Abstract

In the post-COVID-19 pandemic era, the world faces a choice between trade protection and cooperation. However, current literature provides very little information on the benefit or loss of trade friction or cooperation on global economy and climate mitigation. This study applied the Global Trade Analysis Project model to assess the impacts of trade friction on global economic recovery and climate change. The results indicated that international trade friction can both delay global economic recovery and affect CO2 emission reduction. The shocks of consumption reduction and production suspension have a higher marginal effect in developing and emerging economies, whereas trade friction has a higher effect on developed countries. Trade friction has more negative economic effects for developed countries, but developing countries cannot reduce CO2 emissions proportionally with the decrease in trade and related production. In the post-pandemic era, if the global trade barrier increases, the world may face a co-occurring economic decline and an increase in or low abatement of carbon emissions.

Similar content being viewed by others

Introduction

The coronavirus (COVID-19) pandemic began in early 2020 (Callaway et al., 2020), greatly impacting the global economy and people’s lives and simultaneously posing a challenge to global cooperation toward climate change mitigation (Else, 2021; Dibley et al. 2021). There is a rising interest in simulating and modeling strategies for government intervention in economic development (Nishi et al., 2020; Bonaccorsi et al., 2020), substantially contributing to scientific advice on economic recovery domestically. However, with the increasingly complex global economy and severe climate change challenges, countries have different opinions on important issues such as economic cooperation and environmental governance. Although many countries have relaxed their requirements for pandemic control to varying degrees, trade friction remains. Notably, in the post-pandemic era, most countries are facing the dilemma of whether to engage in trade cooperation or avoid extensive trade to minimize the potential of another outbreak. Methods to restore social and economic balance and promote sustainable development goals are thus warranted (Thompson and Petric Howe, 2022); thus, it is necessary to evaluate the related impacts of trade friction.

As a major public health emergency, the COVID-19 pandemic has reduced the pace of global economic development and hindered the pre-pandemic international trade process (World Trade Organization, 2020). On January 30, 2020, the World Health Organization classified the COVID-19 epidemic as a “public health emergency of international concern.” By April 1, 2022, the cumulative confirmed cases of COVID-19 had exceeded 489.49 million worldwide, and the cumulative number of deaths had reached nearly 6.17 million(Worldmeter, 2022). The world economy shrank by 3.1% in 2020 (The Wolrd Bank, 2023) and is forecasted at 1.7 % in 2023 (The World Bank, 2023). This can be attributed to the continuous unstable economic supply chains worldwide. Global economic recovery is expected to be long-term, uneven, and highly uncertain (International Monetary Fund, 2021), which makes it necessary to prepare for various uncertainties to effectively tackle economic development and climate change from a global perspective.

For a long time, epidemiology and economic studies have investigated the economic impacts of pandemics, drawing on past events such as the influenza pandemic in the United States (Meltzer et al., 1999), H1N1 (Rassy and Smith, 2013), and avian flu (Alexander, 2007). Most of these pandemics happened in one region of the world. By comparison, COVID-19 poses numerous challenges to economic globalization and climate change (McNeely, 2021; Volkov, 2022). Economic globalization dominates in global development, grounded by the theories of the customs union, claiming that countries can expand their trades, optimize resource allocation, and achieve technological progress if a unified border is established with the implementation of tariff reduction (Viner, 2014) and global value chains, indicating that regions and countries in different segments of industrial chains can share value creation in global production networks (Yeung and Coe, 2015). After COVID-19, many scholars have been interested in investigating the ensuing impacts, analyzing the extent of the global economic downturn (Fernando and McKibbin, 2021), and the number and groups of people affected (Eichenbaum et al., 2021; Kaplan et al., 2020). The impacts on economic globalization is a novel theme but critically important, thus requiring exploration.

In addition to economic consequences, there are some studies on environmental impacts, especially on carbon emissions. Owing to stagnant production and the decline of service industries, such as tourism and transportation, many countries have experienced a reduction in greenhouse gas (GHG) emissions, including carbon dioxide. Some research has shown that carbon emissions decreased by 4–7% globally in 2020 (Le Quéré et al., 2020). However, some studies indicate such a reduction is negligible when correlated with the changes in global temperatures (Tollefson, 2021; Fyfe et al., 2021), and is even more limited for some countries such as Belgium (Lahcen et al., 2020). Moreover, CO2 emissions increased rapidly during the economic recovery process, even exceeding pre-pandemic levels (Zheng et al., 2020). Liu et al. (2020a) calculated the emissions of 29 countries based on industrial data and the transportation, business, and housing activities of 406 cities. They observed that fossil fuel emissions decreased by 5.8% in the first quarter of 2020 and global CO2 emissions decreased by 8.8% year-to-year in the first half of 2020; these periods of reduction corresponded to the lockdown measures adopted by the analyzed countries. Some studies also predicted that, given the continuation of the lockdown, although global emissions across economic sectors will decrease by 3.9–5.6% over the next five years, the subsequent fiscal incentives provided by 41 major countries will cause global emissions to increase by 4.7–16.4% (Shan et al., 2021). There is disagreement on the pandemic’s environmental impact and the global economic recovery.

In the post-pandemic era, the impacts of trade friction on the global economy and associated environmental impacts are critical questions and have become primary concerns for academia and policymakers. The pandemic has adversely affected the global supply chain and even low-carbon technology development (Goldthau and Hughes, 2020). The global trade growth was 2.7% in 2022, lower than 3.5% as the World Trade Organization estimated in Oct 2022, and is forecasted to be 1.7% in 2023. Therefore, the pandemic’s economic impact far exceeds that of the 2008 financial crisis (Baker et al., 2020). Nonetheless, some countries have considered to adopt measures, such as tariffs, to protect their trade and interests during the crisis (Organisation for Economic Co-operation and Development, 2020). Therefore, after the pandemic, trade friction is perhaps one of the main factors affecting global economic recovery.

These two aspects, that is, the global economy recovery and CO2 emissions, are correlated. In the intertwined network of the global industrial chain and resource utilization, owing to the differences in technical capabilities and industrial structures, the CO2 emissions of different countries vary, and the phenomenon of carbon emissions transfer persists (Chen et al., 2018; Liu et al., 2020b; Davis et al., 2011). Global trade significantly affects carbon emission patterns, and many scholars have evaluated the characteristics and relationship between the development of global and regional trade and climate change (Shughrue et al., 2020; Liu et al., 2020b; Davis et al., 2011). The disparity in the intensity of greenhouse gas emissions in different regions worldwide and changes in the production patterns caused by global trade are the main driving factors for the transfer of embodied pollutant emissions (Guan et al., 2020). Notably, blocking one country’s economic activities may decrease the emissions of other countries without lockdown policies (Shan et al., 2021). Since July 2020, lockdown measures have been lifted gradually, but trade friction still poses a serious challenge for sustainable post-pandemic global economic development. Thus, most countries face a crucial dilemma: should they choose trade friction or cooperation with international trade? This dilemma has complicated the mitigation of global climate change in the post-pandemic era, which is a significant research gap in current literature.

Therefore, this study aims to identify the possible impacts of trade friction on economies and CO2 emissions and classify these impacts on different countries and regions by considering scenarios with different barriers, namely consumption reduction, production suspension, and trade friction. It is hypothesized that trade friction affects the economy and carbon emissions differently among countries and could hinder sustainable development globally. This study is expected to make several contributions to the literature. First, different from other studies measuring the economic impacts of the pandemic on domestic economic loss (Tamasiga et al., 2022; Famiglietti and Leibovici, 2022; Zhang et al., 2021; Meltzer et al., 1999), we focus on the trade friction that arises with protectionism after the economic slump caused by the pandemic. Although this issue has attracted attention (Rammal et al., 2022; Khorana et al., 2022), in-depth investigation is required, especially on its impact on global economy. Second, we analyze CO2 emissions alongside global economic recovery to provide evidence for sustainable development post-pandemic. Although some literature finds reduction in CO2 emissions during the pandemic (Liu et al., 2020a; Le Quéré et al., 2020), little is known whether CO2 emissions increase with economic development post-pandemic. Third, we try to distinguish those impacts on different countries and regions. As countries and regions are at different stages of economic development and with different carbon emission intensities, which affect trade cooperation differently, and they adopted different measures to cope with the pandemic, we identify and compare the possible shocks of major pandemic outcomes, including trade friction, consumption reduction, and production suspension for different countries and regions. In general, the findings support the dire need for nations to work collaboratively to fight climate change in the face of potential trade frictions. Our analysis indicates we may be at a disadvantage regarding increased global trade friction. There is a need for global economies to partake in win-win cooperation and build a sustainable development path to achieve national and global sustainability and emissions goals.

Results

Shock of COVID-19 Pandemic on global economic development and CO2 emission

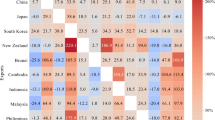

The impact of COVID-19 on major countries and EU region (%), calculated using GTAP analysis, are shown in Fig. 1. According to IMF data, a 6.1% increase in global gross domestic product (GDP) was observed in 2021 after a 3.1% decline in 2020, while economic growth decreased to 3.6% in 2022. According to the error analysis for each scenario (Table 4), the simulation results of the more optimistic scenario, S1, were the most similar to the actual economic situation in 2020, with an average error rate of 11.0%. The error rates with respect to China, the US, and Japan were below 5%. The simulation results reflected how the major countries were impacted by the pandemic with relatively high accuracy (see Materials and Methods).

Countries are ranked by GDP per capita of 2021.

The results show that the pandemic had varying degrees of impact on the economies of the analyzed countries. In all scenarios, the domestic shock (consumption reduction and production suspension) had the most significant impact on India, China, and the US, perhaps due to their large domestic consumption market and production, whereas the top three countries simultaneously affected by domestic and international trade friction (total shock) are the US, EU, and China, by ranking, largely reflecting their situation in global trade and economic power. This situation remained unchanged when the shocks increased from the low to medium and high levels.

In the three scenarios, our model simulates that global CO2 emissions decreased by 6.43, 10.72, and 15.67%, respectively, confirming that COVID curbed carbon emissions, but its effect was limited in 2020 (Tollefson, 2021). The reductions in emissions in China, India, Russia, and the US were the most significant. However, China still contributed to the global carbon emissions at a lower growth rate of 0.63%, as it still recorded positive economic growth, whose share of emissions exceeded 30% of the global carbon emissions in 2020 (S&P Global Platts, 2021). This was consistent with the projections of China’s carbon emissions in all scenarios considered in our study.

Scenarios of the impact of consumption reduction, production suspension, and trade friction on the global economy and CO2 emissions

With the increase in shocks, incremental domestic shock was higher for China and India than the US, whereas total shock increments were higher for the EU, China, US, UK, and Japan than other countries. Domestic shocks affected most developing countries and the US, whereas the opposite trend was observed when international trade friction was included. Developed economies were affected more by international trade friction, especially when incremental measures were considered. The incremental effect of domestic shock was low in the US compared to that of the EU and China, while the incremental effect of the total shock was highest in the US.

As consumption reduction, production suspension, and trade friction happened sequentially during the pandemic, the impact elasticity of the incremental change was employed to indicate the impact of the shock. The elasticity of production suspension was measured as the ratio between the incremental change from the impact caused by both consumption reduction and production suspension to one considering only consumption reduction. Similarly, the impact elasticity of trade friction was defined as the ratio between the incremental change in trade friction to the impact of the domestic shock only (see Materials and Methods for details).

The elasticity of the production suspension shock was larger than that of trade friction in the economies of many developing countries, including India, Russia, China, and Brazil (Table 1); moreover, it was higher for these countries compared to the global elasticity average. This is because they are countries with a large population and still undergoing industrialization, implying that the domestic market is more important for their economy. This was particularly evident in S3. Among all developed countries investigated in this study, only Australia showed a higher level of elasticity of production suspension shock than the global value in S3, which is likely because it is an island. By contrast, the elasticity of trade friction was larger for all developed countries than for developing countries for all the scenarios. Among the developing countries investigated, only Russia (in S1, S2, and S3) and China (in S1 and S2) had high trade friction elasticity when compared to the global value (0.13, 0.15, and 0.28, respectively). Among the investigated countries, India had the largest production suspension shock elasticity, which may be attributed to its developing status, scales of production, and consumer markets. South Korea was most affected by trade friction, as indicated by the high elasticity of this shock. This may likely be due to its high dependence on other economies (OECD, 2020).

Additionally, the elasticity of production suspension shock with respect to CO2 emissions differs substantially for some countries. Australia had a relatively high elasticity figure compared to other countries. Moreover, as Australia is an island, its carbon emissions was greatly affected by production suspension. In Japan, the elasticity of production suspension sharply changes from 1.68 in S1 to 0.19 in S3, reflecting that a deteriorating domestic production shock may not substantially affect carbon emissions because it uses a relatively small volume of its resources and energy for production. However, in the EU, the elasticity of the production suspension shock increased dramatically from −0.11 to 3.36 from S1 to S3. Notably, the economies of the 27 EU countries also showed negative changes due to the pandemic, but CO2 emissions continued to increase under impacts of consumption reduction of S1 and S2 (Fig. 1). According to actual carbon emission data, the CO2 emissions of the energy, ground transportation, and manufacturing industries in the 27 EU countries accounted for 31.3, 28.0, and 20.4% of the total carbon emissions in 2020, respectively. In other words, these emissions accounted for approximately 80% of the EU’s total carbon emissions, whereas the carbon emissions of EU residents only accounted for 20.1% in 2020 (Liu et al., 2020a). That is why consumption reduction does not reduce CO2 emissions; residents may stay home, there using more energy for heating and cooking, or use more ground transportation.

Generally, the elasticity of trade friction shock on CO2 emissions is higher for all investigated developed countries for all scenarios, except for the EU in scenarios S1 and S2. This observation may be attributed to the reduction of emissions in transportation sectors. More importantly, consumption and production in developed countries would be highly directly and indirectly affected by trade friction, as analyzed above, thereby reducing emissions.

Simulation of trade friction’s impact on economic growth and carbon emissions

Trade friction became critical post-COVID. Simulation S1 is very close to the current situation both economically and in terms of carbon emissions, and time is needed for consumption and production suspension to return to pre-pandemic values. Therefore, it is applicable to use this setting in S1 to further simulate the impact of trade friction on economic growth and carbon emissions. Based on the countries’ economic and trade data from 2019, we considered the following three (low-, medium-, and high-level) trade scenarios to project a future situation in which global economies may worsen with increased blockages: T1, T2, and T3 corresponding to 5, 10, and 15% increases in the import tax intensity, respectively.

Trade friction of varying degrees has a negative impact on global GDP growth (Table 2). As trade friction gradually increased, global GDP declined by 1.89, 4.75, and 8.30% in T1, T2, and T3, respectively, compared with the situation without trade friction. Among all investigated countries and EU region, the economic impact was the largest in the EU. As an economic union, it is possible that the preferential policies on tariffs implemented within the EU might be affected by the different shocks of the pandemic; this would have far-reaching effects on the economies of EU nations. The impact on the US and Russia was second only to that of the EU. In T3, the deterioration of trade conditions contributed to economic declines of 13.5, 9.76, and 6.69% in the EU, US, and Russia, respectively.

Notably, in T1, in which the import tax intensity increased by 5%, China and India’s GDPs increased slightly with the increased tariffs, indicating that trade friction can be a powerful means of trade protection. The rise in domestic import tax intensity can have a certain positive impact on domestic economic development for China and India, as these two countries can take advantage of their huge domestic markets to offset negative influences to some extent. However, the general rise in trade friction worldwide in scenarios T2 and T3 could hinder exports and lead to considerable negative GDP growth for China and India, which suffered declines of 8.18 and 5.06% in T3, respectively.

Different tariff levels trigger different CO2 scenarios globally and across countries. Notably, in the T3 scenario, in which the global economy may be affected severely, the deterioration of countries’ trade environment increased the reduction of CO2 emissions by 2.16%, whereas in the T1 scenario, the CO2 emissions may increase by 0.62%. One possible situation is that industries return to home countries with global trade friction, thus contributing to the increase in CO2 emissions. For instance, in the T1 scenario, CO2 emissions in the US increased slightly by 0.59%, while its GDP declined by 6.64%. Moreover, countries and regions may expand the use of their resources and energy to offset the loss of the global trade barrier.

Therefore, it is likely that increasing trade barriers will bring about a decline in the economic level of major countries and regions worldwide. Still, the magnitude of reduction in CO2 emissions may be far less than the decline in economic growth. In scenarios T1, T2, and T3, CO2 emissions increased or decreased to a much lower degree than the reduction of economies. Trade protectionism adversely impacted the global economy and environment. Although higher trade friction (e.g., countries in the T3 scenario) portrayed a certain promotional effect in reducing global CO2 emissions, this contribution to emission reduction was achieved by abandoning a higher rate of economic growth, which was not sustainable.

Discussion

International trade friction can not only delay the process of global economic recovery but also affect CO2 emission reduction. Our study demonstrated that the marginal effect of production suspension shocks on developing countries was higher than that of the international trade friction in both economies and carbon emissions. For developed countries and regions such as the US and EU, the marginal effect of international trade friction was substantially higher than that of production suspension shock. Developed countries may face considerable economic recessions owing to global trade friction. Many countries have lifted economic restrictions in the post-COVID era; however, pressures on the global economy and carbon emissions may still increase if international trade barriers rise. Global trade friction can have considerable negative effects on the economies of developed countries and a relatively lower effect on the CO2 emissions of developing countries. Therefore, this situation implies a decline in economic growth and a rise in carbon emissions globally.

As the economy recovers and transforms, it is still necessary to adopt low-carbon technologies and ensure a low-carbon economy. The temporary carbon emissions reduction due to the shocks of the pandemic did not immediately reduce the concentration of CO2 but only slowed emissions. Fortunately, the economic shock brought by the pandemic in 2020 has considerably affected the energy market. Primary energy consumption and carbon emissions have both reduced rapidly since World War II, decreasing by 4.5 and 6.3% globally, respectively, which are the lowest levels since 2011 (S&P Global Platts, 2021). Simultaneously, renewable installations, such as wind, solar, and hydroelectric power are increasing (Kim et al., 2023; Ledmaoui et al., 2023). The downside is that, although governmental pandemic-related spending has reached USD 12 trillion globally, accounting for 12% of global GDP in 2020, most countries and regions have largely missed the opportunity for fiscal rescue and recovery measures to stimulate their economies and promote the transition to a low-carbon economy. Pandemic-related financial expenditures mainly supported the current global economic status and were dominated by high carbon production (United Nations Environment Programme, 2020). Therefore, it may be necessary to accelerate the shift to low-carbon production (Hanna et al., 2020) and trade, promote international economic and trade cooperation, and continue to work together to fight climate change in the face of potential trade frictions in the post-pandemic era.

Materials and Methods

Scenario design

Considering that countries are connected with various industrial linkages in the global economy and that the economic system operates through feedback loops from production to consumption, this study used the Global Trade Analysis Project (GTAP) (Aguiar et al., 2019) model to analyze possible post-pandemic scenarios of global economic development and carbon emissions. Analysis based on the GTAP model requires a large amount of national and regional data. Subject to data availability, we referenced the analysis and compared it with the actual situation in 2020. We examined data on consumption, production suspension, and trade friction from 129 countries and classified them as main countries and EU region to simplify the analysis. Referring to Tian (2020), we considered three levels: low-, medium-, and high-level, for the analysis (Table 3). In the simulation, the impact are referred to as shocks. The different types of shocks were subsequently added in different scenarios, including consumption demand shock, domestic shock (both consumption reduction and production suspension), and the shock of both domestic shock and trade friction. Production suspension can be measured with labor supply. Trade friction represents a state of international economic affairs, which usually affect a country’s export. The magnitude of these shocks was measured as incremental changes in the relative percentage of the corresponding indicators resulting from the shocks.

Constructing a global computable general equilibrium (CGE) model

The GTAP model developed in this study under the CGE framework was mainly based on an open economic model including four economic entities: residents, enterprises, governments, and foreign countries (Aguiar et al., 2019). The model considered economic and production activities, such as production input, consumption, government purchase, savings, taxation, and transfer payment, as well as import and export. The module was divided into six submodules: production, commodity trade, resident, enterprise, government, equilibrium, and macro closure. Each country’s carbon emissions module was constructed based on the above-mentioned benchmark modules.

Production module

In this study, all production sectors were placed in Set A, while all commodity sectors were placed in Set C. For ease of analysis, we assumed that every production activity sector produced only one commodity. A two-level nested form of CES function was used as the production function. In the first level of the production function, the composite factor input, QVA, and the composite intermediate commodity input, QINTA, formed the total output (or total supply), QA, in the form of a CES function, as shown in Eq. (1). In the second-level function, we assumed that there were only two production factors, labor and capital, inputted to the value-added part of the production function, as shown in Eq. (4). A Leontief production function was used in the intermediate input part of the production function.

where \(\alpha _a^A\) denotes the total factor productivity of production activity sector a and \(\delta _a^A\) is the share parameter of the composite factor input of production activity sector a. Parameter ρa=1−1⁄ε, where ε denotes the elasticity of substitution of the CES function.

The prices of all inputs and outputs in the production activities, PA, PVA, and PINTA, can be obtained from the first-order condition of cost minimization, whose relationships with QA, QVA, QINTA, are as shown in Eqs. (2), (3), (5) and (6).

where PA, PVA, and PINTA denote the prices of production activities, value-added part (including the value-added tax, VAT), and intermediate inputs, respectively. ta denotes all other production tax rates, except VAT.

where WL and WK denote the price of labor and capital factors, respectively. tval and tvak denote the rates of labor VAT and capital gains tax, respectively. QLD and QKD denote the demands for labor and capital factors of production activities, respectively.

where QINTca denotes the demand of production activity a for immediate input commodity c, PINTca denotes the price of production activity a for immediate input commodity c, while PQc denotes the price of commodity c in the domestic market; icaca is the input–output coefficient of the intermediate input part, indicating the quantity of commodity c required for a unit output of sector a.

Trade module

In our analysis, the domestically produced commodity (QA) was divided into two parts: domestic sales (QDA) and export (QE). Their substitution relationship was expressed by a constant elasticity of transformation (CET) function, as shown in Eq. (9). The changes in the relative prices of domestic sales and export affected the relative quantities of domestic sales and exports, being determined by the optimized first-order conditions, as shown in Eq. (10). The relationship between the production price of a sector of activity and the prices of domestic sales and export is shown in Eq. (11). The price of the export commodity was determined using the international price of exported commodity and the exchange rate, as shown in Eq. (12).

where QDAa denotes the quantity of commodity for domestic selling, whose price is PDAa. QEa denotes the quantity of the export commodity, whose price is PEa. pwea denotes the international price of the exported commodity from production activity sector a and EXR denotes the exchange rate. Equations (9), (10), (11) and (12) form the export module for the production activity sector a.

The commodity supplied in the domestic market (QQc) was divided into two parts: one that denotes domestically produced and domestically sold commodities (QDCc) and one that denotes imported commodities (QMc). The substitution relationship between the two was described with Armington’s conditions, as shown in Eq. (13). The relationships of their prices and quantities could be derived using the optimized first-order conditions, as shown in Eqs. (14) and (15). The price of the import commodity was determined using the international price of imported commodity, import tax rate, and exchange rate, as shown in Eq. (16). The commodities supplied in the domestic market were considered the final demands of the economic entities in the country, including the residents, enterprises, and government. In addition, we considered the intermediate input demands of production activities.

where QQc denotes the quantity of commodities supplied in the domestic market, QDCc denotes the quantity of commodities produced and sold domestically, and QMc denotes the imported commodities. Their prices are denoted as PQc, PDCc, and PMc, respectively. pwmc denotes the international price of imported commodity c, and tmc denotes the import tax rate of commodity c. Equations (13), (14), (15), and (16) form the import module for the commodity c.

As there is a one-to-one correspondence between activities and commodities, the activities of domestic production and domestic sales correspond to the commodity prices and quantity, which can be expressed as follows:

where IDENTac denotes the correspondence between production activity a and commodity c. Equations (1)–(18) describe the relationships between the production modules, including those between activities and commodities.

Resident module

Residents’ incomes come mainly from labor remuneration and capital factor income, as well as transfer payments paid to the residents by government departments and the enterprise sector, which can be expressed as in Eq. (19).

where YH denotes residents’ total income. transfrhgov denotes transfer payments paid by government departments to residents and transfrhent denotes transfer payments paid by the enterprise sector. QLS is the total labor supply and QKS is the total capital supply. Capital factor income is distributed to enterprises and residents, and shrhk is the proportion of capital factor income distributed to residents.

In Eq. (20), PQc denotes the price of commodity c, and QHc denotes residents’ demands for commodityc. Residents’ disposable income is denoted by (1-tih)YH, where tih is the residents’ personal income tax rate, while residents’ propensity to consume (mpc) determines the consumption level of residents; shrhc denotes the consumption ratio of residents on commodity c, derived from the data in the input–output table.

The utility function is a Cobb–Douglas function, and consumer demand for commodity c was derived from the first-order condition for utility maximization.

Enterprise module

Enterprises’ incomes come from the capital factor income distributed to enterprises, as shown in Eq. (21). Enterprises’ savings are equal to their income minus taxes and the transfer payment paid to residents, as shown in Eq. (22). A firm’s total investment, that is, capital formation, consists of investments in various sectors, as shown in Eq. (23), assuming that investments are exogenous.

where YENT denotes the enterprises’ total incomes and shrentk is the proportion of capital factor income distributed to the enterprises. ENTSAV denotes the enterprises’ total savings, tient is their income tax rate, and transfrhent denotes the transfer payment paid by enterprises for residents. ENIV denotes a firm’s total investment value, and \(\overline {QINV_c}\) denotes the average demand for commodity c in all sectors.

Government module

Government revenue is mainly composed of the VAT collected from production activities, corporate income tax collected from enterprises, and personal income tax collected from residents, along with various other taxes, including import duties and service taxes, as shown in Eq. (24). Government expenditure mainly includes the government’s consumption of commodities and transfer payments spent for residents, as shown in Eq. (25).

where YG denotes the government’s total income, EG the government’s total expenditure, and QGc the government’s demands for commodity c.

Assume that the proportion of government consumption on commodity c (shrgc) can be determined by the structure of the data in the input–output table, the above function can be re-expressed as follows:

Equilibrium and macro closure module

In this study, we adopted the conditions of neoclassical closure, that is, total demand of commodity c equals its supply, as shown in Eq. (27); labor demand equals labor supply, as shown in Eq. (28); and capital demand equals capital supply, as shown in Eq. (29). Equations (27)–(29) show that when general equilibrium is reached, the foreign exchange receipts and payments of all markets, including the commodity, factor, and international markets, reach a state of clearing.

where QHch denotes the demand of resident h for commodity c. \(\overline {QLS}\) denotes the average labor supply of all sectors, and \(\overline {QKS}\) denotes the average capital supply of all sectors.

The difference between the government’s revenue and expenditure is the government’s net savings (GSAV). When GSAV is positive, there is a fiscal surplus; if it is negative, there is a fiscal deficit. Fiscal balance is not required here; therefore, GSAV is endogenous and can be calculated as follows:

China has adopted a managed floating exchange rate system. For ease of analysis, we assumed that the exchange rate (EXR) was fixed and the foreign exchange receipts and payments were generally unbalanced. The foreign savings (FSAV) adjust the surpluses or deficits of the foreign exchange receipts and payments, so that foreign revenue and expenditure maintain a balance. This can be expressed as follows:

where pwmc denotes the international price of imported commodity c, and QMc denotes the quantity of imported commodity c when EXR denotes the exchange rate. pwea denotes the international price of the exported commodity from production activity sector a, and QEa denotes the quantity of export commodity produced domestically from production activity sector a. The foreign savings (FSAV) multiplied by the exchange rate (EXR) is the residual term to adjust the surpluses or deficits of foreign exchange receipts and payments.

The GDP and PGDP were calculated using the following equations:

where GDP is the gross domestic product and PGDP denotes the GDP index. The definitions of all other variables in Eqs. (32) and (33) are the same as above.

Carbon emissions module

Let CI and CH as denote the carbon emissions of production sector and residents’ consumption, respectively:

where δji refers to the carbon emission coefficient of fossil energy i burned by production sector j, δHi refers to the carbon emission coefficient of fossil energy i burned by residents, Qb refers to residents’ consumption demand for commodity b, and ZHi refers to total domestic demand for class I synthetic products. Carbon emission intensity I can be expressed as the ratio of total carbon emission to GDP:

Referring to Zhang (2021), we considered macroeconomic indicators, such as GDP growth rates and industrial indices of various sectors, as endogenous variables, and populations, investments, skilled labor, and unskilled labor as exogenous variables to fit to the data of the industrial emissions intensity (kg/PPP USD of GDP) of different sectors in the regions. Therefore, we were able to generate a carbon emissions module in a baseline scenario of economic growth without the interference of external factors, while successfully considering a global scenario.

Error analysis

For the three shock scenarios and the overlay situations, the error rates of the scenarios were calculated separately using the following formula:

Table 4 shows the analysis of the error results based on actual GDP data for 2020 (International Monetary Fund, 2021). The results show that S1 was closer to the actual situation, whereas S2 and S3 simulate worse situations.

The pandemic’s impact on the economy and carbon emissions is more complex and uncertain than that of different policies, as a pandemic is a type of natural disaster. Moreover, policy interventions, degree of reaction, and reaction time varies among countries, which will affect the impact paths of countries. Hence, there is a certain gap between the simulation results and the absolute value of the real situation. The main function of this model is scenario analysis, not prediction. As a static CGE model for global multi regional comparison, GTAP artificially sets a scenario with reasonable external impact, and then fits the impact of preset shocks on different countries, industries, and sectors using national input–output activities and economic and trade links. It is an effective simulation tool for policy analysis and to study the impacts of variables. However, it is not an accurate prediction model and is affected by the errors in the impact scenarios and regional groups. In addition, setting the impact degree to a unified level is also one of the main issues of this type of analysis. However, there are few relevant studies on error analysis.

This study verifies the simulation results by comparing the simulated data with the actual data for 2020 (Liu et al., 2020a). According to the error analysis of each scenario, the simulation results of the more optimistic scenario, S1, were the most consistent with the actual economic and carbon emission situation in 2020. The average economic error rate was 11.0 %, and the average carbon emission error rate was 5.75% in S1. The simulation results of the S1 scenario reflect the real situation of the economic and carbon emission impact caused by the pandemic in major countries at an error level of < 15%. In general, the scenario set for the present study is reasonable and the model adopts a short-term closed mode to effectively simulate the pandemic’s impact. Countries showed different adaptabilities to the pandemic and the level of policy intervention. This resulted in a certain deviation from the actual economy and carbon emissions of countries, but this deviation was within the allowable error range of the model. Hence, it did affect the corresponding simulation analysis and conclusions of this study.

Elasticity analysis of pandemic shock simulation

Although the three types of shocks determined in this study have specific characteristics, they overlapped. Under the influences of social distancing and income, the pandemic directly affected consumption, while labor shortages resulted in production suspension. Additionally, trade friction may further impact the economy and increase CO2 emissions. The three types of shocks studied here are progressive and crucial to achieve balance in the post-pandemic scenario. To further measure the problems caused by production suspension and trade friction, we considered the elasticity coefficient of production suspension by measuring the incremental impact of production suspension from consumption reduction on economic development. Similarly, we measured trade elasticity by calculating the ratio of incremental impact from domestic shock to both domestic and trade friction. These are expressed as follows:

where φcl and ωli are production suspension elasticity and trade elasticity, respectively, and Ic, Il, and Ii denote the impacts of the three shocks, namely, consumption reduction, domestic shock (consumption reduction plus production suspension), and trade friction plus domestic shock.

Data sources and processing

The GTAP database is a global data network that supports the calculations of simulation analysis using a CGE model. It contains the data from the input-output tables of 57 industries from 140 countries and regions, with 2014 as the base year. To construct the GTAP database in this study, macroeconomic data were used to update the regional input-output tables of 2019 for analysis. First, the coefficients in the regional input-output tables were measured (using their own national currencies) based on the ratio of GDP calculated from the input-output tables and external GDP data in the current USD value. Second, we used the coefficients to update the values from the regional input-output tables, including private consumption (C), gross fixed capital formation (I), and government consumption (G). Third, we used macroeconomic data to expand various datasets to the coverage of standard countries/regions and as weights to aggregate data from the standard countries/regions to the GTAP regions. For example, the GDP and GDP shares were used to expand the trade datasets to the GTAP standard countries. Fourth, GDP data were also used as weights to aggregate the data of domestic support, factor shares, and labor shares from the standard countries to the GTAP regions. Finally, macroeconomic data, government consumption, and GDP were used to examine and revise the share of government consumption in each input-output table to ensure a uniform treatment of government consumption expenditures of all countries.

CO2 emissions are based on the PRIMAP-hist dataset(Gütschow et al., 2021), which combines existing datasets to create a comprehensive set of GHG emission pathways. They include data from 1850 to 2018 for all member states of the United Nations Framework Convention on Climate Change (UNFCCC), as well as most non-UNFCCC countries and regions. The data covers the main categories identified by the Intergovernmental Panel on Climate Change. The subsector data for energy, industrial processes, and agriculture is available for CO2, CH4, and N2O.

Data processing

To simplify the analysis, we reclassified the countries (regions) in the GTAP database according to the study’s focus and reclassified 57 sectors into 19 national economic sectors according to the industrial classification of national economic activities. The included 19 sectors are agriculture, forestry, animal husbandry, and fishery; mining; manufacturing; electricity, heat, gas, and water production and supply; construction; wholesale and retail; transportation, storage, and postal services; accommodation and catering; information transmission, software, and information technology services; finance; real estate; lease; scientific research and technology services; water conservancy, environment, and public facilities management; residential services, repair, and other services; education; health and social work; culture, sports, and entertainment; and public administration, social security, and social organizations.

As 2014 was the base year of the GTAP database, to reflect the economic development and changes in countries’ foreign trade policies and improve the prediction accuracy of the simulation results, based on the actual data from 2007 to 2019, we adopted Walmsley’s dynamic recursion to adjust the changes in the dataset parameters, including population, non-skilled and skilled labor, and natural endowments, and upgrade the capital stocks. The economic indicators were mainly from IMF forecast data, which can largely reflect the COVID-19 pandemic’s real impact on the economy in 2020. The calculation formula of capital stock is as follows:

where Kt(r) is the capital stock of region r in year t, kt(r) is the rate of change of the capital stock of region r in year t, Kt-1(r) is the capital stock of region r in year t-1, kt-1(r) is the rate of change of the capital stock of region r in year t-1, and DEPR is the capital depreciation rate, set at 4% following the method of Walmsley et al (2000). GDI(r) is the outbound investment of region r, and GDIt(r) is the rate of change in the outbound investment of region r.

According to the public data on global banks, we calculated the intensity of GHG emissions based on the countries’ CO2 emissions and economic data from 1990 to 2016, and conducted trend fitting and extrapolation to obtain the data of each country’s intensity and volume of GHG emissions until 2020. On this basis, the GTAP model was used to simulate the possible scenarios of shocks caused by the COVID-19 pandemic, while mainly interpreting the impacts of consumption, labor supply, and trade shocks on the global macro economy and that of indirect shocks on countries’ GHG emissions; this helped us analyze the pandemic’s impact on global climate change.

Data availability

The GTAP and data can be retrieved from Global Trade Analysis Project (https://www.gtap.agecon.purdue.edu), and the CO2 emission data is from PRIMAP (https://primap.org/primap-hist/).

References

The UN must get on with appointing its new science board 2021. Nature 600(7888):189–190

Aguiar A, Chepeliev M, Corong E et al. (2019) The GTAP Data Base: Version 10. Journal of Global Economic Analysis 41(1):1–27

Alexander DJ (2007) Summary of avian influenza activity in Europe, Asia, Africa, and Australasia, 2002-2006. Avian Diseases 51(1):161–166

Baker S, Bloom N, Davis S, et al. (2020) COVID-Induced Economic Uncertainty. NBER Working Papers 26983, National Bureau of Economic Research, Inc

Bonaccorsi G, Pierri F, Cinelli M et al. (2020) Economic and social consequences of human mobility restrictions under COVID-19. Proceedings of the National Academy of Sciences 117(27):15530–15535

Callaway E, Ledford H, Viglione G et al. (2020) COVID and 2020. Nature 588(7839):550–552

Chen Z-M, Ohshita S, Lenzen M et al. (2018) Consumption-based greenhouse gas emissions accounting with capital stock change highlights dynamics of fast-developing countries. Nature Communications 9(1):3581

Davis SJ, Peters GP, Caldeira K (2011) The supply chain of CO2 emissions. Proceedings of the National Academy of Sciences 108(45):18554–18559

Dibley A, Wetzer T, Hepburn C (2021) National COVID debts: climate change imperils countries’ ability to repay. Nature 592(7853):184–187

Eichenbaum MS, Rebelo S, Trabandt M (2021) The Macroeconomics of Epidemics. The Review of Financial Studies 34(11):5149–5187

Else H (2021) The science events to watch for in 2021. Nature 589(7840):14–15

Famiglietti M, Leibovici F (2022) The impact of health and economic policies on the spread of COVID-19 and economic activity. European Economic Review 144

Fernando R, McKibbin WJ (2021) The policy that is most supportive of a global economic recovery is the successfully implemented public health policy. Reportno. Report Number|, Date. Place Published|: Institution|

Fyfe JC, Kharin VV, Swart N et al. (2021) Quantifying the influence of short-term emission reductions on climate. Science Advances 7(10):eabf7133

Goldthau A, Hughes L (2020) Protect global supply chains for low-carbon technologies. Nature 585(7823):28–30

Guan D, Wang D, Hallegatte S et al. (2020) Global supply-chain effects of COVID-19 control measures. Nature Human Behaviour 4(6):577–587

Gütschow J, Günther A, Pflüger M (2021) The PRIMAP-hist national historical emissions time series (1750-2019). v2.3.1. zenodo. https://doi.org/10.5281/zenodo.5494497

Hanna R, Xu Y, Victor DG (2020) After COVID-19, green investment must deliver jobs to get political traction. Nature 582(7811):178–180

International Monetary Fund (2021) World Economic Outlook, April 2021: Managing Divergent Recoveries

Kaplan G, Mitman K, Violante GL (2020) Non-durable consumption and housing net worth in the Great Recession: Evidence from easily accessible data. Journal of Public Economics 189:104176

Khorana S, Escaith H, Ali S et al. (2022) The changing contours of global value chains post-COVID: Evidence from the Commonwealth. Journal of Business Research 153:75–86

Kim M, Park T, Jeong J, et al. (2023) Stochastic optimization of home energy management system using clustered quantile scenario reduction. Applied Energy 349

Lahcen B, Brusselaers J, Vrancken K et al. (2020) Green Recovery Policies for the COVID-19 Crisis: Modelling the Impact on the Economy and Greenhouse Gas Emissions. Environmental & Resource Economics 76(4):731–750

Le Quéré C, Jackson RB, Jones MW et al. (2020) Temporary reduction in daily global CO2 emissions during the COVID-19 forced confinement. Nature Climate Change 10(7):647–653

Ledmaoui Y, El Maghraoui A, El, Aroussi M et al. (2023) Forecasting solar energy production: A comparative study of machine learning algorithms. Energy Reports 10:1004–1012

Liu Z, Ciais P, Deng Z et al. (2020a) Near-real-time monitoring of global CO2 emissions reveals the effects of the COVID-19 pandemic. Nature Communications 11:1

Liu Z, Meng J, Deng Z et al. (2020b) Embodied carbon emissions in China-US trade. Science China Earth Sciences 63(10):1577–1586

McNeely JA (2021) Nature and COVID-19: The pandemic, the environment, and the way ahead. Ambio 50(4):767–781

Meltzer MI, Cox NJ, Fukuda K (1999) The economic impact of pandemic influenza in the United States: Priorities for intervention. Emerging Infectious Diseases 5(5):659–671

Nishi A, Dewey G, Endo A et al. (2020) Network interventions for managing the COVID-19 pandemic and sustaining economy. Proceedings of the National Academy of Sciences 117(48):30285–30294

OECD (2020) OECD Economic Surveys: Korea

Organisation for Economic Co-operation and Development (2020) COVID-19 and international trade: Issues and actions

Rammal HG, Rose EL, Ghauri PN et al. (2022) Economic nationalism and internationalization of services: Review and research agenda. Journal of World Business 57:3

Rassy D, Smith RD (2013) The economic impact of H1N1 on Mexico’s tourist and pork sectors. Health Economics 22(7):824–834

S&P Global Platts (2021) bp Statistical Review of World Energy 2021. London, the UK

Shan Y, Ou J, Wang D et al. (2021) Impacts of COVID-19 and fiscal stimuli on global emissions and the Paris Agreement. Nature Climate Change 11(3):200–206

Shughrue C, Werner BT, Seto KC (2020) Global spread of local cyclone damages through urban trade networks. Nature Sustainability 3(8):606–613

Tamasiga P, Guta AT, Onyeaka H et al. (2022) The impact of socio-economic indicators on COVID-19: an empirical multivariate analysis of sub-Saharan African countries. Journal of social and economic development 24(2):493–510

The Wolrd Bank (2023) Data Bank

The World Bank (2023) Global Economic Prospects

Thompson B, Petric Howe N (2022) COVID stimulus spending failed to deliver on climate promises. Nature. https://doi.org/10.1038/d41586-022-00630-5

Tian S (2020) The impact of COVID-19 epidemic and its response policies on China’s macro economy: An analysis based on a computable general equilibrium model (in Chinese). Consumer Economics 36(3):42–52

Tollefson J (2021) COVID curbed carbon emissions in 2020 - but not by much. Nature 589(7842):343

United Nations Environment Programme (2020) Emissions Gap Report 2020

Viner J (2014) The Customs Union Issue. Oxford University Press, Great Clarendon Street, Oxford

Volkov A (2022) The Political Implications of COVID-19 for Globalization: Ways to Develop a Global World After the Pandemic. European Review 30(6):773–787

Walmsley TL, Dimaranan BV, Mcdougall RA (2000) A base case scenario for dynamic GTAP model

World Trade Organization (2020) Trade set to plunge as COVID-19 pandemic upends global economy

Worldmeter (2022) COVID-19 CORONAVIRUS PANDEMIC. (accessed July 1, 2022)

Yeung HW-C, Coe N (2015) Toward a Dynamic Theory of Global Production Networks. Economic Geography 91(1):29–58

Zhang H, Ding Y, Li J (2021) Impact of the COVID-19 Pandemic on Economic Sentiment: A Cross-Country Study. Emerging Markets Finance and Trade 57(6):1603–1612

Zhang Y (2021) Potential effects of epidemic on decarbonization process in China: Analysis based on a dynamic CGE model. China Soft Science 8:19–29

Zheng B, Geng G, Ciais P et al. (2020) Satellite-based estimates of decline and rebound in China’s CO2 emissions during COVID-19 pandemic. Science Advances 6:49

Acknowledgements

The Strategic Priority Research Program of the Chinese Academy of Sciences (Grant No. XDA23100402 to Zhenshan Yang, and Grant No. XDA23100403 to Quansheng Ge), and Scenarios of Resource Security under Global Trade Uncertainty under the Program of Supply–Demand Pattern and Survey of Global Mineral Resources (Grant No. DD20230565 (under DD20230123) to Zhenshan Yang).

Author information

Authors and Affiliations

Contributions

ZY and QG designed research; ZY, JW and QG performed research; JW analyzed data; ZY, and JW wrote the paper.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Yang, Z., Wei, J. & Ge, Q. Friction or cooperation? Boosting the global economy and fighting climate change in the post-pandemic era. Humanit Soc Sci Commun 10, 870 (2023). https://doi.org/10.1057/s41599-023-02307-4

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-02307-4