Abstract

Explaining and forecasting inflation are important and challenging tasks because inflation is one focus of macroeconomics. This paper introduces novel investor attention to the field of inflation for the first time. Specifically, the Granger causality test, vector autoregression (VAR) model, certain linear models, and several statistical indicators are adopted to illustrate the roles of investor attention in explaining and forecasting inflation. The empirical results can be summarized as follows. First, investor attention is the Granger cause of the inflation rate and has a negative impact on inflation. Second, predictive models that incorporate investor attention can significantly outperform the commonly used benchmark models in inflation forecasting for both short and long horizons. Third, the robustness checks show that updating investor attention or the model specification does not change the conclusion of the crucial role of investor attention in explaining and forecasting inflation. Finally, this paper proves that investor attention influences inflation through inflation expectations. In summary, this paper demonstrates the importance of investor attention for macroeconomics, as investor attention affects inflation.

Similar content being viewed by others

Introduction

Inflation reflects the rise in price level in a society for a certain period. A lower inflation level is detrimental to the growth of social wealth, while a higher inflation level leads to a decrease in social wealth, and a given society needs a moderate level of inflation to promote sustained wealth growth. Thus, inflation stands as one focus in academia because of its diverse economic and financial aspects and has become one of the most important goals of macroeconomic regulation in various countries (Woodford and Walsh, 2005; Yellen, 2017; Effah Nyamekye and Adusei Poku, 2017). Recently, the urgency of research on inflation has further strengthened and has received increasing attention from central banks due to multiple factors, such as COVID-19, the excessive issuance of global currency, carbon neutrality expectations, and variations in international crude oil prices.

The explanation and forecasting of inflation are two attractive aspects of research on inflation and have made numerous achievements. For example, Fama (1975) and Zakaria et al. (2021) highlight the importance of understanding inflation with traditional economic and financial factors, i.e., interest rates and crude oil; McKnight et al. (2020) and Choi (2021) adopt sophisticated models to forecast actual inflation and argue for the suitability of the selected models in inflation forecasting. However, the shortcomings of current research are also evident. For example, current research overly emphasizes the role of traditional economic and financial factors in inflation determination and lacks in-depth investigations on the roles of emerging factors (Aparicio and Bertolotto, 2020). Additionally, the commonly adopted New Keynes Phillips Curve (NKPC)-based models for inflation forecasting have reached a limit, and their forecast accuracy is weak (Mavroeidis et al. 2014, Aparicio and Bertolotto, 2020).

Thus, discovering novel factors to explain and accurately forecast inflation has become an interesting and important issue. However, relevant investigations seem to be limited, which represents a research gap and motivates the authors to identify and explore novel factors and help fill the gap.

Investor attention, generated from behavioural finance, is an emerging issue in current research on finance and economics and is theoretically connected with inflation. First, investor attention affects asset pricing in diverse ways (Chen et al. 2022; Cai et al. 2022; Liu et al. 2022), and inflation is a direct reflection of general price variations in a society. Second, investor attention reflects individuals’ information acquisition (Chen and Lo, 2019), and information is one of the most critical factors in forming inflation expectations (Larsen et al. 2021). According to the theory of NKPC (Friedman, 1968; Chen and Lo, 2019), inflation expectations affect inflation. Therefore, investor attention and inflation are connected.

Despite the theoretical connections, few studies discuss the connections between investor attention and inflation, making this paper of significance to research both inflation and behavioural finance. In this context, the research objective of this paper is to explore whether investor attention can empirically affect inflation. Consequently, this paper aims to combine behavioural finance and macroeconomics to explore what kind of relationship is hidden between the two issues. Based on the current investigations of explaining and forecasting inflation, the theoretical connection between investor attention and inflation, the research question, and the research objective, this paper proposes three hypotheses:

H1: Investor attention can empirically explain inflation.

H2: Investor attention can empirically forecast inflation.

H3: Investor attention affects inflation through its influence on inflation expectations.

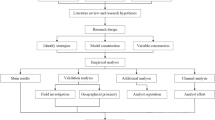

The originality of this paper lies in its connection of investor attention and inflation, thus providing new empirical insight into macro inflation with respect to micro-investor attention. To the best of our knowledge, this paper makes the following contributions to the literature regarding investor attention and inflation. First, this paper may represent the first attempt to empirically explain and forecast inflation from the aspect of investor attention, thus extending the application of emerging investor attention to conventional macroeconomics. Second, this paper provides additional empirical evidence that inflation is influenced by not only conventional factors but also emerging factors, for example, investor attention. The empirical process can be summarized as follows. First, this paper constructs a VAR model and implements the corresponding Granger causality test to explore the explanatory power of investor attention on inflation. Second, based on the models for explaining inflation with investor attention, we construct predictive models to further compare and evaluate the forecast accuracy with commonly used techniques in inflation forecasting during short and long horizons. Third, this paper updates the data and model specifications to implement robustness checks to ensure the rigor required of an academic research paper. Finally, given the connections between investor attention and inflation expectations, this study empirically tests the correlation between inflation expectations and investor attention.

This study is structured as follows. Section 2 provides a brief literature review on inflation and investor attention. Sections 3 and 4 present the data and methodologies, respectively. The empirical results are shown in Section 5. Section 6 describes the robustness checks. Section 7 further discusses investor attention and inflation expectations. Section 8 concludes the paper.

Literature review

This paper focuses on inflation from two perspectives, i.e., inflation explanation and forecasting; in fact, numerous relevant investigations have been performed. For example, Canova and Ferroni (2012) attribute variations in inflation to monetary authorities. Murphy (2014) and Friedrich (2016) explain inflation by the Phillips curve and its derivative models. Hakkio (2009), Monacelli and Sala (2009), Ciccarelli and Mojon (2010), and Mumtaz and Surico (2012) argue that several factors can influence inflation, such as industrial production, unemployment rates, and nominal wages. Altissimo et al. (2009) investigate inflation from the perspective of the aggregation mechanism, and Forbes et al. (2021) use a ‘trendy’ approach to understand inflation dynamics. More recently, Bouras et al. (2023) and Liu and Ma (2023) attribute inflation to the cost of firms and the exchange rate, respectively. Tillmann (2024) argues that supply chain pressure contributes to inflation. Inflation forecasting has also been a focus of research and is a popular topic in academia. Specifically, econometric and statistical forecasting models are preferred by researchers. For example, Marcellino et al. (2003), Ang et al. (2007), Clements and Galvão (2013) select the VAR model, and Forni et al. (2003), Eickmeier and Ziegler (2008), and Hall et al. (2023) adopt the dynamic factor analysis to predict inflation issues. Nakamura (2005), Szafranek (2019), and Almosova and Andresen (2023) use a neural network, and Wright (2009) and Hauzenberger et al. (2023) employ the Bayesian method and nonlinear dimension reduction techniques, respectively. Survey-based inflation forecasts have also been studied (Croushore, 2010; Faust and Wright, 2013; Huber et al. 2023). Moreover, due to the lead-lag relationship in the Phillips curve model, Chletsos et al. (2016), McKnight et al. (2020), and Bańbura and Bobeica (2023) forecast inflation based on the Phillips curve. Recently, advanced machine learning (ML) technology has been introduced to inflation forecasting. For example, Medeiros et al. (2021), Aras and Lisboa (2022), and Araujo and Gaglianone (2023) demonstrate the advantages of the ML model for predicting inflation in the United States, Turkey and Brazil, respectively; Rodríguez-Vargas (2020) uses two variants of k nearest neighbour, random forest, extreme gradient enhancement, and long short-term memory (LSTM) networks to evaluate inflation forecasts in Costa Rica.

Some novel factors have also been introduced in research on inflation. For example, Chen et al. (2014) introduce commodity price aggregates to inflation forecasts. Bec and De Gaye (2016) and Balcilar et al. (2017) incorporate metal price series and oil price forecast errors in predictive models for inflation and argue that such additions benefit inflation forecasting. Aparicio and Bertolotto (2020) combine online price indices and inflation and show that online price indices can forecast inflation well. Clements and Reade (2020), Rambaccussing and Kwiatkowski (2020), Mazumder (2021), and Simionescu (2022) investigate inflation from the perspective of behavioural finance, i.e., investor sentiment; however, the results seem contradictory. As the prices of agricultural products are important components of the whole price level, researchers have introduced agricultural products to inflation forecasts (Tule et al. 2019; Fasanya and Awodimila, 2020). Some factors that seem to be almost impossible to relate to inflation, such as climate variables and carbon market returns, have also been shown to significantly improve the accuracy of inflation forecasts (Boneva and Ferrucci, 2022; Xu et al. 2023). The list is far from exhaustive and exemplifies how active the field of connecting novel factors and inflation has been in recent years.

Behavioural finance has been shown to be an important factor in diverse financial and economic aspects and has become a research hotspot exhibiting numerous academic achievements in recent years (Adra and Barbopoulos, 2018; Audrino et al. 2020). Current investigations are based on two main aspects. The first focus relies on investor sentiments. For example, Fu et al. (2015) derive a sentiment-adjusted Markowitz efficient frontier; Kim and Ryu (2021) argue that investor sentiment is a determinant of investors’ trading decisions and behaviours; and Shen et al. (2023) investigate the effect of investor sentiment on new energy stock returns as well as value at risks (VaR) before and during COVID-19. Ryu et al. (2023) investigate the effects of sentiment on mispricing. Bashir et al. (2024) reveal a positive significant relation between stock price crash risk and investor sentiment. Another focus is investor attention. For example, Vozlyublennaia (2014) and Zhang et al. (2021) argue that investor attention can not only explain but also accurately forecast the stock market. Taking investor attention as a common financial variable, Han et al. (2018) and Wu et al. (2019) prove the importance of investor attention in the foreign exchange market, and Li et al. (2019), Chen et al. (2020), Zhang et al. (2022), Zhou et al. (2022), and Zhou et al. (2023) argue that investor attention matters in the crude oil market, internet financial market, commodity futures market and carbon market, respectively. Investor attention has also been proven to be an important pricing factor in the cryptocurrency market (Ibikunle et al. 2020; Zhu et al. 2021; Smales, 2022; Wan et al. 2023). Recently, investor attention and corporate ESG performance have been combined, and the results indicate that investor attention can significantly improve the ESG standards of listed companies (Zhang and Zhang, 2024). Contagion spillover based on investor attention has also been studied by scholars. For example, Li (2024) investigates the role of investor attention on the price of petroleum products (APPP) in forecasting Chinese stock market volatility.

As seen above, several novel factors are extending to research on inflation. However, relevant investigations are quite limited. Behavioural finance has developed rapidly and has shown to be important in finance and economics. On the one hand, investor sentiment, generated from behavioural finance, shows different empirical results regarding inflation. On the other hand, no investigation has attempted to link investor attention and inflation despite the fact that the two issues are naturally connected. This research gap sparks our interest in exploring the role of investor attention in inflation determination. Thus, in this paper, these connections are comprehensively researched. Specifically, this paper investigates inflation explaining and forecasting from the perspective of investor attention to enrich understanding in both behavioural finance and macroeconomics.

Data

This paper selects the Google Search Volume Index (GSVI) from Google Trends to represent novel investor attention rather than other indicators, i.e., extreme return, abnormal trading volume, advertising expenditure, and media coverage, as GSVI shows advantages in terms of timeliness and information comprehensiveness (Zhang et al. 2022). As we aim to analyze the connection between investor attention and inflation in the United States, we set the search area to ‘America’ and directly searched for the keyword ‘inflation’ from the beginning of the GSVI in January 2004 to July 2020 to obtain data on monthly investor attention. For inflation, this paper chooses the consumer price index (CPI) inflation, as this indicator has a relatively high frequency and sufficient data for empirical investigation at a monthly frequency (Liu and Smith, 2014). Specifically, this study chooses the seasonally adjusted monthly CPI inflation for all urban consumers; as this indicator is officially more useful, we downloaded the related data freely from the Federal Reserve Economic Data. All the two series are transferred to logarithmic differences and are named with \({{Att}}_{t}\) and \({{Inf}}_{t}\) for further empirical research.

Some basic information on investor attention (\({{Att}}_{t}\)) and the CPI inflation rate (\({{Inf}}_{t}\)) is shown in Fig. 1 and Table 1, respectively. As shown in Table 1, the mean CPI inflation rate is positive, while the mean investor attention is negative, suggesting that investor attention and the inflation rate may be negatively connected. Furthermore, as we aim to analyse the selected data under the framework of the VAR model, an ADF-KPSS-PP joint stationary test is implemented to avoid the pseudo-regression phenomenon. The results show that the time series for the inflation rate or investor attention is stationary and can be directly used for VAR modelling. In addition, as shown in Fig. 1, the extreme value of the CPI inflation rate always appears after the peak value in investor attention, which may further imply that investor attention affects the inflation rate. From both Fig. 1 and Table 1, it is obvious that the time series for investor attention fluctuates more than that for the inflation rate.

Variation of investor attention and actual inflation from January 2004 to July 2020.

In this paper, as we analyze inflation explaining and forecasting, the full sample is divided into two parts. The first part, from January 2004 to August 2016, is used as an in-sample period for inflation explained through investor attention, and the remaining period, from September 2016 to July 2020, is used for out-of-sample forecasting.

Methodologies

VAR and Granger causality test

The VAR model is a linear model that allows the variables to be depicted by several lagged indicators and is widely used in exploring the dynamic connections between financial variables (Guidolin and Hyde, 2012; Zhang and Lin, 2019). Thus, this paper adopts the widely used VAR model to explore the relationships between investor attention and the CPI inflation rate. Specifically, the VAR model used in this paper is specified by Eqs. (1) and (2) as follows:

where \({{Inf}}_{t}\) represents the inflation rate at time \(t\), \({{Att}}_{t}\) refers to the current investor attention, n is the lag length for the VAR model, and \((t-i)\) represents the operator for the time lag. The linear Granger causality test examines the joint significance of all the lagged terms of one variable in a certain equation in the framework of the VAR model. Specific to the above VAR model represented by Eqs. (1) and (2), the interested Granger causality test is to determine whether the coefficients of (\({\beta }_{11},\ldots ,{\beta }_{n1}\)) are jointly equal to 0. Specifically, the significance of the Chi-square (\({\chi }^{2}\)) statistic is used to evaluate the results of the Granger causality test.

Linear regression models for inflation explanation and forecasting

As documented by previous studies, the oil market is a crucial external factor in inflation determination (Bec and De Gaye, 2016). Thus, in this paper, we control for non-negligible factors in the regression model to fully understand the role of investor attention in inflation. Specifically, according to Aparicio and Bertolotto (2020) and Zhou et al. (2023), the factor is introduced to the regression model based on the VAR model. The detailed regression model is shown in Eq. (3). Notably, the regression model incorporates the interaction terms between investor attention and the oil market as well:

where \({{oil}}_{t-i}\) represents the lagged oil market return and \({{Att}}_{t-i}\times {{oil}}_{t-i}\) represents the lagged interaction term between investor attention and the oil market return. As Eqs. (1) and (3) contain the ‘lead-lag’ relationship between the inflation rate and other variables, this paper extends these two equations and introduces the following out-of-sample forecasting models in Eqs. (4) and (5):

where \(\widehat{{{Inf}}_{t}}\) is the predicted inflation rate. To accurately forecast the inflation rate, in this study, the rolling window forecasting method is selected. In other words, in the case of out-of-sample forecasting, the window size remains fixed when the estimation window rolls forwards (Zhou et al. 2022, Zhou et al. 2023).

Forecasting evaluation for out-of-sample data

In this paper, as we explore the role of investor attention in inflation forecasting, several evaluation indicators must be introduced. Following previous studies (Zhou et al. 2022; Zhou et al. 2023), this paper compares and assesses the accuracy of different predictive models by calculating the out-of-sample R squared (\({R}_{{oos}}^{2}\)), mean squared forecast error (MSFE), and MSFE-adjusted statistics. \({R}_{{oos}}^{2}\) is obtained by Eq. (6):

where T is the length of the full sample and \(t\) is the size of the rolling window. \({{Inf}}_{k}\) is the actual inflation rate. \(\hat{{{Inf}}_{k}}\) represents the forecasted value of the inflation rate from the predictive model. \(\widehat{{{Inf}}_{k}}\) denotes the predicted inflation rate of the benchmark forecasting model. A positive \({R}_{{oos}}^{2}\) indicates that the predictive model outperforms the benchmark model. Commonly, benchmark forecasts of inflation are obtained by three methods, i.e., forecasts from the autoregression model (AR), random walk (RW) model and Federal Reserve Greenbook (Adebiyi, 2007; Álvarez-Díaz and Gupta, 2016; Rossi and Sekhposyan, 2016). In this paper, we do not select the Federal Reserve’s Greenbook despite the fact that the forecast is made by the experts of monetary policy authority. The reason is as follows. The estimations of the Federal Reserve’s Greenbook are released to the public with a 5-year delay; if we choose the indicator as the benchmark, given the appearance of the GSVI in 2004, the selection may cause the data to be outdated and the sample size to be small. Thus, the remaining two models, i.e., AR and RW, are selected as the benchmarks. The MSFE can be obtained from Eq. (7):

Based on MSFE, Clark and McCracken (2001) developed the MSFE-adjusted statistic. The MSFE-adjusted statistic can further identify whether the out-of-sample forecasts are significant. Specifically, the MSFE-adjusted statistic is measured by Eq. (8):

where \({{MSFE}}_{a}\) and \({{MSFE}}_{b}\) denote the MSFE statistics of the predictive model and the benchmark model, respectively. \(\hat{{{Inf}}_{k,a}}\) and \(\hat{{{Inf}}_{k,b}}\) represent the forecast values of the inflation rate from the predictive model and the benchmark model, respectively.

Empirical results

Explanation of inflation

The basic empirical process shows that the optimal lag length in the VAR model is 1. In other words, setting the lag length to 1 is sufficient to ensure the stability of the VAR model. Based on this lag length, this paper estimates the VAR model and implements the corresponding Granger causality test for the in-sample period. The related estimation results are shown in Table 2. To further illustrate the stability of the VAR model, the AR root test is implemented, and the results are shown in Fig. 2. The AR root test shows that all the characteristic roots are in the unit circle, indicating that the established VAR model has good stability.

A graphic description of the AR root test under the framework of VAR(1) model.

Two interesting discoveries are shown in Table 2. First, current investor attention on inflation indeed has a negative impact on the inflation rate in the next observation period, as the value of \({{Att}}_{t-1}\) in the equation for the inflation rate in the VAR model is significantly negative. Second, the results from the Granger causality test show that investor attention to inflation does indeed Granger cause changes in the inflation rate. The VAR model allows researchers to understand the inflation rate’s reaction to the shock from investor attention under the framework of the impulse response function (IRF). Thus, this paper implements the related impulse response analysis and shows the results in Figs. 3, 4. As shown in Fig. 3, once the inflation receives one unit shock from investor attention, the impact may last approximately 7 months.

Response of inflation rate to investor attention from January 2004 to August 2016 under VAR model.

Response of investor attention to the inflation rate from January 2004 to August 2016 under VAR model.

Equation (3) controls for the factor of the oil market and reinvestigates the relationship between investor attention and the inflation rate. According to Wang et al. (2023), the Brent oil futures market is an important market in the global oil market. Thus, this paper collects the returns of Brent oil futures to represent the oil market. The estimation results of Eq. (3) are shown in Table 3. As shown, after controlling for the oil market factor in the last observation period, investor attention still has a significant negative impact on the current inflation rate.

In summary, investor attention has a negative impact on the inflation rate. This phenomenon may be attributed to the following reasons. First, when investor attention on inflation increases, a society may suffer from inflation in the current period, which may indicate that the public is concerned with currency devaluation in the future (Borensztein and De Gregorio, 1999). Therefore, investors may increase expenditures in the current period by converting paper money to commodities to purchase more products with the same amount of money. Thus, in the next period, total consumption demand in a society may decrease. According to the basic theory of demand and supply in macroeconomics, the price level will decrease in the next observation period. Thus, the inflation rate decreases. Second, according to the investor recognition hypothesis and limited attention theory (Merton, 1987), investors are aware of only a subset of the available assets in informationally incomplete markets; for neglected assets, a return premium is needed. Thus, investor attention should be negatively connected with asset returns. In addition, numerous investigations have empirically documented that an increase in investor attention is followed by a decrease in returns (Smales, 2021; Piñeiro-Chousa et al. 2020). This result implies that prices are decreasing; in other words, the price decreases, resulting in a negative correlation between investor attention and the inflation rate. The results on the significance of investor attention further demonstrate the importance in macroeconomics of considering not only traditional factors but also investor psychology and behaviour when investigating variations in the inflation rate.

All the above analyses show that investor attention has excellent explanatory power regarding the macro inflation rate. Furthermore, due to their significant explanatory power, the results can help authorities guide public attention to stabilize the inflation rate. However, this remarkable explanatory power is not enough to illustrate the crucial role of investor attention in inflation determination, as Welch and Goyal (2008) argue that out-of-sample tests seem to be more precise. Thus, the role of investor attention in inflation determination deserves further investigation. It is also worthwhile to explore whether investor attention can be used to forecast the inflation rate in the out-of-sample period. We show these results in the subsequent subsection.

Inflation forecasting

This paper first implements short-horizon forecasting to explore the predictive power of investor attention for the inflation rate, similar to the findings of numerous studies (Zhu et al. 2021; Zhang et al. 2022; Zhou et al. 2022; Zhou et al. 2023). Specifically, this paper forecasts the inflation rate for the next month based on current information about the inflation rate and investor attention. We set the lag length of the AR benchmark model to 1, as other lag lengths do not show an advantage in forecasting (Aparicio and Bertolotto, 2020). The out-of-sample forecasts are implemented based on Eqs. (4) and (5), and the accuracy evaluation is presented in Table 4. As shown in Table 4, the predictive models with investor attention significantly outperform the two benchmark models in all cases, as all the \({R}_{{oos}}^{2}\) values are greater than 0.05 and the MSFE-adjusted statistics are significant.

The above results indicate that investor attention is a nonnegligible factor in inflation determination, as investor attention can be used to explain and forecast inflation. However, as Zhou et al. (2023) note, models that work well for short-horizon forecasts may not perform well for long-horizon forecasts. Thus, it is also useful to explore whether investor attention can be used to forecast inflation over long horizons. Inspired by Zhu et al. (2021), Zhou et al. (2022) and Zhou et al. (2023), we implement relevant investigations. Specifically, we forecast the inflation rate two or three months ahead and compare the forecast performance with that of the AR (1) and RW benchmark models. The results are presented in Table 5. As shown, in the long-horizon forecasts, the predictive models incorporating investor attention significantly outperform the AR (1) and RW benchmark models, as all the \({R}_{{oos}}^{2}\) values are larger than 0 and the MSFE-adjusted statistics are significant. The empirical results for long-horizon forecasts further confirm the importance of investor attention to inflation.

Robustness checks

The above results demonstrate the important role of investor attention in inflation. However, the results are obtained through investor attention on certain keywords of ‘inflation’ and variable or certain model specifications, which may lack the necessary rigor for an academic research paper. Thus, this paper implements two robustness checks. The first check is to update investor attention with other keywords searched by Google Trends. The second check is to alter the variable or model specifications. The related robustness checks are shown in the following subsections.

Update keywords

We search for another keyword, ‘monetary policy’, which is implemented by the central bank and is closely related to inflation. Based on the two keywords ‘inflation’ and ‘monetary policy’, we reperformed all the above empirical investigations to test our empirical results that investor attention can explain and forecast inflation. The estimation results are shown in Table 6 and Table 7.

As shown in Table 6, investor attention still has a negative impact on inflation and is still the Granger cause of inflation. In other words, the conclusion that investor attention can explain the inflation rate does not change.

Table 7 shows several interesting findings. First, if the RW model is selected as the benchmark model, both predictive models can outperform the benchmarks. Second, if the AR (1) model were selected as the benchmark, the forecasting results would vary. If the GSVI is represented by the sum of inflation and monetary policy, the predictive model can outperform the benchmark model; furthermore, the forecast accuracy is even greater than the results shown in Table 4 and Table 5. However, if the GSVI is represented by monetary policy, the predictive models perform worse than the benchmark. In summary, Table 7 shows that updating the search term does not change the conclusion that the GSVI is a crucial factor in inflation determination.

Update model specifications

In this section, the variables and model specifications used to illustrate the impacts of investor attention on the inflation rate are adjusted to ensure adequate rigor for an academic research paper. Specifically, we make three changes. The first modification involves adding another control variable, i.e., the real interest rate, as the real interest rate is also an important factor in explaining inflation (Lanne, 2006). We collect real interest rate data from Federal Reserve Economic Data and update the model specification as follows in Eqs. (9) and (10). The second modification is to consider the higher moment of investor attention, as high-order moments are proven to be crucial factors for financial variables (Zhou et al. 2022). The model specification is shown in Eq. (11). The third modification involves changing the regression model to an interactive model according to Vozlyublennaia (2014); the model specification is shown in Eqs. (12)-(13).

The detailed regression results of the above equations are provided in Table 8. As shown in Table 8, the coefficient for investor attention is still significantly negative. Thus, we may conclude that changes in the model specification do not change our conclusion that investor attention has excellent explanatory power for inflation. In summary, the robustness checks in subsections 6.1 and 6.2 do not change our conclusion that investor attention has a nonnegligible influence on the inflation rate. Thus, H1 and H2 hold.

Further discussion: investor attention and inflation expectations

Investor attention reflected by searching is a key step in obtaining information to form inflation expectations in the current society, and inflation expectations are a crucial factor for determining actual inflation under the NKPC (Friedman, 1968; Chen and Lo, 2019; Larsen et al. 2021). Thus, it is natural to link investor attention and inflation expectations to better understand the impact of investor attention on inflation. However, relevant studies are lacking. This paper collects data on inflation expectations made by the University of Michigan, which is a survey-based inflation expectation and has been widely used in previous studies (Luoma and Luoto, 2009; Malmendier and Nagel, 2016). The measurement of inflation expectations has several advantages. For example, the survey covers a wide range of daily life for American households and can be used to evaluate the dynamics of inflation expectations and potential consumption in the future. In addition, the measurement is considered the most representative indicator of inflation and consumer behaviour. This paper visualizes the connection between investor attention and inflation expectations in Eq. (14). The model specification is based on the following considerations. According to Friedman (1968), during the formation of inflation expectations, information processing takes a certain amount of time; thus, time lags are introduced. Information processing capabilities vary for individuals; considering the sample of our dataset, twelve lags are introduced.

In Eq. (14), \({{Exp}}_{t}\) refers to the inflation expectation, \({Att}\) is the operator for investor attention, and i is the time lag. We estimate Eq. (14) and show the results in Table 9. As shown below, the coefficients for investor attention are significant. However, these results are not sufficient to conclude that investor attention affects inflation expectations, as investor attention is regarded as a financial time series and potential multicollinearity exists. Thus, this paper further implements a variance inflation factor (VIF) test, and the results are shown in Table 10. According to Table 10, the regression model does not have serious multicollinearity problems because the values for the VIF tests are smaller than the commonly used criteria, i.e., 5. Thus, the results in Table 9 are significant, investor attention is a crucial external factor for inflation expectations, and H3 is supported.

Conclusions

The novelty of this paper is its confirmation of the important role of investor attention in inflation, which broadens the research fields of both behavioural finance and macroeconomics. The empirical process and results can be summarized as follows. First, we select several linear model specifications to conclude that investor attention and inflation are negatively connected. Second, we extend models of inflation explaining out-of-sample forecasts. The empirical results show that predictive models that incorporate investor attention can outperform the AR (1) and RW benchmark models in both short and long horizons. Third, this paper implements robustness checks, and investor attention can still explain and forecast inflation. Fourth, this paper proves that investor attention affects inflation through inflation expectations. In summary, investor attention matters in inflation determination.

The results shed light on several perspectives. For example, on the one hand, central banks may guide public opinions to control inflation to some extent; on the other hand, economic participants may adopt simple models to forecast inflation to avoid potential losses. However, deficiencies exist. First, adopting sophisticated models to further test the linear or nonlinear roles of investor attention is of interest. Second, this paper constructs a linear regression model for inflation expectation and investor attention. The information process is complex, and a linear model may not be applicable, considering alternative models and cumulative values of investor attention are also interesting issues. At a minimum, the two abovementioned deficiencies deserve further investigation.

Data availability

The search volume for “inflation” is retrieved from: https://trends.google.com/trends/explore?date=2004-01-01%202020-07-31&geo=US&q=inflation&hl=en-US. The search volume for “monetary policy” is retrieved from: https://trends.google.com/trends/explore?date=2004-01-01%202020-07-31&geo=US&q=monetary%20policy&hl=en-US. The data for consumer price index is retrieved from: https://fred.stlouisfed.org/series/CPIAUCSL. The data for Brent oil return is retrieved from: https://cn.investing.com/commodities/brent-oil-historical-data. The data for real interest rate is retrieved from: https://fred.stlouisfed.org/series/REAINTRATREARAT1MO. The data for inflation expectation is retrieved from: https://fred.stlouisfed.org/series/MICH.

References

Adebiyi MA (2007) Does money tell us anything about inflation in Nigeria? Singapore Econ Rev 52(01):117–134. https://doi.org/10.1142/S0217590807002592

Adra S, Barbopoulos LG (2018) The valuation effects of investor attention in stock-financed acquisitions. J Empir Finance 45:108–125. https://doi.org/10.1016/j.jempfin.2017.10.001

Altissimo F, Mojon B, Zaffaroni P (2009) Can aggregation explain the persistence of inflation? J Monet Econ 56(2):231–241. https://doi.org/10.1016/j.jmoneco.2008.12.013

Álvarez-Díaz M, Gupta R (2016) Forecasting US consumer price index: does nonlinearity matter? Appl Econ 48(46):4462–4475. https://doi.org/10.1080/00036846.2016.1158922

Almosova A, Andresen N (2023) Nonlinear inflation forecasting with recurrent neural networks. J Forecast 42(2):240–259. https://doi.org/10.1002/for.2901

Ang A, Bekaert G, Wei M (2007) Do macro variables, asset markets, or surveys forecast inflation better? J Monet Econ 54(4):1163–1212. https://doi.org/10.1016/j.jmoneco.2006.04.006

Aparicio D, Bertolotto MI (2020) Forecasting inflation with online prices. Int J Forecast 36(2):232–247. https://doi.org/10.1016/j.ijforecast.2019.04.018

Aras S, Lisboa PJ (2022) Explainable inflation forecasts by machine learning models. Expert Syst Appl 207:117982. https://doi.org/10.1016/j.eswa.2022.117982

Araujo GS, Gaglianone WP (2023) Machine learning methods for inflation forecasting in Brazil: New contenders versus classical models. Latin Am J Cent Bank 4(2):100087. https://doi.org/10.1016/j.latcb.2023.100087

Audrino F, Sigrist F, Ballinari D (2020) The impact of sentiment and attention measures on stock market volatility. Int J Forecast 36(2):334–357. https://doi.org/10.1016/j.ijforecast.2019.05.010

Balcilar M, Katzke N, Gupta R (2017) Do precious metal prices help in forecasting South African inflation? North Am J Econ Finance 40:63–72. https://doi.org/10.1016/j.najef.2017.01.007

Bańbura M, Bobeica E (2023) Does the Phillips curve help to forecast euro area inflation? Int J Forecast 39(1):364–390. https://doi.org/10.1016/j.ijforecast.2021.12.001

Bashir U, Kayani UN, Khan S, Polat A, Hussain M, Aysan AF (2024) Investor sentiment and stock price crash risk: The mediating role of analyst herding. Comput Hum Behav Rep, 100371. https://doi.org/10.1016/j.chbr.2024.100371

Bec F, De Gaye A (2016) How do oil price forecast errors impact inflation forecast errors? An empirical analysis from US, French and UK inflation forecasts. Economic Modelling 53:75–88. https://doi.org/10.1016/j.econmod.2015.11.008

Boneva L, Ferrucci G (2022) Inflation and climate change: the role of climate variables in inflation forecasting and macro modelling. This paper can be achieved at: https://eprints.lse.ac.uk/115533/1/INSPIRE_Sustainable_Central_Banking_Toolbox_Policy_Briefing_Paper_1.pdf

Borensztein E, De Gregorio J (1999) Devaluation and inflation after currency crises. International Monetary Fund, 1-34. This paper can be achieved at: https://www.researchgate.net/publication/245906019_Devaluation_and_Inflation_after_Currency_Crises

Bouras P, Bustamante C, Guo X, Short J (2023) The contribution of firm profits to the recent rise in inflation. Econ Lett 233:111449. https://doi.org/10.1016/j.econlet.2023.111449

Cai H, Jiang Y, Liu X (2022) Investor attention, aggregate limit-hits, and stock returns. Int Rev Financ Anal 83:102265. https://doi.org/10.1016/j.irfa.2022.102265

Canova F, Ferroni F (2012) The dynamics of US inflation: Can monetary policy explain the changes? J Econom 167(1):47–60. https://doi.org/10.1016/j.jeconom.2011.08.008

Chen HY, Lo TC (2019) Online search activities and investor attention on financial markets. Asia Pac Manage Rev 24(1):21–26. https://doi.org/10.1016/j.apmrv.2018.11.001

Chen R, Qian Q, Jin C, Xu M, Song Q (2020) Investor attention on Internet financial markets. Finance Res Lett 36:101421. https://doi.org/10.1016/j.frl.2019.101421

Chen YC, Turnovsky SJ, Zivot E (2014) Forecasting inflation using commodity price aggregates. J Econom 183(1):117–134. https://doi.org/10.1016/j.jeconom.2014.06.013

Chen Q, Zhu H, Yu D, Hau L (2022) How does investor attention matter for crude oil prices and returns? Evidence from time-frequency quantile causality analysis. N Am J Econ Finance 59:101581. https://doi.org/10.1016/j.najef.2021.101581

Chletsos M, Drosou V, Roupakias S (2016) Can Phillips curve explain the recent behavior of inflation? Further evidence from USA and Canada. J Econ Asymmetr 14:20–28. https://doi.org/10.1016/j.jeca.2016.07.005

Choi Y (2021) Inflation dynamics, the role of inflation at different horizons and inflation uncertainty. Int Rev Econ Finance 71:649–662. https://doi.org/10.1016/j.iref.2020.10.004

Ciccarelli M, Mojon B (2010) Global inflation. Rev Econ Stat 92(3):524–535. https://doi.org/10.1162/REST_a_00008

Clark TE, McCracken MW (2001) Tests of equal forecast accuracy and encompassing for nested models. J Econom 105(1):85–110. https://doi.org/10.1016/S0304-4076(01)00071-9

Clements MP, Galvão AB (2013) Forecasting with vector autoregressive models of data vintages: US output growth and inflation. Int J Forecast 29(4):698–714. https://doi.org/10.1016/j.ijforecast.2011.09.003

Clements MP, Reade JJ (2020) Forecasting and forecast narratives: The Bank of England inflation reports. Int J Forecast 36(4):1488–1500. https://doi.org/10.1016/j.ijforecast.2019.08.013

Coibion O, Gorodnichenko Y (2015) Is the Phillips curve alive and well after all? Inflation expectations and the missing disinflation. Am Econ J: Macroecon 7(1):197–232. https://doi.org/10.1257/mac.20130306

Croushore D (2010) An evaluation of inflation forecasts from surveys using real-time data. The BE J Macroecon, 10(1). https://doi.org/10.2139/ssrn.940418

Effah Nyamekye G, Adusei Poku E (2017) What is the effect of inflation on consumer spending behaviour in Ghana? This paper can be achieved at: https://mpra.ub.uni-muenchen.de/81081/1/MPRA_paper_81081.pdf

Eickmeier SZiegler C (2008) How successful are dynamic factor models at forecasting output and inflation? A meta‐analytic approach. J Forecast 27(3):237–265. https://doi.org/10.1002/for.1056

Fama EF (1975) Short-term interest rates as predictors of inflation. The American Economic Review, 65(3), 269-282. This paper can be achieved at: http://www.ressources-actuarielles.net/EXT/ISFA/1226.nsf/8d48b7680058e977c1256d65003ecbb5/38019a3264b83e49c125751e0055f911/$FILE/Mod%C3%A8le%20de%20Fama%20pour%20l’inflation.pdf

Faust J, Wright JH (2013) Forecasting inflation. Handbook of Economic Forecasting 2013 2:2–56. 10.1016/B978-0-444-53683-9.00001-3

Fasanya IO, Awodimila CP (2020) Are commodity prices good predictors of inflation? The African perspective. Resources Policy 69:101802. https://doi.org/10.1016/j.resourpol.2020.101802

Forni M, Hallin M, Lippi M, Reichlin L (2003) Do financial variables help forecasting inflation and real activity in the Euro area? J Monet Econ 50(6):1243–1255. https://doi.org/10.1016/S0304-3932(03)00079-5

Forbes K, Kirkham L, Theodoridis K (2021) A trendy approach to UK inflation dynamics. Manchester School 89:23–75. https://doi.org/10.1111/manc.12293

Friedrich C (2016) Global inflation dynamics in the post-crisis period: What explains the puzzles? Econ Lett 142:31–34. https://doi.org/10.1016/j.econlet.2016.02.032

Friedman M (1968) The role of monetary policy. Am Econ Rev 58:1–17. https://doi.org/10.1007/978-1-349-24002-9_11

Fu C, Jacoby G, Wang Y (2015) Investor sentiment and portfolio selection. Finance Res Lett 15:266–273. https://doi.org/10.1016/j.frl.2015.11.004

Guidolin M, Hyde S (2012) Can VAR models capture regime shifts in asset returns? A long-horizon strategic asset allocation perspective. J Bank Finance 36(3):695–716. https://doi.org/10.1016/j.jbankfin.2011.10.011

Hakkio CS (2009) Global inflation dynamics. Federal Reserve Bank of Kansas City Working Paper. https://doi.org/10.2139/ssrn.1335348

Hall SG, Tavlas GS, Wang Y (2023) Forecasting inflation: The use of dynamic factor analysis and nonlinear combinations. J Forecast 42(3):514–529. https://repec.cal.bham.ac.uk/pdf/22-12.pdf

Han L, Wu Y, Yin L (2018) Investor attention and currency performance: International evidence. Appl Econ 50(23):2525–2551. https://doi.org/10.1080/00036846.2017.1403556

Hauzenberger N, Huber F, Klieber K (2023) Real-time inflation forecasting using non-linear dimension reduction techniques. Int J Forecast 39(2):901–921. https://doi.org/10.1016/j.ijforecast.2022.03.002

Huber F, Onorante L, Pfarrhofer M (2023) Forecasting euro area inflation using a huge panel of survey expectations. Int J Forecast. https://doi.org/10.1016/j.ijforecast.2023.09.003

Ibikunle G, McGroarty F, Rzayev K (2020) More heat than light: Investor attention and bitcoin price discovery. Int Rev Financ Anal 69:101459. https://doi.org/10.1016/j.irfa.2020.101459

Kim K, Ryu D (2021) Does sentiment determine investor trading behaviour? Appl Econ Lett 28(10):811–816. https://doi.org/10.1080/13504851.2020.1782331

Larsen VH, Thorsrud LA, Zhulanova J (2021) News-driven inflation expectations and information rigidities. J Monet Econ 117:507–520. https://doi.org/10.1016/j.jmoneco.2020.03.004

Lanne M (2006) Nonlinear dynamics of interest rate and inflation. J Appl Econom 21(8):1157–1168. https://doi.org/10.1002/jae.908

Li S, Zhang H, Yuan D (2019) Investor attention and crude oil prices: Evidence from nonlinear Granger causality tests. Energy Econ 84:104494. https://doi.org/10.1016/j.eneco.2019.104494

Li D (2024) Forecasting stock market realized volatility: The role of investor attention to the price of petroleum products. Int Rev Econ Finance 90:115–122. https://doi.org/10.1016/j.iref.2023.11.015

Liu TY, Ma JT (2023) Exchange rate and inflation between China and the United States: A bootstrap rolling-window approach. Econ Syst, 101152. https://doi.org/10.1016/j.ecosys.2023.101152

Liu Y, Niu Z, Suleman MT, Yin L, Zhang H (2022) Forecasting the volatility of crude oil futures: The role of oil investor attention and its regime switching characteristics under a high-frequency framework. Energy 238:121779. https://doi.org/10.1016/j.energy.2021.121779

Liu D, Smith JK (2014) Inflation forecasts and core inflation measures: Where is the information on future inflation? Q Rev Econ Finance 54(1):133–137. https://doi.org/10.1016/j.qref.2013.07.006

Luoma A, Luoto J (2009) Modelling the general public’s inflation expectations using the Michigan survey data. Appl Econ 41(10):1311–1320. https://doi.org/10.1080/00036840701604339

Malmendier U, Nagel S (2016) Learning from inflation experiences. Q J Econ 131(1):53–87. https://doi.org/10.1093/qje/qjv037

Marcellino M, Stock JH, Watson MW (2003) Macroeconomic forecasting in the euro area: Country specific versus area-wide information. Eur Econ Rev 47(1):1–18. https://doi.org/10.1016/S0014-2921(02)00206-4

Mavroeidis S, Plagborg-Møller M, Stock JH (2014) Empirical evidence on inflation expectations in the New Keynesian Phillips Curve. Am Econ J: J Econ Lit 52(1):124–188. https://doi.org/10.1257/jel.52.1.124

Mazumder S (2021) The reaction of inflation forecasts to news about the Fed. Econ Model 94:256–264. https://doi.org/10.1016/j.econmod.2020.09.026

McKnight S, Mihailov A, Rumler F (2020) Inflation forecasting using the New Keynesian Phillips Curve with a time-varying trend. Econ Model 87:383–393. https://doi.org/10.1016/j.econmod.2019.08.011

Medeiros MC, Vasconcelos GF, Veiga Á, Zilberman E (2021) Forecasting inflation in a data-rich environment: the benefits of machine learning methods. J Bus Econ Stat 39(1):98–119. https://doi.org/10.1080/07350015.2019.1637745

Merton RC (1987) A simple model of capital market equilibrium with incomplete information. Available at: https://dspace.mit.edu/bitstream/handle/1721.1/2166/SWP-1869-18148074.pdf

Monacelli T, Sala L (2009) The international dimension of inflation: Evidence from disaggregated consumer price data. J Money Credit Bank 41:101–120. https://doi.org/10.1111/j.1538-4616.2008.00200.x

Mumtaz H, Surico P (2012) Evolving international inflation dynamics: world and country-specific factors. J Eur Econ Assoc 10(4):716–734. https://doi.org/10.1111/j.1542-4774.2012.01068.x

Murphy RG (2014) Explaining inflation in the aftermath of the Great Recession. J Macroecon 40:228–244. https://doi.org/10.1016/j.jmacro.2014.01.002

Nakamura E (2005) Inflation forecasting using a neural network. Econ Lett 86(3):373–378. https://doi.org/10.1016/j.econlet.2004.09.003

Piñeiro-Chousa J, López-Cabarcos MÁ, Ribeiro-Soriano D (2020) Does investor attention influence water companies’ stock returns? Technol Forecast Soc Change 158:120115. https://doi.org/10.1016/j.techfore.2020.120115

Rambaccussing D, Kwiatkowski A (2020) Forecasting with news sentiment: Evidence with UK newspapers. Int J Forecast 36(4):1501–1516. https://doi.org/10.1016/j.ijforecast.2020.04.002

Rossi B, Sekhposyan T (2016) Forecast rationality tests in the presence of instabilities, with applications to Federal Reserve and survey forecasts. J Appl Econom 31(3):507–532. https://doi.org/10.1002/jae.2440

Rodríguez-Vargas A (2020) Forecasting Costa Rican inflation with machine learning methods. Latin Am J Cent Bank 1(1-4):100012. https://doi.org/10.1016/j.latcb.2020.100012

Ryu D, Ryu D, Yang, H (2023) Investor sentiment and futures market mispricing. Finance Res Lett, 58, https://doi.org/10.1016/j.frl.2023.104559

Simionescu M (2022) Econometrics of sentiments-sentometrics and machine learning: The improvement of inflation predictions in Romania using sentiment analysis. Technol Forecast Soc Change 182:121867. https://doi.org/10.1016/j.techfore.2022.121867

Smales LA (2022) Investor attention in cryptocurrency markets. Int Rev Financ Anal 79:101972. https://doi.org/10.1016/j.irfa.2021.101972

Shen Y, Liu C, Sun X, Guo K (2023) Investor sentiment and the Chinese new energy stock market: A risk–return perspective. Int Rev Econ Finance 84:395–408. https://doi.org/10.1016/j.iref.2022.11.035

Smales LA (2021) Investor attention and global market returns during the COVID-19 crisis. Int Rev Financ Anal 73:101616. https://doi.org/10.1016/j.irfa.2020.101616

Szafranek K (2019) Bagged neural networks for forecasting Polish (low) inflation. Int J Forecast 35(3):1042–1059. https://doi.org/10.1016/j.ijforecast.2019.04.007

Tillmann P (2024) The asymmetric effect of supply chain pressure on inflation. Econ Lett, 111540. https://doi.org/10.1016/j.econlet.2024.111540

Tule MK, Salisu AA, Chiemeke CC (2019) Can agricultural commodity prices predict Nigeria’s inflation? J Commod Mark 16:100087. https://doi.org/10.1016/j.jcomm.2019.02.002

Vozlyublennaia N (2014) Investor attention, index performance, and return predictability. J Bank Finance 41:17–35. https://doi.org/10.1016/j.jbankfin.2013.12.010

Wan J, Wu Y, Zhu P (2023) The COVID-19 pandemic and Bitcoin: Perspective from investor attention. Front Public Health 11:1147838. https://doi.org/10.3389/fpubh.2023.1147838

Wang S, Feng H, Gao D (2023) Testing for short explosive bubbles: A case of Brent oil futures price. Finance Res Lett 52:103497. https://doi.org/10.1016/j.frl.2022.103497

Welch I, Goyal A (2008) A comprehensive look at the empirical performance of equity premium prediction. Rev Financ Stud 21(4):1455–1508. https://doi.org/10.1093/rfs/hhm014

Wong B (2015) Do inflation expectations propagate the inflationary impact of real oil price shocks?: Evidence from the Michigan survey. J Money Credit Bank 47(8):1673–1689. https://doi.org/10.1111/jmcb.12288

Woodford M, Walsh CE (2005) Interest and prices: Foundations of a theory of monetary policy. Macroecon Dyn 9(3):462–468. https://doi.org/10.1017/S1365100505040253

Wright JH (2009) Forecasting US inflation by Bayesian model averaging. J Forecast 28(2):131–144. https://doi.org/10.1002/for.1088

Wu Y, Han L, Yin L (2019) Our currency, your attention: Contagion spillovers of investor attention on currency returns. Econ Model 80:49–61. https://doi.org/10.1016/j.econmod.2018.05.012

Xu Y, Li X, Yuan P, Zhang Y (2023) Trade-off between environment and economy: The relationship between carbon and inflation. Front Environ Sci 11:334. https://doi.org/10.3389/fenvs.2023.1093528

Yellen JL (2017) Inflation, uncertainty, and monetary policy. Bus Econ 52(4):194–207. https://doi.org/10.1057/s11369-017-0057-x

Zakaria M, Khiam S, Mahmood H (2021) Influence of oil prices on inflation in South Asia: Some new evidence. Resour Policy 71:102014. https://doi.org/10.1016/j.resourpol.2021.102014

Zhang Y, Chen Y, Wu Y, Zhu P (2022) Investor attention and carbon return: Evidence from the EU-ETS. Econ Res-Ekonomska Istraživanja 35(1):709–727. https://doi.org/10.1080/1331677X.2021.1931914

Zhang Y, Chu G, Shen D (2021) The role of investor attention in predicting stock prices: The long short-term memory networks perspective. Finance Res Lett 38:101484. https://doi.org/10.1016/j.frl.2020.101484

Zhang YJ, Lin JJ (2019) Can the VAR model outperform MRS model for asset allocation in commodity market under different risk preferences of investors? Int Rev Financ Anal 66:101395. https://doi.org/10.1016/j.irfa.2019.101395

Zhang Z, Zhang L (2024) Investor attention and corporate ESG performance. Finance Res Lett 60:104887. https://doi.org/10.1016/j.frl.2023.104887

Zhou Q, Zhu P, Wu Y, Zhang Y (2022) Research on the volatility of the cotton market under different term structures: perspective from investor attention. Sustainability 14(21):14389. https://doi.org/10.3390/su142114389

Zhou Q, Zhu P, Zhang Y (2023) Contagion spillover from bitcoin to carbon futures pricing: perspective from investor attention. Energies 16:929. https://doi.org/10.3390/en16020929

Zhu P, Zhang X, Wu Y, Zheng H, Zhang Y (2021) Investor attention and cryptocurrency: Evidence from the Bitcoin market. PLoS One 16(2):e0246331. https://doi.org/10.1371/journal.pone.0246331

Funding

This work was funded by the Key Program of the National Social Science Foundation of China (21ATJ007).

Author information

Authors and Affiliations

Contributions

Panpan Zhu contributed to the “Literature review”, “Data”, “Empirical results” and “Robustness checks” sections. Qingjie Zhou contributed to “Methodologies” and “Further discussion”. Yinpeng Zhang contributed to the conceptional design, “Introduction”, and “Conclusions”. All the authors have read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interest.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

Informed consent was not required as the study did not involve human participants.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Zhu, P., Zhou, Q. & Zhang, Y. Investor attention and consumer price index inflation rate: Evidence from the United States. Humanit Soc Sci Commun 11, 541 (2024). https://doi.org/10.1057/s41599-024-03036-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-03036-y