Abstract

This study investigates the role of financial frictions on firm value within the framework of earnings management, including the impact of productivity growth. In contrast to prior studies, the present study employed an autoregressive model to examine the temporal dynamics of the variables to determine their short-term and long-term connection patterns. The results of the study indicate a negative association between financial frictions and firm value. Accrual earnings management, a practice employed by organizations to enhance their profit margins, serves as a mediator between financial frictions and firm value. This mediation of earnings management alleviates the adverse impact of financial frictions. The enhancement of productivity growth amplifies the conditional, indirect influence of earnings management. Moreover, this study reveals that financial frictions have a significant influence in the short-term, leading to overestimation of factor loadings. However, this impact stabilizes over time in the long run. Financial market frictions have the most prominent impact on firm value compared to the other two forms of frictions, namely, macroeconomic frictions and microeconomic frictions. Larger firms are more inclined to attain higher firm value than smaller enterprises. Managers can enhance firm value by exerting control over the influence of financial frictions in the economy through earnings management. The effectiveness of this strategy is contingent upon the level of productivity growth.

Similar content being viewed by others

Introduction

The significance of financial frictions at both the macro and micro levels have been extensively discussed in previous scholarly works. Financial frictions possess a multilevel and multidimensional nature, exerting a latent influence on both firms and economies across various levels. Financial frictions manifest as a result of the expenses incurred in financial transactions (Cooley and Quadrini, 2001). Regardless of the nature of the economic transaction, it will inevitably involve costs and expenses. There are several manifestations of financial frictions. For instance, Akinci (2021) conceptualizes financial frictions as expenses associated with monitoring. Cesa-Bianchi and Rebucci (2017) identified the imposition of taxes on borrowing and the manipulation of monetary policy interest rates as factors contributing to financial frictions within the macroeconomic framework. Huntington (2005) also noted that worldwide oil prices can be attributed to macroeconomic frictions inside the nation. In short, macroeconomic frictions (MAF) arise from government policies related to prudential and monetary measures, as well as from factors such as interest rates, corporation taxes, and other tariffs imposed by the government. Microeconomic frictions (MIF) refer to the financial limits that organizations encounter in their business-to-business interactions. For instance, Pineda and Blyde (2011) identified trade costs inside trade channels as a micro level obstruction. Asker et al. (2014) and Catherine et al. (2022) identified collateral limits for obtaining short-term borrowing and other trade expenses as MIF. Financial market frictions (FMF) refer to the factors that constrain or deter the smooth execution of trade transactions (DeGennaro and Robotti, 2007). According to Adler (2014), frictions are perceived as constraints, impediments, or limitations that impede the optimal functioning of markets and economies. Financial experts study market frictions due to their potential to expose traders to undesirable or unmanageable levels of risk. According to Olbrys and Majewska (2014), financial frictions may be conceptualized as a range of dysfunctions within the processes of purchasing and selling. For example, the presence of frictions in financial markets leads to discontinuity in the flow of time. From an asymmetric information standpoint, Stiglitz and Weiss (1981) argued that investors hold private knowledge of their projects, where the expected rewards may be equal but the likelihood of success varies. These frictions are present at the macroeconomic level because of monetary, fiscal, and prudential policies (Akinci and Olmstead-Rumsey, 2018; Gomes, Jermann, and Schmid, 2016). The presence of frictions at the micro or business level can be attributed to various factors, such as liquidity requirements, bank securities, collaterals, and tight credit supply (Peia and Romelli, 2022). At the financial market level, these frictions arise due to information asymmetries, market inefficiencies, flotation or brokerage firms costs, and obstacles in the smooth functioning of capital markets, which hinder their efficiency and liquidity (Quadrini, 2011). Furthermore, financial frictions also exist at the firm level and encompass issues related to agency problems, capital adjustment, labor, and operational costs (Khan and Thomas, 2013). Several scholarly investigations (Kim, 2022; Wang et al., 2021) have examined the influence of financial frictions on different economic fundamentals. However, these studies primarily focus on macroeconomic indicators, neglecting the effects of financial frictions on micro- or firm-level fundamentals. Previous studies have not yet addressed the combined impact of macro, micro, and financial market-level frictions on firm value, despite the direct linkages between these frictions and firm value. Hence, the objective of this study is to examine the influence of MAF, MIF and FMF on the valuation of non-financial firms operating in emerging Asian economies.

In previous studies, the frictionless and free market was the dominant paradigm for estimating firm value, as proposed by Modigliani and Miller (1958). This classical perspective of Modigliani-Miller (MM) theory assumes perfect capital markets without taxes or transactional costsFootnote 1. Therefore, comprehending the mechanisms by which firms gain market value within the perspective of a market characterized by different levels of frictions and imperfections, poses a significant dilemma for scholars in the field of management and motivates them to study market imperfection based on financial frictions. The present study investigated the dynamics of firm value in the presence of different levels of economic frictions with the interaction and mediation of earnings management and productivity growth. The influence of financial frictions on firm value is rooted in agency conflict (Jensen and Meckling, 1979; Panda and Leepsa, 2017). According to agency theory, it has been posited that agency conflicts primarily occur within firms, specifically between agents and principals (Moscariello et al., 2019; Panda and Leepsa, 2017; Zogning, 2017). However, it is important to note that these conflicts of interest also extend beyond the boundaries of firms, including interactions between firms, government entities, and market participantsFootnote 2. The primary objective of this study is to expand the existing assumptions of agency theory to assess the value of a firm while considering the presence of frictional costs at various levels, including the macro, micro, and financial market levels. At the macroeconomic level, government agencies and governing bodies operate as principals, while their imposed taxes, tariffs, monetary policies, and prudential regulations serve as agency costs (Grodecka and Finocchiaro, 2018). Similarly, at the micro level, suppliers, traders, financial market institutions, and the corporate sector are similar to principals in the context of agency theory. Moreover, collateral constraints, the cost of debt, flotation, and brokerage costs serve as factors that contribute to the presence of agency costs in financial markets (Zogning, 2017).

Firms face an inevitable and challenging task of overcoming these frictions and constraints to achieve optimal performance. However, they can only partially alleviate negative impacts through various strategies, such as establishing political connections (Yang et al., 2021), making adjustments to capital structure (Macnamara, 2019), maintaining cash holdings (Le, 2016), and fostering financial development (Karaman and Yıldırım-Karaman, 2019). In contrast, a mere analysis of individual factors contributing to firm performance presents a fragmented depiction of the financial well-being of organizations. Consequently, firms must devise strategies within their internal processes, such as earnings management (Yimenu and Surur, 2019) and productivity growth (Impullitti, 2022; Levine and Warusawitharana, 2021), to navigate and endure the challenges and expenses associated with these frictions. Firm value is subject to influence by the firm itself through legitimate manipulation in its earnings management (Shoaib and Siddiqui, 2022). The rationale for choosing earnings management is based on the understanding that financial frictions serve as the underlying cause of economic fluctuations and that various forms of financial frictions can exacerbate the business cycle. There may be conflicting motives for earnings management concerning the macroeconomic business cycle. One theoretical perspective that has been proposed is the concept of countercyclical earnings management (Cohen and Zarowin, 2007). During a recessionary phase, companies are more inclined to engage in earnings management as a means to avoid presenting negative results to investors and creditors or to project a sense of stability in their income generation and financial standing (Cohen and Zarowin, 2007). Another theoretical perspective posits the notion of procyclical adjustment of earnings management (Ze-To, 2012). During a period of economic expansion, corporations may engage in earnings management more frequently to circumvent the disclosure of net profits that fall below analysts’ expectations or the industry average. During periods of economic expansion, both analysts’ expectations and the average net income of other businesses tend to increase. Consequently, firms may engage in a greater degree of earnings management during boom periods than during recessionary periods, assuming that the financial statement of the firm remains unchanged. If the latter reason outweighs the former motivation, earnings management is likely to exhibit a procyclical pattern in relation to the macroeconomic business cycle phase (Ze-To, 2012). Hence, the present study examines the long-lasting issue in the literature of how earnings management, as a mediating variable, evaluates the extent to which firms, through their internal endeavors, can improve their firm value and alleviate the effect of financial frictions. The inclusion of earnings management as a mediating variable in the study is justified by its direct support in helping firms mitigate and avoid frictions in the economy (Al Hussaini, 2018). It is important to note that earnings management is a legal manipulation tool employed for this purposeFootnote 3.

In accordance with signaling theory, management endeavors to provide positive signals to investors by mitigating the impact of financial frictions through the augmentation of productivity growth. This study complements the ideas of Impullitti (2022) and Karabarbounis and Macnamara (2021), who suggest that an increase in productivity growth reduces the adverse effects of financial friction; they differentiate by including more levels of friction rather than just mentioning credit constraints (micro level frictions) and their ultimate impact on firm value in the market. Therefore, productivity growth (PG) is a strong tool and strategy for firms to mitigate the frictional effect of the economy. Productivity growth may be achieved by technology and innovation enhancement, labor growth, and investment in capital and labor resources, which eventually increase sales and profits for the business. Unlike other strategies, productivity growth is a direct and concrete element for firms to outperform in the industry.

Under different levels of friction, productivity growth can influence savings, investments, and capital inflows (Hung, 2020). This PG not only positively impacts firms’ income but also boosts household income. Similarly, during a financial crisis, firms with higher PG may better meet the requirements and pressure of adverse economies. When the cost of goods is higher and expansion is inevitable, firms with higher PG self-financing occur at the worst time.

In our study, it is evident that along with earnings management, enterprises enhances their valuation in the market. The direct and indirect effects of the PG terms in the empirical models also show that PG moderates the main model positively. Therefore, PG is a vital element of this study and has a pivotal role.

This study makes several contributions to literature. Limited academic literature exists on the relationship between financial frictions and firm value. Previous studies have focused predominantly on examining the effects of financial friction at the macroeconomic level (Midrigan and Xu, 2014; Quint and Rabanal, 2013), neglecting the widespread influence of financial friction on firm value, specifically concerning earnings management and productivity growth. Moreover, previous studies have overlooked the significance of earnings management and firm productivity in the transmission of financial frictions on corporate manufacturing firm valuation, particularly in emerging Asian economies, such as China, India, Pakistan, Bangladesh, and Sri LankaFootnote 4. The economic conditions exhibit significant variations, and the enterprises themselves display substantial heterogeneity across different sectors. The differentiations in question are both significant and multifaceted. To effectively handle the concept of distinction, the countries are individually discussed and analyzed.

To achieve optimal financial development within the economy, firms must effectively address all financial constraints and frictions. This can be accomplished only through the optimal performance of firms and the attainment of higher levels of output. Firms have to pay enormous costs to macro, micro, and financial market agents from their revenue, such as predefined and levied taxes and government tariffs, trade credits to other firms, financial costs of financial institutions, financial market flotation, brokerage agents, and other business-level costs. If they do not manage their earnings, they may face financial distress, as poor financial and earnings management practices in the firm are often responsible for market crashes and company failures (Fuentes‐Albero, 2019). These observations have served as a catalyst for researchers to delve deeper into the underlying factors contributing to this phenomenon.

In some studies, the terms “financial frictions” and “financial risks” are used interchangeably (Bai, Lu, and Tian, 2018; Chen and Columba, 2016; Grodecka and Finocchiaro, 2018). However, in this study, we distinguished between these variables, emphasizing the need for differentiation. The categorization of financial frictions and risk factors is distinct because of their inherent differences. Financial frictions comprise predetermined costs encountered by businesses. Conversely, risk factors pertain to unforeseeable shocks and calamities, which are environmentally driven and have uncertain and undetermined magnitude impacts on firm value (Schoenmaker and Van Tilburg, 2016). Moreover, in the short run both financial frictions and financial may have same effect but their long run effect is examined in this study by using partial adjustment model.

The following section will present a review of the relevant literature. The literature review will be used to construct hypotheses and theoretical frameworks in line with the study’s objectives. The subsequent section of the literature review relates to the methodology, wherein the data, sample, and related models to be employed are explicated. The results are presented after the methodology section, and ultimately, the study is concluded in the conclusion section.

Literature review and hypothesis development

The concept of financial friction was initially introduced as “international financial frictions,” which refers to the limitations that companies encounter when establishing their international operations in foreign countries (Fujita et al., 1989). Several studies have shown that the occurrence of macroeconomic shocks leads to financial frictions, specifically in the form of monetary policy. Firms with lower levels of financial leverage tend to exhibit greater responsiveness to these monetary shocks. This can be attributed to the fact that these firms have a flatter cost curve for financing investment, as Ottonello and Winberry (2020) highlight. The housing sector exhibits significant macroeconomic frictions, as evidenced by the impact of macro-prudential regulations, such as reducing loan-to-value ratios, on the volatility of housing prices (Akinci and Olmstead-Rumsey, 2018). These studies provide additional support for the current study’s assertion that including macro-level friction in the assessment of firm value for manufacturing firms in developing economies in Asia is important. This is because financial frictions affect firms’ profitability through adjustments in earnings (earnings management), which ultimately influence the firms’ market value.

At the microeconomic level, frictions arise among businesses due to the relationship between risk-weighted capital requirements, interest rates, lending, and intermediate output. Specifically, an increase in risk-weighted capital requirements leads to a corresponding increase in interest rates, resulting in a decrease in lending and intermediate output (Grodecka and Finocchiaro, 2018). A study conducted by Covas and Driscoll (2014) yielded comparable results, indicating that the implementation of a liquidity requirement by banks leads to a reduction of three percent in the equilibrium loan supply, showing that the implementation of a liquidity requirement by banks leads to a reduction of three percent in the equilibrium loan supply. Additionally, the study showed that bank holdings of safer securities experienced a corresponding increase of six percent. The housing sector exhibits significant microeconomic friction effects, as demonstrated by Chen and Columba (2016). Their findings suggest that higher macroeconomic friction due to higher interest rates can dampen economic activities and reduce consumption at a broader level. Moreover, their findings indicate that higher interest costs reduce mortgage investments, short-term household debt, and aggregate consumption. However, in the long run, the level of debt remains unchanged. Our study develops these findings to investigate the impact of different levels of friction in the short and long run in the framework of manufacturing firm valuation through the implementation of strategies such as earnings management and firm productivity growth, which aim to create differentiation.

Financial markets differ from the real world because of their inherent imperfections, which can be analyzed by examining the collective variations in securities returns and pricesFootnote 5. These imperfections can be attributed to the existence of information asymmetry, also known as informational friction, among borrowers at different levels. Financial market frictions are influenced by various constraints, such as analyst costs, flotation costs, brokerage firm costs, and other fees related to applications and processing (Quadrini, 2011). According to the research conducted by Levin et al. (2004), firms operating in financial markets encounter a significant degree of informational friction. According to Labadie (1998), the presence of capital market frictions not only amplifies overall fluctuations in securities returns but also generates cross-sectional fluctuations that are not readily observable through available data. Therefore, the presence of capital and financial market friction restricts firms and investors from engaging in frictionless market transactions. According to Khan and Thomas (2013), the presence of capital adjustment costs prevents young firms from attaining their optimal scale by transmitting financial shocks. Similarly, according to Spaliara (2011), financial frictions can transmit changes throughout a network of firms, ultimately impacting their decision-making patterns in the short and long run.

The literature suggests a clear association between financial frictions and various financial and economic aspects, such as firm performance, business cycles, expansions, household debt, and financial market efficiency. However, the relationship between financial frictions and firm value remains fragmented and inconclusive, with limited empirical evidence. Several recent studies have explored the integration of financial frictions within the conceptual framework of customer markets, revealing the adverse consequences associated with such frictions (Duca et al., 2017; Montero, 2017; Montero and Urtasun, 2021). The topic of business cycles is frequently examined within the context of macroeconomic frictions, as explored in various macroeconomic theories, such as the bank lending channel theory, modern economic growth theory (Li et al., 2020), and financial constraint theory (Zhang, 2019). The literature reveals a gap in the understanding of the relationship between firm value and financial frictions in the context of earnings management and firm productivity growth. Hence, this study aims to provide a novel perspective on this relatively overlooked domain within the agency theory framework, considering the presence of various degrees of friction as agency costs.

Firm value is affected by financial frictions across various dimensions. One such frictional cost for a firm’s capital is equity payout. When this cost is nonnegative, it ensures that the firm’s value is also nonnegative (Arellano et al., 2019). A decline in firm value was observed after the postwar period of 9/11 as a result of intense financial frictions and an increased occurrence of financial shocks within the economyFootnote 6. Bai et al. (2018) conducted a study wherein they examined two distinct forms of financial friction, namely, default risk and a fixed cost associated with loan issuance, to assess firm leverage. The findings indicate that, compared with larger firms, smaller firms encounter greater limitations in their ability to borrow, resulting in lower levels of leverage. Consequently, smaller firms also exhibit lower market value because of their relatively limited assets and capital values. Since these studies considered risk and cost as elements of friction, the current study attempts to differentiate by the fact that financial risks create shocks that are not long lasting, whereas costs are predefined and have an enduring impact on firms’ fundamental elements. Therefore, this study attempts to differentiate between these concepts by considering different levels of economic costs as agency costs among macro- and microeconomic-level participants. Another study by Hassan and Marimuthu (2016) proposes that firms that possess significant value in the capital market experience a favorable influence on their performance metrics, such as an elevated credit rating, market value, and societal recognition. The study conducted by Desai and Dharmapala (2009) examines the relationship between corporate tax avoidance, micro-level friction, and firm value. The findings indicate that tax avoidance has a positive effect on firm value in companies that exhibit stronger governance. Therefore, it can be deduced that financial friction plays a certain role in influencing a firm’s value. In light of the above literature, the following proposition is proposed.

H1: There is a significant association between different levels of financial friction and firm value.

H1a: Macroeconomic friction has a significant impact on firm value.

The presence of frictions at the micro or business level can be attributed to various factors, such as liquidity requirements, bank securities, collaterals, and tight credit supply, that ultimately affect firm value. (Peia and Romelli, 2022).

H1b: Microeconomic friction has a significant impact on firm value.

At the financial market level, these frictions arise due to information asymmetries, market inefficiencies, contractual constraints, and obstacles in the smooth functioning of capital markets, which hinder their efficiency and liquidity (Quadrini, 2011). Furthermore, financial frictions also exist at the firm level, encompassing issues related to agency problems, capital adjustment, labor, and operational costs (Khan and Thomas, 2013).

H1c: There is a significant impact of financial market friction on firm value.

However, this relationship may be influenced by other factors, such as a firm’s appropriate strategies, such as earnings management and productivity growth, which warrant further investigation. Financial frictions within the economy exert a significant impact on firms characterized by inadequate earning management (Ze-To, 2012), as evidenced by their tendency to maintain higher levels of cash, exhibit lower reporting quality, possess larger inventory holdings, and experience difficulties in collecting cash receivables (Mansali et al., 2019). Accounting information serves as a means to assess the financial performance of a company, while the act of documenting and recording financial information in the form of financial statements can be seen as a practice of earning management following accounting principles. Almari et al. (2021) conducted an assessment to examine the influence of earnings management on firm value. Their findings revealed a positive effect of earnings management on firm value. According to Lisboa (2016), if earnings management involves the creation of financial statements that do not adhere to legal guidelines, the resulting information may be misleading and inappropriate. The primary focus of business groups and enterprises is earnings management because of the greater likelihood of failure. Earning management is a potential strategy for firms to mitigate losses in the event of an unforeseen financial shock (Al Hussaini, 2018). Tang and Han (2018) discovered that acquiring firms should proactively enhance the quality of their financial reporting instead of engaging in earnings manipulation. By doing so, they can effectively reduce information friction, ultimately leading to a decrease in debt financing costs (Almari et al., 2021). Based on the preceding discourse, it can be inferred that earnings management potentially serves as a cushion to absorb the unforeseen financial shocks that may directly affect firms. In other words, earnings management is the mediating factor in the relationship between financial frictions and firm value.

H2: Earnings management mediates the relationship between financial frictions and firm value.

The role of technology adoption in businesses has become increasingly important in driving productivity growth in recent years. However, the presence of credit market imperfections and frictions poses challenges to the adoption of technology, particularly in emerging economies. This challenge is particularly pronounced during times of crisis (Queraltó, 2011). According to Levine and Warusawitharana (2021), a positive relationship exists between debt and equity financing and productivity growth. This correlation remains significant even after accounting for other firm characteristics. However, the relationship between financing and productivity growth is hindered by changes in financing costs (Impullitti, 2022). Specifically, higher financing costs are associated with reduced investment in projects aimed at enhancing productivity (Queraltó, 2011). A study conducted by Hung (2020) provides evidence supporting the notion that financial frictions are endogenous factors and serve as a mechanism through which productivity growth affects net total capital inflows (Ottonello and Winberry, 2020).

In addition to financing and technological advancement, resource allocation plays a crucial role in achieving high productivity. Notably, financial frictions resulting from limited debt enforcement can lead to a significant increase in current labor productivity (Chen and Song, 2007). According to Ly-Dai (2016), an increase in productivity growth has been found to positively affect both household saving rates and firm investments. This increase in saving rates leads to a greater net cash outflow than cash inflow. Based on the aforementioned studies, it is evident that productivity growth exerts a substantial influence on cash flows, capital, savings, and investments, thereby impacting businesses and subsequently influencing firms’ market value. However, these cash flows and investments are managed through earnings management, which further amplifies the impact of productivity growth.

H3: Firm productivity moderates the relationship between financial frictions and earnings management.

H3a: Firm productivity moderates the relationship between earnings management and firm value.

H3b: Firm productivity moderates the indirect relationship between financial frictions and firm value.

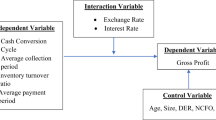

Figure 1 depicts the conceptual framework employed in this study to address its objectives. These objectives encompass the estimation of both direct and indirect effects of financial frictions on firm value and the extent to which productivity growth moderates the influence of earning management within this theoretical framework. Factor loadings measure these direct and indirect impacts.

describes the study’s theoretical framework, defining the direction of the relationship between the dependent variable (firm value), the independent variable (financial frictions), the mediating variable (earnings management), and the moderated mediator (productivity growth).

Methodology

The current study examines a causal relationship that elucidates the influence of financial frictions on firm value, with the mediating role of earning management and the moderating effect of productivity growth. The study examined data on nonfinancial sector firms in emerging economies, focusing specifically on representative countries from the Asia Pacific region, namely, China, India, Pakistan, Bangladesh, and Sri Lanka. The nonfinancial sector is chosen because it is particularly responsive to financial frictions, while the financial sector serves as the conduit for these frictions. Moreover, earnings management practices are also predominantly observed in the nonfinancial sector. The study is motivated by the sensitivity of the nonfinancial sector and the prevalence of earnings management practices. The results of this study can be applied to all industries outside the financial sector in various countries. The rationale behind choosing emerging economies lies in their amplified exposure to market imperfections, particularly financial frictions. Additionally, it is worth noting that emerging economies exhibit considerable growth potential. Consequently, there is a compelling need to examine the impact of financial frictions on the growth potential of businesses within these economies.

Data and sample

The data were gathered from nonfinancial firms operating within the emerging economies of the Asia Pacific region. A total of 735 nonfinancial sector firms were included in the dataset, with 310 originating from China, 200 from India, 100 from Pakistan, 50 from Bangladesh, and 75 from Sri Lanka. The sample mainly consists of manufacturing firms. There are several reasons for choosing Asian rising economies as the focus of study. The occurrence of financial crises in emerging economies throughout the 1990s prompted a significant amount of scholarly research, with a predominant focus on the restricted access to international credit faced by developing nations. However, a limited body of related research has specifically examined the issue of domestic credit market friction, although frictional bank lending has been a significant contributing factor to financial crises. Furthermore, developing markets are characterized by a somewhat weaker banking sector. Goldstein and Turner (1996) highlighted the disparity in the occurrence of financial crises between developing and industrialized nations throughout the 1980s and 1990s. Hence, examining financial crises in an emerging country characterized by a comparatively weaker banking sector is incredibly important. In conclusion, it is worth noting that the prevailing crisis has mostly affected developed nations. Consequently, there has been a notable lack of research on credit market friction in developing economies, which often exhibit weaker performance than established economies and thus pose prospective challenges. This area of study has been largely overlooked in the existing academic literature. The selection of nonfinancial firms is based on two criteria. First, firms that are actively listed on their respective stock exchanges and have not been delisted throughout the study period are selected. Second, companies with the highest market capitalization are selected. The data for this study were collected on an annual basis from 2005 to 2019. This study focuses on the nonfinancial sector due to the potential presence of financial frictions, such as interest rate fluctuations, which might arise from the financial sector. Consequently, enterprises that are susceptible to experiencing significant financial frictions are included in the analysis. The exclusion of post-2019 data is attributed to the impact of the coronavirus pandemic, during which numerous manufacturing firms and other nonfinancial firms suspended their operations and incurred substantial losses. The data about the firms included in the sample are sourced from the Refinitiv Data Stream. The data undergo a process of cross-verification, wherein any missing value is supplemented using information obtained from the financial statement of the firm, which can be accessed on the firm’s official website, as well as from the databases of the country’s security and exchange commission. Data on the macro, micro, and financial market indicators of various countries are gathered from the databases of international institutions such as the World Bank and the International Monetary Fund (IMF). Various proxies and indexes are constructed based on previous studies to measure the relevant variables.

Table 1 presents the operationalization and surrogate indicators employed for the primary variables in this study, drawn from relevant prior research. The controlling variables of firm size, operating cash flow, and leverage are introduced to control the heterogeneity bias of the firms under consideration. Several studies consider interest rates as a macroeconomic friction or a macro-prudential argument for economies (Angelini et al., 2012; Beau et al., 2012; Cesa-Bianchi and Rebucci, 2017; Kannan et al., 2012). These studies show that interest rates, including credit growth, asset prices, and loan-to-value limits, have an impact on the economy. Higher interest rates allow businesses to trade with suppliers at higher rates; higher interest rates also reduce the trend of equity investments as investors seek higher returns by investing in financial institutions. Similarly, higher interest rates cause firms to obtain less debt due to higher interest costs.

For two reasons, this study used the loan-to-asset ratio as a proxy for macroeconomic friction. First, because inflation is an integral part of interest rates, it is considered the primary source of macroeconomic friction in economies. However, in this study, inflation is not used as a source of macroeconomic friction because the sample countries of Pakistan, Sri Lanka, and Bangladesh are hyperinflationary economies with much higher and unstable inflation. Second, a firm’s creditworthiness is determined by its assets; if the loan amount is significantly less than its net assets, this indicates that there are higher interest rates or macroeconomic frictions in the economy, implying that firms avoid debt from financial institutions in their capital structure, despite having large collateralized assets to borrow and repay. However, a lower loan to asset ratio has a negative impact on firm value because firm is unable to take the leverage and thereby affects the firm expansion and growth which adversely affect firm value.

Furthermore, interest rates are not considered macroeconomic friction because, in our sample, most economies are control economies, such as China, Pakistan, Bangladesh, and Sri Lanka, where the government controls the interest rate and markets are not as free as in the U.S. and European countries. However, some studies use oil prices (Huntington, 2005; Jain and David, 2013), exchange rate risk (Priya and Sharma, 2023), tariffs and transportation costs (Corlay et al., 2017), the debt-to-income ratio in mortgage loans (Huo and Ríos-Rull, 2015), the cost of debt, and price and wage stickiness (Smets and Wouters, 2007) as proxies for financial frictions. Aside from these metrics, the loan-to-net asset ratio is the best indicator for capital-intensive manufacturing firms in emerging Asian economies. For these reasons, the total debt-to-net assets ratio is used as a proxy for macroeconomic frictions because debt is regarded as the primary capital requirement of businesses relevant to the firm’s net assets. Moreover, the study sample includes both small and large firms, total debt cannot be considered separately.

Previous studies use different proxies and measures for estimating productivity growth; for instance, labor growth (Song et al., 2011), an increase in technology and innovation adoption (Xie, 2023), an increase in capital resources (King and Levine, 1993; Lin et al., 2022), allocation and return on financial resources (Beck et al., 2000), output per worker, and per capita invested (Impullitti, 2022). If technology and innovation is improved, the manufacturing process of existing products will change to reduce costs, waste, defects, and lead time, as well as improve production efficiency. This will eventually increase firm sales and profits, which is empirically tested by Vivero (2002) that when the number of employees in Spain has increased by 1.4%, capital increased by 8.8%, and sales is increased by 16.5%. Similarly, investing in labor or capital will increase sales due to increased production facilities or machinery; otherwise, the enterprise will not grow effectively. As a result, sales growth is an indicator of firm growth that is dependent on a number of factors; if these factors are inefficient, sales will not increase. Complement to these facts, Syverson (2011) argued that all productivity growth measures produce almost similar results.

Moreover, the present study data are related to non-financial sector firms in which the majority are manufacturing firms that must sell physical goods, and their increase in goods sales is an indication of productivity growth. If firms invest in labor, technology, and innovation in products and increase their assets, their main purpose is to increase sales and not to enhance these factors. Therefore, due to these reasons, we have used sales growth as a proxy to measure productivity growth, which is a true picture of multiple factors.

Financial models

The estimation procedure involves the development of a hierarchical linear moderated mediation model using autoregressive path analysis equations proposed by Hayes (2015). The Hayes moderated mediation model is a method that enables the estimation of observed variable mediation, moderation, moderated mediation, and conditional process analysis. Igartua and Hayes (2021) assert that the current generation of models enables the examination of both direct and indirect effects within mediation and moderated moderation models.

Preacher and Hayes (2004) suggest that moderation and mediation can coexist inside a single paradigm. Moderated mediation, also referred to as conditional indirect effects, is a phenomenon wherein the impact of a treatment variable, specifically frictions, on an outcome variable, namely, firm value, is influenced by a mediator variable, in this case, earnings management. The extent of this influence varies based on the level of the moderator variable, which in this context is productivity growth. The estimation of moderated mediation by the Preacher and Hayes approach involved two models, namely, Model 1 and Model 2.

The mediation model, which has gained historical popularity, is the technique proposed by Baron and Kenny (1986). Throughout history, a considerable proportion of mediation analyses that have been published have relied on the causal stages’ method as their underlying logic. This technique continues to be extensively employed in contemporary research. Nevertheless, the increasing popularity of mediation analysis may be attributed, in part, to the persuasive arguments put out by quantitative methodologists who specialize in this field. These experts have effectively criticized its usage and proposed more effective alternatives.

In contemporary analyses of mediation, scholars have highlighted the observation that large mediated effects can occur even when one of the route coefficients has a negative value, despite the absence of a significant correlation between them (Hayes, 2009). If there is no significant relationship between any of the variable pairs in the model during bivariate analysis, it becomes less meaningful to evaluate the mediated models. The discrepancy in question is examined and analyzed through the utilization of the process models of mediation and moderation proposed by Hayes (2009).

In summary, the bootstrapping approach proposed by Preacher and Hayes (2004) offers a solution to the power constraints associated with the Sobel test. The proposed approach calculates the point estimate of the indirect impact by analyzing a substantial number of random samples. This method does not make any assumptions about the normal distribution of the data and is particularly well suited for situations with limited sample sizes, in contrast to the Barron & Kenny method.

The present study employs panel data models to estimate the coefficients of the models for continuous outcomes. Additionally, it aids in the establishment of percentile-based bootstrap confidence intervals for both conditional and unconditional indirect impacts. A moderated mediation model (MMM) is developed to assess the mediating effect of earnings management on the relationship between financial frictions and firm value while also considering the moderating role of productivity growth in this process. Productivity growth can be achieved through technology and innovation enhancement, labor growth, and investment in capital and labor resources, resulting in increased sales and profits for the company. Unlike other strategies, productivity growth is a direct and tangible way for businesses to outperform in their industry.

Financial leverage is a control variable in the study, it is incorporated in the models to control the heterogeneity of the listed manufacturing firms of various sectors like textile, cement, food and beverages and chemicals etc. Moreover, financial leverage has a significant relationship with firm performance (Ghosh, 2007; Stelk et al., 2018; Vătavu, 2015). Therefore, financial leverage being an essential component of firms’ performance is added in the study as a controlling variable.

Financial leverage also supports agency theory which is the underpinning theory of the study, as higher leverage usually leads to higher agency costs because of the diverging interests between shareholders and debt holders (Dey et al., 2018).

The moderated mediation model, as proposed by Preacher and Hayes (2004), posits that the relationship between independent variables and dependent variables is influenced by both moderating and mediating variables. In this model, the mediating variables serve as intermediaries through which the independent variables impact the dependent variables. Additionally, the moderating variables play a role in controlling the mediation process by influencing the conditional indirect effect. To evaluate the conditional direct influence and moderating role of productivity growth, multiple financial frictions and earning management techniques, along with their respective interaction terms, are incorporated simultaneously at each stage of the hierarchical test equation.

Mediation model

Wen and Ye (2014) examined the advantages and disadvantages of four test methodologies: the sequential test, the hierarchical test, the interval test of the coefficient product, and the test for differences in mediating effects. The hierarchical test demonstrated a greater degree of explanatory power than the other methods. The anticipated impact of financial frictions on Firm value is calculated using Hayes’ hierarchical technique, specifically Model 59, which outlines the moderated Mediation effect. Preacher and Hayes (2004) have developed different models to address the moderation and mediation dynamics. They developed 70 different models with each model having different dynamics of moderation and mediation. Each model is denoted with numbers from 1 to 70. The present study adopted the settings of model 59, which is known as Moderated Mediation Model, which is based on hierarchical method. The current study utilizes Moderated Mediation to examine how earnings management mediates the link between financial frictions and firm value, while also considering how productivity growth moderates this relationship. Given below is Model 1 which estimates the mediating impact of Earnings management, specifically focusing on the straightforward mediation of earnings management.

where MAF is the macroeconomic friction, MIF is the microeconomic friction, FMF is the financial market friction, FV is the firm value, EM is earnings management, and PG is productivity growth. In Eq. (1), i stands for the firm, t for the year, EM is the mediating variable, MAF, MIF, and FMF are the main independent variables, and \({\beta }_{1}\) is a constant term in Eq. (1). \({{\beta }_{6}{MAF}}_{{it}}{({PG})}_{{it}},\,{\beta }_{7}{{MIF}}_{{it}}{({PG})}_{{it}}\), and \({\beta }_{8}{{FMF}}_{{it}}{({PG})}_{{it}}\) are the interaction terms of the independent variables with the moderating variable, \({\mu }_{t}\) is the cross section fixed effect.

The mediating effect of Earnings Management between Financial Frictions and Firm Value is given by the coefficients \({\beta }_{2},{\beta }_{3}\), and \({\beta }_{4}\). These coefficients indicate the significance of the mediating effect of Earnings Management. Similarly, if \({\beta }_{5},{\beta }_{6},\,{\beta }_{7}\), and \({\beta }_{8}\) are significant, then this tells us the substantial role of Productivity Growth in the mediation of Earnings Management.

Moderated mediation model

To examine the moderated mediation effect of Productivity Growth on the mediating process, a series of regression analyses are conducted. These analyses are evaluated sequentially using Model 2 which is as follow.

where MAF is the macroeconomic friction, MIF is the macroeconomic friction, FMF is the financial market friction, FV is the firm value, EM is the earnings management, PG is the productivity growth, OCF is the operating cash flow, SIZE is the size of the firm, and LEV is the leverage.

The current study aims to predict the mediating impact of earnings management, moderated by productivity growth, based on the significance of factor loadings. In addition, the factor loadings of the equations are utilized to calculate the conditional direct and indirect impact of macro, micro, and financial market frictions on firm values.

Partial adjustment model

The present investigation examined the effects of financial frictions on the valuation of firms. Nevertheless, it is important to note that the firm’s value does not instantaneously adapt to the presence of financial frictions. Over time, it undergoes adjustments and exhibits delayed effects on the valuation of a company. The estimation of the long-term adjustment of firm value, considering various categories of frictions, is conducted using a partial adjustment model. This model is chosen based on the nature of the relationships between the variables.

The partial adjustment model addresses the lagged adjustment through lag estimation. Consider the adjusted factor λ as scaling factor for estimating short run relationship. The partial adjustment model works under the assumption that the actual variation is equally adjusted to the optimal properties. Mathematically, this process can be represented as

where y* is the desired value of y. The adjusted factor λ equals both sides of the above equations. Moreover, it also depicts the speed of adjustment. The greater the value of λ is, the greater the efficiency. Traditionally, the λ value is less than one, but in special cases, it can be greater than one. From Eq. 3, the statistical identity is as follows:

The current study analyzed the impact of financial frictions on firm value through the moderated mediation of PG and EM, where \({\rm{\lambda }}\) is the adjusted factor that estimates the effect of FF on FV in the long run, as follows.

where MAF is the macroeconomic friction, MIF is the microeconomic friction, FMF is the financial market friction, FV is the firm value, EM is earnings management, and PG is productivity growth.

The factor loadings and parameters are examined in the short-term and long-term to assess the effects of financial frictions on firm value. This analysis considers the delayed influence of the mediation process, as well as the conditional impacts observed in both the short-term and long-term.

where MAF is the macroeconomic financial friction, MIF is the macroeconomic financial friction, FMF is the financial market friction, FV is the firm value, EM is the earnings management, PG is the productivity growth, OCF is the operating cash flow, Size is the size of the firm, and LEV is the leverage.

The utilization of panel data models is employed to estimate partial adjustment models, given the panel data structure of the dataset. The efficiency of panel data models is assessed using diagnostic tests such as the Hausman test, Pesaran test, Wooldridge test, and Wald test.

Empirical evidences

This study aims to estimate the influence of financial frictions on firm value within the context of moderated mediation involving earning management and productivity growth. The analysis is conducted based on the assumptions of the partial adjustment model. The initial step involved the evaluation of descriptive data, followed by the estimation of mediation and moderated mediation models through case wise analysis.

Descriptive statistics

Descriptive statistics provide an analysis of the characteristics and organization of the data of individual variables. The descriptive statistics are used to assess the fundamental features of all the data including the mean, standard deviation, skewness, and level of dispersion of the main and control variables, as presented in Table 2. The analysis reveals that certain variables, such as macroeconomic frictions, microeconomic friction, and size, exhibit considerable standard deviations. This indicates a high level of variability in the data, resulting in a decrease in kurtosis and a reduction in the mean dispersion of the curve. The skewness statistics indicate that the data exhibit a deviation toward one side. The observed high skewness in the dataset can be attributed to the presence of cross-sectional variations and heterogeneity within the panel data.

The problem of panel data heterogeneity is resolved by employing panel data estimation techniques for moderated mediation models and by including control variables. The kurtosis of PG and EM exhibits a substantial magnitude, indicating a distribution fatter tailed than normal expecting higher residuals. Such higher kurtosis is because of panel heterogeneity of the data.

Empirical estimation

To examine the relationship in both the short and long-term, we employed a developed moderated mediation model and tested it using the autoregressive model. The statistical analysis reveals that the coefficients of all the independent variables associated with financial frictions have a significant impact on firm value in the short run, as indicated in Table 3, while Table 4 provides the same implications for FFs in the long run by applying a partial adjustment model.

The presence of negative factor loadings indicates that the combined influence of MAF, MIF, and FMF on FV is predominantly negative and significant. The devaluation of firms is a consequence of higher financial frictions in emerging economies. In Model 1, FMF had the highest constant negative impact (−0.3390) compared to the other two forms of friction in the short run in Bangladesh, while FMF had the most negative impact (−0.9435) in the case of Pakistan. This is due to Pakistan having the highest financial market friction because of having the highest inflation, interest, and tax costs compared to the other countries. Similarly, compared with the other two types of friction, the interaction term of FMF with PG had the greatest negative impact. The effect of all the FFs in their interaction terms with PG is much less than their independent effect in Model 1, which shows the significance of the moderation of PG, which mitigates their independent effects. The overall effect of PG is positive and reaches a maximum in the case of Bangladesh (0.1345). Through the use of EM mediation in Model 2, it was observed that MIF had the lowest effect, which was found to be zero. The findings indicate that the mediating role of EM in relation to FFs is characterized by a positive effect with a maximum value of 0.0460 in India. While incorporating the mediation equation in Model 2, it is observed that the effect of all the FFs decreases in the absolute values of the MAF, MIF, and FMF coefficients, suggesting that EM serves to alleviate the adverse impact of financial frictions on firm value. This reduction is recorded in the FMF coefficient by 23.64%, specifically from −0.025 to −0.019 in China. In the case of India, the reduction amounts to 20.69%. In Pakistan, the reduction is recorded at 30.43%. In Bangladesh and Sri Lanka, the reductions are 56.75 and 47.22%, respectively. These results provide robust evidence in favor of the proposition that earnings management plays a significant role in mediating the negative impact of financial frictions on firm value. These findings are in line with prior similar studies conducted by Al Hussaini (2018), Arellano et al. (2019), and Chen and Song (2007). The results of the study provide empirical evidence that the practice of earnings management, specifically through legitimate manipulation, serves to mitigate the adverse effects of financial frictions on the overall value of a firm. The results of the study also showed that there is a positive relationship between firm value and firm size. The results presented in Table 3 indicate that the inclusion of the mediation effect in the consolidated model reveals significant and negative relationships between the coefficients of MAF, MIF, and FMF and firm value. According to Mansali et al. (2019), the introduction of firm EMs in both models effectively mitigates the impact of FFs, suggesting that EMs play a crucial role in mediating the relationship between firm valuation and financial frictions. MIF has the lowest degree of adverse consequences across all nations, while FMF has the highest level of negative repercussions.

In both models, the detrimental effects of frictions are mitigated through the inclusion of the moderating variable PG in the interaction term of FF and PG in the short-term. The impact of PG is more pronounced for FMF than for MAF and MIF. In the second model, the inclusion of the interaction term resulted in a heightened influence of EM mediation. The aforementioned studies by Midrigan and Xu (2014), Peia and Romelli (2022), Peters and Roberts (2022), and Schoenmaker and Van Tilburg (2016) provide empirical evidence in support of the proposition that earnings management serves as a mediating factor in the association between firm value and financial frictions. Additionally, these studies suggest that productivity growth plays a moderating role in the relationship between firm value and financial friction, as previously posited. Both models propose that there exists a positive relationship between firm value and both size and operating cash flow, while a negative relationship is observed between firm value and leverage. The coefficient value suggests that over time, the detrimental influence of financial frictions on firm value diminishes, while the influences of EM and PG intensify. This finding implies that moderated mediation exerts a more pronounced effect in the long-term than in the short-term.

Table 4 illustrates the alterations in factor loadings over an extended period, exhibiting a diverse range of transformations. In each instance, the factor loadings in Model 1 experienced a decrease, suggesting that the estimated coefficients of the model are inflated in the short-term but reach a stable state in the long-term. Model 1 pertains to the mediation model, which provides evidence for the mediating effect of EM. This finding suggests that the influence of financial frictions on EM may be exaggerated or excessively reactive in the short run but becomes more stable in the long run. The observed disparity in outcomes between the short and long run can be attributed to the proactive management of frictions by the EM in the short run, which subsequently stabilizes in the long run.

The coefficients presented in Table 4 demonstrate that the factor loadings in the moderated mediation model increased over time. This finding suggested that the impact of moderated mediation has also increased in the long run. Additionally, the analysis reveals that firm value exhibits greater sensitivity to the mediation of EM and moderated mediation through productivity growth. This finding indicates that firm value is more responsive to financial frictions in the long run, which aligns with the timing of the occurrence of financial frictions.

According to the findings presented in Table 5, the presence of financial frictions has a detrimental effect on firm value in the short-term, specifically when considering the conditional direct impact in relation to the PG. The introduction of the mediating effect of EM results in a decrease in the conditional direct impact of all financial functions. Compared with alternative financial frictions, financial market friction (FMF) has the most significant adverse effects, both directly and indirectly.

Pakistan experiences the most significant negative conditional direct impact from FMF, followed by India and China. The MIF exhibits the lowest conditional direct and indirect influence on firm value in comparison to the other two financial frictions across all countries. With the exclusion of the direct impacts of the MAF on FV in China and Sri Lanka, as well as the indirect impacts of MIF on FV in Pakistan and Sri Lanka, the majority of bootstrap confidence intervals indicate that all conditional direct and indirect effects are statistically significant. It is evident that PG plays a substantial role in the moderation of the model.

In a similar vein, the conditional direct and indirect impacts of financial frictions are measured through the utilization of partial adjustment models, as illustrated in Table 6. The significance of all the variable coefficients remains consistent with the short-term context. The findings indicate that the enduring direct and indirect consequences of financial frictions are notably diminished compared to their immediate effects, suggesting normalization of the frictional impact. It can be argued that there is an overestimation of financial frictions in the short-term. The observed conditional impacts align with the intermittent previous studies about financial frictions.

Robustness tests

The Hausman test, Pesaran test, Wooldridge test, and Wald test are commonly employed in academic researches to evaluate the robustness of empirical findings. The purpose of these tests was to evaluate the efficacy of panel data models and validate their ability to elucidate the examined relationship. The results of the Hausman test, as presented in Table 7, indicate statistical significance, indicating that the fixed effect model is superior to the random effect model. When comparing the results of other efficiency tests, it is observed that Model 2 exhibits a more random effect than a fixed effect in the case of the Pakistan data, which is once again subject to adverse selection. The results of the Pesaran test exhibit statistical significance, suggesting a robust cross-sectional correlation among the variables.

Based on the lack of significance of the Wooldridge test results, it can be inferred that there is a lack of autocorrelation. Autocorrelation is found to be minimal solely in the context of Bangladesh, and we have mitigated this concern by incorporating the lag effect in the long-term analysis. The Wald test is a statistical method used to assess the presence of heteroscedasticity within groups. A parametric statistical measure is employed to assess the collective significance of a set of independent variables in a model. The significance of all the results in both models suggests that all the financial functions included in the models are collectively significant and that there is no heteroscedasticity in the data.

Conclusions

The primary aim of this research is to investigate the relationship between different levels of financial friction and firm value. The findings indicate a negative association between financial frictions and firm value, suggesting that there is ample evidence to support this relationship. Furthermore, the analysis reveals that the influence of financial market frictions on firm valuation surpasses that of macroeconomic and microeconomic frictions, revealing the pronounced impact of constraints arising from the agency problem. This study provides compelling evidence that the involvement of nonfinancial firms in accrual earnings management serves as a mediator, resulting in a positive impact on the relationship between financial frictions and firm value, which is a countercyclical tendency theory of earnings management. Furthermore, it effectively mitigates the adverse effects of financial frictions (Cohen and Zarowin, 2007). The findings presented in this study align with the conclusions drawn in prior research conducted by Almari et al. (2021), Filandari and Suhendra (2017), Handayani and Ibrani (2020) and Karabarbounis and Macnamara (2021). However, these aforementioned studies did not incorporate earnings management as a variable in their regression models. The findings of this study are aligned with those reported by Peters and Roberts (2022), which reveal that there is a positive relationship between productivity growth and firm value, which is the signaling effect of productivity growth. This relationship was established through the examination of conditional direct and indirect effects, as well as interaction terms. Additionally, the study reveals that productivity growth plays a significant role in mitigating the consequential impact of financial frictions (through signaling) and enhancing the mediation of earnings management, as was evident in the study of Karabarbounis and Macnamara (2021), which is based on a comparison of private and public firms. This finding suggests that improved firm dynamics can alleviate financial frictions, as highlighted by Jacoby et al. (2018). There exists a positive correlation between the size and operating cash flow of a firm and its value. Moreover, empirical evidence suggests that in the contexts of China and India, larger firms tend to show greater firm value. The results of the study showed a significant inverse correlation between leverage, which refers to higher levels of debt, and the valuation of a company.

The findings suggest that there is greater consistency of firm value in the long run than in the short run. This implies that financial frictions are likely to be overestimated in the short run when compared to the long run, and their adverse impact is mitigated over time. The normalization and control of financial frictions are achieved through the mediation of earnings management and the moderation of productivity growth.

The relationship between financial frictions and firm value is negatively influenced (agency theory), and this negative effect is mediated by accrual earnings management (countercyclical theory). Additionally, the presence of productivity growth moderates the relationship between financial friction and firm value (signaling theory), further reinforcing the mediating effect of EM.

The current research has significant implications for developing economies regarding the influence of financial frictions on their firm value. Financial friction causes turbulence in the value of firms in emerging economies’ capital markets. These frictions result from higher interest rates, material costs, and equity costs for investors. This implies that companies will encounter heightened economic stress at different levels, and disregarding the concerns of market and economic participants is inevitable. Consequently, firms are advised to formulate strategic plans to address these limitations, which have economic consequences. Initially, it is recommended that the company strive to attain optimal productivity growth through enhancements in technology, innovations, the adoption of efficient labor practices, cost reduction, or sales expansion. Implementing effective accrual-based earnings management can also lead to an increase in firm value for companies.

According to the study’s findings, firms must bear higher costs in the short run than in the long run, but these frictions eventually stabilize over time. As a result, it is suggested that firms increase their working capital to meet short-term liabilities and economic constraints. If firms do not prepare for these frictions, they will be unable to achieve their optimal firm level in the economy. Following these economic frictional effects, firms may be better prepared and able to adjust their product prices in response to changes in demand or supply, potentially mitigating the impact of frictional shocks to inflation and inputs.

This study contends that incorporating frictions can improve the model’s ability to match real-world data when investigating firm value in economies, as most models previously assumed free economies with no frictional effects. Incorporating frictions into the moderated mediation model can account for a broader range of economic phenomena and provide a more nuanced understanding of the forces driving firm value, resulting in better policy recommendations for firms. We can develop more effective economic stabilization and growth policies by better understanding firm values and the role of friction. The present study also provides a complete guide for governing bodies to develop comprehensive policies regarding interest rates and tax costs. These costs are the root cause of increased economic friction and instability, as well as firm losses.

Although this study focused on South Asian countries, the findings may also apply to other emerging and developing countries. To gain a more complete understanding of the economy, future research should focus on integrating findings from the current study into other macroeconomic frameworks and industries, such as new Keynesian models, service sectors, financial institutions, and public sectors. Further research can look into firms’ value constraints caused by international frictions, labor market frictions, channel market frictions, and other levels of frictions, and empirical solutions can be proposed.

The present study is subject to limitations concerning the number of metrics employed to examine macroeconomic and microeconomic frictions, with a specific emphasis on external financing and trade credits. Furthermore, the study is limited to emerging economies in South Asia. By including emerging economies from other continents, the study could have obtained more generalized results.

Data availability

The source of Data is the Refinitiv® DataStream International® repository. The Data can be accessed from the Refinitiv® DataStream International® repository under its term of use. Before downloading the data, user must register to Refinitiv DataStream International (https://eikon.refinitiv.com/). The supplementary Data Material is available at: https://doi.org/10.7910/DVN/P9OYBW.

Notes

According to the fundamental Modigliani and Miller (1958), M&M theorem a company’s financing has no impact on its firm value when there are no taxes, bankruptcy costs, agency costs, symmetric information, or efficient markets in place. The assumptions of this theory suggest that companies are performing in a world with perfectly frictionless markets where they have to pay no taxes, trade securities without incurring any transaction costs, be able to file for bankruptcy without incurring any fees and have perfectly symmetrical information.

Zogning, (2017) explained the broad scope of agency theory. The goal of agency theory is both explained and settled disagreements over the relative interest held by principals and the agents who work for them. Since principals rely on agents to carry out some transactions, there is often a lack of consensus on the order of priority and the procedures to be used. The process of bringing the divergent expectations into alignment is referred to as “reducing agency loss”. One technique that is employed to establish a balance between principal and agent is through the use of remuneration that is dependent on performance.

See Toumeh and Yahya (2019) that explained the different types of legitimate earnings management according to International Financial Reporting Standards, IFRS.

Emerging markets are typically attractive to investors from other countries because of the significant potential return on investment they may offer. Many countries require a sizable infusion of money from outside sources in order to transition from having an economy that is focused on agriculture to having an economy that is developed because they do not have sufficient resources domestically (Divecha et al. 1992).

Cheng et al. (2020) discovered that entrepreneurs choose between innovative and mature technical ventures based on a threshold value of financial frictions. This implies that economic progress is guaranteed by a frictionless financial market, however financial innovation may be the driving force behind economic expansion.

Bergin et al. (2014) explained that why there was a decline in the establishment of new businesses and a decline in the value of company equity during the postwar period in the United States due to unfavorable financial shocks. Additionally, a useful macroeconomic adjustment margin permits the number of enterprises to decline following a negative financial shock.

References

Adler D (2014) The new economics of liquidity and financial frictions. CFA Institute Research Foundation Working Paper(3). Available at https://www.cfainstitute.org/-/media/documents/book/rf-publication/2014/rf-v2014-n4-1-pdf.pdf

Ahmad N, Salman A, Shamsi A (2015) Impact of financial leverage on firms’ profitability: an investigation from cement sector of Pakistan. Res J Financ Account 6(7):2222–1697

Akinci Ö (2021) Financial frictions and macro‐economic fluctuations in emerging economies. J Money Credit Bank 53(6):1267–1312

Akinci O, Olmstead-Rumsey J (2018) How effective are macroprudential policies? An empirical investigation. J Financial Intermediation 33:33–57

Al-Slehat ZAF, Zaher C, Fattah A, Box P (2020) Impact of financial leverage, size and assets structure on firm value: evidence from industrial sector, Jordan. Int Bus Res 13(1):109–120

Al Hussaini AN (2018) Earning management through marginal effect of firm based and regional economic indicators: a study on listed firms in Kuwait. Asian J Empir Res 8(11):417–433

Almari MOS, Weshah SRS, Saleh MMA, Aldboush HHH, Ali BJ (2021) Earnings management, ownership structure and the firm value: an empirical analysis. J Manag Inf Decis Sci 24(7):1–14

Angelini P, Neri S, Panetta F (2012) Monetary and macroprudential policies, No 1449, Working Paper Series, European Central Bank, https://EconPapers.repec.org/RePEc:ecb:ecbwps:20121449

Arellano C, Bai Y, Kehoe PJ (2019) Financial frictions and fluctuations in volatility. J Polit Econ 127(5):2049–2103

Asker J, Collard-Wexler A, De Loecker J (2014) Dynamic inputs and resource (mis) allocation. J Polit Econ 122(5):1013–1063

Ayuba H, Bambale AJA, Ibrahim MA, Sulaiman SA (2019) Effects of Financial Performance, Capital Structure and Firm Size on Firms’ Value of Insurance Companies in Nigeria. J Finance Account Manag 10(1):57–74

Bah E-h, Fang L (2016) Entry costs, financial frictions, and cross-country differences in income and TFP. Macroecon Dyn 20(4):884–908

Bahraini S, Endri E, Santoso S, Hartati L, Pramudena SM (2021) Determinants of firm value: a case study of the food and beverage sector of Indonesia. J Asian Financ Econ Bus 8(6):839–847

Bai Y, Lu D, Tian X (2018) Do financial frictions explain Chinese firms’ saving and misallocation? (Working Paper No. w24436). National Bureau of Economic Research. Available at https://www.nber.org/system/files/working_papers/w24436/w24436.pdf?sy=436

Baron RM, Kenny DA (1986) The moderator–mediator variable distinction in social psychological research: conceptual, strategic, and statistical considerations. J Personal Soc Psychol 51(6):1173

Beau D, Clerc L Mojon B (2012) Macro-prudential policy and the conduct of monetary policy. Banque de France Working Paper No. 390, Available at SSRN: https://doi.org/10.2139/ssrn.2132404

Beck T, Levine R, Loayza N (2000) Finance and the sources of growth. J Financial Econ 58(1-2):261–300

Bergin P, Feng L, Lin CY (2014). Financial frictions and firm dynamics. National Bureau of Economic Research, NBER Working Paper, (w20099). Available at https://www.nber.org/system/files/working_papers/w20099/w20099.pdf

Bernanke BS, Gertler M, Gilchrist S (1999) The financial accelerator in a quantitative business cycle framework. Handb Macroecon 1:1341–1393

Caballero RJ, Engel E (1991) Dynamic (S, s) economies. National Bureau of Economic Research Cambridge, Mass., USA

Catherine S, Chaney T, Huang Z, Sraer D, Thesmar D (2022) Quantifying reduced‐form evidence on collateral constraints. J Financ 77(4):2143–2181

Cesa-Bianchi A, Rebucci A (2017) Does easing monetary policy increase financial instability? J Financial Stab 30:111–125

Chen K, Song ZM (2007) Financial Friction, Capital Reallocation and News-Driven Business Cycles. Capital Reallocation and News-Driven Business Cycles (July 5, 2007). Available at SSRN: https://ssrn.com/abstract=998819 or https://doi.org/10.2139/ssrn.998819

Chen MJ, Columba MF (2016) Macroprudential and monetary policy interactions in a DSGE model for Sweden: International Monetary Fund. (Working Paper No. # WP/16/74). Available at https://www.imf.org/external/pubs/ft/wp/2016/wp1674.pdf

Cheng D, Cheng L, Guo Y (2020) Financial Market Improvement, Entrepreneurs’ Technology Choice, and Economic Growth. In: Wang TS, Ip A, Tavana M, Jain V (eds) Recent Trends in Decision Science and Management. Advances in Intelligent Systems and Computing, vol 1142. Springer, Singapore. https://doi.org/10.1007/978-981-15-3588-8_44

Choi S, Smith BD, Boyd JH (1996) Inflation, financial markets, and capital formation. Rev-Fed Reserve Bank St Louis 78:9–35

Cohen DA, Zarowin P (2007) Earnings management over the business cycle. New York University/Stern School of Business. Available at https://web-docs.stern.nyu.edu/old_web/emplibrary/EM_08_23_07FINAL.pdf

Cooley TF, Quadrini V (2001) Financial markets and firm dynamics. Am. Econ Rev 91(5):1286–1310

Corlay G, Dupraz S, Labonne C, Muller A, Antonin C, Daudin G (2017) Comment: inferring trade costs from trade booms and trade busts. Int Econ 152:1–8

Covas F, Driscoll JC (2014) Bank Liquidity and Capital Regulation in General Equilibrium. FEDS Working Paper No. 2014-85, Available at SSRN: https://ssrn.com/abstract=2520193 or https://doi.org/10.2139/ssrn.2520193

DeGennaro RP, Robotti C (2007) Financial market frictions. DeGennaro, Ramon. P. Cesare Robotti. “Financial Mark. Frict. ” Economic Rev. 92:1–16

Desai MA, Dharmapala D (2009) Corporate tax avoidance and firm value. Rev Econ Stat 91(3):537–546

Dey RK, Hossain SZ, Rahman RA (2018) Effect of corporate financial leverage on financial performance: A study on publicly traded manufacturing companies in Bangladesh. Asian Soc Sci 14(12):124

Divecha AB, Drach J, Stefek D (1992) Emerging markets: a quantitative perspective. J Portf Manag 19(1):41

Duca I, Montero JM, Riggi M Zizza R (2017) I will survive. Pricing strategies of financially distressed firms. Pricing Strategies of Financially Distressed Firms (March 28, 2017). Bank of Italy Temi di Discussione (Working Paper) No, 1106

Filandari M, Suhendra ES (2017) The influence of earning management to firm value in Indonesia manufacturing companies. Econ şi Soc 3:28–36

Fuentes‐Albero C (2019) Financial frictions, financial shocks, and aggregate volatility. J Money Credit Bank 51(6):1581–1621

Fujita M (1989) Internationalization of Japanese commercial banking and the Yen: the recent experience of city banks. In Developments in Japanese Economics. Academic Press, pp. 217-251

Ghosh S (2007) Leverage, managerial monitoring and firm valuation: A simultaneous equation approach. Res Econ 61(2):84–98

Goldstein M, Turner P (1996) Banking crises in emerging economies: origins and policy options. Ch. 8, (pp. 301-363). World Scientific Publishing Co. Pte. Ltd. Available at https://EconPapers.repec.org/RePEc:wsi:wschap:9789814749589_0008

Gomes J, Jermann U, Schmid L (2016) Sticky leverage. Am. economic Rev. 106(12):3800–3828

Gonatha M, Juliana R (2021) The Effect of Financial Market Frictions to Firm’s Diversification Level in Indonesia. Paper presented at the 4th International Conference on Sustainable Innovation 2020-Accounting and Management (ICoSIAMS 2020). Atlantis Press, pp. 361-369. https://doi.org/10.2991/aer.k.210121.051

Grodecka A, Finocchiaro D (2018) Financial frictions, financial regulation and their impact on the macroeconomy. Sveriges Riksbank Econ Rev 48:48–69