Abstract

In the last few decades, rising prices of agricultural commodities have been an area of concern for most countries owing to high population growth, increased unemployment, and per capita food needs. The current study intends to examine the positive and negative shocks of agricultural product prices, credit disbursement, and the labor force’s impact on the agricultural growth of Pakistan. The nonlinear autoregressive distributed lag (NARDL) method was applied using secondary data sources from 1970 to 2018. The results revealed that positive and negative price shocks contribute positively to agriculture growth; however, positive price shock has a more stimulating effect than negative prices. Furthermore, credit disbursement and labor force significantly positively impact agricultural value added in the short and long run. Finally, the study’s findings have far-reaching consequences for policymakers dealing with Pakistan’s asymmetric relationship between agricultural credit disbursement, commodity prices, and agricultural growth.

Similar content being viewed by others

Introduction

Pakistan is an agriculture-based country, and the agriculture sector was the main economic contributor, with a contribution of 22.7% to the GDP of Pakistan. It is the second-largest sector, providing employment opportunities to 37.4% of its labor force (PES, 2022). The agriculture sector engages 65% of the population directly or indirectly, accounting for 59% of the total export revenues. Pakistan devoted 48% of land to agriculture, of which 40% is arable. Irrigation plays a significant role, supporting 90% of the food production with 80% use of cultivated land (PBS, 2020). Similarly, wheat, cotton, sugarcane, and rice are key crops. Wheat is considered an essential commodity, and its production assures that there will be enough food supply in the country. However, the devoted land has declined by 2.1 percent (from 9.168 to 8.976 million hectares (M-ha)), and its production by 3.9 percent (from 27.464 to 26.394 million tonnes) during 2022 (PES, 2022). The main goal of every country is self-reliance on wheat, which is considered the most constant challenge for agriculturalists and legislators (Chandio et al., 2019). Likewise, cotton, a major export crop, decreased in production area from 2.079 to 1.937 M-ha in 2022, representing a drop of 6.8 percent (PES, 2022). Agriculture serves as raw materials for other industries, leading to industrial expansion and promoting economic growth. However, the development of the agricultural sector has been greatly affected due to socio-environmental and political situations. Despite having a more extensive irrigation system, Pakistan still imports several agricultural products (Chandio et al., 2018).

Furthermore, different nations have worked better than others, and in addition to the kind of government, commodity prices have played a significant role in fostering economic growth. Some less developed nations have seen relatively slow economic development due to their weak responses to price shocks, which have worsened their debt issues (Chandio et al., 2020). It may be due to a failure to capitalize on positive shocks and a failure to prevent large losses from negative shocks. The uncertainty caused by a sudden rise or fall in commodity prices has the potential to exacerbate the consequences of price declines relative to gains and even induce an asymmetric reaction to GDP growth (Kilian, 2014). Moreover, According to Deaton and Miller (1996), rising commodity prices have a short-term positive influence on economic development in African nations. However, Collier and Gunning (1999) demonstrate that fluctuations in commodity prices do not lead to long-term increases in per capita income. Vink (2012) revealed that rising agricultural price inefficiencies have a significant detrimental effect on growth in sub-Saharan African countries.

In addition, it is vital to get prime growth and raise profitability in agriculture by using sources at hand effectively because it can directly reduce rural poverty (Valdes, 2013). Increased agricultural growth fulfills food demands, enlarges exports, and supports exchange rates. Meanwhile, agricultural development in Pakistan has witnessed a negative tendency caused by disparaging strategies implemented over the last few decades (Shah et al., 2015). Overall, the Pakistani agriculture industry faces several difficulties and barriers, i.e., inability to get capital, insufficient grain and pesticides supplies, power outages, water scarcity, unstable gas prices, and higher input costs. Nonetheless, Pakistan can achieve sustainable growth in agriculture by putting farmers back at the core circle of policy-making processes. It requires a concerted effort by businesses, researchers, governments, and other segments of society to focus on food availability (Kashif et al., 2020). These stakeholders should coordinate to help the country’s agricultural households. Mainly smallholders increase their crop yield with better access to resources, more robust markets, profound participation in research, and dedicated information exchange without compromising environmental or social standards. This strategy promises increased productive output and long-term viability. When coupled with more efficient markets, a more robust agricultural system may provide stable food supplies, equitable pricing, and environmentally responsible land use, all of which contribute to a thriving economy (Kashif et al., 2023).

The existing literature related to agriculture was mainly concentrated on agricultural contribution to growth (Addison et al., 2016; Byerlee et al., 2009; Diao et al., 2010; Tiffin and Irz, 2006); governmental expenditure impact on GDP growth (Alene and Coulibaly, 2009; Furceri, 2007; Iganiga and Unemhilin, 2011) and commodity price volatility impact on GDP (Collier and Goderis, 2012; Deaton, 1999; Harvey et al., 2017; Hovhannisyan and Bozic, 2017). However, few studies observe commodity prices’ positive and negative shocks and their effect on agriculture value added (AVA). Following the argument of Collier and Gunning (1999), Aysan et al. (2009), Addison et al. (2016) Kinda et al. (2018) about the potential asymmetry in responses to price shocks, we examine whether positive shocks have a greater impact than negative shocks on Pakistan. Juselius et al. (2014) believe that a country-based approach offers dependable proof. Apart from the pricing shocks, the current study also considers credit disbursement and the labor force. Moreover, many developing nations have a significant share of their primary trade-in commodities, suggesting that relative price fluctuations could profoundly impact economic growth and poverty alleviation (Harvey et al., 2017). Food price fluctuations require significant attention because they reduce the household welfare of people experiencing poverty in case of price rises. A ten percent rise in food prices triggers a poverty ratio of 2 percent (ADB, 2008).

Similarly, credit disbursement to the agriculture sector has enormous ramifications for developing nations’ economic growth volume and intensity. The impact and productivity of agricultural labor have also been neglected extensively. In the case of Pakistan, the uncertainty factor deteriorates further due to political instabilities, and the prices of products change rapidly with less control by authorities. Therefore, the current study employs a nonlinear approach to examine the positive and negative shocks of agriculture product prices on AVA in Pakistan, along with credit disbursement and labor force. The prices of agricultural commodities were the primary concern for local agriculture producers and consumers; therefore, examining its positive and negative shocks will be a valuable addition to the literature. As per the author’s best knowledge, such a study with the NARDL framework has not been carried out in the Pakistani context. Moreover, this study will address the following research question on to what extent the negative and positive price shocks affect AVA?

The rest of the paper is arranged as follows: Section 2 discusses the literature and the hypotheses formulation. Section 3 describes data, model specification, and econometric techniques. Section 4 reported the study’s results with a comprehensive discussion. Lastly, section 5 concludes the study.

Existing literature and hypothesis development

Generally, it involves several steps for agricultural goods to pass from manufacturing to end-users, like, corporate supply chain, procurement, refining, warehousing, distribution, wholesaling, retailing, etc.; at each step, the products increase in value, ultimately establishing retail pricing. The prices of agricultural products fluctuate more than other goods due to the environment, supply, and demand shocks (Taghizadeh-Hesary et al., 2019). The development of pricing is influenced by numerous elements, such as intrinsic (qualities and manufacturing) and extrinsic elements (substitute pricing and market situation). Furthermore, the relationship between agriculture and climate is universal, i.e., floods, rainfall, temperature, and other aspects considerably influence agriculture. Agricultural machinery, land size, and productive assets of farms were the elements deemed to have substantial impacts apart from climate shocks (Chandio, Magsi, et al., 2020). It affects the commodity pricing and performance of the agriculture sector, which subsequently weakens economic growth (Sethi et al., 2002).

Moreover, Pakistan is a massive importer of oil and gas, and the excessive use of diesel oil in the agriculture sector puts an extra burden on the farmers, which compels them to raise the prices. Consequently, Taghizadeh-Hesary et al. (2019) suggest that energy prices and exchange rates contributed to Pakistan’s rise in food prices. Meanwhile, during the last decade, financial and food price crises (2008 and 2011) have been observed, which raised concerns regarding the effects of food price shocks and food insecurity (Chandio, Magsi, et al., 2020). Furthermore, commodity prices can be influenced by global market dynamics, including supply and demand fluctuations, weather conditions, trade policies, and geopolitical factors (Chandio et al., 2018). These external factors can significantly impact the profitability and stability of Pakistani agriculture, affecting farmers’ livelihoods and the overall economic performance of the sector. The volatility in the pricing of agricultural commodities increases threats for concerned participants. This threat will hurt farmers’ benefits, which is unsuitable for businesses and stunts the country’s agriculture growth progress (Chandio et al., 2016). Likewise, Blattman et al. (2007) found that nations with more price fluctuations in commodities had slower economic growth than those with steady price changes. Collier and Goderis (2012) examined commodity price impact on growth using a panel error correction model and found that rising prices affect GDP in the short and long run. The average five years growth, wholesale price indices, credit disbursement, and labor force data are exhibited in Table 1.

Agricultural GDP growth continuously decreases, and the only phases where agriculture GDP reverts from declining were 1995–1999 and 2010–2014. It was a worrying sign for a country known as an agrarian; however, some scholars support the decline of the agriculture portion at the cost of other industry expansions (Chandio et al., 2019). Still, with the high population growth rate, it is difficult for any country to feed people with a reduced agriculture sector (Anderson, 2010). Furthermore, price indices show both upward and downward trends during the sample period; however, there were two phases (1985–1994 and 2000–2009) where price indices declined, and both were under strict Martial Law administrations. Moreover, total credit disbursement to the agriculture sector has an upward trend, but it never meets the producer’s demand due to an increase in the cost of production. Farmers need to import seeds and other materials from different countries; therefore, the exchange rate can be influential. The apparent reasons noticed in agriculture fall were the wealth concentration among wealthy farmers, lack of technological advancement in the tools used for production, corruption with its steadily planted roots, and lack of good governance.

Furthermore, methodological problems might be the reason for the lack of agreement on the long-term influence of commodity prices because possible nonlinear impacts of price shocks were mostly ignored in earlier research. In this regard, Addison et al. (2016) evaluated the positive-negative impacts of price shocks on growth for selected Sub-Saharan African nations and observed hardly any proof of such asymmetry. Similarly, Kinda et al. (2018) emphasized the significance of differentiating between positive and negative shocks, arguing that the latter have irrevocable consequences. Aysan et al. (2009) assessed the asymmetric impact of prices on growth and found that negative shocks have significant adverse impacts, whereas no positive long-run shock effects. Deaton and Miller (1996) showed that commodity price increases, as opposed to price decreases, were more beneficial in the short run for African economies.

In line with the above argument about possible asymmetries in the reaction of commodity price shocks, we tried to contribute to the existing literature by assessing the relationship between commodity pricing and AVA and believe it will provide impactful suggestions and recommendations. Pricing of agricultural commodities is regarded as an essential concern because its fluctuations impact people’s incomes locally and exporters at the country level; therefore, setting the correct prices remains a critical subject. The studies mentioned above have identified price asymmetries, with most of them observing positive shocks, although there were instances where negative shocks were also observed. Nevertheless, we believe that the impact of increasing prices surpasses that of decreasing prices. Hence, based on the above discussion and reported studies, we have formulated the following hypotheses.

H1: Positive agriculture price shock increases agricultural economic growth.

H2: Negative agriculture price shock increases agricultural economic growth.

Materials and methods

Variables and data

The variables used in the present research were agriculture, forestry, and fishing, value added (AVA), credit disbursement in agriculture (CD), the labor force (LF), and agriculture product prices (PI) from 1970 to 2018. Data on AVA (in current US$) was sourced from World Development Indicators. CD (Rupees in Millions), Labor (in millions), and Prices (Index Numbers of wholesale prices of wheat and cotton) data were selected from different Pakistani statistical yearbooks and economic surveys of Pakistan. The reason for choosing wheat and cotton is that both are leading cash crops from different production seasons. The annual data for analysis were changed to log form.

Econometric model

The following Equation has been defined to analyze the long-term effects of credit disbursement, prices, and labor force on the AVA of Pakistan.

AVA, PI, CD, and LF represent the agriculture value added, the price index of agricultural commodities, credit disbursement in agriculture, and the labor force, respectively. According to the authors’ understanding, previous studies analyzed growth in agriculture concerning spending and prices under linear background. However, the present study conducted its analysis in a nonlinear framework which helps foresee whether the time series components (both positive and negative) are cointegrated or not. This research’s primary objective was to examine the asymmetric impact of commodity prices on agriculture growth. The nonlinear model is specified as the following functional form.

where, PI+ and PI− indicates the positive price and negative price indices. Shin et al. (2014) proposed an estimation technique named nonlinear ARDL, which used partial sums of positive and negative changes to define the short and long-term asymmetric effect. The NARDL procedure has various benefits over other conventional models of cointegration: (i) NARDL does not oblige for a stationary test, (ii) even in small samples, the NARDL model operates appropriately, (iii) NARDL can be applicable whether the included variables were stable at the level I(0) or first difference I(1) or integrated fractionally (Ibrahim, 2015; Lee et al., 1997). However, this method does not work well when any I(2) variable is involved. After examining the empirical efforts (Dhaoui and Bacha, 2017; Katrakilidis and Trachanas, 2012; Koutroulis et al., 2016; Meo et al., 2018; Raza et al., 2016), we specified the following model:

where Φ0 denotes long-run parameters, PI+ and PI− indicates positive and negative asymmetric effects and partial sums change in commodity prices. Equation (1) offers only a long-run impact on the model. However, we have to redefine Eq. (1) under the error correction model (ECM) because it provides the basis for assessing the constant speed of adjustment rate and the dependent variable’s short-run performance in the stochastic Equation. The ECM arrangement in a multivariate perspective is given below:

where, π1−π4 and ∆ represents long-run coefficients and short-run differenced variables, respectively, q1 − q4 signifies optimum lag length. Equation (4) implies that the predicted variables have a symmetrical connection; however, the present research seeks to explore the asymmetric effect of commodity prices on the AVA of Pakistan. Therefore, the desired variables were decomposed into negative and positive segments to see the asymmetric impact by considering the following nonlinear Equation. This decomposition regression \({{{\mathrm{p}}}}_{{{\mathrm{t}}}} = \sigma ^ + {{{\mathrm{m}}}}_{{{\mathrm{t}}}}^ + + \sigma ^ - {{{\mathrm{m}}}}_{{{\mathrm{t}}}}^ - + \mu _{{{\mathrm{t}}}}\), where σ+ and σ− are associated with the coefficient of the long run and mt is a decomposed parameter of explanatory variables as:

where the regressors were denoted with m+ and m− that is partially decomposed into positive and negative-sum variations. Subsequently, Eqs. (5) and (6) represent the partial sums of positive and negative adjustments in agricultural commodity prices.

To make specification (4) asymmetric ARDL, we integrated a decomposed positive and negative series of prices (Eqs. 5 and 6) in Eq. (4).

After the estimation of Eq. (7), the bound F-statistics technique developed by Pesaran et al. (2001) was applied to evaluate the long-term cointegration among variables with two boundaries (lower and upper).

Results

It is essential to ascertain the properties of time series data used in Eq. (4) by limiting the concerns of spurious regression; therefore, assessing the data series to check the unit root could be appropriate. Although there was no condition to apply the unit root test or verify the stationary level of incorporated variables (Ibrahim, 2015), asymmetric ARDL cannot be used if any I(2) variable was involved. Thus, to ensure the integration level of variables and that no I(2) variables were contained in the estimation process, this study employed ADF, PP, and KPSS tests (Asteriou and Hall, 2015; Gujarati, 2009; Maddala and Wu, 1999). The reason to avoid any second difference variable is that the value of cointegration F-statistics turns out to be invalid (Ilyas et al., 2010; Meo et al., 2018). In the above tests, the essence of the unit root is the null hypothesis, and variables were stationary in an alternative assumption. Results of all unit root tests at a level I(0) and the first difference I(1) form were represented in Table 2. All the variables were stationary at first difference form in ADF and PP tests. Furthermore, the whole series was stationary at a level form in the KPSS test, and none of the variables is I (2). This situation allows us to proceed with the asymmetric ARDL bound test procedure.

Meanwhile, Table 3 depicts summary statistics. The descriptive statistic results stated that data series were normally distributed, and the values of standard deviations, Jarque-Bera (J-B), and probability endorsed it. The mean value of AVA (10.109) is the highest, followed by CD (4.221), PI (2.145) and LF (1.533). The study variables show changes in their Min-Max values, indicating different levels of the parameters for Pakistan. Likewise, the parameters reveal different deviations, with the highest value of CD (0.994), followed by AVA, PI, and LF. The p-values of the J-B test are more than 0.05 (except PI), suggesting that the data is normally distributed for most variables.

Table 4 exhibits F-statistics long-run relationship results, which were sensitive in selecting the ideal lag length of a model (Bahmani-Oskooee and Bohl, 2000). The F-statistics bound testing method with critical values has two assumptions in which variables are I(0) for lower bounds and I(1) for the upper bound. F-statistics must be more than the critical values of upper limits while considering null hypothesis rejection. In contrast, the t-statistic value below analytical lower bounds values supports the null hypothesis’s acceptance, whereas the value between upper and lower limits gave inconclusive results. Similarly, lower and higher bounds values at 95% significance level were 2.56 and 3.49, correspondingly. Hence, the estimated F-statistic value (8.649) supports rejecting the null hypothesis of no long-run relationship. It is higher than the upper bound, and there was a long-run cointegration relation among variables.

Table 5 postulated the short-run results based on the Akaike information criterion (AIC) from NARDL estimates. The PI+ and PI- shocks significantly affect AVA; however, the scale of negative shock has a more stimulating effect in the short run. The results suggest that negative and positive shocks in prices enhance agricultural growth by 0.507 and 0.168 percent, respectively. The findings support both hypotheses (H1 and H2), which propose that PI+ and PI- shock effects of commodity prices increase agricultural economic growth. Furthermore, credit disbursement in the agriculture sector had a significant positive relationship with AVA in the short-run, which elaborates that a one percent rise in CD will improve agriculture performance by 0.379%. The positive coefficient of CD indicates that more government agriculture spending will add greater value to agriculture. Moreover, LF has a significant positive relation with AVA, which indicates that a one percent rise in the labor force will expand agriculture development by 1.291% in the short term. In addition, diagnostic test results from asymmetric ARDL estimations are shown at the bottom of Table 5. The adjusted R-square value (0.999) described the best fit of the model. The p-value in SC, normality, and heteroscedasticity tests are more than the significance level, suggesting the rejection of the null assumption. The reported results conclude that the model has found no autocorrelation and heteroscedasticity issues and is appropriately specified. The error terms can be assumed to be independent, and the basic presumptions of the model are probably correct.

Table 6 represents the long-run results from NARDL estimates. Similar to the short run, the PI+ shock significantly influences AVA; however, their magnitude differs. The outcomes imply that PI+ raises growth in agriculture by 0.418%, which endorses H1 hypotheses. Likewise, the PI- shock is also positively linked to AVA in the long term (a coefficient of 0.109), which validates H2 hypotheses. The outcome suggests that whether price indices increase or decrease, they will improve agriculture performance. However, the effect scale is higher for PI+ shock than PI- shock. The PI+ seems good for the farmers; however, PI- does not affect them much. Reducing commodity prices can boost affordability, increasing demand for these goods. To fulfill this demand, farmers need to raise their production levels, which can contribute to agricultural growth.

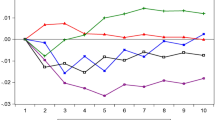

Furthermore, CD in the agriculture sector had a significant positive relationship with AVA in the long run, which elaborates that a one percent rise in CD will increase growth by 0.055%. The positive coefficient of CD elaborates that more expenditure disbursement to the agriculture sector will enhance its growth significantly. Additionally, LF has a significant positive relation with AVA, which specifies that a one percent upsurge in the labor force will enlarge agriculture development by 1.138% in the long term. Moreover, to examine the parameter stability of the selected asymmetric ARDL model, the Cumulative sum of recursive residuals (CUSUM) and the Cumulative sum of squares of recursive residuals (CUSUMSQ) tests were exercised (Brown et al., 1975). Figure 1 graphically expressed the estimated coefficients which is inside the critical bounds (solid dotted lines) at a 5 % significance level; hence, we determined that the model was structurally stable. The straight-line characterizes analytical limits at a 5% level of significance.

Cumulative sum of recursive residuals (CUSUM) and square of CUSUM.

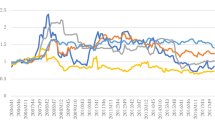

Lastly, Fig. 2 represents the dynamic multiplier graph (DMG) for NARDL model. The DMG shows the volatile reaction of a response variable to a change in an explanatory variable. The negative and positive curves indicated the asymmetric variation of AVA to positive and negative price shocks at a specified time. The results of the dynamic multiplier graph suggest that PI+ shocks have more influence on AVA than adverse price shocks, suggesting the presence of positive asymmetry in the long run.

Dynamic multiplier graph.

Discussion

The results of positive price shocks in agricultural products were startling, suggesting that it will lead to flourishing agriculture growth; however, this can be useful only if the economic conditions of the people are sound enough to bear high costs. Meanwhile, higher costs for agricultural products can result in higher inflation, making it difficult for governments to maintain general financial stability. In the case of Pakistan, the government cannot put extra pressure on the people to improve their growth, where more than half of the population is already below the poverty line. The increased prices burden common people, but in a country like Pakistan, it is a usual practice to raise growth. Rising prices will hurt people with low incomes more because they must spend more money to purchase the same commodities.

Meanwhile, a rise in commodity pricing benefits the harvesters since they receive greater value for their products. Many factors caused a rise in commodity prices during the sample period; however, the most visible events were the Asian financial crises in the late 90 s, 2008 and 2011 global food and oil price crises. Apart from the concerns mentioned above, unfavorable weather conditions (with two major floods in 2010 and 2014), energy crises, expensive fertilizers, monopoly of agricultural companies, inflation, rising oil prices in international markets, foreign debt repayments, exchange rates, and undocumented transboundary trade of agricultural products were also contributed in the rising costs. Government authorities also had undue direct interventions in procurement and sales price determination. The favorable price shock results were aligned with Haji and Gelaw (2012), Joiya and Shahzad (2013), and Awan and Imran (2015) .

Likewise, the adverse shocks in agricultural product prices also positively influenced agricultural economic growth, although in another aspect. The negative shock in the prices can escalate consumer demand and change their behavior to consume more. The increase in consumption may influence farmers to produce additional products with lower production costs, enhancing growth. The inflationary threat can be reduced by lowering the prices of agricultural commodities, which promotes economic development and investment across all industries, including agriculture. However, the adverse shocks in prices were not seen in developing countries normally because once the prices of commodities rise, the reduction is complicated. Additionally, PI- shocks of agricultural products harm the farmers was revealed for Pakistan. The overall results of commodity prices conclude that PI+ and PI- shocks generate economic activities and improve agricultural development with more influence of PI+ than PI- in the long run and also found scarce confirmation of such asymmetry. In conclusion, the price-growth link is complicated since several other elements, including weather patterns, market forces, legislation, and infrastructure, can substantially impact agricultural development.

Moreover, the reported coefficient of CD, in the long run, was observed to be relatively small. Still, it cannot be discouraged because Pakistan will likely need favorable conditions for agricultural investments to assist farmers in meeting the sustenance demands of a rapidly growing population. Unlike the developed world, Pakistan is still missing in setting up long-term goals for its development due to governmental instabilities. The subsequent governments disregarded the policies made by previous administrations because of political conflict, irrespective of its gains to the economy. The authorities and departments lack inefficiency, preventing the money from reaching potential growers. The stated policies require time for implementation to achieve the original specific objectives, so CD sometimes may negatively impact AVA in the short term.

Furthermore, more than 40% of the populace is attached to the agriculture sector for their incomes, with small farmers’ preferring to run their households by utilizing old-fashioned techniques for output. However, these traditional agriculture production methods consume more resources and time, which may negatively impact growth for a shorter period. Moreover, unless the methods of production will not change from traditional ones, subsidies provided by the government will further damage the progress. In this regard, it is crucial to conduct awareness campaigns at the government and local levels to educate farmers about the newly developed agriculture methods and help them transition. This changeover is critical because the annual growth rate of agriculture declines. In 1970, agricultural GDP was 33.43%, but it reduced to 22.7% in 2022. It is an alarming sign for a country known as an agricultural whose population growth rate is among the highest in the entire region. In addition, the results of LF suggest that expanding skilled labor is crucial for improving agricultural production and development in Pakistan. However, in the current scenario with a literacy rate of 60% (minimum in South Asia), it looks challenging for the agriculture sector to avail skilled labor facilities.

Conclusions

The current research contributes to the existing literature by analyzing the positive and negative shocks in agricultural product prices using the NARDL methodology in Pakistan. The variables used in this research were agriculture, forestry, fishing value-added, credit disbursement in agriculture, the labor force, and agricultural product prices from 1970 to 2018. The NARDL approach was used for statistical inferences because of several benefits over other techniques. Empirical results show that positive and negative price shocks in agricultural products contribute to Pakistan’s agricultural growth in the short and long run; however, the positive shock impact is more than the negative shocks. Furthermore, credit disbursement and labor force significantly contribute to agricultural development in the short and long run.

The outcomes of our study suggest that rising prices generate troubles for middle and weak-income groups because they must compromise their education and health allocation budgets for essential agricultural items. A strict and faithful monetary policy is required to support commodity prices. At the ground level, the core responsibility is on price control authorities; hence, it should be observed energetically. Such bodies should avoid any political interference and execute prices spontaneously, as it directly impacts the daily households of the maximum population. Furthermore, the current study found significant and positive results for credit disbursement. Still, a country like Pakistan should critically evaluate its credit disbursement because of the continuous contraction of agriculture’s share of economic growth and consistent budget deficits. A proper balance should be made as more investments will burden the economy further, and fewer subsidies will put extra pressure on producers. The credit disbursement should focus on the development of technological innovation as the traditional methods already reduced the agricultural contribution and raised the food imports. The government should increase the labor force’s education and awareness levels to gain maximum productivity by effectively utilizing scarce resources.

Future research is encouraged to extend the country’s context and replace Pakistan with other agriculture-based countries like African nations to check positive and negative shocks in agriculture product prices. The upcoming analysis can examine the technological effect of agriculture, prices of different commodities (i.e., maize, rice, sugarcane, etc.), environmental variations, and energy sources’ influence on agricultural output. Moreover, the global 2008 and 2012 financial and food crises can be discussed based on the NARDL framework by considering structural breaks. In addition, different time series techniques like ARMA, Johansen test, SARIMA, vector autoregression, ARDL, or panel data methods such as GMM, PMG, and AMG can be used to reveal interesting outcomes or answer new research questions.

Data availability

The final data can be accessed from https://doi.org/10.17605/OSF.IO/DB8J9.

References

ADB (2008) Asian Development Bank. Food Prices and Inflation in Developing Asia: Is Poverty Reduction Coming to an End? Economic and Research Department

Addison T, Ghoshray A, Stamatogiannis MP (2016) Agricultural Commodity Price Shocks and Their Effect on Growth in Sub‐Saharan Africa. J Agric Econ 67(1):47–61

Alene AD, Coulibaly O (2009) The impact of agricultural research on productivity and poverty in sub-Saharan Africa. Food Policy 34(2):198–209

Anderson K (2010) Globalization’s effects on world agricultural trade, 1960–2050. Philos Transac R So B 365(1554):3007–3021

Asteriou D, Hall SG (2015) Applied econometrics: Macmillan International Higher Education

Awan AG, Imran M (2015) Food price inflation and its impact on Pakistan’s economy. Food Sci Qual Manag 41:61–72

Aysan A, Pang G, Véganzonès-Varoudakis M-A (2009) Uncertainty, economic reforms and private investment in the Middle East and North Africa. Appl Econ 41(11):1379–1395

Bahmani-Oskooee M, Bohl MT (2000) German monetary unification and the stability of the German M3 money demand function. Econ Lett 66(2):203–208

Blattman C, Hwang J, Williamson JG (2007) Winners and losers in the commodity lottery: The impact of terms of trade growth and volatility in the Periphery 1870–1939. J Dev Econ 82(1):156–179

Brown RL, Durbin J, Evans JM (1975) Techniques for testing the constancy of regression relationships over time. J R Stat Soc 37(2):149–163

Byerlee D, De Janvry A, Sadoulet E (2009) Agriculture for development: Toward a new paradigm. Annu Rev Resour Econ 1(1):15–31

Chandio AA, Jiang Y, Rehman A (2018) Energy consumption and agricultural economic growth in Pakistan: is there a nexus? Int J Energ Sect Manag 13(3):597–609

Chandio AA, Jiang Y, Rehman A (2019) Using the ARDL-ECM approach to investigate the nexus between support price and wheat production: an empirical evidence from Pakistan. J Asian Bus Econ Stud 26(1):139–152

Chandio AA, Jiang Y, Rehman A, Jingdong L, Dean D (2016) Impact of government expenditure on agricultural sector and economic growth in Pakistan. Am-Eurasian J Agric Environ Sci 16(8):1441–1448

Chandio AA, Magsi H, Ozturk I (2020) Examining the effects of climate change on rice production: case study of Pakistan. Environ Sci Pollution Res 27(8):7812–7822

Collier P, Goderis B (2012) Commodity prices and growth: An empirical investigation. Eur Econ Rev 56(6):1241–1260

Collier P, Gunning JW (1999) Why has Africa grown slowly? J Econ Perspect 13(3):3–22

Deaton A (1999) Commodity prices and growth in Africa. J Econ Perspect 13(3):23–40

Deaton A, Miller R (1996) International commodity prices, macroeconomic performance and politics in Sub-Saharan Africa. J Afr Econ 5(3):99–191

Dhaoui A, Bacha S (2017) Investor emotional biases and trading volume’s asymmetric response: A non-linear ARDL approach tested in S&P500 stock market. Cogent Econ Financ 5(1):1274225

Diao X, Hazell P, Thurlow J (2010) The role of agriculture in African development. World Dev 38(10):1375–1383

Furceri D (2007) Is Government Expenditure Volatility Harmful for Growth? A Cross‐Country Analysis. Fis Stud 28(1):103–120

Gujarati DN (2009). Basic Econometrics: Tata McGraw-Hill Education

Haji J, Gelaw F (2012) Determinants of the recent soaring food inflation in Ethiopia. Univers J Educ Gen Stud 1(8):225–233

Harvey DI, Kellard NM, Madsen JB, Wohar ME (2017) Long-run commodity prices, economic growth, and interest rates: 17th century to the present day. World Dev 89:57–70

Hovhannisyan V, Bozic M (2017) Price endogeneity and food demand in urban China. J Agric Econ 68(2):386–406

Ibrahim MH (2015) Oil and food prices in Malaysia: a nonlinear ARDL analysis. Agric Food Econ 3(1):2

Iganiga B, Unemhilin D (2011) The impact of federal government agricultural expenditure on agricultural output in Nigeria. J Econ 2(2):81–88

Ilyas M, Ahmad HK, Afzal M, Mahmood T (2010) Determinants of manufacturing value added in Pakistan: An application of bounds testing approach to cointegration. Pak Econ Soc Rev 48(2):209–223

Joiya SA, Shahzad AA (2013) Determinants of high food prices: The case of Pakistan. Pak Econ Soc Rev 51(1):93–107

Juselius K, Møller NF, Tarp F (2014) The long‐run impact of foreign aid in 36 African countries: Insights from multivariate time series analysis. Oxf Bull Econ Stat 76(2):153–184

Kashif U, Hong C, Naseem S, Khan WA, Akram MW (2020) Consumer preferences toward organic food and the moderating role of knowledge: a case of Pakistan and Malaysia. Ciência Rural 50(5):1–13

Kashif U, Hong C, Naseem S, Khan WA, Akram MW, Rehman KU, Andleeb S (2023) Assessment of millennial organic food consumption and moderating role of food neophobia in Pakistan. Curr Psychol 42(2):1504–1515

Katrakilidis C, Trachanas E (2012) What drives housing price dynamics in Greece: New evidence from asymmetric ARDL cointegration. Econ Model 29(4):1064–1069

Kilian L (2014) Oil price shocks: Causes and consequences. Annu Rev Resour Econ 6(1):133–154

Kinda T, Mlachila M, Ouedraogo R (2018) Do commodity price shocks weaken the financial sector? World Econ 41(11):3001–3044

Koutroulis A, Panagopoulos Y, Tsouma E (2016) Asymmetry in the response of unemployment to output changes in Greece: Evidence from hidden co-integration. J Econ Asymmet 13:81–88

Lee K, Pesaran MH, Smith R (1997) Growth and convergence in a multi‐country empirical stochastic Solow model. J Appl Econom 12(4):357–392

Maddala GS, Wu S (1999) A comparative study of unit root tests with panel data and a new simple test. Oxf Bull Econ Stat 61(S1):631–652

Meo MS, Chowdhury MAF, Shaikh GM, Ali M, Masood Sheikh S (2018) Asymmetric impact of oil prices, exchange rate, and inflation on tourism demand in Pakistan: new evidence from nonlinear ARDL. Asia Pac J Tour Res 23(4):408–422

PBS (2020) Pakistan Bureau of Statistics. Agriculture Statistics. Government of Pakistan

PES (2022) Pakistan Economic Survey. Pakistan: Ministry of Finance, Government of Pakistan

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econom 16(3):289–326

Raza N, Shahzad SJH, Tiwari AK, Shahbaz M (2016) Asymmetric impact of gold, oil prices and their volatilities on stock prices of emerging markets. Resour Policy 49:290–301

Sethi LN, Kumar DN, Panda SN, Mal BC (2002) Optimal crop planning and conjunctive use of water resources in a coastal river basin. Water Resour Manag 16(2):145–169

Shah SWA, Haq M, Farooq R (2015) Agricultural export and economic growth: A case study of Pakistan. Public Policy Adminis Res 5(8):88–96

Shin Y, Yu B, Greenwood-Nimmo M (2014) Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework Festschrift in Honor of Peter Schmidt (pp. 281–314): Springer

Taghizadeh-Hesary F, Rasoulinezhad E, Yoshino N (2019) Energy and food security: Linkages through price volatility. Energy Policy 128:796–806

Tiffin R, Irz X (2006) Is agriculture the engine of growth? Agric Econ 35(1):79–89

Valdes A (2013) Agriculture Trade and Price Policy in Pakistan. Secondary publication, Washington, D.C., USA. 1–38

Vink N (2012) Food security and African agriculture. South Afr J Int Aff 19(2):157–177

Acknowledgements

This research is supported by Philosophy and Social Sciences Excellent Innovation Team Construction Foundation of Jiangsu Province (Grant Number: SJSZ2020-20). The usual disclaimers apply.

Author information

Authors and Affiliations

Contributions

UK and SN are responsible for data collection, organizing the progress of the paper, article writing, finalization, and structure of the article’s content; JS is responsible for the interpretation of results, structural content of the article, and supervision. MA and RSB are responsible for data collection and analysis, and part of the manuscript writing; WAK and MASA-F are responsible for guiding the topic selection, research methods, final revision, and comprehensive management of the structure of the article.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any authors.

Informed consent

This article does not contain any studies with human participants performed by any authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Kashif, U., Shi, J., Naseem, S. et al. Do agricultural commodity prices asymmetrically affect the performance of value-added agriculture? Evidence from Pakistan using a NARDL model. Humanit Soc Sci Commun 10, 391 (2023). https://doi.org/10.1057/s41599-023-01888-4

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-01888-4

This article is cited by

-

Balancing agriculture, environment and natural resources: insights from Pakistan’s load capacity factor analysis

Clean Technologies and Environmental Policy (2023)