Abstract

This article analyzes how trade openness and political stability affect foreign direct investment (FDI) in 25 Asia-Pacific countries from 1990 to 2020. This study employs the dynamic system Generalized Method of Moments to mitigate the heteroskedasticity and autocorrelation issues. We also perform the Johnson–Neyman test to examine whether trade openness moderates the relationship between political stability and FDI. Our findings show that trade openness positively affects FDI, while political stability has a negative effect. Noticeably, the Johnson–Neyman test indicates that Trade Openness moderates the relationship between political stability and FDI in Asia-Pacific nations. Trade openness and its moderating role remained robust before the 2008 financial crisis. The impacts of trade openness and political stability on FDI persist in non-tax-heaven countries. Our findings align with market-seeking, efficiency, resource-seeking, and regulatory risk theories. Finally, these findings are helpful for policymakers to attract FDI projects sustainably across the Asia-Pacific region.

Similar content being viewed by others

Introduction

Recent studies report that Foreign Direct Investment (FDI) is the primary driver of economic growth because it transfers the latest technologies from developed to developing countries (Chenaf-Nicet and Rougier, 2016). Kurecic and Kokotovic (2017) argue that political stability does not significantly affect FDI because investors take political risks for granted. Sabir et al. (2019) indicate that political stability positively affects foreign direct investment. Prior studies indicate that trade openness helps the country access a broader market, creating resources for import and export, causing investors to expect much revenue in the host country. Therefore, trade openness greatly influences foreign direct investment (Djulius, 2017).

This study is conducted in the Asia-Pacific region for the reasons listed below. First, the most significant and rapidly expanding economies, including China, India, and Southeast Asian nations, are found in the Asia-Pacific area, which in 2020 accounted for almost 34% of the world’s gross domestic product (GDP). According to World Bank data, China had a GDP of over $16.64 trillion in 2020, making it the largest economy in the Asia-Pacific region and a significant contributor to the global GDP. India is also the third-largest purchasing power parity (PPP) economy, and its GDP was about $3.05 trillion in 2020. Additionally, the Asia-Pacific area has established itself as an essential commercial partner on the global stage. Due to their sizable consumer markets, wealth of resources, and competitive manufacturing capacities, these nations draw a sizable amount of FDI. Second, according to World Trade Organization (WTO) data, exports from Asia rose from approximately 12% in 1980 to about 38% in 2020. This growth underlines the region’s expanding significance in world trade. Therefore, it is essential to research how trade openness and FDI interact in the Asia-Pacific region. Third, political governance in the Asia-Pacific area is crucial to consider since, in countries like Myanmar, Cambodia, and the Philippines, where corruption is still a problem and can affect political governance, it can impede progress. In addition, North Korea is renowned for having a closed and intensely secretive governmental structure. The government tightly controls information, and its governance procedures are opaque. Laos has a one-party communist government, constrained press freedom, and little room for civil society. These elements may undermine national openness and accountability standards. Fourth, the Asia-Pacific region has received substantial foreign direct investment (FDI), accounting for approximately 40% of worldwide FDI inflows in recent years, according to the United Nations Conference on Trade and Development (UNCTAD). Therefore, researchers can examine how these factors determine investment patterns in critical economic centers and how FDI helps economic growth and development by looking at the effects of political stability and trade openness in these nations.

Additionally, the study investigates whether trade openness in Asia-Pacific countries moderates the relationship between political stability and FDI. Finally, the governments of the Asia-Pacific region have actively sought trade liberalization, undertaken economic reforms, and taken steps to maintain a politically stable environment that will promote growth and draw foreign direct investment. These policies frequently involve vows to respect the rule of law, transparent governance procedures, investor-friendly regulations, and political reforms.

Our study significantly contributes to the growing international economics literature in the following ways. First, our study complements prior studies such as Hashmi et al. (2020) and Shan et al. (2018) because we employ more efficient estimation methods. Hashmi et al. (2020) examined the effect of trade openness on FDI inflow and employed OLS. Shan et al. (2018) examined the effect of political stability on FDI inflow and employed the Fixed Effect Model. Our study follows Duong et al. (2022) and Xu et al. (2021) to utilize the dynamic system Generalized Method of Moments (GMM) because of the following reasons. First, GMM is generally more efficient than OLS and FEM because GMM uses all available moment conditions to estimate the parameters, which reduces the estimation bias. In addition, GMM is more likely to produce consistent estimates than OLS and the FEM if the number of instruments is relative to the sample size. Furthermore, GMM is a more flexible method than OLS and the FEM because it can estimate a wide range of models with different specifications, including models with autocorrelations and heteroskedasticity.

Second, our study closely relates to Xu et al. (2021) because it examines the relationship between trade openness, political stability, and FDI inflows. However, our study contributes to the literature by employing the Johnson–Neyman test to analyze whether trade openness moderates the relationship between political stability and FDI inflows in Asia-Pacific nations. This moderation analysis allows us to assess whether trade openness strengthens or weakens the relationship between political stability and attracting net FDI inflows. Therefore, the results support empirical evidence for policymakers to construct effective strategies to attract FDI projects in Asia-Pacific nations.

Finally, our study makes essential contributions because it includes two robustness tests to reinforce the main findings. These tests provide further validation and strengthen the credibility of our results, which subsequently support the policy implications for attracting FDI inflows sustainably. Furthermore, our study offers a more comprehensive dataset than Xu et al. (2021). While Xu et al. (2021) focused on sub-Saharan African countries, our research focuses on 25 Asia-Pacific (APAC) countries, covering a more extended period from 1990 to 2020. This larger sample size and extended period provide a more extensive and representative coverage of the APAC region, enhancing the generalizability of our findings.

This study generates the following striking results. The findings show that political stability discourages FDI inflows in Asia-Pacific nations. This result aligns with Kurecic and Kokotovic (2017) and Shan et al. (2018) and supports the regulatory risk theory. Second, our findings report the positive relationship between trade openness and net FDI inflow in Asia-Pacific nations. This result is in line with Gnangnon (2018), Hashmi et al. (2020), Bhasin and Garg (2020), Kurul and Yalta (2017), and Mudiyanselage et al. (2021), and supports the market-seeking theory, efficiency-seeking theory, and resource-seeking theory. In addition, our findings indicate that trade openness moderates the relationship between political stability and FDI inflows in Asia-Pacific nations. This result is consistent with Kurul and Yalta (2017), Sabir et al. (2019), and Kinuthia and Murshed (2015). Finally, the robustness tests indicate that the moderating role remains robust even if we employ Two-Stage Least Squares estimation. While trade openness and political stability robustly affect FDI in non-tax haven countries, the moderating role of trade openness is not robust in non-tax haven countries.

The structure of our paper is as follows. First, we describe the literature review and developing research hypotheses. Then we illustrate the data collection and methodology. Next, we report our empirical results. The following section discusses our findings. Next, we provide the policy implications. The last section is the conclusion.

Literature review

The relationship between trade openness and FDI

Recent studies from Bhasin and Garg (2020), Mudiyanselage et al. (2021), and Khan and Hye (2014) show that higher trade openness reduces FDI in emerging markets for several reasons. First, trade openness in these countries is less attractive than in their counterparts, thus dismissing FDI inflows. Second, while trade openness attracts foreign investors, local governments tighten environmental regulations to avoid inefficient foreign investment projects, reducing investment funds. Third, because risk and uncertainty affect investor decisions, trade openness may also harm FDI. The requirement for greater confidence in the stability of trade liberalization policies is one of the significant variables influencing investors’ long-term investment decisions. Due to the risk, unpredictability, and lack of confidence associated with liberalization policies, foreign investors save money compared to local investment expenses by opting not to invest in a hazardous country (Khan and Hye, 2014).

In contrast, by removing trade restrictions on tax rates and quotas, trade openness encourages foreign investors to invest in host countries. Similarly, Gnangnon (2018), Hashmi et al. (2020), and Kurul and Yalta (2017) found results that support the market-seeking theory, efficiency-seeking theory, and resource-seeking theory report that increased trade openness would be a better option to attract additional FDI inflows in both the short and long term, as foreign multinational corporations seek cost efficiency through tariff and import duty reductions. Kurul and Yalta (2017) state that FDI and free trade in the host country will be affected as the demand for goods increases abroad and the demand for exports increases in the host country. Gnangnon (2018) argues that less advanced countries have more experience using FDI attraction policies than advanced countries. It is argued that lower cross-border business costs such as tariffs and taxes on foreign goods and services, government policy activities, lower transaction costs, and the removal of quantitative restrictions on imports create favorable conditions for efficiency-seeking FDI and thus encourage foreign multinationals to invest.

Based on the results of Gnangnon (2018), Hashmi et al. (2020), Kurul and Yalta (2017), market-seeking theory, efficiency-seeking theory, and resource-seeking theory, we propose the following hypothesis:

Hypothesis 1: Trade openness has a positive relationship with FDI.

Notably, we follow Mariotti and Marzano (2021) and Duong et al. (2022) to measure foreign direct investment (FDI) and trade openness (TO). The FDI variable is calculated by dividing net FDI inflows by total GDP; trade openness is measured by dividing the sum of total imports and exports by total GDP. The data is collected from the World Bank Database.

The relationship between political stability and FDI

Elish (2022), Buitrago and Barbosa Camargo (2020), and Ciesielska-Maciagowska and Koltuniak (2021) stated that more excellent political stability creates a favorable climate for businesses to make foreign direct investments and foreign portfolio investments. This research supports the institutional theory and the Governance theory report that stable political regimes create and uphold precise laws and rules that safeguard property rights, guarantee the execution of contracts, and create a stable economic climate. Due to their ability to lower investment risks and serve as a base for long-term commitments, these institutional traits attract foreign investors (Acemoglu et al., 2001). Furthermore, efficient institutions, such as governmental organizations, judicial systems, and regulatory bodies, are frequently linked to stable political regimes. These institutions are more successful in fostering trust, enabling investment, and lowering political risk perception. By fostering trust and collaboration between foreign investors and local stakeholders, this shared understanding and agreement on institutional standards help to facilitate the inflow of FDI.

Kurecic and Kokotovic (2017) and Shan et al. (2018) stated that political stability is one of the factors impeding the attraction of FDI inflows. They indicate that African political stability and the absence of violence negatively impact Chinese FDI because of bilateral political agreements between China and politically unstable African countries that might help reduce the risks of Chinese investment. Chen et al. (2023) point out that political stability in host countries promoted China’s outward foreign direct investment in the Asian region before 2009 became a deterrent in the post-2009 era, while other indicators of quality of institutions (e.g., voice and accountability and regulatory quality) acted as barriers for the Chinese overseas foreign direct investment (OFDI) throughout the period from 2003 to 2018. This research is consistent with the regulatory risk theory that political stability can deter FDI when accompanied by unfavorable regulatory policies or excessive government intervention. Stable political systems may impose restrictive regulations, cumbersome bureaucracy, or unpredictable policy changes, making it difficult for foreign investors to operate efficiently and profitably (Busse and Hefeker, 2007).

Based on the results of Elish (2022), Buitrago and Barbosa Camargo (2020), and Ciesielska-Maciagowska and Koltuniak (2021), we propose the following hypothesis:

Hypothesis 2: Political stability has a positive relationship with FDI.

Notably, we follow Xu et al. (2021) to collect data on Political stability from the World Bank Database. This variable, which spans from −2.5 to 2.5, represents the estimation of governance performance and denotes weak and high governance performance, respectively.

The moderating role of trade openness on the relationship between political stability and FDI

Prior research indicates that a country with a high level of trade openness or political stability will become more attractive to foreign investors (Blomstrom et al., 2001; Hashmi et al., 2020; Kurul and Yalta, 2017; Rashid et al., 2017; Sabir et al., 2019; Kinuthia and Murshed, 2015). These prior researches support the market-seeking theory that political stability, when combined with trade openness, political stability enhances the benefits of market-seeking FDI. Foreign investors are more likely to view politically stable and open economies as reliable and conducive environments for conducting business, as they can access a more extensive consumer base and operate confidently due to the stable political environment. Prior studies also support the institutional quality theory (Wei, 2000) that trade openness may act as a mechanism for improving the quality of institutions, as trade liberalization often necessitates the establishment of transparent and efficient regulatory frameworks, reducing corruption and bureaucratic barriers that hinder FDI.

Based on the results of Blomstrom et al. (2001), Hashmi et al. (2020), the market-seeking theory, and the institutional quality theory, we propose the following hypothesis:

Hypothesis 3: The Moderating Role of Trade Openness on the Relationship between Political Stability and FDI.

Data and methodology

Data

The sample includes 25 countries in the Asia and Pacific Region (APAC) from 1990 to 2020. We collected data from the World Bank Database. We follow Duong et al. (2022) to mitigate outliers by winsorizing our sample at 5% and 95% levels. We follow Duong et al. (2022) and Tran et al. (2022) to exclude observations with insufficient data to calculate variables. Our final data sample includes 25 Asia-Pacific countries with 463 annual observations.

Estimation methods

In this study, we use the standard estimation method of Panel Least Square (OLS), Fixed Effects Model (FEM), and Random Effect Model (REM). We follow Shan et al. (2018) and Duong et al. (2022) to apply the Hausman Test and Lagrange Multiplier Test to choose the most appropriate estimation method. However, standard panel regressions may violate the autocorrelation and heteroskedasticity assumption. Thus, we apply Durbin-Watson and the Laplace Likelihood Ratio Test to check for Heteroscedasticity and autocorrelation issues. Finally, we follow Duong et al. (2022) and Xu et al. (2021) to implement dynamic system Generalized Methods of Moments (GMM) estimations to solve autocorrelation and heteroskedasticity problems. Finally, we employ the first robustness test in non-tax havens countries and the second robustness by employing the Two-Stage Least Squares (TSLS) estimations to ensure our findings are robust.

In addition, we employ the moderated regression effect and Johnson–Neyman estimations to test whether trade openness moderates the relationship between political stability and FDI. Johnson–Neyman estimation is a statistical method used to analyze moderation effects in regression analysis. Moderation occurs when the relationship between an independent variable (predictor) and a dependent variable (outcome) changes depending on the level of another variable (moderator). Besides, Johnson–Neyman estimation helps identify the specific values or ranges of the moderator variable where the relationship between the predictor and outcome variables becomes statistically significant. It allows researchers to determine the conditions under which the moderator influences the relationship between the predictor and outcome variables. Furthermore, this test helps understand the moderation effects and identifies the conditions under which the relationship between variables changes.

Model construction

Gnangnon (2018) and Hashmi et al. (2020) found that higher TO increases FDI, while Bhasin and Garg (2020) and Mudiyanselage et al. (2021) found a negative relationship between these two variables. Therefore, we follow them to examine the relationship between trade openness (TO) and foreign direct investment (FDI) in model 1 as follows:

Similarly, Elish (2022), Ciesielska-Maciagowska and Koltuniak (2021) found a positive relationship between political stability (POL) and FDI, while Kurecic and Kokotovic (2017) and Shan et al. (2018) found that higher POL leads to a decrease in FDI. Therefore, to test Hypothesis 2, we replace Trade Openness with Political stability in Model 2 as follows:

Finally, we follow Mariotti and Marzano (2021) to add the interaction variable (TO*POL) to model 3 and model 4 to evaluate the moderating role of TO on the relationship between POL and FDI.

Where FDI represents foreign direct investment; TO denotes Trade Openness; POL stands for Political stability; Control includes the consumer price index (CPI), control of corruption (COC), and the growth rate in GDP (GDP_GROWTH). In addition, “i” is cross-sections, “t” is time, αi is the firm fixed effect, αt is the year fixed effect, and μit is the residual value. All variable definitions are displayed in Appendix A.

Empirical results

Descriptive statistics

Table 1 presents descriptive statistics of the main variables. The average value of FDI is 4.94, with a standard deviation of 5.93. Our results are similar to those of Xu et al. (2021), who studied 38 countries between 2000 and 2015, showing an average value of foreign investment of 5.02. However, the standard deviation of the FDI in Xu et al. (2021) is 9.25 higher than in our study. The average level of political stability between countries in our study is 0.31, which is also similar to Xu et al. (2021) because they report an average value of political stability of 0.483, indicating instability in political institutions in sub-Saharan Africa. Our study also shows that the average trade openness of the 25 APAC countries is positive, consistent with Xu et al. (2021) and Hashmi et al. (2020).

Pearson correlation matrix

Table 2 shows the Pearson correlations between independent variables. The COC is highly correlated with POL at 0.7187, indicating a possible multicollinearity issue. We then perform the VIF to check for multicollinearity between the variables. The results show that the mean VIF is 1.5842 and all the VIF is less than 5, so there is no multicollinearity issue in our study (Duong et al., 2022; Tran et al., 2022)

The impacts of trade of openness and political stability on FDI

We follow Shan et al. (2018) to apply Hausman and Lagrange Multiplier Test to choose the most appropriate analysis estimation method among OLS, FEM, and REM. The Hausman and Lagrange Multiplier tests show that the REM is the most suitable estimation for our data sample. We report the REM estimations in Table 3.

Table 3 reports that trade openness positively increases FDI inflow. Our finding is consistent with Kurul and Yalta (2017) and Hashmi et al. (2020). Besides, political stability has a positive impact on FDI, which is consistent with Rashid et al. (2017), Sabir et al. (2019), and Kinuthia and Murshed (2015). Finally, the interaction term between trade openness and political stability positively and significantly impacts FDI. Our findings imply that countries with higher political stability and more free-trade agreements can attract a higher FDI inflow.

However, the Durbin-Watson and The Laplace Likelihood Ratio Test for Heteroscedasticity suggest that REM violates autocorrelation and heteroskedasticity assumption. Finally, we follow Deseatnicov and Akiba (2016), Xu et al. (2021), and Duong et al. (2022) to implement the dynamic system Generalized Methods of Moments (GMM) to solve autocorrelation and heteroskedasticity assumption problems.

Table 4 shows the result from GMM estimations. The J-statistic determines endogeneity, and the AR test determines autocorrelation. The model has no quadratic autocorrelation if the AR (2) probability is above 20%. Suppose the p-value of the J-statistic is above 20%. In that case, all instrument variables are valid, and the models have no endogeneity issues. The instrumental variables are FDI(-1), TO, POL, and TO*POL.

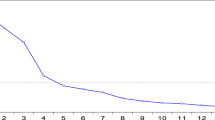

In addition, to explain the moderation effect clearly, this study followed He and Ismail (2023); Compton et al. (2023); Sarintohe et al. (2023); Gorgol et al. (2022) to implement the Johnson–Neyman technique to identify the threshold of significance for the simple effects of political stability on FDI for different levels of the moderator (TO). The Johnson–Neyman regions are provided in Fig. 1. Moreover, Fig. 2 represents the Simple slope analyses for the effect of POL on FDI when there is high trade openness (1 standard deviation above the mean), average trade openness (mean), and low trade openness (1 standard deviation below the mean).

The figure demonstrates the moderating effects of trade openness on the nexus between political stability and foreign direct investment.

The figure examines the effect of political stability on foreign direct investment with high trade openness (1 standard deviation above the mean), average trade openness (mean), and low trade openness (1 standard deviation below the mean).

Robustness tests

After employing alternative estimation methods, we perform the first robustness test to check whether our results are robust. We follow Calmès and Théoret (2023) to employ the Two-Stage Least Squares (TSLS) because it is the simplest form of GMM. We report the first robustness test results in Appendix B.

In the second test, we follow Mariotti and Marzano (2021) to test whether our findings are robust in non-tax haven nations. Specifically, we exclude tax haven nations to check if tax havens influence our findings in the sample because tax competition and lower domestic tax rates have undoubtedly had a competitive effect on attracting FDI (Jones and Temouri, 2016). Therefore, this study excludes Hong Kong, Singapore, and Vanuatu from the sample. After that, we estimate the regression results using the dynamic system GMM estimation approach and report the results in Appendix C.

Discussions

Table 4 reports that trade openness is positively correlated with foreign investment. When trade openness increases by 1%, foreign investment increases by 0.0330%. Our results are consistent with Gnangnon (2018), Hashmi et al. (2020), Kurul and Yalta (2017), and the market-seeking theory that suggest that trade openness enhances market potential and seeks cost efficiency by reducing trade barriers such as tariffs, quotas, and import restrictions, attracting FDI. Besides, our results are also consistent with the efficiency-seeking theory because they suggest that FDI is attracted to countries with trade openness because it allows firms to access inputs, resources, or production factors at a lower cost or of higher quality. Furthermore, our results are consistent with the resource-seeking theory that trade openness plays a significant role in resource-seeking FDI because it allows firms to take advantage of the principle of comparative advantage by engaging in international trade; firms can tap into resources that are abundant and inexpensive in foreign countries, thus reducing their production costs and enhancing their competitiveness. The findings support hypothesis 1.

Table 4 reports a negative relationship between political stability and FDI. When political stability increases by one percentage point, foreign investment decreases by 0.1571%. Our results are consistent with Kurecic and Kokotovic (2017), Shan et al. (2018), and the regulatory risk theory that political stability, accompanied by unfavorable regulatory policies or excessive government intervention, can deter FDI. Stable political systems may impose restrictive regulations, cumbersome bureaucracy, or unpredictable policy changes, making it difficult for foreign investors to operate efficiently and profitably (Busse and Hefeker, 2007). Our findings reject hypothesis 2.

Table 5 shows that POL had a positive effect on FDI, and TO had a significant positive effect on FDI. TO positively moderated the relationship between POL and FDI. These results indicated that higher TO combined with POL enhances FDI. According to Hashmi et al. (2020), international investors are more likely to see politically stable and open countries as reliable and conducive places for business since they have access to a more extensive consumer base and can operate safely due to the stable political environment. In addition, Wei (2000) stated that trade openness may operate as a mechanism for increasing institutional quality since trade liberalization frequently entails the construction of transparent and efficient regulatory frameworks, eliminating corruption and bureaucratic hurdles that impede FDI. This result is consistent with Hashmi et al.(2020) and Wei (2000). It also aligns with market-seeking and institutional quality theories and supports hypothesis 3.

In addition, The Johnson–Neyman test suggests that the moderation effect was significant when TO support was lower than −67.116 and higher than −24.743. The moderation effect was nonsignificant when TO was between −67.116 and −24.743. Moreover, as shown in Fig. 2, with higher TO (one standard deviation above the mean), the association between POL and FDI was more substantial than with lower TO (one standard deviation below the mean). The Johnson–Neyman significant regions are provided in Fig. 1, whereas the interaction is presented in Fig. 2.

Our findings report a positive relationship between inflation and foreign direct investments in models 2 and 3 but insignificant in models 1 and 4. Our results are inconsistent with Rusu and Dornean (2019). Inflation rates might be associated with growing economies. Rapidly growing economies might attract FDI due to the potential for higher returns and expanding consumer markets. Moreover, the increasing inflation rates in host countries weaken local currency value, making their export products more competitive in the global market. Therefore, slightly increasing the inflation rate could result in increased FDI inflows.

Table 4 reports that corruption control has a positive impact on attracting FDI. The results also show that lower corruption protects foreign investors from bureaucracy costs and unnecessary procedures. Better control of corruption also enhances investor confidence, so FDI inflows are more likely to increase accordingly. While the impact of corruption control on FDI is statistically insignificant, this finding aligns with Hossain (2016).

Table 4 reports a positive relationship between economic growth and FDI inflows (Rao et al., 2023; Khan et al., 2022). More substantial economic growth positively correlates with strong purchasing power. Economic growth is a significant indicator of a good business climate, including a larger market, greater consumer demand, and better investment prospects. Aside from that, rapid economic growth is linked to technological developments, human capital development, and infrastructure. These elements may improve the effectiveness and productivity of foreign companies doing business in these economies, increasing their appeal to FDI. Economic growth also denotes political stability, solid macroeconomic policies, and advantageous regulatory frameworks, all fostering an atmosphere beneficial to international investors.

Appendix B reports the first robustness test results by employing the TSLS estimations. Our findings indicate that trade openness has a significant and robust positive effect on FDI. However, Political Stability affects FDI negatively, but the coefficient is statistically insignificant. In addition, the moderating role of Trade Openness on the relationship between Political Stability and FDI remains unchanged.

Appendix C reports the second robustness test results after excluding the tax haven nations. The findings suggest that trade openness and political stability remain robust in non-tax haven nations. However, the trade openness and political stability interaction become statistically insignificant in the non-tax haven nations. Hong and Smart (2010) suggest that in countries with high tax rates for legal or political reasons, it is impossible to distinguish the tax rate between changes in foreign investment and fluctuations in domestic investment. As a result, tax haven nations become a competitive advantage because these nations indirectly offer lower corporate tax rates to foreign investors. It is the reason why we separate tax haven countries. Finally, Appendix C reports a robust impact of trade openness and political stability on attracting FDI, even after excluding the tax haven nations.

Implication

This study contributes practical implications for policymakers and academics in emphasizing the importance of trade openness and political stability policies to attract more FDI inflows into the country. First, given that trade openness has a positive impact on attracting foreign direct investment (FDI), Governments can negotiate and enter into Free-Trade Agreements (FTAs) to reduce tariffs and other trade barriers between participating countries, and they can implement measures to simplify and streamline customs procedures, reduce administrative burdens, and enhance transparency in trade-related processes such as implementing electronic customs systems, harmonizing trade documentation requirements, and improving infrastructure and logistics networks to facilitate the movement of goods across borders. Besides, Governments can support exporters by providing trade promotion services, market research, and assistance in accessing foreign markets such as trade missions, participation in international trade fairs and exhibitions, and export financing programs to help businesses expand their reach and access new markets. In addition, aligning standards, regulations, and technical requirements across countries can reduce trade barriers and facilitate trade in goods and services. Furthermore, promoting regional economic integration initiatives, such as regional trading blocs and economic cooperation frameworks, can deepen economic ties and enhance trade openness.

Second, while higher political stability reduces net FDI inflows, policymakers must establish and reinforce a solid legal framework that upholds the rule of law, which is crucial for attracting FDI projects. This includes ensuring transparent and efficient legal systems, enforcing contracts, protecting property rights, and providing a fair and impartial dispute resolution mechanism. Improving the quality and effectiveness of the judiciary can enhance investor confidence in the legal system. Moreover, the government may simplify regulations and administrative procedures to reduce bureaucratic hurdles and promote ease of doing business. Governments can implement business-friendly policies, such as reducing red tape, minimizing unnecessary regulations, and adopting transparent and predictable regulatory frameworks. Regulatory impact assessments and periodic reviews of regulations can help identify and address any barriers to investment. Furthermore, Governments can establish anti-corruption agencies, enforce strict anti-corruption laws, promote transparency and accountability in public administration, promote whistle-blower protection, and enhance transparency in government transactions can help deter corruption and attract FDI.

Finally, our study also highlights the moderating role of trade openness on the relationship between political stability and FDI. Policymakers can leverage this finding by strategically utilizing trade openness to attract FDI, particularly in countries where political stability might be a concern. By actively promoting trade openness and creating an investor-friendly trade environment, countries can offset the potential adverse effects of political instability on FDI. This approach allows policymakers to take advantage of the positive impact of trade openness on FDI while working toward enhancing political stability in the long run.

Conclusion

The study analyzes how trade openness and political stability affect FDI in Asia-Pacific countries from 1990 to 2020. We employ the dynamic system to analyze a balanced sample of 463 annual observations in 25 Asia-Pacific nations.

Our study generates the following striking results. First, our findings show that trade openness positively correlates with FDI inflows, implying that investors choose countries with open trade policies to reduce the cost of doing business when investing in that country. Meanwhile, political stability is negatively correlated with foreign investment. This finding indicates that investors want to choose a market with a more volatile political background. This study also shows that the interaction between trade openness and political stability positively impacts attracting FDI. This finding implies that trade openness has more impact on attracting FDI than political stability, which indicates that trade openness has a moderating role in empowering political stability’s positive effects in attracting FDI in 25 Asia-Pacific nations.

Although this study contributes to the growing international economic literature on 25 countries in the Asia and Pacific Region, it has the following limitations. The GMM method is inefficient in differentiating independent variables' short-term and long-term impacts on dependent variables. Thus, we suggest future studies employ the panel Autoregressive Distributed Lag estimations to examine the short-term and long-term causality relationship between trade openness, political stability, and net FDI inflows.

Data availability

The datasets generated during and/or analyzed during the current study are available in the Harvard Dataverse repository, https://doi.org/10.7910/DVN/LNL3GH.

References

Acemoglu D, Johnson S, Robinson JA (2001) The colonial origins of comparative development: an empirical investigation. Am Econ Rev 91(5):1369–1401

Bhasin N, Garg S (2020) Impact of institutional environment on inward FDI: a case of select emerging market economies. Glob Bus Rev 21(5):1279–1301

Blomstrom M, Globerman S, Kokko A (2001) The determinants of host country spillovers from foreign direct investment: review and synthesis of the literature. J Int Bus Stud 32(3):469–486

Buitrago RRE, Barbosa Camargo MI (2020) Home country institutions and outward FDI: an exploratory analysis in emerging economies. Sustainability 12(23):10010

Busse M, Hefeker C (2007) Political risk, institutions, and foreign direct investment. Eur J Polit Econ 23(2):397–415

Calmès C, Théoret R (2023) Bank performance before and after the subprime crisis: evidence from pooled data on big US banks. J Econ Finance 47:472–516

Chen H, Gangopadhyay P, Singh B, Chen K (2023) What motivates Chinese multinational firms to invest in Asia? Poor institutions versus rich infrastructures of a host country. Technol Forecast Soc Change 189:122323

Chenaf-Nicet D, Rougier E (2016) The effect of macroeconomic instability on FDI flows: a gravity estimation of the impact of regional integration in the case of Euro-Mediterranean agreements. Int Econ 145:66–91

Ciesielska-Maciagowska D, Koltuniak M (2021) Foreign direct investments and home country’s institutions: the case of CEE countries. Eur Res Stud J 1:335–353

Compton SE, Slavish DC, Weiss NH, Bowen HJ, Contractor AA (2023) Associations between positive memory count and hazardous substance use in a trauma‐exposed sample: examining the moderating role of emotion dysregulation. J Clin Psychol 79(5):1480–1508

Deseatnicov I, Akiba H (2016) Exchange rate, political environment and FDI decision. Int Econ 148:16–30

Djulius H (2017) Energy use, trade openness, and exchange rate impact on foreign direct investment in Indonesia. Int J Energy Econ Policy 7(5):166–170

Duong KD, Truong LTD, Huynh TN, Luu QT (2022) Financial constraints and the financial distress puzzle: evidence from a frontier market before and during the Covid-19 pandemic. Invest Anal J 51:35–48

Elish E (2022) Political and productive capacity characteristics as outward foreign direct investment push factors from BRICS countries. Humanit Soc Sci Commun 9(1):1–10

Gnangnon SK (2018) Effect of multilateral trade liberalization on foreign direct investment outflows amid structural economic vulnerability in developing countries. Res Int Bus Finance 45:15–29

Gorgol J, Waleriańczyk W, Stolarski M (2022) The moderating role of personality traits in the relationship between chronotype and depressive symptoms. Chronobiol Int 39(1):106–116

Hashmi SH, Hongzhong F, Ullah A (2020) Effect of political regime, trade liberalization and domestic investment on FDI inflows in Pakistan: new evidence using ARDL bounds testing procedure. Int J Inf Bus Manag 12(1):276–299

He L, Ismail K (2023) Do staff capacity and performance-based budgeting improve organisational performance? Empirical evidence from Chinese public universities. Humanit Soc Sci Commun 10(1):1–16

Hong Q, Smart M (2010) In praise of tax havens: international tax planning and foreign direct investment. Eur Econ Rev 54(1):82–95

Hossain S (2016) Foreign direct investment (FDI) and corruption: is it a major hindrance for encouraging inward FDI? Afr J Bus Manag 10(10):256–269

Jones C, Temouri Y (2016) The determinants of tax haven FDI. J World Bus 51(2):237–250

Khan H, Weili L, Khan I (2022) The role of institutional quality in FDI inflows and carbon emission reduction: evidence from the global developing and belt road initiative countries. Environ Sci Pollut Res Int 29(20):30594–30621

Khan REA, Hye AQM (2014) Foreign direct investment and liberalization policies in Pakistan: an empirical analysis. Cogent Econ Finance 2(1):944667

Kinuthia BK, Murshed SM (2015) FDI determinants: Kenya and Malaysia compared. J Policy Model 37(2):388–400

Kurecic P, Kokotovic F (2017) The relevance of political stability on FDI: a VAR analysis and ARDL models for selected small, developed, and instability threatened economies. Economies 5(3):22

Kurul Z, Yalta AY (2017) Relationship between institutional factors and FDI flows in developing countries: new evidence from dynamic panel estimation. Economies 5(2):17

Mariotti S, Marzano R (2021) The effects of competition policy, regulatory quality and trust on inward FDI in host countries. Int Bus Rev 30(6):10188

Mudiyanselage R, Mayoshi M, Epuran G, Tescas B (2021) Causal links between trade openness and foreign direct investment in Romania. J Risk Financ Manag 14:90

Rao DT, Sethi N, Dash DP, Bhujabal P (2023) Foreign aid, FDI and economic growth in Southeast Asia and South Asia. Glob Bus Rev 24(1):31–47

Rashid M, Looi XH, Wong SJ (2017) Political stability and FDI in the most competitive Asia Pacific countries. J Financ Econ Policy 9(02):140–155

Rusu VD, Dornean A (2019) The quality of entrepreneurial activity and economic competitiveness in European Union countries: a panel data approach. Adm Sci 9(2):35

Sabir S, Rafique A, Abbas K (2019) Institutions and FDI: evidence from developed and developing countries. Financ Innov 5(1):1–20

Sarintohe E, Larsen JK, Vink JM, Maciejewski DFJCP(2023) Expanding the theory of planned behavior to explain energy dense food intentions among early adolescents in Indonesia Health Psychol 10(1):2183675

Shan S, Lin Z, Li Y, Zeng Y (2018) Attracting Chinese FDI in Africa. Crit Perspect Int Bus 14(2/3):139–153

Tran O, Nguyen D, Duong K (2022) How market concentration and liquidity affect non-performing loans: evidence from Vietnam. Polish J Manag Stud 26(1):325–337

Wei SJ (2000) How taxing is corruption on international investors? Rev Econ Stat 82(1):1–11

Xu C, Han M, Dossou TAM, Bekun FV (2021) Trade openness, FDI, and income inequality: evidence from sub‐Saharan Africa. Afr Dev Rev 33(1):193–203

Acknowledgements

This study is supported by Ton Duc Thang University, Van Lang University and Ho Chi Minh City Open University.

Author information

Authors and Affiliations

Contributions

ANNL (ai.lnn@vlu.edu.vn) conceived and designed the experiments, performed the experiments, analyzed and interpreted the data, and wrote the first draft of the manuscript. HP (ha.p@ou.edu.vn) performed the experiments, contributed reagents, materials, analysis tools, or data. DTNP (phamthingocdung@tdtu.edu.vn) performed the experiments and contributed reagents, materials, analysis tools, or data. KDD (duongdangkhoa@tdtu.edu.vn) analyzed and interpreted the data and wrote the first draft of the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval is not applicable because this article does not contain any studies with human or animal subjects.

Informed consent

Informed consent is not applicable because this article does not contain any studies with human or animal subjects.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Le, A.N.N., Pham, H., Pham, D.T.N. et al. Political stability and foreign direct investment inflows in 25 Asia-Pacific countries: the moderating role of trade openness. Humanit Soc Sci Commun 10, 606 (2023). https://doi.org/10.1057/s41599-023-02075-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-02075-1