Abstract

Although extensive research has examined the credit risk of real estate enterprises, the relationship between the political connection of real estate enterprises and these enterprises’ credit risk has not been formally studied. Using the panel data of 123 real estate listed companies in the Chinese stock market from 2008 to 2021, this paper finds a significant positive correlation between the political connection of private real estate listed companies and their credit risk. This phenomenon is attributed to the excessive debt that benefits from political connections since it may raise the credit risk of any real estate firm. Interestingly, considering that 2013 is the first year of China’s Internet finance era, we find that the popularity of Internet finance and other decentralized lending financing channels may enhance the impact of political connections on real estate credit risk. Our findings provide new micro evidence for the influencing factors and mechanism of credit risk of real estate enterprises during the recent “credit crisis” in the real estate market in China.

Similar content being viewed by others

Introduction

Since April 2007, the US subprime crisis has swept across the world as an unprecedented financial tsunami, which is mainly due to banks’ underestimation of the credit risk of the real estate industry. Since then, how to correctly understand the credit risk of real estate enterprises and the possible influencing factors attracted researchers’ attention (Davis and Zhu 2004; Kim 2013; Hu et al. 2018; Eichholtz 2021). Due to the impact of the epidemic, the real estate regulatory policy, the Federal Reserve’s interest rate increase, and other internal and external events, China’s real estate enterprises have been in crisis since 2021 (Li et al. 2021). Many highly leveraged real estate enterprises broke their capital chain and defaulted on their debts. For example, Evergrande Group has a debt of 200 billion yuan, and Blu-ray Group has a total capital gap of more than 150 billion yuan.Footnote 1 Other famous real estate enterprises such as Taihe Group, Huaxia Happiness, and Sunshine 100 China have also successively defaulted on bonds. According to the statistics of IFIND database, by September 2022, 173 real estate enterprises had defaulted on their credit bonds, with a default amount of nearly 170 billion yuan, accounting for 23% of the total default amount of credit bonds.

The credit risk of real estate enterprises is not only related to their own development but also affected by the entire financial system, which threatens the healthy development of the national economy. Guo Shuqing, secretary of the Party Committee of the People’s Bank of China, pointed out in the magazine Seeking Truth that “real estate is the biggest gray rhino threatening financial security”. Therefore, it is of great significance to study the influencing factors and mechanism of credit risk of Chinese real estate enterprises. The intricate relationship between the real estate industry and the government, shaped by policy and political ties, is particularly noteworthy. The influence of political connections on the credit risk of real estate enterprises is multifaceted. On the one hand, political connections, as a form of social capital, provide informational advantages and resources that can foster enterprise development. On the other hand, substantial political connections, often associated with investment opportunities, can also lead to over-investment.

In particular, under China’s current economic system, state-owned enterprises are inherently more closely connected with the government. In contrast, private enterprises are less controlled by the government. In order to obtain resource advantages, they often have a stronger motivation to “rent seeking” from the government, that is, to seek more political connections. Existing research on credit risk primarily focuses on factors such as policy adjustments and excessive expansion, yet tends to overlook the role of political connections. These connections represent an informal, special form of government-enterprise relationship that can increase leverage. Moreover, private real estate enterprises are often more motivated to seek political connections, a factor that should not be underestimated in understanding their credit risk dynamics. Examining the credit risk of real estate enterprises through their political correlation and considering the enterprise investment and financing efficiency are important supplements to the credit risk research of the real estate industry. Based on these, this paper mainly studies the research question that whether or not there is an impact of political correlation on the credit risk of private real estate enterprises. If there is, we further examine its impact mechanism through intermediary variables such as excessive debt.

According to the industry classification of the China Securities Regulatory Commission in 2012, this paper selects the panel data of 123 real estate listed companies in Chinese stock markets (Shanghai and Shenzhen A shares) from 2008 to 2021 as our research sample. Through the annual financial report of the real estate company and collecting the records of 5157 former or current government officials, representatives of the People’s Congress, and members of the Chinese People’s Political Consultative Conference (CPPCC), we score the strength of political connection of the real estate listed companies. The default probability EDF of listed real estate companies is calculated by KMV model to measure their credit risk. We find that (1) there is a significant positive correlation between the political connection of private real estate listed companies and their credit risk, which suggests that the higher the political connection, the higher their credit risk, while the state-owned real estate listed companies do not have this phenomenon. (2) The political connection of private real estate listed companies will lead to excessive debt, which may increase the pressure of debt repayment and eventually lead to the accumulation of credit risk. We have replaced the measurement method of political connection and credit risk and the two-stage least squares method to test the robustness of our results. (3) We further find that political connections play different roles in different industries and the fact that political connections can increase credit risk is a unique phenomenon of real estate. In addition, considering that 2013 is the first year of China’s Internet finance, it is interesting to find that the popularity of Internet finance and other decentralized lending channels, as well as the diversity of financing channels, make real estate enterprises more likely to enter the risk of excessive debt, leading the relative higher significance of the impact of political connections on real estate credit risk.

The remainder of this paper is organized as follows: Section “Empirical model and data” outlines the empirical models and presents the data. Section “Results” presents the empirical results. Section “Influence channel and heterogeneous impact analysis” examines the influence mechanism and discusses the heterogeneous impact of political connections on real estate credit risk. Section “Conclusion” concludes and discusses the policy implications.

Literature review

Credit risk of real estate enterprises

The real estate industry played an extremely important role in the Southeast Asian financial crisis in 1997 and the US subprime crisis in 2007. Therefore, the research on the credit risk of real estate enterprises has also attracted much attention. For instance, Davis and Zhu (2004) studied the relationship between the asset value of real estate enterprises and their credit risk. The study found that due to the profit-seeking nature of capital, real estate enterprises will expand their financing needs when house prices rise, while commercial banks also tend to increase loans for high-capital real estate enterprises, eventually increasing the foam and increasing credit risk. Kim (2013) deduced the probability of default and expected loss of commercial real estate mortgage loans under the Morton framework and believed that only when the net operating income and property value were lower than the threshold level the real estate enterprises would default. When studying the credit risk of the real estate industry in the United States, Eichholtz (2021) found that the credit cycle of the real estate industry significantly affects its default risk. Identifying the credit level of the real estate industry through indicators such as the overall debt water can effectively identify and prevent the credit risk of the real estate industry. Manz et al. (2021) analyzed the credit risk of real estate enterprises from the perspective of regional economics, believed that the economic development level of the region where the enterprise headquarters is located is an important indicator to study its credit risk, and proposed that the enterprise financing channel has a significant impact on its credit risk.

China’s real estate industry began to rise and gradually become market-oriented in the 1990s, and thus, the research on its credit risk started late. Early studies, such as Jin (2007), used the Credit Portfolio View (CPV) model to study the credit default risk of China’s real estate enterprises and found that the high debt ratio brought serious financial risks. The credit risk of China’s real estate enterprises is not sensitive to changes in house prices but is very sensitive to the credit policy of the real estate industry. Recently, Hu et al. (2018) studied the real estate credit risk measurement and its key indicators in China from five aspects: solvency index, profitability index, operational ability index, development ability index, and macroeconomic index. Following that, this paper studies and finds that the profitability and development ability of enterprises plays a more important role in the credit risk of real estate enterprises.

The impact of political connections on real estate enterprises

Political connection, that is, the informal relationship between enterprises and government, can provide enterprises with advantages in resource allocation. This paper introduces the political correlation of real estate enterprises for the first time and studies its impact on the credit risk of real estate enterprises. The real estate industry is extremely vulnerable to the guidance of national macro policies. In addition, land, a scarce resource controlled by the government, is the key to real estate development and operation. There are often various types of political connections between real estate enterprises and the government in order to obtain the advantages of information resources and other scarce resources. For real estate enterprises, the impact of political connection can run through the main process of project development, including early project planning and selection, land purchase and financing, and pre-sale approval.

Although there is no evidence found on the role of political connections on real estate credit risk, previous studies have also pointed out that political connections can affect the investment and financing process of enterprises. For example, Faccio (2006) found through a comparative study of more than 20000 enterprise samples from 27 countries that enterprises with higher political affiliation have higher asset-liability ratios and find it easier to obtain bank loans but also have higher default rates. Political connections could bring more financing channels for enterprises but also increase their credit risk. Yu and Pan (2008) found that political connections can reduce the tax burden for enterprises, and enterprises in higher tax areas will have a stronger tendency to establish political connections. Yu et al. (2012) found that political connection can indeed alleviate the financing constraints of enterprises, and its core mechanism is information effect and resource effect, of which resource effect plays a leading role. Based on the perspective of political connection and technological innovation, Yuan et al. (2015) examined whether Chinese enterprises had the curse effect of political resources and found that corporate political connection hindered the innovation activities of enterprises and reduced the efficiency of innovation. The latest research, such as Li and Jin (2021), Ding et al. (2023), Liu and Zhao (2023), and Brahma et al. (2023) further investigated the impact of quantitative political correlation on corporate performance, M&A performance, risk resistance, and other aspects. Different countries and regions adapt to different methods of defining political connections. Combined with China’s actual condition, political connection is defined as whether the chairman of the board, board members, or other senior executives have served in the government or as a representative of the National People’s Congress and the CPPCC. Corresponding to this definition, we assign the level of political connection.

To sum up, there has been a long line of literature on real estate credit risk, mainly focusing on its influencing factors and formation mechanism. Existing literature shows that real estate credit risk mainly arises from investment and financing efficiency. It is found that asset value, operating income, financing channels, financial hidden dangers, financing capacity, and other factors will have an impact on enterprise credit risk. Still, few articles discuss the impact of political connections on real estate credit risk. Therefore, this paper aims to fill this research gap and further explore whether the political connection affects credit risk through excessive debt.

Data and variables

Research method

The main regression model of panel data is constructed as follows:

In Eq. (1), \(EDF_{i,t}\) denotes real estate listed companies’ credit risk, \(PC_{i,t}\) represents political connection, \(controls_{i,t}\) represents control variables. Table 1 describes the definition of related variables. Equation (1) is applied to describe the relationship between political connection and credit risk (Chi et al. 2021). If the coefficient of political connection is significantly positive, it means that there is a positive correlation between political connection and credit risk of real estate listed companies. That is, the greater the political connection, the higher the credit risk. Reversely, if it is significantly negative, it means that there is a negative correlation between the political connection and the credit risk of the real estate listed companies, indicating that the greater the political connection, the lower the credit risk.

Data sources

Our sample includes Chinese A-share real estate listed companies from 2008 to 2021. Financial data of real estate listed companies are from the IFind database and the People’s Bank of China statistical database. Due to the credit risk of real estate listed companies, we exclude the samples of ST or *ST or PT occurred in the accounting year and the samples of listing suspension. Political connections of real estate listed companies are collected from the company’s annual financial report and manually collated by combining with Oriental Fortune (https://www.eastmoney.com/).

Dependent variable

As shown in Table 1, the credit risk (EDF) of real estate listed companies is calculated based on the KMV model: (1) We calculate the company’s equity value E and equity value volatility \(\sigma _E\), where where E = Net assets per share × Number of non − tradable shares + Daily closing price × Number of outstanding shares. (2) The relationship between the volatility of equity value and the volatility of asset value can be obtained by calculating the volatility of equity value according to the calculation method of historical volatility. (3) We calculate the default point DP = short − term liabilities + 0.5 × long − term liabilities. Default distance (DD) is calculated as the distance between the default point of any listed company and its asset value. (4) Assuming that the distribution of asset value follows the normal distribution, the default distance DD is its standard parameter, and the credit risk (the default probability, EDF) of the company can be obtained as N(-DD). The estimated EDF value ranges between 0 and 1. The higher the EDF value, the higher the credit risk of the enterprise.

Explanatory variables

First, the political connection (PC) indicates the degree of political relevance of senior executives by political relevance level and sets a sequenced variable. If the chairman or general manager of the enterprise has served or is currently serving in the government, the Party Committee (Discipline Inspection Commission), the People’s Congress or the Standing Committee of the CPPCC, the procuratorate and the court, the PC is assigned four levels: the value of section level cadre is 1, the value of department level cadre is 2, the value of department level cadre is 3, the value of ministerial level cadre is 4, and the value of non-political association is 0. If the chairman or general manager of an enterprise has served or is currently serving as a party representative, a representative of the People’s Congress or a member of the CPPCC, the value is also assigned at four levels: 1 at the district and county level, 2 at the municipal level, 3 at the provincial level, 4 at the national level, and 0 at the non-political level. If one enterprise is defined in two different levels, then the higher level is set as its political connect level.

Second, since the construction of the over-liability index in the impact mechanism analysis involves the largest shareholder holdings, asset-liability ratio, total asset growth rate, ROA, and company size, we control other enterprise-level variables such as management shareholdings, the proportion of independent directors, the number of senior executives, the growth rate of total operating income at the company level, and the macro-level variable M2 and GDP of the tertiary industry where the real estate is located.

According to the descriptive statistics in Table 2, the distribution of default probability of listed real estate companies is very scattered from 2008 to 2021, indicating that the credit risk spread of listed real estate companies in China is large and the risk management level is uneven. From the perspective of other control variables, the standard deviation of enterprise growth is large, which means that the main business growth of different enterprises in different years is highly volatile, and the average value is small. This is consistent with the evidence in the literature (Taufiq et al. 2020; Kousik et al. 2023), where real estate enterprises are found to have low growth. The classification of Chinese enterprises’ property rights can be broadly divided into two categories based on the presence of the government as the actual controller: state-owned enterprises (SOEs) and non-state-owned enterprises (Sun et al. 2020). The actual controllers of SOEs are typically the central or local State-Owned Assets Supervision and Administration Commission. In contrast, non-state-owned enterprises are generally controlled by natural persons or legal entities of private enterprises. Meanwhile, some studies regard state-owned shareholders in private enterprises as another channel for enterprises to establish political connections to examine the relationship between state-owned shareholders and the under-investment of private enterprises (Chen et al. 2011; Deng et al. 2020). However, as shown in Fig. 1, the histogram of political connections and the line of state-owned shareholders ratio in private enterprises have clearly different trends, indicating that the existing evidence based on state-owned shareholders ratio might not be able to explain the true relation between political connections and firms’ performances or risks.

Political connection and state-owned shareholders in private enterprises from 2008 to 2021. Political connection represents the degree of political relevance of senior executives by political relevance level and sets a sequenced variable. The histogram of political connection and the line of state-owned shareholders ratio in private enterprises are the sum of all private real estate enterprises. Private enterprises have a certain degree of connection with the political background of senior executives.

According to the Pearson correlation coefficient matrix of relevant variables shown in Table 3, the correlation coefficient between political connection and credit risk of listed real estate companies is 0.118, which is highly correlated at the significance level of 1%. The shareholding ratio of directors, supervisors and senior executives (Manager), the proportion of independent directors (Director), and the number of senior executives (Num) are significantly positively correlated with the political relevance of enterprises. The broad money supply (M2) and GDP of the tertiary industry are significantly negatively correlated with the political connection. Only the correlation between the growth rate of enterprise operating income and political connection is not significant, which indicates that it is necessary to control these variables in this study.

Results and discussion

The relationship between political connection and credit risk of private listed real estate companies

Throughout the baseline results of Table 4, there is a significant positive correlation between political connection and credit risk of private listed real estate companies, irrespective of adding control variables and controlling fixed effects.

In Column (1), we directly regress credit risk (EDF) on political connection (PC) without any control variables. The result shows that the estimated coefficient of PC is positive and significant, which indicates that with the increase of PC, the credit risk of private real estate listed companies will increase accordingly. In Columns (2) and (4), four enterprise-level and two macro-level control variables are further added. The estimated coefficients of PC remain significantly positive. In other words, the higher the political association, the higher the credit risk. Columns (3) and (5) of Table 4 present the results of re-estimating Eq. (1) by adding fixed effects, which is similar to the regression results obtained by controlling fixed effects before. This finding is consistent with that of Maurizio et al. (2022) and Kousik et al. (2023). They found that companies managed by politically involved managers or board members tend to have poor financial performance and higher financial leverage.

In light of the actual situation, private real estate enterprises are at a disadvantage in resource allocation. According to the rent-seeking theory written by Gordon Tullock (1967), private enterprises have a stronger motivation to “rent seeking” from the government to establish political connections. Private real estate enterprises mainly have two approaches to establishing politics. On the one hand, board members, senior executives and CEOs within the firm establish representative-type political connections by serving as deputies to the people’s congresses or members of the CPPCC at all levels, and the other is to establish government-type political connections by employing government resigning officials as directors and senior executives of the company, using the influence left by their government. No matter how the political connection is established, the manager’s personal motivation with political connection is consistent with the enterprise’s development goals to maximize the company’s profit. However, most executives with political connections normally have a “temporary” term and have double standards of political performance during the term of office. Therefore, they tend to expand the short-term profits of the enterprise in business decision-making, ignore the long-term development, increase the possibility of over-investment, and even lead to excessive liabilities.

Although political connections provide information advantages and resource convenience for private real estate enterprises, capital liquidity is still the main obstacle in development. Political connection is conducive to enterprises’ access to more policy support and tax incentives. There are also costs that businesses bear, such as the cost of obtaining political favors and lower management quality (Marianne et al. 2018; Maurizio et al. 2022). Consequently, greater recourse to political ties will require compensation for the potential benefits acquired, increasing costs for the company. High political task and high-yield model keep their debt ratio at high levels, which might bring more financial risks. The financing cost advantage brought by high political connections makes it difficult to cover the increase in financing risks. Schweizer et al. (2020) indicated that politically connected firms are more likely to issue corporate bonds as a debt financing instrument, which have weaker corporate governance and a surprisingly higher default probability. Therefore, the stronger the political connection, the greater the possibility of aggravating corporate credit risk.

Robustness tests: alternative variable measures

We replace the explanatory variables to conduct robustness tests referred to by Taufiq et al. (2020) and Li and Jin (2021): (1) eliminate the observations without political relevance; (2) use the binary political connection, the value is 1, and if there is no political connection, the value is 0. Replace the explained variable: referring to the research of Bharath and Shumway (2008), Merton DD is simplified and assigned: the market value of the company’s debt (D) is estimated as the book value of the debt (F). Company market value (V) = Debt market value (D)+ Equity market value (F), and debt volatility of each company is estimated by equity volatility: \(\sigma _D = 0.05 + 0.25\sigma _E\), an approximate estimation of the asset volatility (σV) by the weighted algorithm.

The expected return on assets is the risk-free interest rate (r), The specific value is the one-year fixed deposit rate published by the People’s Bank of China, and the debt maturity is set at 1. Substitute it into the formula \(DD^ \ast = {\textstyle{{{{{\mathrm{ln}}}}\left( {{{{\mathrm{V}}}}/{{{\mathrm{F}}}}} \right) + \left( {\mu - 1/2\sigma _{{{\mathrm{V}}}}^2} \right){{{\mathrm{T}}}}} \over {\sigma _{{{\mathrm{V}}}}\sqrt {{{\mathrm{T}}}} }}}\), and then calculate the default probability of the enterprise through the standard cumulative normal distribution function N(-DD*). Results are shown in Table 5 and all consistent to those in Table 4.

Endogeneity problems

To avoid endogeneity problems caused by measurement errors, explanatory variable omitted, and simultaneity, we refer to Marianne et al. (2018), Manz et al. (2021), and Maurizio et al. (2022). Firstly, we use the two-stage least square model, referred to as 2SLS, to solve endogenous problems. The instrumental variable used in the model is executive education background: 1=technical secondary school and below, 2 = junior college, 3 = undergraduate, 4 = master’s degree, 5 = doctoral student, 6=other (education published in other forms, such as honorary doctorate, correspondence, etc.), and 7 = MBA/EMBA as suggested by Li and Yu (2021). Wald chi-square test shows Wald χ² = 130.32, p = 0.000 < 0.05, which means the model is effective. According to test results, the F-statistic is 17.53 and greater than 10, indicating a strong correlation between instrumental and endogenous variables.

Secondly, the propensity score matching (PSM) method is employed to address the issue of selection bias and to control for confounding factors. PSM is predicated on the assumption that the two companies differ significantly in their political connections and are otherwise remarkably similar in other aspects. To implement PSM effectively, a range of firm-level control variables were selected. These include Size (represented by the logarithm of the enterprise’s market value), Solvency (measured as the Equity Ratio, or the proportion of shareholders’ equity to total assets), Investment Opportunity (quantified by Tobin’s Q, the ratio of asset market value to replacement cost), Growth Ability (indicated by AGR, the total asset growth rate), Profitability (assessed through ROA, the ratio of net profit to average total assets), and Development Ability (reflected by OGR, the operating income growth rate). These variables are detailed in Table 1 as matching variables for the study (Shao et al. 2021).

Figure 2 illustrates the variable balance before and after the matching process. As shown in Fig. 2a, the standard deviation of most variables has significantly decreased following the matching, with the bias for all covariates being reduced to less than 10%. In Fig. 2b, it is evident that most observed values fall within the common value range (on support), indicating that only a minimal number of samples are lost during the propensity score matching. However, values of the propensity score outside this common range are considered extreme.

a Variable standardization deviation. Variable standardization deviation is the output of the propensity score matching (PSM) approach. Covariates in PSM are solvency (equity ratio), investment opportunity (Tobin Q), growth ability (GROWTH), profitability (ROA), and development ability. (growth rate of operating income). The standard deviation of most variables has significantly decreased following the matching, with the bias for all covariates being reduced to less than 10%, indicating the match between the treatment and control groups is well balanced. b Common value range. Common support range is an important factor affecting the estimation effect of a specific matching method. The absence of a common support range indicated that the treatment and control groups were not comparable for propensity score analysis. Most observed values are within the common value range (on support); only a small number of samples will be lost when matching the tendency score. c Kernel density of propensity score. Kernel density describes whether there are differences between the two groups’ tendency scores before and after matching. The deviation of the kernel density curve between treatment and control groups before matching is relatively large, while the kernel density curve after matching is relatively close, indicating that the matching effect is good.

Kernel density can directly reflect whether there are differences between the two groups’ tendency scores before and after matching (Cheung et al. 2023). From Fig. 2c, we can find the deviation of the kernel density curve between the two groups before matching is relatively large, while the kernel density curve after matching is relatively close, indicating that the matching effect is good.

Matched control group samples may be the matching objects of multiple processing group samples, and thus, the importance of control group samples with different weights in overall control group samples is different. Therefore, as shown in Table 6, when comparing regression results, in addition to two benchmark regression columns (1) - (2), one regression using samples with non-empty weights (as shown in Column (3)) and one regression using samples that meet the common support hypothesis (as shown in Column (4)), a frequency-weighted regression considering the importance of samples (as shown in Column (5)) are also included. The regression results of the samples when using the propensity score matching are still significant.

Influence channel and heterogeneous impact analysis

Firstly, influence channel analysis. Enterprises with political connections will have a higher willingness to lend. On the one hand, reducing financing costs means enterprises are more likely to obtain “cheaper loans”. On the other hand, enterprises are eager to expand on a larger scale, resulting in an increase in the asset-liability ratio and financial risks.

The main reasons for private real estate companies’ excessive debt in order to expand investment are as follows. First, politically connected enterprises are more likely to obtain financing and increase the book-free cash flow, while the over-investment theory believes that the increase in book-free cash flow means an increase of over-investment probability (Zhang et al. 2014). Second, real estate has always been an important growth point of the local government’s economy, “GDP doctrine” before the economic transformation and upgrading often makes local government require its associated real estate enterprises to expand investment more blindly. Third, the professional knowledge of senior executives transferred from government departments is often lacking, and they are more likely to pursue short-term interests and over-invest. Eventually, excessive liabilities will be formed.

In our study, we adopt the methodology proposed by Lu et al. (2015) to calculate excessive liabilities, which serves as an indicator of the solvency and financial risks of listed real estate companies:

For a given firm i, the actual debt ratio is computed as the total debt divided by total assets. The variable SOE denotes the nature of the company’s property rights; it is assigned a value of 1 for state-owned enterprises and 0 for non-state enterprises, based on the nature of the actual controller. ROA represents the company’s profitability, calculated as net profit divided by total assets. IND signifies the industry median of the company’s asset-liability ratio. GROWTH reflects the company’s growth, measured as the total asset growth rate, which is the change in total assets from the end of the previous period to the end of the current period, divided by the total assets at the end of the previous period. FATA refers to the proportion of fixed assets in the company, calculated as fixed assets divided by total assets. SIZE is the natural logarithm of the company’s size, represented by total assets at the end of the period. FIRST indicates the shareholding ratio of the company’s largest shareholder.

The target liability ratio (LEVB*) is estimated using the Tobit regression model as outlined in formula (2). The degree of excessive debt (LEVB) is then determined by subtracting the actual debt ratio from the target debt ratio. This approach allows for a nuanced assessment of the real estate sector’s financial leverage and associated risks, particularly in the context of varying property rights and corporate structures.

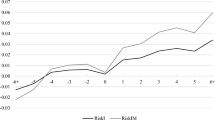

From the diagram of private enterprises’ excessive debt level and equity ratio in Fig. 3, we find that during high excessive debt years, which corresponds to the year with high political connection in Fig. 1, the solvency is poor. Intuitively, the higher the financial leverage, the worse the solvency. It carries some implications between political connections and excessive debt. The degree of excessive debt has declined recently.

The tendency of excessive debt and solvency from 2008 to 2021 are shown. Excessive debt is measured by the actual debt ratio minus the target debt ratio, and solvency is the equity ratio. During high excessive debt years, which correspond to the years with high political connections, the solvency is poor. The higher the financial leverage, the worse the solvency. However, the degree of excessive debt has declined recently.

In Table 7, two intermediary variables are used to investigate the influence channel: One is the asset-liability ratio (LEV), a financial indicator reflecting the solvency; and the other is excessive debt (LEVB), the compound indicator reflecting financial distress. Column (2) reports the estimated coefficient of the intermediary variable (LEV) is significantly positive, which means that the increasing asset-liability ratio will significantly improve the credit risk of enterprises. Political connection affects credit risk completely through the asset-liability ratio. In Column (3), political connection of private real estate listed companies is significantly positively correlated with excessive debt at the level of 10%, indicating that the higher the political connection, the more inclined the enterprises are to excessive debt. Column (4) of Table 7 reports a credit risk regression model considering excessive debt; the estimated coefficient of excessive debt and credit risk of private real estate listed companies is 1.17, which is significant at the level of 1%, indicating that the higher the degree of excessive debt of private real estate listed companies, the higher the credit risk.

Moreover, the estimated coefficient of political connection is 0.012, which is significant at the level of 5%, indicating that political correlation will affect credit risk by forming excessive debt. Our findings are consistent with Chkir et al. (2019) and Taufiq et al. (2020); politically connected firms experience a relatively lower cost of debt benefit from debtholders reducing the interest rate on debt. Further, private real estate listed companies make use of reducing the perception of default risk, and political connections grant these firms access to a higher debt level and higher leverage. Thus, politically connected firms had a significantly higher debt ratio and experienced a lower cost of debt.

Secondly, heterogeneous impact analysis. Baseline regression results show that the political connection of private real estate companies is significantly positively correlated with credit risk, indicating that the political connection of private real estate companies will aggravate credit risk. In order to further study the relationship between political connection and credit risk, we compare state-owned real estate listed companies with the construction industry, which has a high degree of correlation with the real estate industry and the manufacturing private listed companies, which account for 66.37% of the A-share listed companies (see Table 10).

Table 8 draws fascinating conclusions from sub-industry regression results: First, Columns (1) - (2) show a significant relationship between political connection and credit risk only exists in private enterprises instead of state-owned enterprises. Second, although the political connection and credit risk of private listed companies in the construction industry are significantly and positively correlated, the relationship between excessive debt and the political connection is not significant in Columns (3) - (4), which indicates that excessive debt is not an influence channel. Political connection in the manufacturing industry has no impact on credit risk. At the same time, political connection reduces excessive debt, while political connection in the manufacturing industry can increase technological innovation in Columns (5) - (7) (where Tech represents the number of companies affiliated to listed companies recognized as high-tech enterprises, innovative enterprises, and other qualifications). Our heterogeneous impact analysis reveals that political connections play different roles in different industries.

The year of 2013 is recognized as the inaugural year of Internet finance in China. Real estate enterprises may react differently to changes brought about by Internet finance. Table 9 shows the estimation result is positively significant between political connection and credit risk after 2013, while there is no significant evidence before 2013. It is interesting to find that the popularity of Internet finance and other decentralized lending channels, as well as the diversity of financing channels, make real estate enterprises more likely to enter the risk of excessive debt, leading to the relatively higher significance of the impact of political connections on real estate credit risk.

Conclusion

This paper delves into the impact of political connections on the credit risk of China’s private real estate firms, a crucial aspect of the nation’s economic stability. It highlights how local government priorities, driven by GDP growth and political performance, influence corporate decision-making, leading to potential over-indebtedness and investment failures. Understanding this dynamic is vital for addressing the risks associated with the real estate industry in China.

Existing research on political connections primarily examines their impact on corporate performance and innovation. However, there is a paucity of studies exploring the role of political connections in the realm of credit risk. The pervasive presence of political connections during China’s economic transformation and upgrading significantly influences the allocation of scarce resources, a phenomenon particularly pronounced in the real estate industry. Our research uncovers a notable positive correlation between the political connections of private listed real estate companies and their credit risk. More specifically, we observe that stronger political connections in private listed real estate firms correlate with increased levels of excessive debt and heightened debt repayment pressures, culminating in an accumulation of credit risks.

Conversely, state-owned real estate firms and related key industries show no increased debt due to political connections, indicating that credit risk amplification through such connections might be specific to the private real estate sector. Our findings have significant policy implications, suggesting ways for real estate companies to improve their management and mitigate credit risk. Additionally, this research offers guidance for government interaction with businesses, promoting sustainable growth in the real estate industry.

Several limitations to this study need to be acknowledged. Firstly, the scope of our definition of political connections is focused, primarily encompassing formal ties with current or former government officials, members of the People’s Congress, and CPPCC members. Future research could benefit from an expanded scope, considering a wider array of relationships, including personal friendships and affiliations with government departments or some leading financial institutions. Secondly, the sample of our study is only specific to a certain region and sector. Future studies may consider including a more diverse range of regions or countries as well as different sectors, thereby providing a more comprehensive analysis of the relationship between political connections and company credit risks.

Data availability

The datasets generated during and/or analyzed during the current study are available from the corresponding author upon reasonable request.

Notes

Evergrande Real Estate Group issued a notice on major matters involving major litigation and failure to repay matured debts on April 25, 2023 (https://www.evergrande.com/ir/sc/announcements.asp?year=2023). Finance-related data from notice announcement in Investor Relations of Blue Light Development Company Official Website (http://www.brc.com.cn/investor.aspx?t=3).

References

Bharath ST, Shumway T (2008) Forecasting default with the Merton distance to default model. Rev Financ Stud 21(3):1339–1369

Brahma S, Zhang J, Boateng A, Chioma N (2023) Political connection and M&A performance: Evidence from China. Int Rev Econ Financ 85:372–389

Chen S, Sun Z, Tang S, Wu D (2011) Government Intervention and Investment Efficiency: Evidence from China. J Corp Financ 17(2):259–271

Cheung YL, Mak BS, Shu H, Tan W (2023) Impact of financial investment on confidence in a happy future retirement. Int Rev Financ Anal 89:102784

Chi M, Muhammad S, Khan Z, Ali S, Li M (2021) Is centralization killing innovation? The success story of technological innovation in fiscally decentralized countries. Technol Forecast Soc Change 168(1):120731

Chkir I, Galleli MI, Toukabri M (2019) Political connections and corporate debt: Evidence from two U.S. election campaigns. Q Rev Econ Financ 75:229–239

Davis E, Zhu HB (2004) Bank Lending and Commercial Property Roales: Some Cross-Country Evidence. BIS Working Pap 150:1–37

Deng L, Jiang P, Li S, Liao M (2020) Government Intervention and Firm Investment. J Corp Financ 63:1–19

Ding H, Hu Y, Kim KA, Xie M (2023) Relationship-based debt financing of Chinese private sector firms: The role of social connections to banks versus political connections. J Corp Financ 78:102335

Eichholtz P (2021) The Total Return and Risk to Residential Real Estate. Rev Financ Stud 34(8):3608–3646

Faccio M (2006) Politically connected firms. Am Econ Rev 96(1):369–386

Hu S, Lei HH, Hu HQ (2018) Research on credit risk measurement of China’s real estate enterprises based on logistic model. China Soft Science 336(12):157–164

Jin FJ (2007) Research on measurement and forecast of the real estate credit risk basing on CPV model. Finance Forum 141(09):40–43

Kim Y (2013) Modeling of commercial real estate credit risks. Quant Financ 13(12):1977–1989

Kousik G, Ajay KM, Bhavik P (2023) Do Political connections influence investment decisions? Evidence from India. Financ Res Lett 52:103385

Li B, Li R, Wareewanich T (2021) Factors influencing large real estate companies’ competitiveness: A sustainable development perspective. Land 10(11):1239

Li SQ, Yu B (2021) Dispersion,consumer risk perception and transaction volume of P2P platform. J Financ Dev Res 476(08):42–50

Li X, Jin Y (2021) Do political connections improve corporate performance? Evidence from Chinese listed companies. Financ Res Lett 41:101871

Liu H, Zhao W (2023) The role of political connections in bad times: Evidence from the COVID-19 pandemic. Econ Lett 224:110999

Lu ZF, He J, Dou H (2015) Whose leverage is more excessed, SOEs or Non-SOEs? Econ Res J 50(12):54–67

Manz F, Müller B, Schiereck D (2021) The pricing of European non-performing real estate loan portfolios: Evidence on stock market evaluation of complex asset sales. J Bus Econ 90(7):1087–1120

Marianne B, Francis K, Antoinette S, David T (2018) The cost of political connections. Rev Financ 22(3):849–876

Maurizio LR, Francesco F, Francesco C, Neha N (2022) The relationship between political connections and firm performance: An empirical analysis in Europe. Financ Res Lett 49:103157

Schweizer D, Walker T, Zhang A (2020) False hopes and blind beliefs: How political connections affect China’s corporate bond market. J Bank Financ 151:106008

Shao XF, Li Y, Suseno Y, Li RYM, Gouliamos K, Yue XG, Luo Y (2021) How does facial recognition as an urban safety technology affect firm performance? The moderating role of the home country’s government subsidies. Saf Sci 143:105434

Sun S, Li T, Ma H, Li RYM, Gouliamos K, Zheng J, Yue XG (2020) Does employee quality affect corporate social responsibility? Evidence from China. Sustainability 12(7):2692

Taufiq A, Iftekhar H, Rezaul K (2020) Transactional and relational approaches to political connections and the cost of debt. J Corp Financ 65:0929–1199

Tullock G (1967) The welfare costs of tariffs, monopolies and theft. Econ Inq 5(3):224–232

Yu MG, Pan HB (2008) The relationship between politics, institutional environments and private enterprises’ access to bank loans. J Manag World 179(08):9–21+39+187

Yu W, Wang MJ, Jin XR (2012) Political connection and financing constraints: information effect and resource effect. Econ Res J 47(09):125–139

Yuan JG, Hou QS, Chen C (2015) The curse effect of enterprise’s political resources: An investigation based on political relevance and enterprise’s technological innovation. J Manag World 256(01):139–155

Zhang WD, Cheng ZC, Zhou DH (2014) Over-investment, diversification and local government intervention. Econ Rev 187(03):139–152

Acknowledgements

This work is partially supported by grants from the Major Program of National Social Science Foundation (No. 22&ZD073) and the National Natural Science Foundation of China (No. 72171051, 72101229).

Author information

Authors and Affiliations

Contributions

All persons who meet authorship criteria are listed as authors, and all authors certify that they have participated sufficiently in the work to take public responsibility for the content. In particular, the specific contributions made by each author is illustrated as following. RC: Conceptualization, Validation, Formal analysis, Funding acquisition. JY: Methodology, Investigation, Resources, Data Curation. CJ: Writing—Original, Visualization, Supervision. XC: Writing—Original. LY: Supervision, Validation, Writing—Review & Editing Preparation. SZ: Resources, Writing—Review & Editing Preparation.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

Informed consent was not required as this article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Chen, R., Yu, J., Jin, C. et al. Political connection and credit risk of real estate enterprises: evidence from stock market. Humanit Soc Sci Commun 11, 174 (2024). https://doi.org/10.1057/s41599-023-02522-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-02522-z