value basis. b, Mass basis14,16. At least 80% of the market value of the critical minerals in the number of batteries the blue bars depict derives from the United States and FTCs. Maximum-availability scenarios assume the United States purchases all exported minerals from FTCs. Baseline-imports scenarios assume import levels will follow historical patterns. Results (blue bars, mean mineral market value ± s.d.) are the number of tax-credit-eligible batteries available as calculated with the mean mineral market value over five years (n = 5). Error bars reflect the minimum and maximum number of tax-credit-eligible batteries when calculated with mineral market values equal to one standard deviation above and below the mean mineral market value. The centre of the error bar corresponds to the result calculated when the mean mineral market values are used.

We also assessed the viability of the market-based target for smaller PHEV batteries (Supplementary Fig. 1a) with LFP, NMC and lithium manganese oxide (LMO) chemistries. LFP batteries would meet demand under both mineral-availability scenarios. It would be just possible to meet demand for NMC batteries when supply is at baseline mineral levels. In the baseline imports scenario, enough LMO batteries may not be available. In general, the 80% market-value target is viable for PHEVs, even under baseline mineral availability (Supplementary Fig. 1).

The IRA’s choice of a market-value-based target limited to certain critical minerals raises four challenges. First, a market-based target may be met before all the critical minerals in a battery are acquired from a secure source (for example, the United States and FTC countries), depending on the battery chemistry. Second, the environmental effects of critical minerals acquisition are physically tied to the amount of mineral produced rather than its market value. (Although a high market value does, of course, drive mineral production.) Third, market values fluctuate. For example, the prices of cobalt and nickel have increased by about US$13,000 and US$4,000 per metric ton, respectively, since 201914. In interpreting the IRA policy, guidance on what market values to use and from which sources would help reduce uncertainty and gamesmanship and hold all automakers to the same standard in the interpretation of market value. Finally, non-critical minerals central to batteries, such as iron for LFP batteries, are produced mainly (98%14) outside the United States, raising supply risks. Even though they may be Earth-abundant, the extraction of these minerals—largely in non-FTC countries (61% for iron14)—may degrade environmental quality.

Using a mass-based target could avoid these four challenges. Accordingly, we also evaluated achieving the IRA’s target if the 80% were based on mass rather than market value (Fig. 1b). Graphite, aluminium and nickel had the largest mass shares in batteries (Supplementary Table 2H). Overall, it was not possible to meet an 80% mass-share threshold for IRA-eligible minerals. Compared with Fig. 1a, LFP and NCA battery availability shrank. NMC battery availability rose because the limiting ingredient on a mass basis is graphite, rather than cobalt as in the market-value target case, and supplies of graphite are larger than cobalt supplies. For PHEVs, the number of batteries achieving a mass-based target also falls for LFP and LMO chemistries compared with market-value-based results. Again, NMC battery availability grows. High-level conclusions about eligible battery production are similar whether a mass- or market-based target is used although absolute numbers of eligible batteries vary. Given the fluctuations in mineral market values, using a mass-based target in the policy could improve its transparency but may not incentivize production of high-value minerals domestically, which is important for mineral security.

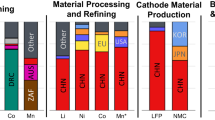

In Fig. 2, we illustrate—in the context of the IRA—which minerals are at the core of the availability challenge for different battery chemistries. Mineral by mineral, we calculated how many batteries could be made for each of the three chemistries on the basis of IRA-eligible mineral supply. This analysis does not account for a battery-level market value or mass target for critical minerals. It indicates that IRA-eligible nickel and aluminium supplies are plentiful. Notably, however, there is not enough cobalt or graphite to meet demand under either availability scenario. Manganese supply is also constrained. In the case of PHEVs, only cobalt and lithium exhibit insufficient supply (Supplementary Fig. 2); supplies of other IRA-eligible minerals would support production of enough batteries to meet demand. For BEVs, lithium supply is sufficient under the maximum-availability scenario, but supply falls short at typical import levels. Today, the United States does not import any lithium from Australia, a dominant lithium producer and an FTC country, because Australian lithium destined for battery materials is exported to China (94% of market value in 202217). As supply chains shift to reflect a changing policy landscape, the United States could increase its share of eligible minerals, including lithium, by increasing imports from FTC countries such as Australia.

Blue, yellow and rust-coloured bars represent batteries with NMC, NCA and LFP chemistries, respectively14,16. Bars falling in grey-, yellow- and green-shaded areas indicate insufficient, constrained and sufficient mineral supply, respectively. The International Energy Agency estimates a range in battery demand that introduces uncertainty into mineral requirements; this is reflected by the height of the yellow-shaded area.

The barriers facing the critical minerals target in the IRA bring to mind the inability of the young cellulosic biofuels industry to meet the 16-billion-gallon annual production target set for it in the 2007 Renewable Fuel Standard (RFS) for 202218. In 2021, the US Environmental Protection Agency set a 2022 Renewable Volume Obligation of 630 million gallons of this fuel19, a far cry from the original aspirations of the RFS. If, as with the RFS targets for cellulosic biofuels, IRA critical mineral targets fail, will US consumers be slower to adopt EVs because there will be fewer that are tax-credit eligible? How will this lack of adoption impact GHG reduction targets? While domestic mining increases are probably essential to meet IRA targets, establishing and expanding mining activity is subject to lengthy and important permitting and environmental protection activities. To increase the likelihood of success in reducing transportation GHGs and the overall sustainability of electrified transportation, battery recycling20 is an unqualified necessity, albeit one that may be slow to rise to the challenge without an infusion of greater support.

Methods

The quantities of critical minerals (as defined in IRA Section 45c(6): aluminium, cobalt, graphite (natural and synthetic), lithium, manganese and nickel) in BEV and PHEV batteries are from the Greenhouse Gases, Regulated Emissions and Energy Efficiency in Technologies (GREET) model2. Mass and market-value shares for BEVs and PHEVs are in Supplementary Tables 2H, 3G, 11D and 12D.

The International Energy Agency projects that between 990,000 and 1,900,000 BEVs and between 500,000 and 1,100,000 PHEVs will be sold in 2025. We therefore adopted a range of BEV sales of 1–2 million new BEVs and 0.5–1.5 million new PHEVs in 2027 for the United States.

Annual production and import data of the six selected critical minerals were obtained from the US Geological Survey (USGS) Mineral Commodity Summaries and Yearbooks. We assumed constant production and imports between 2021 and 2027. We accounted for use of critical minerals in multiple industries. Only a fraction of minerals produced and imported are used in battery production. We estimated these fractions on the basis of data from the USGS as documented in Supplementary Table 5A. The resulting mineral availabilities represent upper bounds; we erred on the side of assuming maximum amounts of minerals would be available for battery production. For example, if USGS documentation indicated mineral consumption was divided among several industries that included battery production, we assumed that entire fraction went to battery production. Our analysis included recycled and scrap minerals. We assumed that all aluminium scrap had an aluminium content of 90% (Supplementary Table 4A) and that all nickel scrap (Supplementary Table 4F) had a nickel content of 100%. We note that critical minerals are produced as multiple types of compounds. For example, lithium may be on the market as lithium carbonate, lithium hydroxide, lithium chloride or spodumene. Nickel can be found in ferronickel, sulfide and laterite ores. We calculated mineral availability using stoichiometry or estimates of a typical amount of mineral in different types of ore (Supplementary Table 4A–F). For each battery chemistry, we identified the limiting critical mineral ingredient on the basis of market value for which IRA-allowable critical mineral supply would first be depleted. The limiting mineral was graphite for LFP batteries. It was cobalt for NMC and NCA batteries. We then determined the minimum market-value share of that limiting mineral that was required to produce batteries that meet the IRA 80% critical mineral market-value target. After determining the mass share of the mineral that corresponded to the minimum market-value share, for each mineral-availability scenario, we estimated the number of tax-credit-eligible batteries that could be produced when the market value of each mineral was at its average, minimum and maximum values. We note that individual battery manufacturers use different battery ‘recipes’ that influence the amount of minerals used per battery and, accordingly, the number of batteries that would be tax-credit eligible. Given that this information is proprietary, we used GREET values for amounts of minerals per battery. We set the range of market values on the basis of the standard deviation of a five-year span of mineral market values. A similar approach to calculating the population of tax-credit-eligible batteries was taken to evaluate an 80% target based on mass share. Market values are five-year averages14. Ranges reflect the standard deviation in market values for each mineral over the past five years (Supplementary Table 8I).

Reporting summary

Further information on research design is available in the Nature Portfolio Reporting Summary linked to this article.

Data availability

All calculations, data and data sources are provided in the Supplementary Information.

References

Chordia, M., Nordelöf, A. & Ellingsen, L. A.-W. Environmental life cycle implications of upscaling lithium-ion battery production. Int. J. Life Cycle Assess. 26, 2024–2039 (2021).

Dunn, J. B., Gaines, L., Kelly, J. C., James, C. & Gallagher, K. G. The significance of Li-ion batteries in electric vehicle life-cycle energy and emissions and recycling’s role in its reduction. Energy Environ. Sci. 8, 158–168 (2015).

Dunn, J., Kendall, A. & Slattery, M. Electric vehicle lithium-ion battery recycled content standards for the US—targets, costs, and environmental impacts. Resour. Conserv. Recycl. 185, 106488 (2022).

Söderholm, P. & Ekvall, T. Metal markets and recycling policies: impacts and challenges. Miner. Econ. 33, 257–272 (2020).

Stringfellow, W. T. & Dobson, P. F. Technology for the recovery of lithium from geothermal brines. Energies 14, 6805 (2021).

Franus, W., Wiatros-Motyka, M. M. & Wdowin, M. Coal fly ash as a resource for rare earth elements. Environ. Sci. Pollut. Res. 22, 9464–9474 (2015).

Leal Filho, W. et al. Deep seabed mining: a note on some potentials and risks to the sustainable mineral extraction from the oceans. J. Mar. Sci. Eng. 9, 521 (2021).

Diallo, M. S., Kotte, M. R. & Cho, M. Mining critical metals and elements from seawater: opportunities and challenges. Environ. Sci. Technol. 49, 9390–9399 (2015).

Sovacool, B. K. The hidden costs of batteries. Science 377, 478–478 (2022).

Meißner, S. The impact of metal mining on global water stress and regional carrying capacities—a GIS-based water impact assessment. Resources 10, 120 (2021).

Ranjan, R. Assessing the impact of mining on deforestation in India. Resour. Policy 60, 23–35 (2019).

Alam, M. A. & Sepúlveda, R. Environmental degradation through mining for energy resources: the case of the shrinking Laguna Santa Rosa wetland in the Atacama Region of Chile. Energy Geosci. 3, 182–190 (2022).

The Greenhouse Gases, Regulated Emissions, and Energy Use in Technologies (GREET) Model (Argonne National Laboratory, 2021).

Mineral Commodity Summaries 2022. (USGS, 2022); https://doi.org/10.3133/mcs2022

Lithium—Mineral Yearbook 2019 (USGS, 2021).

Global EV Data Explorer (IEA, 2022).

Insights into Australian Exports of Lithium. (Austalian Bureau of Statistics, 2022); https://www.abs.gov.au/articles/insights-australian-exports-lithium

Zhong, J. & Khanna, M. Assessing the efficiency implications of renewable fuel policy design in the United States. J. Agric. Appl. Econ. Assoc. 1, 222–235 (2022).

Final Volume Standards for 2020, 2021, and 2022 (US EPA, 2022); https://www.epa.gov/renewable-fuel-standard-program/final-volume-standards-2020-2021-and-2022

Bauer, C. et al. Charging sustainable batteries. Nat. Sustain. 5, 176–178 (2022).

Acknowledgements

J.B.D. acknowledges support from the National Science Foundation Future Manufacturing Program (NSF CMMI-2037026). J.N.T acknowledges support from the Ryan Fellowship at Northwestern University.

Author information

Authors and Affiliations

Contributions

J.B.D. contributed conceptualization, writing and editing, and supervision. J.N.T. contributed analysis, visualization, writing and editing.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Sustainability thanks Zhi Cao and the other, anonymous, reviewer(s) for their contribution to the peer review of this work.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Supplementary Information

Supplementary Figs. 1–3 and sample calculations.

Supplementary Data 1

Supplementary Tables 0–13, containing all data and calculations used to generate results presented in the manuscript.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Trost, J.N., Dunn, J.B. Assessing the feasibility of the Inflation Reduction Act’s EV critical mineral targets. Nat Sustain 6, 639–643 (2023). https://doi.org/10.1038/s41893-023-01079-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41893-023-01079-8

This article is cited by

-

Reducing supply risk of critical materials for clean energy via foreign direct investment

Nature Sustainability (2024)

-

Electric vehicle battery chemistry affects supply chain disruption vulnerabilities

Nature Communications (2024)