Abstract

Tax non-compliance is a persistent problem that is becoming increasingly common worldwide. The main objective of this study is to examine the factors that influence voluntary tax compliance among large taxpayers in Ethiopia based on the theoretical foundation of tax compliance. This study used an ordinary logit regression model, a closed-ended questionnaire with 1550 taxpayers, and quantitative data analysis. The regression analysis shows that tax compliance behavior is positively and significantly influenced by government trust, taxpayers’ tax knowledge, tax system fairness, and rewards. However, compliance costs negatively and significantly affect tax compliance. To improve voluntary tax compliance, the government and tax authorities need to be more open and responsible. They must also increase tax awareness among taxpayers through websites, seminars, and the media. Ultimately, they must reduce compliance costs and deliver tangible and intangible benefits to honest taxpayers.

Similar content being viewed by others

Introduction

Even if governments are interested in taxation, the potential tax revenue that countries can generate through their tax policies far exceeds the actual revenue received. In addition to the factors that influence taxpayer behavior and lead to partial tax compliance, the gap between potential revenue and actual revenue is also due to incomplete and ineffective tax administration (Lois et al., 2019; Mebratu et al., 2020).

Tax noncompliance is a persistent problem that is becoming increasingly common worldwide (Kefela and Ghirmai, 2009). Ethiopia is one of the sub-Saharan African countries grappling with issues related to widespread tax evasion, threatening the national tax base of most of these countries. According to Shallo (2018), many factors, including non-compliance with tax regulations, cause low tax collection. Noncompliance with tax regulations generates significant revenue for the Ethiopian government, as many taxpayers do not meet their tax obligations and are prosecuted for not paying taxes on time. The country’s tax system relies heavily on law enforcement to ensure smooth operations, despite government incentives for voluntary compliance (Shallo, 2018).

Tax compliance refers to the willingness of taxpayers to comply with tax laws to achieve an economic balance in a country. It is the process and procedure of convincing taxpayers to comply with the relevant tax laws (Oladipo et al., 2022). On the other hand, tax non-compliance poses a major challenge for many tax authorities, and convincing taxpayers to comply is difficult (James and Alley, 2002). According to the economic deterrence model, taxpayer behavior is influenced by the tax rate, which determines the benefits of tax avoidance, and by the likelihood of detection and the penalty for fraud, which determines the costs of tax avoidance fees (Allingham and Sandmo, 1972). Another compliance theory, the financial exchange theory, suggests that the presence of incentives can promote compliance and that governments can increase compliance by providing products that people prefer in a more effective and accessible way (Cowell and Gordon, 1988). The third type of compliance theory, “social influence,” posits that individuals’ compliance behavior and attitudes toward the tax system are influenced by the behavior and social norms of the individual’s reference group (Snavely, 1990). Comparative treatment theory emphasizes that the fairness and reasonableness of the tax system affect tax compliance behavior (Walsh, 2012). The political accountability model states that tax compliance depends on the degree to which citizens trust their governments (Kirchler et al., 2008b). The theory of planned behavior also suggests that perceived behavioral control depends on beliefs (related to attitudes toward the behavior and subjective norms), that is, controlling beliefs (perceptions about the acquisition of skills, resources, and opportunities (Saad, 2011).

To support a government’s tax policy, a country’s tax system endeavors to collect taxes in an orderly and professional manner. While recent experiences indicate notable progress in certain regions of the world, tax administrations have encountered challenges in achieving this goal. Taxpayer noncompliance is the main cause of developing countries’ difficulties in collecting tax revenues efficiently (Okpeyo et al., 2019b). Tax evasion and avoidance are characteristics of tax violations, defined as the inability to file tax returns, report income, accurately calculate deductions, and make timely payments (Jenkins and Forlemu, 1993). Both tax avoidance and evasion pose substantial economic challenges for a nation. For example, tax avoidance can lead to investment distortions, leading individuals and companies to undervalue their assets, or even exempt some of them from taxation. On the other hand, tax evasion can destroy business morals and ethics as people look for loopholes in the system, which can lead to companies reporting higher dividends and increasing take-home profits (Dalu et al., 2012). Therefore, this would have an adverse impact on the economy and lead to national inflation. One measure that the government or tax authorities take to reduce the rate of tax evasion and compliance is to increase the level of voluntary or forced tax compliance for taxpayers.

Although several studies have been conducted on the factors influencing tax compliance behavior, they have found different results for the same variables. For instance, (Jemberie, 2020; Engida and Baisa, 2014; Assfaw and Sebhat, 2019; and Deyganto, 2018b), conclude that fairness and justice do not have a significant impact on tax compliance behavior. Ademe and Simret (2020) find that fairness, justice, equity, and fairness in the tax system have a significant impact on tax compliance behavior. The researchers mentioned above also found differences in their results when it came to another variable, tax knowledge. For example, Assfaw and Sebhat (2019), Jemberie (2020), and Deyganto (2018b)) identified that tax knowledge significantly influences tax compliance behavior. Tax compliance and knowledge are unrelated, according to the conclusions of Ademe and Simret (2020), who found that tax compliance behavior is not influenced by tax knowledge. Given these inconsistent results, additional research based on different tax compliance theories is required. This study is structured as a theoretical foundation for tax compliance behavior and hypothesis development, research materials, results, and conclusions.

Theoretical foundations of tax compliance behavior and hypothesis development

A variety of factors can influence taxpayers’ attitudes toward tax compliance, subsequently affecting their tax compliance behavior cultural components and other socio-cultural factors; these potential predictors of tax compliance and noncompliance vary across countries (Okpeyo et al. 2019a). Taking this analysis further, Barbuta-Misu (2011) classifies the determinants of tax compliance into three non-economic and seven economic categories. The amount of actual income, tax rate, fines, penalties, tax benefits, and likelihood of a tax audit were considered the seven economic determinants of tax compliance. Non-economic factors include one’s view of the fairness of the tax system; one’s attitude towards taxes; and national, social, and personal norms. However, Palil and Mustapha (2011) argue that the legal system, ethics, and other contextual factors influence tax design to some extent.

Fiscal exchange theory

According to the fiscal exchange theory, governments can improve compliance by providing and spending money on preferred products to citizens in more effective and accessible ways (Cowell and Gordon, 1988). Alm et al. (1992) showed that perceptions of the availability of public goods and services are positively correlated with compliance. Therefore, taxpayers are primarily concerned with what they actually receive in return for paying taxes in the form of public services, that is, consideration. This perspective views taxes and the provision of public goods and services as a type of contract between the government and the people who pay them. People may value the products and services provided by the government and pay taxes because they understand that their contributions are necessary to finance those products and services and to encourage others to do the same (Fjeldstad and Semboja, 2001). Consequently, positive returns can increase the likelihood of voluntary compliance without direct coercion. It follows that a taxpayer’s behavior might depend on how satisfied or dissatisfied he/she is with the terms of his/her contract with the government. If taxpayers believe that the tax system is unfair, they may attempt to change their terms of trade with the government through tax evasion (Helhel and Ahmed, 2014).

Beyond threats, punishments, and detention, incentives are specific actions taken by the government to increase compliance with the law. In addition to monetary benefits, positive incentives can promote qualities such as satisfaction, dignity, sincerity, recognition or identification with others, and a sense of justice or stability (Smith and Stalans, 1991). A specific aspect of tax legislation, known as tax incentives, aims to reward or encourage certain compliant behaviors among taxpayers. Thus, the first hypothesis is as follows:

H1: rewards and incentives have a positive and significant effect on tax compliance behavior.

Social influences- comparative treatment theory

According to social influence theory, an individual’s compliance behavior and attitudes toward the tax system are influenced by the social norms and behavior of their reference group (Snavely, 1990). As with other aspects of behavior, taxes can also be assumed to influence human behavior. A person’s reference group, which includes friends, neighbors, and family, can influence compliance behavior and attitudes towards the tax system. Thus, knowing that several members of significant groups are tax evaders weakens a taxpayer’s commitment to compliance. In addition, people with social connections may be discouraged from committing fraud because they fear the consequences of their cover-up being exposed and made public. Furthermore, Sah (1991) argues that social influences can affect compliance by altering, among other things, the perceived likelihood of detection.

With its foundation in equity theory, the comparative treatment model suggests that better compliance could come from eliminating imbalances in the exchange relationship between taxpayers and government. The relationship between the state and its citizens cannot be viewed as a vacuum involving only both parties. As per Fjeldstad et al. (2012), they could also think about their own relationships with the state before thinking about their fellow citizens. Perceptions of how the government treats them compared to others can significantly influence their views on both peers and the government. If a group is granted preferential treatment by the state, this could affect both the group receiving benefits and the citizens’ relationship with the state. Consequently, the state’s treatment of an individual in relation to the other members of its larger national community is as important as what the individual receives from the state. The way each taxpayer is treated and the relationship between others’ tax burdens and compliance behavior are just two ways the perceived fairness of the tax system influences compliance decisions. According to Walsh (2012), people are more likely to comply if they believe that others around them also pay tax.

Treating equal people matched under equal circumstances is the most understandable requirement for fairness (Jayawardane, 2015). Horizontal and vertical equities, also known as tax equity, are the two main elements of tax equity. While vertical equity suggests that taxpayers who are better off should contribute the same percentage of their income as those who are less well off, horizontal equity supports collecting taxes based on the financial situation (Sahu, 2021). Individuals with different income levels are characterized by vertical equity (Barjoyai, 1987). This allows for the formulation of the second hypothesis.

H2: Fairness in the tax system has a significant and positive effect on tax-compliance behavior.

Political legitimacy theory

Political legitimacy theory suggests that citizens’ trust in their government affects their tax compliance (Kirchler et al., 2008b). Political scientists have studied the processes leading to political legitimacy and civic identification. Legitimacy can be defined as the belief or trust that the government, institutions, and social arrangements are appropriate, just, and fair, and serve the interests of the general public (Fjeldstad et al., 2012). For taxpayers to willingly pay their taxes, trust is crucial (Scholz and Lubell, 1998). Controlled expectations and trust in an uncertain environment are related to the relationship between government and power (Sitardja and Dwimulyani, 2016). When taxpayers who have less trust in the government view events negatively, those who have more trust view events positively (Robinson, 1996). Taxpayers who lack trust in the government are likely to be more skeptical about the use of the tax revenue collected by the government. Taxpayers’ commitment to the tax system and payment of taxes increases when they trust the government (Jimenez and Iyer, 2016b). They also behave differently in terms of their taxes. Thus, the third hypothesis is as follows:

H3: The perception of government trust has a positive and significant effect on tax compliance behavior.

Theory of planed behavior

An influential theory in social psychology that aims to explain people’s behavior is the theory of planned behavior (Bobek and Hatfield, 2003). The theory of rational action that Icek Ajzen and Fishbein (1970) proposed to explain conscious behavior was refined into this theory developed by Icek Ajzen (1991). This idea assumes that certain elements, starting methodically and evolving for various reasons, have an impact on the behavior of people in society. However, a person’s ability to perform a particular behavior depends on their motivation to do so. The three elements of subjective norms, behavioral attitudes, and cognitive behavioral control define the purpose of a behavior (Bobek and Hatfield, 2003). In addition, behavioral, normative, and control beliefs influence the factors listed above (Ajzen, 2002). According to Saad (2011), the theory of planned behavior also suggests that beliefs, that is, control beliefs, are a necessary prerequisite for perceived behavioral control as well as for attitudes toward behavior and subjective standards. As stated by Mathieson (1991), control beliefs are the recognition of the acquisition of opportunities, resources, and capabilities, and the understanding of the importance of these resources in achieving objectives. A person’s ability to control their behavior depends heavily on their skills, expertise, and social support.

One of the factors affecting tax compliance is taxpayers’ ability to understand tax laws and their willingness to comply with them. Tax knowledge refers to the general level of tax knowledge, knowledge of avoidance options, general educational qualifications, or knowledge of tax law (Bornman and Ramutumbu, 2019). A taxpayer’s knowledge of their rights, obligations, and tax payment procedures as well as the consequences of non-compliance is acquired through tax education (Machogu and Amayi, 2016). The authors suggest that taxpayer education can promote a positive attitude toward tax compliance and provide the necessary knowledge to comply with tax laws. This leads to the formulation of the fourth hypothesis.

H4: Tax-payer tax knowledge has a significant and positive effect on tax compliance behavior.

Economic deterrence theory

According to Allingham and Sandmo (1972), the economic deterrence model assumes that a variety of factors, including tax rates, the benefits of tax evasion, the likelihood of fraud being detected, and the severity of penalties for doing so can influence taxpayers’ behavior. Therefore, rational decisions are made amidst uncertainty, where tax evasion can lead to tax savings or penalties (Fjeldstad et al., 2012). As a result, the more likely tax evasion is to be discovered and punished more severely, the fewer people will engage in it. Conversely, when the likelihood of audits is low and fines are minimal, the expected return from evasion is high. According to Helhel and Ahmed (2014), the model predicts significant non-compliance. In certain situations, the fear of being discovered or caught can serve as an effective deterrent to encourage honest behavior. For example, the fear of being caught has been found to be an effective strategy for eliciting truthful behavior, although there is criticism that the model only considers the coercive side of compliance at the expense of consensus. Tax administrations, influenced by the concepts of economic deterrence, have developed enforcement strategies that primarily focus on penalties and fear of detection, as well as the associated time and financial cost, including the burden of the tax payment itself.

The economic costs of taxes include not only the actual tax payment and the associated additional burden but also the time and money spent on tax compliance and tax planning (Blaufus et al., 2011). Your legal and regulatory obligations from tax authorities and laws are referred to as compliance costs. Neither the actual tax payment nor any costs related to tax distortions are included in these expenses (Eragbhe and Modugu, 2014). Compliance costs disappear when taxes are collected. In addition to the costs incurred in obtaining and maintaining the knowledge required for this position, such as understanding legal responsibilities and penalties, this also includes the costs of collecting, disclosing, and filing taxes on the company’s products and income and on the wages and salaries of its employees. Eragbhe and Modugu (2014) divided compliance costs into two categories: tax planning and calculation. To maintain an accurate accounting system, the costs associated with data collection and tax liability calculations are referred to as computational costs. However, when taxpayers attempt to legally reduce or avoid taxes, planning costs increase. This leads to the following hypotheses:

H5: Compliance costs have a negative and significant effect on tax compliance.

Research materials and model specification

The relationship between independent and dependent variables was examined in this study using a quantitative research approach. The target group of the study was 1550 large Ethiopian taxpayers. The primary data collected consisted of questionnaires with five Likert scales adjusted to range from “strongly agree” (SA) = 5 to “strongly disagree” (SD) = 1. The questionnaires were adopted from the works of Nandal, Diksha, and Jaggarwal (2021), Sapiei and Abdullah (2008), and Augustine and Enyi (2020).

Model specification: ordinary logit regression model

The characteristics of the dependent variable typically determine which model is appropriate. The dependent variable in the study determines the voluntary tax compliance of Ethiopian taxpayers and is categorical or ordered. Consequently, the ordered logit model was used to examine the factors influencing voluntary tax compliance behavior, which according to Palil et al. (2013) is divided into low, medium, and high compliance. According to Torres-Reyna (2012), an ordinary Logit regression model is used when a dependent variable includes three or more categories and the values of each category are arranged in a meaningful order. The proportional odds model (POM) is the most commonly used model for ordinal logistic regression (Fuks and Salazar, 2008). To achieve the desired results, the researchers reviewed the variables used in various studies mentioned in the literature review and developed the model as follows.

\(\mathrm{ln}\frac{{\bf{probabilty}}\,{\bf{of}}\,{\bf{event}}}{{\bf{1}}-{\bf{probability}}\,{\bf{of}}\,{\bf{event}}\,}\) is called logit. It is the log of the odds that an event occurs. The odds that an event occurs are the ratio of the number of categories which happened over not occurs categories.

Where Yi* is latent outcome variable measure of tax payers;

X1, X2, X3……Xi are vectors of independent variables of ith case;

β0, threshold values;

β1, β2…βk are parameter vectors to be estimated (regression coefficients);

Єi is a random error term; k is the number of regression coefficients.

The dependent variable, tax compliance level (Yi*), is determined by averaging the scores of the four items: timely filing of tax returns, timely reporting of all income, satisfaction with tax payment, payment of taxes without enforcement, and the overall taxpayer score (which ranged from 1 = strongly disagree to 5 = strongly agree). The following formula was used to calculate the probability of each tax compliance level (low-Y1, medium-Y2, and high-Y3).

To estimate the tax compliance level, µ is a set of thresholds that can be determined using the parameter vector of βs, and y is an observable variable that represents different tax compliance levels of the taxpayer. The following model, which estimates the parameters of the study, was developed using the general equation mentioned above.

Where: TPVC = Tax Payers Voluntary Compliance;

β0 = Constant (Y intercept);

β1, β2, β3, β4 and + β5 = Coefficient of the independent variables

RI = Reward and Incentives

FTS = Fairness of Tax System

PGT = Perception of Government Trust

TPTK = Tax Payers Tax Knowledge

CC = Compliance Cost

Є = Error term;

Results and discussion

Spearman’s rho correlation test

According to Gogtay and Thatte (2017), a correlation coefficient is a single value that indicates the relationship between the two variables being studied. A nonparametric rank statistic that has been proposed to measure the degree of correlation between two variables is the Spearman rank correlation coefficient (Hauke and Kossowski, 2011). The Spearman chi-square test is used due to the ordinal and non-linear nature of the dependent variable, tax compliance. Using SPSS version 28 software, the correlation coefficient of the variables included in the study was determined using Spearman’s Rho test, as shown in the following table.

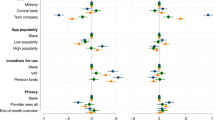

Table 1 shows a positive and significant relationship between the voluntary compliance of large taxpayers in Ethiopia and independent perceptions of government trust, taxpayers’ tax knowledge, tax system fairness, rewards, and incentives. Conversely, the Spearman correlation coefficient value indicated a significant negative relationship between compliance behavior and compliance costs.

Ordered logistic regression parameter estimates

The log-likelihood ratio is utilized in ordinal logistic regression to interpret the coefficient. The probability that the perceived values of the independent and dependent variables are similar is called the log-likelihood. This probability function is crucial for calculating the probability of observing data given unknown parameters (α and β). Like other probabilities, the probability ranges from 0 to 1. Since it is a logarithmic function, the log-likelihood function is easier to use. The log-likelihood method is used to compare different models.

The parameter estimate coefficient in Table 2 was used in this study to identify the influence of factor variables (perceptions of government trust, taxpayers’ tax knowledge, tax system fairness, compliance costs, rewards, and incentives) on the outcome variable (taxpayers’ voluntary tax compliance behavior). The results indicate that for large taxpayers in Ethiopia, the perception of trust in the government, taxpayers’ tax knowledge, perceptions of fairness of the tax system, and rewards and incentives have a positive and significant influence on voluntary tax compliance. On the other hand, compliance costs have a negative and significant effect on voluntary tax compliance.

From the parameter estimate in Table 3, the following logit equations were developed for significant variable categories. 1 represents a low level of voluntary tax compliance behavior, while 2 indicates a medium level of voluntary tax compliance behavior, which serves as cutoff points or thresholds. When the response variable is categorized according to its order of magnitude, ordinal/ordered logistic regression should be used (Nwakuya and Mmaduka, 2019). The proportional odds model is the most widely used in ordinal logistic regressions. The exponential estimate B can be used to determine the relationship of the factor variables to the dependent variable.

Independent variables with odds ratios or Exp(B) significantly greater than 1.0 have a significant positive impact on the response variable in the model. However, variables with odds ratios (exponential beta values) significantly less than 1.0 hurt the response or dependent variable (Liu, 2009).

Rewards and incentives

H1: rewards and incentives have a positive and significant effect on tax compliance behavior.

As indicated in Table 3 above, the odds ratio values show that taxpayers who strongly agree believe that rewards increase compliance more than punishment, rewards create goodwill for the business, being rewarded confirms the love of the country, tax deductions as rewards encourage tax compliance, and there is a need for improvement in the current reward system in Ethiopia. Hence, it is better to state that rewards and incentives have a positive and significant impact on tax compliance behavior. This confirms that the fiscal exchange theory of taxpayer compliance is primarily concerned with what taxpayers receive in return for paying taxes in the form of public services. This perspective considers taxes and the provision of public goods and services as a form of contract between the government and the taxpayers. In addition to monetary benefits, positive incentives can also promote qualities such as satisfaction, dignity, sincerity, recognition, identification with others, and a sense of justice or stability (Smith and Stalans, 1991).

Fairness in the tax system

H2: fairness in the tax system has a positive and significant effect on voluntary tax compliance behavior.

The odds ratio for the fairness of the tax system is presented in Table 3. It indicates that when all other factors are kept constant, taxpayers who perceived the current tax system as very fair were more inclined to exhibit high levels of voluntary compliance compared to taxpayers who did not perceive the tax system as fair. In general, the higher odds ratio for fairness suggests a positive and significant relationship between tax system fairness and voluntary tax compliance behavior in this study. It implies that a fair tax system - one in which the tax office treats all taxpayers equally, provides services based on the amount of tax collected, and requires taxpayers with the same income level to pay the same tax - will result in taxpayers voluntarily complying. An unfair tax system encourages taxpayers to evade taxes and avoid paying their dues. Consequently, the state’s treatment of an individual by other members of its larger national community is as important as what the individual receives from the state. The treatment of each taxpayer and the relationship between others’ tax burdens and compliance behavior are just two of the factors that demonstrate how the perceived fairness of the tax system influences compliance decisions. According to Walsh (2012), people are more likely to comply if they believe that others around them also pay taxes, which proves social influence. The comparative treatment theory affects taxpayers’ voluntary compliance.

Perception of government trust

H3: The perception of government trust has a positive and significant effect on tax compliance behavior.

Table 3 shows that Ethiopia’s voluntary tax compliance behavior is positively and significantly influenced by trust in the government. Taxpayers who trust their government are more likely to comply than those who do not, according to the overall quota ratio value. In other words, taxpayers in Ethiopia who have higher trust in the government are more likely to comply with voluntary tax laws. Conversely, taxpayers with lower perceptions are less inclined to comply with voluntary tax laws, which is in line with what the political legitimacy theory suggests: that citizens’ trust in their government affects tax compliance (Kirchler et al., 2008b). Taxpayers’ commitment to the tax system and payment of taxes increase when they have trust in the government (Jimenez and Iyer, 2016b), which aligns with political legitimacy theory.

Tax payers Tax knowledge

H4: Taxpayers’ tax knowledge has a significant and positive effect on tax compliance behavior.

The odds ratio values of tax knowledge in each category were greater than one, as shown in Table 3. This demonstrates that tax compliance is positively and significantly influenced by tax knowledge. This suggests that taxpayers who have received tax training and have in-depth tax knowledge, such as the type of income reported on tax returns and the proportion of expenses retained for tax purposes on the annual income return, are more compliant than taxpayers who have not received any training and lack in-depth knowledge of tax or payment processes. A taxpayer’s understanding of their rights, obligations, tax payment procedures, and the consequences of non-compliance is gained through tax education (Machogu and Amayi, 2016). Machogu and Amayi (2016) point out that taxpayer education can promote a positive attitude toward tax compliance and provide the necessary tax knowledge to comply with tax laws, which is in line with the theory of planned behavior.

Compliance costs

H5: Compliance costs have a negative and significant effect on tax compliance behavior.

Table 3 clearly illustrates the odds ratio for compliance costs, which have a statistically significant and negative impact on the voluntary tax compliance behavior of Ethiopian taxpayers. Thus, taxpayers who strongly agreed with compliance costs were less likely to achieve high voluntary compliance compared to taxpayers who strongly disagreed, with all other variables held constant. According to the odds ratio value, taxpayers in Ethiopia who strongly agreed, agreed, or were neutral about compliance costs (such as high cash register machine prices, high time spent organizing tax and related documents, high additional payments for accountants and sellers in their company, and high payments for tax advisors) were less likely to demonstrate high levels of voluntary compliance compared to those who strongly disagreed. As a result, the more likely tax evasion is to be discovered and punished severely, the fewer people will engage in it. Conversely, in situations where the likelihood of audits is low and fines are minimal, the expected return from evasion is high. As indicated by Helhel and Ahmed (2014), the model predicts significant non-compliance, which is explained by economic deterrence theory.

Conclusion and policy implication

Paying taxes does not come with a direct reward, but it is a mandatory payment that citizens make to the government. The level of tax compliance is determined by the willingness of taxpayers to follow tax laws, which is crucial for a nation to achieve economic stability. Convincing taxpayers to comply with tax laws is a challenging task, and tax non-compliance remains a significant issue for many tax authorities. Tax evasion and avoidance are the primary characteristics of taxpayers’ noncompliant behavior according to various theoretical frameworks. The findings revealed that all variables with theoretical foundations (taxpayers’ tax knowledge, perceptions of fairness in the tax system, perceptions of government trust, cost of compliance, and rewards) have a significant effect on voluntary tax compliance levels.

To enhance taxpayers’ perception of government trust, the tax administration office should ensure accountability and transparency in their actions by allocating the annual budget based on population size and other situational factors such as drought or war. Additionally, a portion of tax revenue should be directed toward essential projects for society. Furthermore, to enhance the level of trust in the government among taxpayers, the government should strongly combat corruption by government authorities and implement appropriate measures to address corrupt practices among tax authorities and all employees in revenue and customs offices.

Taxpayers with a good understanding of tax regulations are more likely to comply compared to those who are unaware of tax laws. Therefore, revenue authorities should prioritize raising awareness among taxpayers through ongoing training programs, media advertisements, workshops, and seminars. However, it is important to note that awareness should not be limited to providing tax knowledge alone. It should also involve consultation meetings and discussions with influential individuals such as religious leaders, well-known figures in society, or other persuasive individuals. This approach will help to have a broader impact on society through influential individuals who are respected within their respective groups.

Data availability

The datasets generated and analyzed during the current study are available upon reasonable request.

References

Ademe, H, & Simret, D (2020) Determinants of Tax Compliance Behavior in Ethiopia: Evidence from South Gondar Zone

Allingham MG, Sandmo A (1972) Income tax evasion: a theoretical analysis

Alm J, McClelland GH, Schulze WD (1992) Why do people pay taxes? J public Econ 48(1):21–38

Assfaw, AM, & Sebhat, W (2019). Analysis of tax compliance and its determinants: evidence from Kaffa, bench Maji and Sheka zones category B tax payers, SNNPR, Ethiopia

Augustine AA, Enyi EP (2020) Control of corruption, trust in government, and voluntary tax compliance in South-West, Nigeria. Manag Stud 8(1):84–97

Barbuta-Misu, N (2011) A review of factors for tax compliance

Barjoyai, B (1987) Taxation: Principle and Practice in Malaysia (Pencukaian Prinsip dan Amalan di Malaysia. J Kuala Lumpur, Dewan Bahasa dan Pustaka

Blaufus K, Eichfelder S, Hundsdoerfer J (2011) The hidden burden of the income tax: compliance costs of German individuals, of the income tax: Compliance costs of German individuals, Diskussionsbeiträge, No. 2011/6, Freie Universität Berlin, Fachbereich Wirtschaftswissenschaft, Berlin

Bobek DD, Hatfield RC (2003) An investigation of the theory of planned behavior and the role of moral obligation in tax compliance. Behav Res Account 15(1):13–38

Bornman M, Ramutumbu PJMAR (2019) A conceptual framework of tax knowledge

Cowell FA, Gordon J (1988) Unwillingness to pay: tax evasion and public good provision. J Public Econ 36(3):305–321

Dalu T, Maposa VG, Pabwaungana S, Dalu T (2012) The impact of tax evasion and avoidance on the economy: a case of Harare, Zimbabwe. African. J Econ Sustain Dev 1(3):284–296

Deyganto KO (2018b) Factors influencing taxpayers’ voluntary compliance attitude with tax system: evidence from Gedeo zone of Southern Ethiopia. Univers J Account Financ 6(3):92–107

Engida TG, Baisa GA (2014) Factors influencing taxpayers’ compliance with the tax system: an empirical study in mekelle city, Ethiopia. eJTR 12:433

Eragbhe E, Modugu KP (2014) Tax compliance costs of small and medium scale enterprises in Nigeria. Int J Account Tax 2(1):63–87

Fjeldstad O-H, Semboja J (2001) Why people pay taxes: the case of the development levy in Tanzania. World Dev 29(12):2059–2074

Fjeldstad O-H, Schulz-Herzenberg C, Hoem Sjursen I (2012) People’s views of taxation in Africa: a review of research on determinants of tax compliance

Fuks M, Salazar E (2008) Applying models for ordinal logistic regression to the analysis of household electricity consumption classes in Rio de Janeiro, Brazil. Energy Econ 30(4):1672–1692

Gogtay NJ, Thatte UM (2017) Principles of correlation analysis. J Assoc Phys India 65(3):78–81

Hauke J, Kossowski T (2011) Comparison of values of Pearson’s and Spearman’s correlation coefficients on the same sets of data. 30(2): 87. https://doi.org/10.2478/v10117-011-0021-1

Helhel Y, Ahmed Y (2014) Factors affecting tax attitudes and tax compliance: a survey study in Yemen. J Eur J Bus Manag 6(22):48–58

Ajzen I, Fishbein M (1970) The prediction of behavior from attitudinal and normative variables. J J Exp Soc Psychol 6(4):466–487

Ajzen I (1991) The theory of planned behavior. Organ Behav Hum Decis Process 50(2):179–211

Ajzen I (2002) Perceived behavioral control, self‐efficacy, locus of control, and the theory of planned behavior 1. J Appl Soc Psychol 32(4):665–683

James S, Alley C (2002) Tax compliance, self-assessment and tax administration

Jayawardane D (2015) Psychological factors affect tax compliance. A review paper. Int J Arts Commer 4(6):131–141

Jemberie DB (2020) Determinants of tax compliance: a case of nekemte town category ‘C’Business profit tax payers. Int J Econ Financ Manag Sci 8(3):89

Jenkins, GP, & Forlemu, EN (1993). Enhancing voluntary compliance by reducing compliance costs: a taxpayer service approach: Harvard Institute for International Development. Harvard University

Jimenez P, Iyer GS (2016b) Tax compliance in a social setting: the influence of social norms, trust in government, and perceived fairness on taxpayer compliance. Adv Account 34:17–26

Kefela D, Ghirmai T (2009) Reforming tax polices and revenue mobilization promotes a fiscal responsibility: a study of east and West African states. J Law Confl Resolut 1(5):98–106

Kirchler E, Hoelzl E, Wahl I (2008b) Enforced versus voluntary tax compliance: The “slippery slope” framework. J Econ Psychol 29(2):210–225

Liu X (2009) Ordinal regression analysis: fitting the proportional odds model using Stata, SAS and SPSS. J Mod Appl Stat Methods 8(2):30

Lois P, Drogalas G, Karagiorgos A, Chlorou A (2019) Tax compliance during fiscal depression periods: the case of Greece. EuroMed J Bus 14(3):274–291

Machogu C, Amayi JB (2016) The effect of taxpayer education on voluntary tax compliance, among SMEs in Mwanza City-Tanzania. Int J Market Financ Services Manage Res 2(8):12–23. http://www.indianresearchjournals.com/

Mathieson K (1991) Predicting user intentions: comparing the technology acceptance model with the theory of planned behavior. Inf Syst Res 2(3):173–191

Mebratu AA, Leyku F, Meroune L (2020) Determinant of tax revenue effort in sub-Saharan African countries: a stochastic frontier analysis. Int J Sustain Dev World Policy 9(1):47–71

Nandal S, Diksha D, Jaggarwal S (2021) Impacts of perceived tax fairness & tax complexity for GST structure on tax compliance: the perspectives of small and medium enterprises (SMEs). J NVEO-Nat 8(5):7337–7365

Nwakuya MT, Mmaduka O (2019) Ordered logistic regression on the mental health of undergraduate students. Int J Probab Stat 8(1):14–18

Okpeyo ET, Musah A, Gakpetor ED (2019a) Determinants of tax compliance in Ghana. J Appl Account Tax 4(1):1–14

Okpeyo ET, Musah A, Gakpetor ED (2019b) Determinants of tax compliance in Ghana. J Appl Account Tax 4(1):1–14

Oladipo O, Ogunjobi J, Eluyela D (2022) The impact of ethical tax behaviour on tax compliance of tax authority and corporate taxpayers of listed manufacturing companies in Nigeria. Academia Letters, Article 4698. https://doi.org/10.20935/AL4698

Palil MR, Mustapha AF (2011) The evolution and concept of tax compliance in Asia and Europe. Aust J Basic Appl Sci 5(11):557–563

Palil MR, Akir M, Ahmad W (2013) The perception of tax payers on tax knowledge and tax education with level of tax compliance: a study the influences of religiosity. ASEAN J Econ Manag Account 1(1):118–129

Robinson SLY (1996) Trust and breach of the psychological contract. Adm Sci Q 574–599

Saad N (2011) Fairness perceptions and compliance behavior: taxpayers’ judgments in self-assessment environments. Procedia - Social and Behavioral Sciences Vol 109, pp 1069–1075. https://doi.org/10.1016/j.sbspro.2013.12.590

Sah RK (1991) Social osmosis and patterns of crime. J Polit Econ 99(6):1272–1295

Sahu P (2021) Fairness dimension of goods and services tax: evidence from Indian MSMEs. Int J Account, Bus Financ 1(1):40–47

Sapiei NS, Abdullah M (2008) The compliance costs of the personal income taxation in Malaysia. Int Rev Bus Res Pap 4(5):2219–2230

Scholz JT, Lubell M (1998) Trust and taxpaying: testing the heuristic approach to collective action. Am J Polit Sci 42(2):398–417. https://doi.org/10.2307/2991764

Shallo L (2018) Determinants of tax compliance in ethiopia: case study in revenue and customs authority, Hawassa Branch. Res J Financ Account 9(21):95–104

Sitardja M, Dwimulyani S (2016) Analysis about the influences of good public governance, trust toward tax compliance on public companies that listed in Indonesian Stock Exchange. OIDA Int J Sustain Dev 9(09):35–42

Smith, KW, & Stalans, LJ (1991). Encouraging tax compliance with positive incentives: a conceptual framework and research directions. 13(1): 35–53

Snavely K (1990) Governmental policies to reduce tax evasion: coerced behavior versus services and values development. Policy Sci 23:57–72. https://doi.org/10.1007/BF00136992

Torres-Reyna, O (2012) Getting started in Logit and ordered logit regression. J Princeton University, http://dss.princeton.edu/training/Logit.pdf

Walsh K (2012) Understanding taxpayer behaviour–new opportunities for tax administration. Econ Soc Rev 43(3):451–475

Author information

Authors and Affiliations

Contributions

This paper was solely conducted by one author, from conceptualization and design of the article to analysis and interpretation of the data for the study, final approval of the version to be published, and agreement to be responsible for all aspects of the work. The author ensured that any questions regarding the accuracy or completeness of any part of the work were properly investigated and resolved.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests

Ethical approval

This article does not involve any studies with human participants conducted by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Mebratu, A.A. Theoretical foundations of voluntary tax compliance: evidence from a developing country. Humanit Soc Sci Commun 11, 443 (2024). https://doi.org/10.1057/s41599-024-02903-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-02903-y