Abstract

Measuring a country’s sustainable development by its gross domestic product (GDP) is insufficient to capture the loss of capital that determines future human welfare. To address this, we propose the inclusive wealth index, which integrates biophysical quantities and monetary values of natural, human, and produced capital. We analyzed the level of Inclusive Wealth in 163 countries over the past 30 years to assess sustainable development goals (SDGs) going beyond GDP. Global wealth has suffered significant losses in natural capital, with the biased accumulation of capital assets leading to unsustainable and unequal development. In low-income countries, soaring population levels and biased capital investments exacerbate the depletion of natural capital. Our results underscore the critical role of natural capital and inclusive capital management in sustainable development. Policymakers can use this information to make capital investments in their economies and promote recovery from COVID-19 that aligns with the SDGs, the Paris Climate Agreement, and initiatives beyond GDP.

Similar content being viewed by others

Introduction

There is a growing consensus that gross domestic product (GDP), traditionally used as a measure of short-term income fluctuations, does not adequately capture the nuances of long-term sustainable progress and overall human well-being (Stiglitz et al., 2009; Colglazier, 2015; Fleurbaey and Blanchet, 2013; Jones and Klenow, 2016). In response, there has been growing interest among researchers and policymakers in developing alternative measures that more comprehensively reflect the economic, social, and environmental dimensions of sustainable development. The landmark ‘Beyond GDP’ conference in Brussels in 2007, organized by the European Commission under the leadership of Jose M. Barroso, marked a crucial step towards this goal and catalyzed the creation of new indicators (Bleys, 2012). More recently, after the COVID-19 pandemic, which triggered a global environmental, health, and economic crisis, governments worldwide have recognized the need to address interconnected environmental, economic, social, and relational challenges to build back better (OECD, 2021). United Nations Secretary-General António Guterres (2022) echoed these sentiments at the Stockholm+50 international conference in June 2022, emphasizing the need to value environmental health and move beyond GDP as the sole measure of human progress. Recent policy dialogs and initiatives, notably the ‘Beyond Growth’ conference hosted by the European Parliament in Brussels in May 2023 (Jensen et al., 2023), continue to advance this narrative. This gathering, which echoes Barroso’s earlier initiatives, underlines the ongoing shift in the discourse on sustainable economic policy.

This paper proposes the Inclusive Wealth Index (IWI) as a measure beyond GDP. This indicator tracks natural, human, and produced capital assets as sub-categories of national wealth. IWI integrates biophysical data and monetary calculations for the different capital components into a single indicator (Managi and Kumar, 2018; Dasgupta Managi and Kumar, 2022). Conceptually, IWI establishes the equivalence between wealth and human welfare, and the wealth indicator shows that long-term and multidimensional sustainable development goals can be achieved through comprehensive wealth management strategies (Arrow et al., 2012; Dasgupta, 2014).

To date, there have been three empirical measures of inclusive wealth (UNU-IHDP, 2012; UNU-IHDP and UNEP, 2014; Managi and Kumar, 2018). Our latest fourth edition covers 163 countries from 1990 to 2019, including all significant economies on all continents, accounting for 98% of the world’s population. It has been improved with updated data covering multiple sustainable development goals (SDGs). Our empirical results reveal overexploitation of natural capital and uneven capital accumulation across countries. We conclude that developing and low-income countries with poor natural capital management are more vulnerable to natural capital depletion and other capital accumulation deficits, leading to unsustainable progress despite short-term income improvements.

We discuss trade-offs that policymakers can identify to achieve the best long-term outcomes for the well-being of their citizens. Inclusive wealth offers an opportunity to recover from the COVID-19 pandemic regarding sustainable development, the Paris Climate Agreement, and changes beyond GDP. In this sense, it enables policymakers to manage the economy sustainably.

In the following sections, we explain the concept of indicators beyond GDP and the assessment of the capital base for achieving the SDGs. We then describe the empirical challenges of estimating inclusive wealth matrices and updating state-of-the-art datasets. Based on our key findings, we summarize and discuss the main results. Finally, we close the paper with a conclusion.

Measure sustainable progress beyond GDP

Since the Industrial Revolution, economic growth has led to remarkable improvements in human well-being, including progress in eradicating deadly diseases, significant reductions in extreme poverty, and increases in literacy and mobility (Steffen et al., 2007; Steffen et al., 2018; Crutzen and Stoermer, 2000). At the same time, the intensification of globalized economic activity has led to human impacts that may exceed the limits of the safe and sustainable functioning of Earth’s natural systems (Rockström et al., 2009; Scheffer, 2020). The concept of ‘planetary limits’ highlights the need for a more sustainable and equitable development model (Leach et al., 2013; Steffen et al., 2018; Stafford-Smith et al., 2017; Kortetmäki et al., 2021). The UN’s 17 sustainable development goals (SDGs) aim to guide the international community toward an intrinsic development path by providing a comprehensive and integrated framework for all aspects of sustainable development, including economic, social, and environmental considerations (Obersteiner et al., 2016; Stafford-Smith et al., 2017; Brewer, 2019; Glaser, 2012).

However, assessing progress towards the sustainable development of nations, particularly in light of a better recovery from the COVID-19 pandemic, implies that GDP as a measure of economic growth needs to be improved (OECD, 2021). The ‘Beyond GDP’ movement has gained increasing attention in the literature over the past decades (Stiglitz et al., 2009; Aitken, 2019; Stiglitz et al., 2018). Leading economists have been supporting the call to go beyond GDP for at least half a century (Fleurbaey and Blanchet, 2013; Colglazier, 2015). Going beyond GDP is necessary to measure sustainable progress for three reasons. First, GDP does not adequately reflect changes in human well-being, leading policymakers to adopt policies that reduce welfare (Sen, 1999). Second, as a measure of changes in income flows over time, GDP ignores changes in the underlying assets that generate them, such as natural capital (Arrow et al., 2012; Arrow et al., 2003). Finally, official statistics on GDP do not keep pace with changes in the nature and structure of economic activity, such as the deepening process of globalization (Stiglitz et al., 2009; van den Bergh, 2022). These shortcomings of GDP are strongly correlated and lead to increased uncertainty about sustainable development.

Finding measures beyond GDP is a challenging task, as commonly proposed alternatives based on the current System of National Accounts (SNA), such as green GDP-type indicators, including the Index of Sustainable Economic Welfare (ISEW) (Daly, 1994) and the closely related Genuine Progress Indicator (GPI) (Posner and Costanza, 2011), have been criticized for being too closely related to GDP and may not provide entirely new information. Moreover, the stability and convergence of the Human Development Index (HDI) and GDP suggest that GDP per capita remains valuable (Van Den Bergh and Botzen, 2018). According to the Sustainable Development Goals (SDG) Index and Dashboard (Sachs et al., 2019), GDP per capita is the strongest predictor of SDG performance, although it explains only half of the variance in SDG scores across countries (Agarwal and Saha, 2021).

The Inclusive Wealth Index (IWI) provides a framework for assessing a country’s sustainable development beyond GDP (Managi and Kumar, 2018; Managi, 2019). The uniqueness of the IWI lies in its equity (capital) based approach to measuring changes in national wealth, which differs from but complements GDP in that the IWI measures the capital stock, potentially generating economic liquidity output. The IWI measures the social value of all assets (or stocks) that are sources of human well-being: human capital, produced (tangible) capital, and natural capital. The IWI framework recognizes the limited substitutability of finite natural resources and emphasizes the importance of efficient and effective capital management for sustainable development. Wealth accounts show that achieving the SDGs is not only linked to environmental policies but also to efficient and effective capital management (Dasgupta, 2021).

Wealth accounts have two fundamental relationships with the current SNA in national accounts. First, they provide a forward-looking perspective by measuring the productive base that enables future production of goods and services, in contrast to the SNA, which measures consumption and welfare that has already occurred. Second, wealth accounts allow for greater flexibility and experimentation, which is essential given that the degradation of natural assets can have far-reaching effects beyond a country’s borders and the scope of the SNA. Wealth accounts offer a broader scope because specific components of wealth, such as global public goods like the climate system and biodiversity, are not limited to the same geographical and political scope as the SNA.

Despite their advantages, national IW accounts still need improvement in several areas (van den Bergh, 2022; Cook and Davı́ðsdóttir, 2021). For example, the valuation of intangibles, such as education quality and human capital’s health component, can be improved. Another challenge is reducing reliance on market prices and measuring the interaction between different capital assets. It is important to note that more than market valuation is needed to address human participation in public goods related to the biosphere, as natural processes cannot fulfill the technical conditions necessary for the market to function effectively. In addition, the relationship between technological progress and environmental policy and the insufficient focus on intergenerational inequalities require further discussion.

To address these issues, the latest round of Inclusive Wealth Accounts has updated methods and data and added new discussions to complement and improve the IW accounts. The following section details the methodological and data improvements made in the latest IW Accounts.

Methods

The Inclusive Wealth Index (IWI) is an indicator that measures wealth by combining biophysical data and monetary calculations for multiple components of capital. Its foundations have been developed through extensive theoretical and empirical research (Dasgupta and Mäler, 2000; Arrow et al., 2003; Arrow et al., 2004; Arrow et al., 2012; Dasgupta, 2014; Agliardi et al., 2012). Demonstrations of the equivalence between wealth and social welfare form the basis of the IWI assessment of intergenerational sustainability (Supplementary Information: S1.1. General Framework).

The construction of a cross-country IW account is a complex task that requires the aggregation of global databases on various aspects of the economy, society, natural resources, and the environment, and the quantification and valuation of each country’s assets according to a consistent methodology (see Supplementary Information: S1.2–S1.5 for details of specific capital accounting methodologies and data sources). The ultimate, but not redundant, assets that provide exhaustive intergenerational benefits are natural, human, and produced capital. In the current IWI valuation method, intangible capital, such as social capital, is assumed to be the potential embodied value of the three main capitals that are not separately accounted for in the basic accounts.

The crucial concept in IW is to assign shadow prices to capital assets that reflect their social value and contribution to intergenerational welfare. The ratio of weights measures the marginal social substitution rates between capital assets. The valuation of capital assets is crucial for the construction of wealth accounts. Market prices are the primary source of information for the shadow prices used in the wealth accounts, and we adjust them to reflect long-term sustainability considerations rather than relying solely on volatile market prices. One exception is the value of ecosystem services. We have derived their value from the Ecosystem Services Valuation Database. (ESVD) (Brander et al., 2023).

The experience of rapid population growth in history and the considerable uncertainty in future population projections show that sustainability can only be maintained if population growth is taken into account (Dasgupta, 2014; Barbier, 2019). We therefore use the non-declining IWI per capita estimate at constant shadow prices to measure real sustainable development. In addition to population growth, three other time-varying adjustments are considered: total factor productivity (TFP), CO2 damages, and oil price gains. The first reflects technological and skill progress in capital accumulation, while the latter two adjustments reflect the impact of transnational externalities on national welfare.

The earlier IW accounts provided valuable insights, including the significant global decline in natural capital and the clear independence of IW from GDP or other wealth indicators. The third update also found strong correlations between IW and SDG indicators, particularly for SDGs 12, 13, and 7 (Sugiawan et al., 2023). Building on the work of previous reports, we have produced the latest cross-country Inclusive Wealth Index (IWI) by further updating and refining the previous framework (UNEP, 2022; UNEP, 2023). Table 1 briefly summarizes the scope and updates made to each capital account between the last three reports and the latest update.

The main updates are as follows: first, the scope of natural capital accounting under the original classification has been expanded by updating the data, resulting in an increase in the number of national accounts assessed from 140 to 163, covering the period from 1990 to 2019. Second, comprehensive information on the dimensions of gender, education, and health has been integrated to estimate human capital, expanding the scope of the assessment in relation to the SDGs. Third, the accuracy of the estimate of produced capital has been improved by considering sub-categories such as investment in buildings, roads, and transport equipment by country and year, and by applying aggregated depreciation rates.

Although the IW account has been improved, there are still limitations and challenges exist, such as the need for more consideration of ecosystem services other than forests, the lack of consumption-side accounts, and the lack of information on gender differences in annual wages for estimating the shadow prices of human capital. Despite these limitations, analyzing trends in different capital assets provides the necessary insights and knowledge to discuss sustainability performance. The following section presents the main findings of the updated IW accounts. In particular, we focus on changes in national wealth in relation to GDP-focused growth and the correlation with intragenerational inequality.

Results

This study uses updated national IW accounts to assess the dynamics of wealth accumulation in 163 countries. Our analysis focuses on two key issues: first, we examine the relationship between population growth, consumption, and natural capital depletion and how this affects global per capita IW decline. Second, we examine the developmental disparities associated with natural capital depletion between and within countries. We examine these trends and discuss the underlying factors driving wealth changes across countries. We categorize the 163 countries according to the World Bank definition by income and region (see Supplementary Information: S2 for region and income grouping), highlighting the distinction of the G20 countries as a separate group from other classifications.

Identifying population-consumption-environment nexus

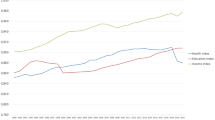

Figure 1 illustrates global changes in IW and natural capital. The data show that natural capital has declined by 28% since 1990. Meanwhile, per capita natural capital in 2019 was almost 50% lower than in 1990. This translates into a global decline in per capita IW of 0.5%. This is a worrying trend as economic growth has come at a significant cost to natural capital due to the rapid net increase of 2.4 billion people. Figure 1a also shows that human capital per capita is a source of wealth accumulation, although its growth rate has slowed in recent years.

a Shows the percentage change from 1990 for IW per capita, capital components per capita, GDP per capita, and total population. b Shows the change in the composition of natural capital since 1990, with East Asia and Pan-Pacific (EAP), East Central Asia (ECA), Latin America and the Caribbean (LAC), Middle East and North Africa (MENA), Sub-Saharan Africa (SSA), and G20 countries as groups.

Furthermore, unequal consumption and ownership of natural capital across regions exacerbate countries’ environmental challenges. As shown in Fig. 1b, there is an alarming concentration of natural capital in the hands of the G20 countries, which now hold 68% of the world’s share of natural capital, up from 60% in 1990. In contrast, natural capital in Latin America, the Caribbean (LAC), East Asia, and the Pacific (EAP) has declined in quantity and global share. This disparity in natural capital between the wealthiest countries and the rest of the world highlights the challenge of achieving sustainable and equitable development.

Table 2 summarizes the average rate of change in wealth per capita and the contribution of capital accumulation and population growth for each income group over the period 2010–2019. The results show significant differences in wealth accumulation and the contributing factors across income groups. G20 countries have the highest growth in per capita wealth. In contrast, lower-middle-income countries experienced slower growth, and low-income countries even saw their wealth shrink due to population growth and natural capital depletion. High-income countries had the highest investment in human and produced capital. However, their wealth accumulation was limited by the more significant impact of population growth and natural capital depletion, leading to less wealth accumulation than in upper-middle-income countries.

Figure 2 shows a stacked bar chart of per capita wealth changes in natural, human, and produced capital for 163 countries from 2010 to 2019, with per capita accumulation excluding the impact of population growth. Of the 163 countries, 45 experienced negative per capita wealth growth over the past decade, 30 of which were low and lower-middle-income countries, as they experienced the lowest per capita growth in human and produced capital and the largest per capita decline in natural capital. Sixteen countries experienced a decline in human capital per capita, as population growth outpaced human capital accumulation. Over the last decade, 18 countries, mostly in the G20, experienced depopulation. However, they still had positive growth in human capital per capita due to increased investment in human capital. Ten of these countries still experienced a loss of natural capital per capita despite population decline, suggesting that fewer people may not lead to reduced consumption of natural capital.

The average contribution of capital in per capita wealth growth in 2010–2019.

These findings highlight the complex interactions between population, consumption, and the environment. Population growth generates more human capital but leads to more consumption and, consequently, more natural capital depletion. Even with increased investment in human and physical capital, faster natural capital depletion and population growth threaten per capita wealth accumulation. On the other hand, population decline in developed countries does not necessarily mean less consumption of natural capital per capita. Countries need to monitor population growth patterns and identify excessive consumption leading to natural capital depletion.

In conclusion, the inadequate accumulation of capital such as manufactured capital, the stagnation of investment in human capital, and the uneven depletion of natural capital pose a new challenge to global, intergenerational well-being.

Identifying natural capital depletion and inequality

The relationship between natural capital depletion and development disparities between countries is another critical issue in this study. To this end, we examine the relationship between total factor productivity (TFP) growth and natural capital depletion for countries. Figure 3 shows the average growth rate of TFP and the average rate of change of natural capital per capita for each income group from 2010 to 2019. TFP measures the efficiency of the inputs used in the production process (Christensen et al., 1973). In the Wealth framework, TFP extends this concept to include natural capital as an input in addition to human and manufactured capital. Wealth TFP recognizes that natural capital is also essential to the production process. Inequitable capital accumulation can have a significant impact on economic growth and development.

The relation between TFP growth and natural capital depletion.

Figure 3 shows the depletion of natural capital per capita from 1990 to 2019 in relation to changes in countries’ TFP. Most countries in Fig. 3 fall into the fourth quadrant, implying that productivity and technological progress contribute to GDP growth through capital accumulation. However, most countries also face further depletion of natural capital. Low-income countries have the highest rates of natural capital depletion, while G20 countries have the lowest. Moreover, TFP and changes in natural capital show a positive correlation for low-income and upper-middle-income countries, suggesting that productivity growth in these countries may be associated with worsening natural capital depletion. In contrast, high-income countries show a trend that the more technological progress is made, the lower the level of natural capital depletion. G20 and lower-middle-income countries also show similar trends but are less clear-cut.

These results show that natural capital depletion exacerbates development disparities between countries. The correlation between TFP growth and natural capital depletion highlights the need to develop more sustainable production methods less dependent on natural capital. In this respect, high-income countries are doing better than others in adopting technologies that reduce natural capital depletion. At the same time, low-income countries need more support to develop sustainable production methods to achieve sustainable economic growth while protecting the environment.

We then examined the relationship between natural capital depletion and national income inequality by subcategory. We collected a time series of Gini coefficients for 35 countries from the World Bank database. We compared these values against natural capital per capita (log) changes for each subcategory from 2000 to 2010 and 2010 to 2019 (Fig. 4). As the most widely used measure of inequality, the Gini coefficient reflects a country’s income distribution (UN DESA, 2015). It compares the income distribution in a country with a perfectly equal distribution for each percentile (where each citizen is modeled as having the same income). The Gini coefficient is calculated using the Lorenz curve, which represents the distribution of wealth or income among people within geographical boundaries and is derived from a perfectly equal distribution (Gastwirth, 1972). The index ranges from 0 to 100: the higher the value or Gini coefficient, the higher the degree of inequality and the greater the share of total income held by the wealthiest class.

The relation between income inequality and natural capital depletion in country groups in 2000, 2010, and 2019.

Our results show that for non-renewable energy, mineral, and fishery resources, improvements in income equity are often associated with the loss of natural resources in highly unequal middle-income countries. In contrast, for high-income and G20 countries, the opposite trend is observed, with inequality worsening with the development of natural capital, such as energy resources in the United States, Denmark, and India; mineral resources in Russia, Sweden, and India; and fishery resources in Denmark, the United States and India.

The situation for agriculture and forestry may be more complicated, as the decline in forest resources may be related to increased land clearing for agriculture. The decline in forest resources per capita in middle-income countries is associated with increased income equality. However, only two countries (Honduras and Bolivia) show that increases in agricultural resources per capita are associated with improvements in income equality. In G20 and high-income countries, the decline in forest and agricultural resources may be associated with income inequality, as shown in India and Denmark.

These findings highlight the inequality of natural capital depletion. Middle-income countries can improve income equality by giving citizens free access to natural resources. However, public goods must be better managed, as the tragedy of the commons and rapid population growth may lead to further resource loss. Losses of natural capital cannot be replaced by other forms of human or manufactured capital, which significantly impacts wealth accumulation and sustainable development in these countries. In contrast, in high-income and G20 countries with relatively well-established capital management and markets, economic development and other capital accumulation can be achieved with relatively low natural capital losses. However, without effective redistributive policies, the benefits of natural resource depletion may be limited to certain groups in these countries, exacerbating income inequality. Therefore, a comprehensive policy framework that considers the complex interactions between natural capital, income inequality, and sustainable development is crucial.

Discussion

Based on the latest IW country accounts, our study shows that global per capita inclusive wealth has not been on a sustainable development and equity trajectory in recent decades. Historically, the iterative relationship between rapid population growth, consumption, and natural capital depletion has adversely affected global wealth accumulation. In particular, developing and low-income countries with inadequate natural resource management have faced exacerbated natural capital depletion and unsustainable development. These countries may benefit from free access to natural resources to improve short-term income and inequality issues. However, they are challenged to accumulate other capital assets to compensate for the loss of natural capital due to rapid population growth and poorly constructed capital investments. In particular, other capital assets cannot replace the non-market loss of natural capital. The irreversible loss of natural capital leads to unsustainability in these countries.

Countries have recognized the non-substitutability of natural resources, and the past mode of development based solely on economic growth is changing. However, policies to protect resources and the environment can exacerbate inequalities. Another key finding of this study is that the G20 countries, which have historically been committed to resource and environmental protection policies, now hold an even larger share of the world’s natural resources, exacerbating natural capital inequalities between countries. While high-income countries are reducing the loss of natural resources through technological change, middle-income, and low-income countries are contributing to the irreversible depletion of natural resources through technological progress and capital accumulation. The uneven management of natural capital has exacerbated development inequalities. In addition, policies to protect natural resources can increase inequality within these countries due to the unequal distribution of wealth across income groups.

Previous seminal works on natural and environmental sustainability take the pessimistic view that due to the non-substitutability of natural capital, production, and consumption must be limited to maintain future human well-being (Daly, 1994; Georgescu-Roegen, 1975). On the other hand, the Inclusive Wealth framework shows that sustainable development requires efficient management of all capital, including natural resources, beyond environmental policy. The COVID-19 pandemic disrupted progress on many of the Sustainable Development Goals. However, the experience of the pandemic has shown that mobilizing capital is critical to addressing common global challenges. Public investment, if effectively allocated and coordinated, can provide the foundation for a sustainable, inclusive, resilient, and prosperous global recovery. The United Nations 2030 Agenda for Sustainable Development has taken the first steps towards achieving the targets set out in its 17 Sustainable Development Goals.

Conclusion

Based on the theory of wealth and welfare equivalence, the Inclusive Wealth Index was developed in response to the Beyond GDP movement and represents an evolutionary step in sustainability measurement. Research and policy initiatives are promoting and strengthening inclusive wealth metrics (White House, 2023; World Bank, 2021; OECD, 2020; Schwab, 2019). There is a consensus that decision-makers must focus on wealth growth to ensure the well-being of people in the 21st century.

The IWI provides a comprehensive assessment of a nation’s wealth. As nations strive to achieve the Sustainable Development Goals, there is a critical need to balance the enhancement of enabling assets with strategic capital investments. Our extended IW accounting, which mirrors a corporate balance sheet, provides a more nuanced and comprehensive assessment, enhancing its practical relevance.

While our extended IW accounting provides a robust framework for asset valuation, data limitations require further research and refinement. Challenges remain in accurately valuing ecosystem services, particularly for diverse ecosystems and their evolving functions. In addition, incorporating finer gender disaggregation into human capital valuations will require innovative shadow-pricing methods. These limitations, however, do not detract from the IWI’s crucial contribution to the advancement of environmental economics. Instead, they highlight exciting opportunities for future research to strengthen the accuracy and applicability of the IWI.

Despite the data challenges, our study paves the way for further research refinement. The stark contrast between sustainable wealth accumulation and depletion paths revealed by our IWI analysis underscores the urgency of tailored development strategies. For nations grappling with rapid urbanization and resource depletion, the IWI provides a roadmap for investing in human capital, fostering technological innovation, and protecting vital natural capital. To achieve sustainable development goals and ensure equitable prosperity for all, policymakers must embrace inclusive wealth metrics and actively integrate them into policy frameworks.

Going forward, we advocate the systematic inclusion of the IWI alongside other non-GDP indicators that provide more robust perspectives on inclusive development and the achievement of sustainable development goals. Such comparative analyses can strengthen policy discourse and ensure a comprehensive approach to assessing progress and guiding nations toward sustainable prosperity.

Data availability

The datasets generated and/or analyzed in the current study are not publicly available. However, these data are available from the authors upon reasonable request and subject to certain conditions. Requests for access to the data should be addressed to the author. Requests for access to the data should be directed to the author and will be considered in accordance with the data-sharing policies of the Urban Institute of Kyushu University and the requirements of the data custodians.

References

Agarwal M, Saha R (2021) Water and sanitation: achievement of large Indian states. Indian J Hum Dev 15:82–99. https://doi.org/10.1177/09737030211001767

Agliardi E, Agliardi R, Pinar M, Stengos T, Topaloglou N (2012) A new country risk index for emerging markets: A stochastic dominance approach. J Empir Financ 19(5):741–761. https://doi.org/10.1016/j.jempfin.2012.08.003

Aitken A (2019) Measuring Welfare Beyond GDP. Natl Inst Econ Rev 249(1):3–16. https://doi.org/10.1177/002795011924900110

Arrow KJ, Dasgupta P, Mäler KG (2003) Evaluating projects and assessing sustainable development in imperfect economies. Environ Resour Econ 26:647–685. https://doi.org/10.1023/B:EARE.0000007353.78828.98

Arrow KJ, Dasgupta P, Mäler K-G (2003) The genuine savings criterion and the value of population. Econ Theory 21(2/3):217–225. http://www.jstor.org/stable/25055622

Arrow KJ, Dasgupta P, Goulder LH, Mumford KJ, Oleson K (2012) Sustainability and the measurement of wealth. Environ Dev Econ 17(3):317–353. http://www.jstor.org/stable/26265518

Arrow KJ, Dasgupta P, Goulder LH, Daily G, Ehrlich P, Heal G, Levin S, Mäler K-G, Schneider S, Starrett D, Walker B (2004) Are we consuming too much? J Econ Perspect 18(3):147–172. https://doi.org/10.1257/0895330042162377

Barbier EB (2019) How to make the next Green New Deal work. Nature 565(7737):6. https://doi.org/10.1038/d41586-018-07845-5

Bleys B (2012) Beyond GDP: classifying alternative measures for progress. Soc Indic Res 109(3):355–376. http://www.jstor.org/stable/23325435

Brander LM, de Groot R, Guisado Goñi V, van ‘t Hoff V, Schägner P, Solomonides S, McVittie A, Eppink F, Sposato M, Do L, Ghermandi A, Sinclair M (2023) Ecosystem Services Valuation Database (ESVD). https://www.esvd.net/. Accessed 3 Apr 2021

Brewer MK (2019) Slow fashion in a fast fashion world: promoting sustainability and responsibility. Laws 8(4):24. https://doi.org/10.3390/laws8040024

Christensen LR, Jorgenson DW, Lau LJ (1973) Transcendental logarithmic production frontiers. Rev Econ Stat 55(1):28–45

Colglazier W (2015) Sustainability. Sustainable development agenda: 2030. Science (N. Y, N. Y) 349(6252):1048–1050. https://doi.org/10.1126/science.aad2333

Cook D, Davíðsdóttir B (2021) An appraisal of interlinkages between macro-economic indicators of economic well-being and the sustainable development goals. Ecol Econ 184:106996. https://doi.org/10.1016/j.ecolecon.2021.106996

Crutzen PJ, Stoermer EF (2000) The “Anthropocene”. IGBP Newsl 41:17–18. Available at Accessed on 22 May 2022 http://www.igbp.net/download/18.316f18321323470177580001401/1376383088452/NL41.pdf

Daly HE (1994) For the common good: Redirecting the economy toward community, the environment, and a sustainable future. Beacon Press

Dasgupta P (2014) Measuring the wealth of nations. Annu Rev Resour Econ 6:17–31. https://doi.org/10.1146/annurev-resource-100913-012358

Dasgupta P, Mäler K-G (2000) Net national product, wealth, and social well-being. Environ Dev Econ 5(1):69–93. https://doi.org/10.1017/S1355770X00000061

Dasgupta P, Managi S, Kumar P (2022) The inclusive wealth index and sustainable development goals. Sustain Sci 17(3):899–903. https://doi.org/10.1007/s11625-021-00915-0

Dasgupta P (2021) The economics of biodiversity: the Dasgupta review. Hm Treasury. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/962785/The_Economics_of_Biodiversity_The_Dasgupta_Review_Full_Report.pdf

Fare R, Grosskopf S, Noh D-W, Weber W (2005) Characteristics of a polluting technology: theory and practice. J Econ 126(2):469–492. https://doi.org/10.1016/j.jeconom.2004.05.010

Fleurbaey M, Blanchet D (2013) Beyond GDP: measuring welfare and assessing sustainability. Oxford University Press

Gastwirth JL (1972) The estimation of the Lorenz Curve and Gini Index. Rev Econ Stat 54(3):306–316. https://doi.org/10.2307/1937992

Georgescu-Roegen N (1975) Energy and economic myths. South Econ J 41(3):347–381. https://doi.org/10.2307/1056148

Glaser G (2012) Base sustainable development goals on science. Nature 491:35. https://doi.org/10.1038/491035a

Jensen LE et al. (2023) Beyond growth—pathways towards sustainable prosperity in the EU. https://doi.org/10.2861/602232

Jones CJ, Klenow PJ (2016) Beyond GDP? Welfare across countries and time. Am Econ Rev 106(9):2426–57

Jorgenson DW, Fraumeni BM (1992) The output of the education sector. In: Output measurement in the service sectors. University of Chicago Press. pp. 303–341

King RG, Levine R (1994) Capital fundamentalism, economic development, and economic growth. Carnegie-Rochester Conf Ser Public Policy 40:259–292

Kortetmäki T, Mikael P, Miikka S, et al. (2021) Planetary well-being. Humanit Soc Sci Commun 8(1). https://doi.org/10.1057/s41599-021-00899-3

Leach M, Raworth K, Rockström J (2013) Between social and planetary boundaries: navigating pathways in the safe and just space for humanity. In: World Social Science Report, 2013: Changing Global Environments, pp. 84-89. UNESCO/OECD, Paris, France. CC BY-SA 3.0 IGO

Managi S (2019) Wealth, inclusive growth and sustainability. Routledge New York, New York

Managi S, Kumar P (eds) (2018) Inclusive Wealth Report 2018: Measuring Progress Towards Sustainability (1st edn.). Routledge. https://doi.org/10.4324/9781351002080

Martell S, Froese R (2013) A simple method for estimating MSY from catch and resilience. Fish Fish 14(4):504–514

Obersteiner M et al. (2016) Assessing the land resource-food price nexus of the Sustainable Development Goals. Sci Adv 2(9):e1501499. https://doi.org/10.1126/sciadv.1501499

OECD (2020) Beyond growth: towards a new economic approach, new approaches to economic challenges. OECD Publishing, Paris, https://doi.org/10.1787/33a25ba3-en

OECD (2021) COVID-19 and well-being: life in the pandemic. OECD Publishing, Paris, https://doi.org/10.1787/1e1ecb53-en

Posner SM, Costanza R (2011) A summary of ISEW and GPI studies at multiple scales and new estimates for Baltimore City, Baltimore County, and the State of Maryland. Ecol Econ 70(11):1972–1980. https://doi.org/10.1016/j.ecolecon.2011.05.004

Rockström J, Steffen W, Noone K et al. (2009) A safe operating space for humanity. Nature 461:472–475. https://doi.org/10.1038/461472a

Sachs JD, Schmidt-Traub G, Mazzucato M et al. (2019) Six transformations to achieve the sustainable development goals. Nat Sustain 2:805–814. https://doi.org/10.1038/s41893-019-0352-9

Scheffer M (2020) Critical transitions in nature and society (vol. 16). Princeton University Press

Schwab K (2019) How keeping score can end the era of short-termism. Available via World Economic Forum. https://www.weforum.org/agenda/2019/10/how-we-can-end-short-termism-by-keeping-score/. Accessed 24 Dec 2019

Sen A (1999) Commodities and capabilities. Oxford University Press. ISBN 9780195650389

Stafford-Smith M, Griggs D, Gaffney O et al. (2017) Integration: the key to implementing the sustainable development goals. Sustain Sci 12:911–919. https://doi.org/10.1007/s11625-016-0383-3

Steffen W et al. (2018) Trajectories of the earth system in the anthropocene. Proc Natl Acad Sci USA 115:8252–8259. https://doi.org/10.1073/pnas.1810141115

Steffen W, Crutzen PJ, McNeill JR (2007) The Anthropocene: are humans now overwhelming the great forces of nature? Ambio 36(8):614–621. http://www.jstor.org/stable/25547826

Stiglitz J, Fitoussi J-P, Durand M (2018) Beyond GDP: Measuring What Counts for Economic and Social Performance. OECD Publishing, Paris. https://doi.org/10.1787/9789264307292-en

Stiglitz J, Sen A, Fitoussi J (2009) Report of the Commission on the Measurement of Economic Performance and Social Progress (CMEPSP). Available via European Commission. https://ec.europa.eu/eurostat/documents/8131721/8131772/Stiglitz-Sen-Fitoussi-Commission-report.pdf. Accessed 24 Mar 2022

Sugiawan Y, Kurniawan R, Managi S (2023) Assessing the United Nations sustainable development goals from the inclusive wealth perspective. Sci Rep 1313:1601. https://doi.org/10.1038/s41598-023-28540-0

Tamaki T, Shin KJ, Nakamura H, Fujii H, Managi S (2018) Shadow prices and production inefficiency of mineral resources. Econ Anal Policy 57:111–121. https://doi.org/10.1016/j.eap.2017.03.005

UN Development Strategy and Policy Analysis Unit (2015) Concepts of inequality development issues no. 1. Available via UN. https://www.un.org/development/desa/dpad/wp-content/uploads/sites/45/publication/dsp_policy_01.pdfofsubordinatedocument. Accessed 14 Feb 2020

UN Secretary-General (2022) Secretary-General’s remarks to Stockholm+50 international meeting [as delivered]. In: United Nations Official Statements. United Nations. Available via UN website. https://www.un.org/sg/en/content/sg/statement/2022-06-02/secretary-generals-remarks-stockholm50-international-meeting-delivered. Accessed 15 Oct 2022

UNEP (2022) Inclusive Wealth Report 2022: Executive Summary. United Nations, NewYork. https://wedocs.unep.org/20.500.11822/40601

UNEP (2023) Inclusive Wealth Report 2023: Measuring Sustainability and Equity. https://wedocs.unep.org/20.500.11822/43131

UNU-IHDP (2012) Inclusive Wealth Report 2012: measuring progress toward sustainability. Cambridge University Press, Cambridge

UNU-IHDP, UNEP (2014) Inclusive Wealth Report 2014: measuring progress toward sustainability. Cambridge University Press, Cambridge

van den Bergh JCJM (2022) A procedure for globally institutionalizing a ‘beyond-GDP’ metric. Ecol Econ 192:107257. https://doi.org/10.1016/j.ecolecon.2021.107257

van den Bergh JCJM, Botzen WJW (2018) Global impact of a climate treaty if the Human Development Index replaces GDP as a welfare proxy. Clim Policy 18(1):76–85. https://doi.org/10.1080/14693062.2016.1227954

White House (2023) National strategy to develop statistics for environmental-economic decisions. Avaialbe via the white house(gov). http://www.whitehouse.gov/wp-content/uploads/2023/01/Natural-Capital-Accounting-Strategy-final.pdfofsubordinatedocumaent. Accessed 24 Mar 2023

World Bank (2021) The changing wealth of nations 2021: managing assets for the future. World Bank, Washington, DC, http://hdl.handle.net/10986/36400

Author information

Authors and Affiliations

Contributions

SM: led the overall project, including the design of the study (conceptualization), managing funding (funding acquisition), overseeing research activities (project administration and supervision), and played a key role in writing the original draft (writing—original draft). SC: contributed to developing the research methods (methodology), conducted the research work and data collection (investigation), was responsible for the creation of visual data representations (visualization), and co-wrote the original manuscript (writing—original draft). PK: involved in designing the study (conceptualization) and played a significant role in developing the research methods (methodology). PD: assisted in conceptualizing and developing the study idea (conceptualization).

Corresponding author

Ethics declarations

Competing interests

The authors declare that they have no competing interests in this research. No financial or personal relationships with other people or organizations have influenced the work reported in this paper. This statement is made for full disclosure and to ensure the research’s integrity.

Ethical approval

All procedures performed in this study, which did not involve human participants, were conducted following the ethical standards of Kyushu University and the relevant national research committee. This research adheres to the ethical principles of the 1964 Helsinki Declaration and its later amendments or comparable ethical standards. Since the study did not involve any procedures requiring ethical approval by an institutional review board, no specific protocol number was assigned.

Informed consent

This study did not involve human participants, and therefore, no informed consent was required. All research procedures were conducted in accordance with the ethical guidelines and standards of the Urban Institute of Kyushu University and/or the relevant national research committee.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Managi, S., Chen, S., Kumar, P. et al. Sustainable matrix beyond GDP: investment for inclusive growth. Humanit Soc Sci Commun 11, 185 (2024). https://doi.org/10.1057/s41599-024-02659-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-02659-5