Abstract

The remaining carbon budget for limiting global warming to 1.5 degrees Celsius will probably be exhausted within this decade1,2. Carbon debt3 generated thereafter will need to be compensated by net-negative emissions4. However, economic policy instruments to guarantee potentially very costly net carbon dioxide removal (CDR) have not yet been devised. Here we propose intertemporal instruments to provide the basis for widely applied carbon taxes and emission trading systems to finance a net-negative carbon economy5. We investigate an idealized market approach to incentivize the repayment of previously accrued carbon debt by establishing the responsibility of emitters for the net removal of carbon dioxide through ‘carbon removal obligations’ (CROs). Inherent risks, such as the risk of default by carbon debtors, are addressed by pricing atmospheric CO2 storage through interest on carbon debt. In contrast to the prevailing literature on emission pathways, we find that interest payments for CROs induce substantially more-ambitious near-term decarbonization that is complemented by earlier and less-aggressive deployment of CDR. We conclude that CROs will need to become an integral part of the global climate policy mix if we are to ensure the viability of ambitious climate targets and an equitable distribution of mitigation efforts across generations.

Similar content being viewed by others

Main

Delivering on the many national and corporate net-zero emission pledges will probably require the gross removal of atmospheric carbon dioxide (CO2) on top of conventional emission reductions6,7. To achieve the Paris Agreement, global gross CO2 removals will need to exceed gross residual emissions4,8 after the middle of the century1,9. The resultant net-negative emissions compensate for the carbon debt3 accrued by CO2 emissions that overshoot the remaining carbon budget10,11. Carbon debt is projected to amount to roughly the equivalent of 9 years of global emissions before the COVID-19 pandemic according to the 1.5 °C ‘middle of the road’ scenario P3/S2 of the Intergovernmental Panel on Climate Change (IPCC)1 (Extended Data Table 1). Such large-scale deployment of CDR is controversial mainly for the implied economic and technological risks12,13,14,15,16 and environmental effects17,18; and because reliance on CDR in mitigation scenarios often goes hand-in-hand with a substantial shift of the mitigation burden to future generations19.

Here we would like to highlight a fundamental economic problem associated with the existing assessments of climate mitigation scenarios, aiming to inform international climate negotiations. Existing economic policy instruments for emission control are inadequate to incentivize a global transformation towards a net-negative carbon economy without imposing excessive fiscal burden from 2050 onwards. Currently envisaged carbon tax schemes would turn into public subsidies under net-negative emissions with potentially prohibitive fiscal implications5. Emission trading schemes (ETS), on the other hand, are presently designed to handle only positive emission caps. Negative emissions are merely treated as offsets, suggesting that CO2 emissions from one point in time cannot be compensated by an equivalent quantity of negative emissions at another point in time, as required by most mitigation scenarios. Notably, we observe that pricing the depletion of the remaining carbon budget is fundamentally different to pricing overshot emissions after the depletion of the budget, which has profound implications for the consistent earmarking of accrued revenues from a price on CO2.

We argue that establishing the responsibility of emitters for carbon debt is a prerequisite to ensuring viable net-negative carbon futures. Carbon debt could therefore be treated similar to financial debt, including interest payments on physical liabilities (that is, as a CRO) to internalize the inherent risks. On the basis of this idealized global carbon policy proposal motivated by the IPCC’s mitigation scenarios, our numerical results address the shortcomings of the existing climate mitigation literature20. Despite the conceptual character of this study, we establish profound implications for national carbon policies, which are strongly influenced by the IPCC’s global mitigation pathways in many high-emission countries21.

Carbon pricing for net-negative emissions

Integrated assessment models (IAMs) provide global carbon price paths that serve as a proxy for a wider range of cost-effective climate policy options to achieve specified greenhouse gas mitigation goals9. Such carbon prices typically increase exponentially with the interest rate as a consequence of the Hotelling rule, which defines the intertemporally optimal extraction schedule and price of an non-renewable resource22,23, such as the carbon budget. If understood as a global common, revenues generated from pricing its depletion should consistently add to public budgets, for instance to compensate for the associated welfare effects, which may be unfairly distributed across society. However, in scenarios in which the carbon budget is overshot and subsequently replenished, the budget can no longer be regarded as a non-renewable resource. In this case, the Hotelling rule lends itself to an ‘intertemporal interpretation’ for carbon policy: revenues from carbon pricing after the depletion of the budget can be invested at the market interest rate to finance net carbon removal later in the century. Because marginal abatement costs increase at the market interest rate, this calculation is exact under perfect foresight conditions—as assumed in most IAMs—if the retained funds purchase net-negative emissions at marginal costs later on. Because emitters pay for future net CDR through the carbon price, this intertemporal interpretation is compatible with the ‘polluter pays principle’. The resultant intertemporal financial transfer thereby addresses concerns of intergenerational equity because public budgets in the near-term no longer spuriously benefit from pricing an already depleted resource, while future generations thereafter are forced to replenish the carbon budget through other sources, such as income, sales or payroll taxes. According to the ‘conventional interpretation’ of the Hotelling rule, revenues from carbon pricing are merely treated as contemporaneous additions to public budgets, with no clear earmarking of accrued funds. Notably, as both approaches are simply interpretations of the same underlying carbon price paths, emitters also pay the discounted future costs of net emission removal in case of the conventional interpretation. However, in the absence of consistent earmarking, the financial viability of net CDR in the second half of the twenty-first century is highly doubtful5, and intergenerational equity remains unaccounted for.

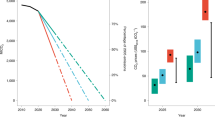

To operationalize a future net-negative carbon economy, carbon tax revenues could be partially retained and transferred over generations to finance net CDR in the style of a nuclear decommissioning trust fund or a sovereign wealth fund. The value of such a global net carbon removal fund is potentially enormous, yet in the range of comparable funds, peaking at roughly 100% of global gross domestic product (GDP) in the median of the Shared Socioeconomic Pathway (SSP) scenarios that are compatible with Representative Concentration Pathway 1.9 (RCP 1.9)24 (Fig. 1). For comparison, Norway’s large sovereign wealth fund has passed 250% of national GDP25. Given this order of magnitude, intermediate investment portfolios could be a game changer to lift CDR out of the pilot phase even before pay-out of the fund. However, protecting financial resources from diversion for other purposes as political environments change, or as public finances become stressed, will surely be extremely challenging. For instance, sovereign borrowing to cushion the effects of the COVID-19 pandemic meant that by the end of 2020 the debt-to-GDP ratio of governments according to the Organisation for Economic Co-operation and Development had increased by about 13.4 percentage points26. Severe crises in the future could induce considerable pressure for governments to appropriate savings originally reserved for net CDR.

a, Bottom, public income and expenditure from a tax on net emissions expressed as a percentage of GDP. Hotelling-compatible (exponential) carbon prices from SSP–RCP 1.9 scenarios are multiplied by net emissions and divided by GDP (grey dashed lines). An idealized income/expenditure curve (black solid line) was derived from these scenarios using a strictly exponential median carbon price, median net emissions and GDP. Instead of reserving 100% of tax revenues after depletion of the carbon budget, we assert that a fraction ϕ = 0.76 of revenues is earmarked for net carbon removal, from 2020 onwards. This share of income (green area) would need to be accrued into a net carbon removal fund invested at the market rate of interest to account for later expenditure when net emissions turn negative. See Methods for a definition of ϕ. b, Top, cumulative payments into the net carbon removal fund (green) and interest (orange) in theory pay exactly for cumulative tax expenditure (blue), such that the net value of the fund (brown solid line) gets exhausted as the warming target is achieved in 2100.

The success of a net CDR fund also depends on the appropriate choice of several inherently uncertain parameters, including future abatement costs. If costs and other socioeconomic parameters are not estimated in line with the precautionary principle, or if regulators are reluctant to adequately reflect future carbon removal in near-term price instruments, insufficient financial resources would be collected as observed for nuclear decommissioning27. Because the carbon debt and associated risks would be mutualized by a net CDR fund, missing financial resources would need to be replenished by public budgets.

Dynamic emission trading

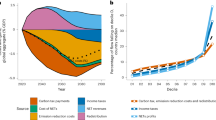

Emission trading with fully liberalized banking and borrowing of allowances can be regarded as a response to these concerns. Decentralized decision-making and price determination in a competitive market is believed to improve efficiency by leveraging the ability of carbon markets to determine cost-effective time paths of mitigation28. In an idealized global scheme, the remaining carbon budget would be distributed over time resulting in positive emission caps for consecutive auctioning periods. Emitters would decide in each period what fraction of their CO2 emissions to compensate for by allowances and how much carbon debt to generate for compensation by future allowances—or future CDR in the absence of a positive emission cap. Effectively, emitters generating carbon debt would remain liable for the timing and delivery of net-negative emissions (Fig. 2) and can therefore balance present against future abatement based on individual expectations, such as those concerning technological breakthroughs. Stranded assets can be avoided by harmonizing abatement investments with natural renewal cycles of capital; and fluctuations in the business cycle can be addressed. Fixed price schedules under a carbon tax suggest lower costs for hedging risks related to the long-run costs of negative emissions and low-carbon investments. However, increased intertemporal flexibility in emission trading stabilizes the price—which reflects discounted future marginal abatement costs—compared with currently implemented ETS with no intertemporal trade of allowances29,30. At least in principle, this ETS arrangement enables emitters to develop optimal investments over longer time horizons, increasing the dynamic efficiency of emission trading. Although emission caps can be overshot, the quantity of cumulative emissions remains exactly controlled under an ETS with intertemporal trade of carbon debt, which is, more generally, the main advantage of cap-and-trade schemes compared with carbon taxes. If caps no longer directly control emission reductions, they can be set to equitably distribute ETS revenues over time. However, as the carbon budget diminishes rapidly—the 1.5 °C compatible budget is projected to become depleted roughly within the next 10 years1—the importance of carbon debt management increasingly outweighs the requirement of an adequate temporal distribution of the remaining carbon budget.

Illustrative 2 °C pathway with gross carbon emissions from FFI, LUC and non-specified sources of CDR including the schematic architecture of idealized global intertemporal emission trading. ETS emission caps bt are obtained by distributing the carbon budget in tranches over consecutive periods. The amount by which emission caps bt are exceeded by net emissions is conceptualized as ‘carbon debt’ (dt). In this idealized illustration, dt is compensated later by corresponding net-negative emissions (eNN,t) such that dt = −eNN,t. In a conventional ETS, emission caps would be set to bt + dt, and eNN,t would have to be incentivized by public subsidies. dt, bt and eNN,t (in which t indicates 1, 2 and so on) are simplified discrete analogues of the continuous variables d(t), b(t) and eNN(t), respectively, which are described in the Methods. Historical emissions are from a previously published study39.

Privately managed carbon debt within an ETS also has considerable drawbacks: the enforcement of carbon debt, assessment of creditworthiness of emitters, the potential for speculation on future softening of emission targets and subsequent deferral of mitigation (time inconsistency)—which is stronger the lower the solvency of emitters (adverse selection)—and the resultant incentive to lobby for cancellation of carbon debt (moral hazard) are crucial obstacles that explain why such intertemporal mechanisms are severely restricted in currently implemented ETS28. Moreover, intertemporal trade of carbon debt by means of forward and future markets trading negative emissions over potentially long periods at a fixed price is perceived as infeasible, given the deep uncertainty in the parameters guiding a large-scale CDR rollout31.

Carbon removal obligations

Intertemporal emission trading would necessarily come at the cost of considerable regulation to address these drawbacks. We argue, however, that practices from the financial industry and monetary policy could be leveraged to reduce risks and adaptively balance potentially competing interests of economic development and climate mitigation by treating carbon debt in a similar manner to a financial debt obligation, and thereby invoking an interest on carbon debt. Economic growth, aggregate demand for carbon debt and individual financial ratings of debtors would define a general base rate, individual mark-ups, term structures and debt maturities. To assure its physical conservation and exert control over its aggregate level, carbon debt would initially be issued at the base rate by managing authorities—for example, Central Banks—to which commercial banks would be held liable in case of insolvent debtors. Commercial banks, or their equivalents, would issue debt to emitters and, assisted by rating agencies, assess and hedge their insolvency risk by determining individual mark-ups on the base rate. Carbon debt would enter the balance sheets of firms as a physical liability in tonnes (t) CO2—a carbon removal obligation, for which interest payments would be due (Extended Data Fig. 7a). This chain of legal liabilities across layers of public and private actors reduces the moral hazard that governments would ultimately pick up the bill for net emission removal, and limit the issuance of CROs to debtors who are reluctant to fulfil their (interest) obligations. Individual interest mark-ups would also balance the push of the market for adverse selection and incentivize a debt transfer from agents losing ground under stringent climate policy to low-risk agents; or lead to more near-term abatement (see below) if risks are deemed non-insurable. The rate controls the volatility of the carbon price (Extended Data Fig. 1) and therefore directly affects the price–risk costs of scheduled abatement investments. More generally, interest and debt maturities would need to reflect the speculative nature of CDR, leading to short—but potentially renewable—repayment terms and elevated rates in the near-term. A concrete phase-in scenario of CROs in the ETS of the European Union and beyond is described in Box 1.

For intertemporal emission trading to work efficiently—for instance to reduce issues of time inconsistency and price volatility—emission caps would need to be credibly announced as early as possible. As a consequence, regulators would lose the flexibility of adapting caps as new knowledge concerning the Earth system becomes available. In an idealized global scheme, emission caps need to exactly reflect the remaining carbon budget. Budget uncertainties related to the issuing of carbon debt, similar to those of permafrost thaw after a temperature overshoot2, could be hedged by collecting risk funds through base rate payments and by incentivizing more-ambitious emission reductions to minimize the risk of climate feedback effects (see below). Such uncertainties should remain manageable by risk reserves, allowing for the budget to be replenished by drawing on risk funds rather than requiring a downwards correction of scheduled emissions caps. In the best case, uncertainties and base rates would decrease over time as updated estimates of the carbon budget converge to a value within the expected range of the previously announced budget. However, new findings might realistically also lead to exceeding of the abilities of risk management, requiring a combined effort of future generations to counter potentially abrupt climate change. Management of physical risks therefore remains limited to what is presently perceivable and realistically quantifiable.

Climate mitigation under carbon debt

In IAMs, abatement costs are discounted at the market interest rate, implying a cost advantage for abatement in the distant future compared with near-term decarbonization in terms of net present value. The interest rate is therefore a key driver of carbon debt accrual in IAMs32,33. This ‘discounting effect’ is balanced by imposing interest on carbon debt. Longer CRO maturities indicate lower net present costs for CDR. Simultaneously, carbon debt interest is paid over a longer period, compensating for these gains. When the market rate of interest and the carbon debt interest rate (rd) coincide, the gains from discounting are balanced exactly, as we analytically show in the Methods. In Fig. 3, we illustrate the sensitivity of 2 °C-compatible global mitigation pathways to interest on carbon debt, with rates constant over the 2020–2100 period ranging from rd = 0 to rd = 0.08. For each rate, 13 scenarios are computed based on different SSPs and IAMs that are used to calibrate the marginal abatement cost curves of our model (Extended Data Table 2).

a, Net CO2 emissions of all scenarios with rd = 0 (turquoise) and rd = 0.08 (yellow), including geometric median paths (bold solid lines) and minimum to maximum ranges (shaded areas). b, Marginal abatement costs of scenarios with rd = 0 (turquoise) and rd = 0.08 (yellow). Bold solid lines indicate geometric medians, shaded areas indicate 25–75% interquartile ranges. c, d, Geometric median net emissions as in a, including gross emissions from FFI, BECCS and LUC. c, rd = 0. d, rd = 0.08. e, Total discounted abatement costs (net present value, including interest costs) expressed as a percentage cost increase compared with the baseline (rd = 0) are shown as function of total carbon debt D. The boxes indicate the 25–75% interquartile ranges around the median values of the costs and D. Symbols linked by grey solid lines indicate the medians grouped by SSP. The entire dataset is shown in the top right corner, in which each scenario is reflected by a symbol, grouped by SSP (symbol type) and rd (colour).

For comparison, only the two extreme cases—rd = 0 and rd = 0.08—are illustrated in Fig. 3a–d. Notably, when rd = 0.08, the cumulative emission target is achieved without the accrual of carbon debt in the median path (Fig. 3d), suggesting that emissions remain at the net-zero level once achieved. This is accomplished by the contemporaneous compensation of residual CO2 from fossil fuels and industry (FFI) with negative emissions from bioenergy with carbon capture and storage (BECCS) and land-use change (LUC). Complete decarbonization of FFI emissions is, however, not cost-effective owing to the high marginal costs of emission reductions from hard-to-abate sectors. Notably, net-negative emissions of individual scenarios in Fig. 3a turn back to zero before 2100, thereby minimizing the ‘problem of phasedown’34. With reduced reliance on net-negative emissions, marginal costs are higher in the near-term due to the more-rapid reduction in FFI emissions and increase in BECCS, but considerably lower in 2100 (Fig. 3b). Figure 3e shows a reduction in the total carbon debt D as rd is gradually increased. Carbon debt risks are therefore greatly reduced at a moderate cost increase of below 12.5% in more than 75% of scenarios in which rd > 0.02.

A similar analysis was performed for the 1.5 °C global warming target; however, direct air capture and storage (DACS) is added to the mitigation technology mix, represented by six different DACS-specific marginal abatement cost curves with low, medium and high costs as well as low- and high-capacity limits. This results in a set of 78 scenarios for each rate rd. Not surprisingly, the higher the potential for DACS to be deployed, the larger the level of D when rd = 0. By contrast, when interest is invoked, this discounting effect is reversed and scenarios with large-capacity low-cost DACS simultaneously exhibit the lowest levels of D (Extended Data Fig. 2). The pathways in Fig. 4 show baseline (Fig. 4a, b) and reduced D (Fig. 4c, d) scenarios for those scenarios that achieve a reduction in D of at least 30% compared with their associated baselines (see Extended Data Figs. 3–5 for reductions of 5%, 15% and 45%, respectively). For illustration, we interpret the CRO-ETS baseline scenarios, in which rd = 0, as conventional ETS scenarios because both schemes are theoretically equivalent in terms of the resultant emission profiles while they imply a qualitatively different timing of financial flows.

a, b, A conventional ETS is used. c, d, A CRO-ETS is used. a, c, Geometric median net emissions (solid line) and gross emissions from FFI, BECCS, LUC and DACS. Net emissions from a are also displayed in c (dashed line) and vice versa. The total carbon debt D is shown as a box-and-whiskers plot. Boxes indicate the 25–75% interquartile range around the median values (bold line), whiskers indicate minimum to maximum ranges, points mark the outliers. b, d, Annual mitigation costs as a percentage of GDP, including the share of average abatement costs attributed to emission reductions (ABM), to the compensation of residual emissions by CDR (RES) and to net-negative emissions (NNE), as well as expenditures for allowances (ETS) and interest costs (INT). Total mitigation costs (that is, ABM + RES + NNE + ETS + INT) from d are also displayed in b (dashed line) and vice versa. Box-and-whiskers plots show the total discounted abatement costs (that is, ABM + RES + NNE) as a percentage of GDP, the number above the chart indicates out-of-range outliers. Pie charts in d summarize the properties of the underlying set of scenarios (see Methods). The distribution of rd in CRO-ETS scenarios is depicted in c.

Despite the earlier increase in DACS in Fig. 4c, causing emissions to turn net zero around 2050, an emission overshoot appears to be inevitable if warming is to be limited to 1.5 °C. Remaining net-negative emissions might cause problems of phasedown in 2100, unless CRO maturities are further extended to enable a smooth transition to net-zero emissions; or more net-negative emissions are needed to stabilize the climate in the twenty-second century35. Therefore, the median D is equal to roughly 7 years of global net emissions in 2019 in Fig. 4c. Yet, the role of CDR changes considerably: without considering risks, CDR seems to justify late-century compensation of carbon debt. In this case, the median D is equivalent to about 11 years of 2019 global net emissions, with compensation starting roughly 10 years later in Fig. 4a. However, when risks are accounted for by imposing interest, CDR supports a rapid decrease in net emissions by balancing the residual emissions. Controversially, the availability of cheap and large-scale CDR options, such as DACS, is key in 1.5 °C scenarios with reduced reliance on the accrual of carbon debt. As illustrated by the pie charts in Fig. 4d, the share of high-capacity DACS scenarios among feasible scenarios with respect to the 30% reduction requirement grows to 81% (50% in the underlying set) and the share of low-cost DACS scenarios to 54% (33% in the underlying set). Should CDR not become readily available as asserted in IAMs36,37,38, this would be reflected in an elevated carbon debt interest rate, incentivizing emission reductions provided by other sources, such as the replacement of fossil fuel with renewable energy sources in hard-to-abate sectors—even if this leads to much higher costs.

Effect on financial flows over time

Figure 4, moreover, illustrates the distribution of annual mitigation cost shares, including investments in emission reductions and negative emissions and the financial flows associated with ETS allowances and interest for CROs. The share of abatement costs for emission reductions (ABM), negative emissions compensating for residual emissions (RES) and net-negative emissions (NNE) incurred in the near- versus the long-term increases with larger levels of rd (compare Fig. 4d to Extended Data Figs. 3d–5d). Here, CROs with interest induce a more equitable temporal distribution of these cost items, in sum peaking at 2.4% in Fig. 4d compared to 4.5% of GDP in Fig. 4b. This is partly because the CRO-ETS requires carbon debtors to reserve financial resources early in the century, and such funds earn interest until they are spent for net-negative emissions. By contrast, net-negative emissions expenditures in Fig. 4b are incurred at the time of net carbon removal and would need to be funded by public sources in the absence of intertemporal financial transfers. Note that here we show average abatement costs. If marginal costs are paid by incentivizing net CDR on a market, public expenditures are much higher (for comparison, see Fig. 1). Pricing overshot emissions under a conventional ETS, moreover, implies much larger revenues (‘ETS’) than under the CRO-ETS, where emission caps reflect exactly the remaining carbon budget. Median total discounted abatement costs, excluding ETS costs and interest costs (‘INT’), increase from 1.6% to 2.0% of GDP when interest is invoked within the CRO-ETS. Median interest costs in these scenarios are substantial, peaking at above 1.3% of GDP, and 0.4% to 1.5% in Extended Data Figs. 3–5. These numbers are, however, highly uncertain and will need to be determined considering the viability and scalability of near-term CDR options and other emission reduction technologies.

Enlarging IAM CDR portfolios to reduce technological risks and environmental effects would probably lead to further burdening of future generations in scenarios if CDR remains primarily a motivation for reducing net present costs by accrual of carbon debt. This is especially problematic if such results trickle down through the IPCC and international climate negotiations into national target setting because no viable mechanisms for the repayment of carbon debt have entered the policy debate at the moment. Simultaneously, mitigation pathways with reduced carbon debt heavily rely on CDR, requiring that risks be appropriately managed. Similar pathways result from lowering the market interest rate in IAMs32 or from adequately setting intermediate climate targets or constraints on net emissions20. However, such measures would individually not resolve the more profound issue of finance of net-negative emissions discussed here.

Conclusion

In view of the rapid depletion of the global carbon budget, CROs seem to be indispensable for any robust climate mitigation framework. CROs imply a paradigm shift from pricing the permanent to pricing the temporary storage of CO2 in the atmosphere, with carbon debtors being responsible for delivering net CDR. The implied flexibility for emitters also bears the largest drawback of intertemporal emission trading, if public bailout of carbon debtors becomes necessary. To minimize such risks, the ‘conservation of carbon debt’ needs to take top priority by controlling the total amount of carbon debt and by establishing liability across several layers of actors. Risk management under a CRO-ETS relies on imposing interest on carbon debt. For higher and risk-adjusted carbon debt interest rates, net-negative emission investments no longer benefit from net present cost gains when mitigation is deferred to the distant future. By implication, CDR under a CRO-ETS will need to prove its viability compared with conventional options for the reduction of emissions already in the near-term. This will promote bottom-up CDR market development with the accompanying benefits of price discovery, earlier technological learning, testing of scalability and identification of socio-environmental co-benefits and hazards, and ultimately, eliminating the uncertainties surrounding CDR.

Methods

Basic analytical setup

Emission reductions induced by a CRO-ETS are quantified using a Hotelling-type optimization problem (see ref. 32 for an analytical solution of the model). A global social planner is tasked to implement emission reductions at minimum costs to meet a cumulative emission target—that is, the remaining carbon budget B—by T = 2100 (t0 = 2020). Exogenously given baseline emissions Ebase—that is, future emission paths based on ‘business-as-usual’ climate policy assumptions, are reduced by a fraction a to obtain net emissions e:

Total abatement costs ctot are discounted at the market interest rate r to obtain the net present value of total abatement costs, which is minimized:

subject to:

Integrating over marginal abatement costs MAC(a) gives the cost per tonne CO2 for an instantaneous emission reduction of a compared to the baseline. Consequently, total abatement costs ctot are defined as:

Assume that under an idealized CRO-ETS, a constant fraction 1 − ϕ of net-positive emissions eNP is equivalent to a (continuous) emission cap b (that is, the amount of conventional emission allowances issued over time) and ϕ < 1 of eNP equals carbon debt d (that is, the quantity of CROs issued). Then ϕ is defined as the ratio of cumulative net-negative emissions eNN to cumulative net-positive emissions eNP:

and net-negative emissions and net-positive emissions equal the negative and positive parts of net emissions (eNP, eNN > 0)

Carbon debt d and the continuous emission cap b are defined as:

and total carbon debt D is obtained by integration over the planning horizon T (combining equations (5) and (8)):

Consequently, we can write ϕ as:

By implication, a fraction ϕ of cumulative net-positive emissions overshoots B and thereby generates D, and a fraction 1 − ϕ depletes the budget B.

Instead of exogenously imposing ETS emission caps, ϕ allows us to endogenously compute caps b and carbon debt d to conceptualize the intertemporal allocation of carbon debt such that debt is solely compensated by net-negative emissions eNN. On this basis, we can compute a ‘physical repayment term’ TR linking the timing of net-positive to net-negative emissions (equation (12)). CROs in this idealized ETS therefore represent a long-term intertemporal net transaction for financing net-negative emissions. This aggregate can be regarded as a proxy for a multitude of smaller carbon debt transfers over shorter timeframes that are possible in real ETS implementations in which CROs can be compensated by (gross) carbon removal, issuance of new CROs or allowances at a later point in time.

Average abatement costs are obtained from total abatement costs by dividing by the abated quantity of CO2:

Next, we introduce interest payments that are due for carbon debt d over the repayment term t → t + TR(t), that is, from issuance of the CRO until its retirement (Extended Data Fig. 7b–e). TR is implicitly defined as:

and instantaneous interest payments are obtained by multiplication of the quantity of CO2 for which CROs have been issued (d = ϕeNP) and the average abatement costs, cavg, the moment of retirement of the CRO, t + TR(t), with the interest rate on carbon debt rd:

Integrating and discounting instantaneous interest payments over the repayment term TR gives the total net present interest costs at t for carbon debt d(t):

Now we add interest costs to the standard objective function (equation (2)) to obtain the optimization problem for a CRO-ETS:

Mitigation cost discounting

If we set r = rd, the objective function can be written as (Supplementary Information section 3):

Notably, instead of pricing eNN, carbon debt d in this new formulation is paid for the moment it is created; however, it is paid for at the average (undiscounted) future costs during removal at t + TR, which is due to our definition of interest costs in equation (13). This is because when we set r = rd, interest payments exactly compensate for the cost reduction in the net present value terms from discounting. The second term, Ebase(t) − eNP(t) equals emission reductions in the net-positive/net-zero domain. These reductions can be achieved by a mix of CDR, low-carbon and zero-carbon technologies; however, CDR is deployed only to offset contemporaneous emissions and not to recapture previously released CO2.

Intuitively, rd therefore controls to what extent cost discounting becomes a driver for accruing carbon debt. If rd equals the market interest rate, future costs cavg at t + TR—which depend on technological learning and the aggregate demand for abatement a in t + TR—determine whether the carbon debt route (d) proves competitive compared to instantaneous emission reductions (Ebase − eNP). However, if d is reduced, eNP needs to be reduced simultaneously to meet the emission target (less carbon debt leads to higher demand for near-term emission reductions and, therefore, an increase in near-term marginal costs). Because near-term emission reductions potentially include CDR, technological and socio-environmental learning associated with CDR is induced earlier, leading to a reduction in the uncertainty, which is key for operating in the net-negative domain later in the century. In this Article, we provide some intuition about the dynamic effects of invoking an interest on carbon debt, but do not determine optimal risk-reducing rates, which could—but do not necessarily need to—coincide with market interest rates. However, we expect, under circumstances in which physical and financial risks associated with carbon debt are managed by appropriately setting an interest rate on carbon debt, that rd is driven by the market interest rate. In our model, an increase in the market interest rate induces deferral of mitigation due to discounting, leading to higher quantities of D, thereby also to an increase in risks and, finally, the necessity to correct rd upwards to account for the increased risks.

Assessing the value of carbon debt

Net present cost gains from discounting are only cancelled exactly if the market interest rate is invoked on abatement costs at t + TR. Costs are known in our model, but are potentially impossible to determine in the context of real emission control policy. Therefore, given their liability for issued debt, managing authorities and financial institutions need to estimate the financial value of carbon debt as a basis for interest payments and CRO maturities. The incentive to correctly value debt has a societal benefit of gradually reducing uncertainty with respect to CDR and other technologies relied on at large scales in mitigation scenarios. Notably, by prudently valuing debt, issuing bodies assure the quality of price signals on carbon markets, instead of relying on the carbon price to value debt. In fact, carbon prices on their own are insufficient benchmarks for valuing debt. For instance, a large demand for carbon debt would lead to a lower near-term carbon price if this is not balanced by an increase in rd, which in turn would lead to an undervaluation of risks.

Supply and demand of CROs

The supply of allowances under a pure ETS is completely inelastic, whereas the supply in a tax system is infinitely elastic. By contrast, the supply of CROs (adding to the supply of allowances) is finitely elastic. Generally, the supply curve is increasing because the larger the demand for CROs, the more abatement is required in the future, making future abatement and thus CROs more expensive. Because the total discounted interest costs (itot) are reflected in the supply curve, by valuing carbon debt and setting the rate rd accordingly, debt-issuing bodies can partly control its slope. The slope, however, determines the level of price volatility, for example, resulting from a demand shock, as depicted in Extended Data Fig. 1. By implication, price volatility is the largest in a pure ETS, and zero in a tax system. By increasing the interest costs in a CRO-ETS, the potential for volatile prices increases, and vice versa. On the other hand, net emissions are fixed in an idealized ETS and subject to demand fluctuations in a tax system. In a CRO-ETS, the cumulative quantity of net emissions is fixed, however, only if default risks are adequately managed.

Numerical solution of the model

The model used to solve the CRO optimization problem (equation (15)) is based on marginal abatement cost curves (MACCs; equation (4)) that are derived from scenarios reported in the SSP scenario database24,54. MACCs are derived for each IAM and SSP by combining and fitting a curve to carbon prices from different RCPs in each time step. For instance, a MACC in 2040 for a specific IAM–SSP configuration is composed of the carbon prices reported for RCP 1.9–RCP 6.0. The set of parameters of each IAM–SSP configuration of our model is therefore composed of net emissions from the baseline scenario (Ebase), the interest rate r (derived from the slope of log-transformed carbon prices), the carbon budget B derived from the sum of net emissions compatible with specific climate targets and eight MACCs for the period from 2030 to 2100, that is, one per decade. We fix abatement rates a during optimization in which no MACCs could be derived because the reported prices pi are (close to) zero over the whole range of ai—that is, in 2020 for all configurations; for IMAGE–SSP 2 in 2030; for IMAGE–SSP 3 in 2030 and 2040; for IMAGE–SSP 5 in 2030. In decades in which abatement is fixed, costs are set to zero. Moreover, for the 1.5 °C and 2 °C case studies, carbon budgets were corrected using historical emission data39 (scenarios reported in the SSP database start in 2005 or 2010 and were exceeded by estimated net emissions in the past decades). Baseline emissions in 2020 were replaced by the projection for 2019 in ref. 39.

We fit the inverse of the generalized logistic function55 to log-transformed prices pi as reported in the SSP database. Abatement rates ai are computed by subtracting net emissions in a scenario with a climate target from the net emissions in the baseline scenario and dividing by the baseline. The index i denotes the different RCPs within the same IAM–SSP configuration and the same year (see Supplementary Information section 2.1 for the cost curves of all IAM–SSP configurations):

MACs are therefore a power law defined for the interval \(\{a\,\in {\mathbb{R}}|L < a < A\}\):

where b = exp(P) and \(c=\frac{1}{k}\). An interpretation of the parameters is provided in Extended Data Fig. 8a. L ≈ 0 (subject to model fitting) and A = max(ai) + ε (such that a can become max(ai) without MAC(a) becoming ∞)—that is, A is set to the maximum abatement (plus ε = 0.01) observed in each decade for each IAM–SSP configuration because this level cannot be exceeded. For numerical reasons, however, a is also constrained by A during optimization such that a < A.

In most IAMs, the carbon prices are either imposed exogenously as driver of mitigation (for example, in the recursive dynamic models AIM–CGE or GCAM4) or prices are derived after optimization from Lagrange multipliers of emission caps (for example, in the intertemporal optimization models MESSAGE–GLOBIOM, WITCH–GLOBIOM or REMIND–MAgPIE). In these cases, the carbon prices typically increase exponentially with the interest rate, as explained by the Hotelling rule22,23. In heavily constrained, detailed process-based IAMs, intertemporally optimal carbon prices are a good proxy of marginal costs; however, they do not necessarily reflect MACs exactly in each point of time, as a consequence of growth constraints or caps on total deployment levels of specific mitigation technologies. This is also the case here because we limit a < A with an additional constraint and we fix a in cases in which no MACCs could be derived, suggesting that MAC and carbon prices (derived from the Lagrange multiplier of the budget constraint (equation (3))) do not necessarily coincide.

We compare MAC and carbon prices from our model with carbon prices as reported for the individual scenarios in the SSP database for all models, SSPs and RCPs (Supplementary Information section 2.2). Reported carbon prices in the database for AIM–CGE do not follow an exact exponential curve because these prices reflect marginal costs from the SSP 1 scenario, which was initially constrained by emission caps to obtain the climate target. Then, prices were manually scaled and imposed on other SSP scenarios to achieve the respective climate targets56. Therefore, AIM–CGE prices are better replicated by the MAC of our model than by carbon prices. The same is true for the IMAGE framework, which contains simulation as well as optimization components and does not report Hotelling-type carbon prices.

Furthermore, we show abatement costs for all SSPs, IAMs and RCPs computed with our model (Supplementary Information section 2.3). Because abatement costs are not explicitly reported in the database, we compare costs from our model with close proxies—that is, GDP loss and consumption loss in SSP scenarios. For GCAM4 and IMAGE, GDP loss and consumption loss are either not reported or losses are close to zero. For GCAM4, we therefore added abatement costs for some scenarios as reported in the supplementary information of ref. 57, which are well replicated by our model. No comparable data could be retrieved for the IMAGE model. For the other IAMs, abatement costs of our model mainly coincide with consumption loss. Net CO2 emissions are also compared for all SSPs, IAMs and RCPs (Supplementary Information section 2.4).

Abatement rates a cannot exceed A, hence only IAM–SSP configurations with RCP 1.9 data are used for our 2 °C case studies, because more-ambitious mitigation under a CRO-ETS requires our model to partly operate in the 1.5 °C abatement domain to achieve 2 °C. Therefore, thirteen IAM–SSP parameter sets of our model are used for the case studies: AIM–CGE (SSP 1 and SSP 2), GCAM4 (SSP 1, SSP 2 and SSP 5), IMAGE (SSP 1), MESSAGE–GLOBIOM (SSP 1 and SSP 2), REMIND–MAgPIE (SSP 1, SSP 2 and SSP 5), WITCH–GLOBIOM (SSP 1 and SSP 4); that is, six parameter sets for SSP 1, four for SSP 2, one for SSP 4 and two for SSP 5 (Extended Data Table 2). All 2 °C scenarios are shown graphically in Supplementary Information section 1.1 and numerically in Supplementary Information section 1.2.

Scenarios for DACS

For our 1.5 °C (RCP 1.9) case study, additional sources of abatement are required to assess compatible pathways of more-ambitious mitigation than suggested by RCP 1.9 scenarios. We therefore add DACS to the mitigation portfolio; however, we treat this technology in a stylized manner as completely stand-alone and independent of other abatement technologies (for example, the energy needs for DACS are assumed to be met by additional local renewable sources that do not interfere with the ramp-up of renewable energy as part of conventional abatement). DACS is less controversial than BECCS with respect to land use and has potentially limited environmental effects compared to other large-scale CDR options16, making it more independently scalable. However, capital and energy requirements are uncertain and potentially enormous. Costs range between US$20 and US$1,000 per t CO2 (refs. 16,18,58,59,60) and potentials for CDR range from 0.5–5 Gt CO2 yr−1 in 2050 to 15–40 Gt CO2 yr−1 in 210018; however, these potentials are mainly constrained by cost considerations rather than biophysical limits61. Here we derive six idealized MACCs for DACS covering three cost ranges and two maximum abatement rates (Extended Data Fig. 8b). Instead of modifying the MACCs derived from SSP scenarios to account for DACS, we add aDACS to equation (1):

and change the total costs in equation (4) to:

Moreover, MACs are always required to be equal:

To obtain a detailed technology downscaling of sources and sinks of CO2 (fossil fuels and industry, including residual emissions from carbon capture and storage; BECCS and land-use emissions) we interpolate linearly between the closest abatement levels reported in the SSP database—that is, ai < a < ai+1 (again, i denotes different RCPs within the same IAM–SSP configuration and the same year)—and add DACS after the interpolation.

The 1.5 °C scenarios used

For Fig. 4, the set of all 468 scenarios (13 IAM–SSP parameter sets, 6 rates rd and 6 DACS parameters sets) is filtered for scenarios that achieved at least a 30% reduction in D compared with their baselines (that is, where rd = 0). For scenarios depicted in Extended Data Figs. 3–5 this reduction in D needs to be at least 5%, 15% and 45%, respectively. From scenarios with different rates rd but otherwise identical parameters, only the lowest rate is kept, resulting in a potential set of 78 scenarios, of which 26 are feasible regarding the 30% carbon debt reduction requirement in Fig. 4. Hence, in Fig. 4c, d the 26 scenarios for which rd > 0 are compared to the associated 26 baselines in Fig. 4a, b in which rd = 0. Baselines are interpreted as ‘conventional ETS’ scenarios, which are—in terms of emission paths—equivalent to CRO-ETS scenarios with rd = 0. All underlying scenarios are shown graphically in Supplementary Information section 1.3 and numerically in Supplementary Information section 1.4, abatement and interest costs are illustrated in Extended Data Fig. 6 for all scenarios.

A note on technological learning

Technological learning in most IAMs is either exogenous—that is, purely time dependent—or induced by learning-by-doing, which is strongly backed by empirical evidence. However, learning is best perceived as a complex interplay between research and development, learning-by-doing and different types of spillovers62, which only few models attempt to fully address. The MACCs derived here from SSP scenario results reflect learning rates in the IAMs that are used to generate these scenarios, resulting in typically decreasing marginal costs over time for similar abatement rates. Therefore, learning in our model is exogenous (purely time dependent), which is one of the main caveats of this model, because fixed learning rates over time imply an incentive to wait until abatement becomes cheaper. More-ambitious near-term mitigation under a CRO-ETS, however, would probably lead to earlier cost reductions than reflected in the model. Owing to the complexity of learning and the simplicity of our model, we disregard DACS-related technological change.

Software and solver

The model is solved using the CONOPT solver in GAMS v.26.1. CONOPT is based on the generalized reduced gradient algorithm, one of the most robust and commonly applied methods for solving models with highly nonlinear objective functions or constraints63.

Data availability

All data generated or analysed during this study are included in this published Article and its Supplementary Information.

Code availability

The source code of the numerical model used for generating the data used in this study is available at https://github.com/jobednar/CROmodel. The numerical model was calibrated using scenarios from the SSP scenario database hosted by IIASA (https://tntcat.iiasa.ac.at/SspDb/).

References

Masson-Delmotte, V. et al. Global warming of 1.5 °C. An IPCC Special Report (IPCC, 2018).

Gasser, T. et al. Path-dependent reductions in CO2 emission budgets caused by permafrost carbon release. Nat. Geosci. 11, 830–835 (2018).

Geden, O. The Paris Agreement and the inherent inconsistency of climate policymaking. Wiley Interdiscip. Rev. Clim. Change 7, 790–797 (2016).

Peters, G. P. & Geden, O. Catalysing a political shift from low to negative carbon. Nat. Clim. Change 7, 619–621 (2017).

Bednar, J., Obersteiner, M. & Wagner, F. On the financial viability of negative emissions. Nat. Commun. 10, 1783 (2019).

Black, R. et al. Taking Stock: A Global Assessment of Net Zero Targets https://eciu.net/analysis/reports/2021/taking-stock-assessment-net-zero-targets (ECIU, 2021).

Rogelj, J., Geden, O., Cowie, A. & Reisinger, A. Three ways to improve net-zero emissions targets. Nature 591, 365–368 (2021).

McLaren, D. P., Tyfield, D. P., Willis, R., Szerszynski, B. & Markusson, N. O. Beyond “net-zero”: a case for separate targets for emissions reduction and negative emissions. Front. Clim. 1, 4 (2019).

Clarke, L. et al. Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change (eds Edenhofer, O. et al.) Ch. 6, 413–510 (Cambridge Univ. Press, 2014).

Rogelj, J., Forster, P. M., Kriegler, E., Smith, C. J. & Séférian, R. Estimating and tracking the remaining carbon budget for stringent climate targets. Nature 571, 335–342 (2019).

Rogelj, J. et al. Differences between carbon budget estimates unravelled. Nat. Clim. Change 6, 245–252 (2016).

van Vuuren, D. P., Hof, A. F., van Sluisveld, M. A. E. & Riahi, K. Open discussion of negative emissions is urgently needed. Nat. Energy 2, 902–904 (2017).

Honegger, M. & Reiner, D. The political economy of negative emissions technologies: consequences for international policy design. Clim. Policy 18, 306–321 (2018).

Anderson, K. & Peters, G. The trouble with negative emissions. Science 354, 182–183 (2016).

Fuss, S. et al. Betting on negative emissions. Nat. Clim. Change 4, 850–853 (2014).

Lawrence, M. G. et al. Evaluating climate geoengineering proposals in the context of the Paris Agreement temperature goals. Nat. Commun. 9, 3734 (2018).

Lenzi, D., Lamb, W. F., Hilaire, J., Kowarsch, M. & Minx, J. C. Don’t deploy negative emissions technologies without ethical analysis. Nature 561, 303–305 (2018).

Fuss, S. et al. Negative emissions—part 2: costs, potentials and side effects. Environ. Res. Lett. 13, 063002 (2018).

Obersteiner, M. et al. How to spend a dwindling greenhouse gas budget. Nat. Clim. Change 8, 7–10 (2018).

Rogelj, J. et al. A new scenario logic for the Paris Agreement long-term temperature goal. Nature 573, 357–363 (2019).

United Nations Environment Programme. The Emissions Gap Report 2019, Annex B (UN, 2019).

Hotelling, H. The economics of exhaustible resources. J. Polit. Econ. 39, 137–175 (1931).

Mattauch, L. et al. Steering The Climate System: An Extended Comment Centre for Climate Change Economics and Policy Working Paper 347/Grantham Research Institute on Climate Change and the Environment Working Paper 315 (London School of Economics and Political Science, 2018).

Rogelj, J. et al. Scenarios towards limiting global mean temperature increase below 1.5 °C. Nat. Clim. Change 8, 325–332 (2018).

Norges Bank Investment Management. Investing with a Mandate. https://www.nbim.no/contentassets/cd563b586fe34ce2bfea30df4c0a75db/investing-with-a-mandate_government-pension-fund-global_web.pdf (2020).

OECD. OECD Sovereign Borrowing Outlook 2020 (2020).

Steitz, C. & Lewis, B. EU short of 118 billion euros in nuclear decommissioning funds - draft. Reuters (16 February 2016).

Fankhauser, S. & Hepburn, C. Designing carbon markets. Part I: carbon markets in time. Energy Policy 38, 4363–4370 (2010).

Murray, B., Newell, R. & Pizer, W. Balancing Cost and Emissions Certainty: An Allowance Reserve for Cap-and-Trade. NBER Working Paper 14258 http://www.nber.org/papers/w14258.pdf (National Bureau Of Economic Research, 2008).

Goulder, L. & Schein, A. Carbon Taxes vs. Cap and Trade: A Critical Review. NBER Working Paper 19338 http://www.nber.org/papers/w19338.pdf (National Bureau Of Economic Research, 2013).

Coffman, D. & Lockley, A. Carbon dioxide removal and the futures market. Environ. Res. Lett. 12, 015003 (2017).

Emmerling, J. et al. The role of the discount rate for emission pathways and negative emissions. Environ. Res. Lett. 14, 104008 (2019).

Hilaire, J. et al. Negative emissions and international climate goals—learning from and about mitigation scenarios. Clim. Change 157, 189–219 (2019).

Parson, E. A. & Buck, H. J. Large-scale carbon dioxide removal: the problem of phasedown. Glob. Environ. Polit. 20, 70–92 (2020).

Meinshausen, M. et al. The shared socio-economic pathway (SSP) greenhouse gas concentrations and their extensions to 2500. Geosci. Model Dev. 13, 3571–3605 (2020).

Workman, M., Dooley, K., Lomax, G., Maltby, J. & Darch, G. Decision making in contexts of deep uncertainty - an alternative approach for long-term climate policy. Environ. Sci. Policy 103, 77–84 (2020).

Butnar, I. et al. A deep dive into the modelling assumptions for biomass with carbon capture and storage (BECCS): a transparency exercise. Environ. Res. Lett. 15, 084008 (2020).

Gough, C. et al. Challenges to the use of BECCS as a keystone technology in pursuit of 1.5 °C. Glob. Sustain. 1, e5 (2018).

Friedlingstein, P. et al. Global carbon budget 2019. Earth Syst. Sci. Data 11, 1783–1838 (2019).

Capros, P. et al. Energy-system modelling of the EU strategy towards climate-neutrality. Energy Policy 134, 110960 (2019).

European Commission. A Clean Planet for All. A European Strategic Long-term Vision for a Prosperous, Modern, Competitive and Climate-neutral Economy (EC, 2018).

European Environment Agency. EEA Greenhouse Gas - Data Viewer. https://www.eea.europa.eu/data-and-maps/data/data-viewers/greenhouse-gases-viewer (EEA, 2021).

Geden, O. & Schenuit, F. Unconventional Mitigation: Carbon Dioxide Removal as a New Approach in EU Climate Policy. SWP Research Paper 2020/RP08 https://www.swp-berlin.org/10.18449/2020RP08/ (SWP, 2020).

Rickels, W., Proelß, A., Geden, O., Burhenne, J. & Fridahl, M. Integrating carbon dioxide removal into European emissions trading. Front. Clim. 3, 62 (2021).

Davis, S. J. et al. Net-zero emissions energy systems. Science 360, eaas9793 (2018).

Luderer, G. et al. Residual fossil CO2 emissions in 1.5–2 °C pathways. Nat. Clim. Change 8, 626–633 (2018).

Allen, M. R., Frame, D. J. & Mason, C. F. The case for mandatory sequestration. Nat. Geosci. 2, 813–814 (2009).

Friedmann, S. J. Engineered CO2 removal, climate restoration, and humility. Front. Clim. 1, 3 (2019).

Beuttler, C., Charles, L. & Wurzbacher, J. The role of direct air capture in mitigation of anthropogenic greenhouse gas emissions. Front. Clim. 1, 10 (2019).

Levihn, F., Linde, L., Gustafsson, K. & Dahlen, E. Introducing BECCS through HPC to the research agenda: the case of combined heat and power in Stockholm. Energy Rep. 5, 1381–1389 (2019).

The World Bank. Carbon Pricing Dashboard. https://carbonpricingdashboard.worldbank.org/ (accessed 11 March 2020).

Newman, A. L. & Posner, E. Putting the EU in its place: policy strategies and the global regulatory context. J. Eur. Public Policy 22, 1316–1335 (2015).

Santikarn, M., Li, L., Theuer, S. L. H. & Haug, C. A Guide to Linking Emissions Trading Systems (ICAP, 2018).

Riahi, K. et al. The Shared Socioeconomic Pathways and their energy, land use, and greenhouse gas emissions implications: an overview. Glob. Environ. Change 42, 153–168 (2017).

Richards, F. J. A flexible growth function for empirical use. J. Exp. Bot. 10, 290–301 (1959).

Fujimori, S. et al. SSP3: AIM implementation of Shared Socioeconomic Pathways. Glob. Environ. Change 42, 268–283 (2017).

Calvin, K. et al. The SSP4: a world of deepening inequality. Glob. Environ. Change 42, 284–296 (2017).

Strefler, J. et al. Between Scylla and Charybdis: delayed mitigation narrows the passage between large-scale CDR and high costs. Environ. Res. Lett. 13, 044015 (2018).

Marcucci, A., Kypreos, S. & Panos, E. The road to achieving the long-term Paris targets: energy transition and the role of direct air capture. Clim. Change 144, 181–193 (2017).

Sanz-Pérez, E. S., Murdock, C. R., Didas, S. A. & Jones, C. W. Direct capture of CO2 from ambient air. Chem. Rev. 116, 11840–11876 (2016).

Smith, P. et al. Biophysical and economic limits to negative CO2 emissions. Nat. Clim. Change 6, 42–50 (2016).

Clarke, L., Weyant, J. & Birky, A. On the sources of technological change: assessing the evidence. Energy Econ. 28, 579–595 (2006).

Drud, A. S. CONOPT—a large-scale GRG code. ORSA J. Comput. 6, 207–216 (1994).

Acknowledgements

We acknowledge financial support from the European Research Council Synergy grant ERC-SyG-2013-610028 IMBALANCE-P as well as from the FWF grant P-31796 Medium Complexity Earth System Risk Management (ERM) and support from the HSE University Basic Research Program for A.B.

Author information

Authors and Affiliations

Contributions

M.O., F.W., M.T. and J.B. have contributed equally to identifying the knowledge gaps and main ideas of this Article, as well as sharpening the field of interest. J.B. acted as lead author and was primarily involved in formalizing and quantifying the ideas of the Article, as well as in drafting the main paper and developing the analytical and numerical methods. J.W.H. and M.O. supervised the development of the paper from the first draft throughout the review process. J.W.H., O.G., M.A., F.W. and M.T. contributed to the framing, conception and design of the work, as well as to the interpretation of the results. A.B. provided quality control of methods and the presentation of the results and contributed the mathematical proof of the equations derived in the Methods. O.G. contributed by markedly improving the policy relevance of the Article (for instance, by developing the EU implementation scenario). All authors were equally involved in the revision process and have approved the submitted version of the Article.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Peer review information Nature thanks David Stainforth and the other, anonymous, reviewer(s) for their contribution to the peer review of this work.

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Extended data figures and tables

Extended Data Fig. 1 Schematic supply of emission allowances and CROs at a fixed point in time.

The supply of allowances is completely inelastic (emission cap), whereas the supply elasticity of CROs is determined by discounted future abatement costs, which increase as the demand for CROs increases, as well as interest costs, which can be controlled by managing authorities and financial institutions (dashed blue CRO supply curves). If CROs are traded on a market, they clear at the same price as allowances and thereby reduce the price of allowances. The larger the elasticity of the CRO supply curve, the lower the potential for price volatility (red arrows), as—for example—induced by a demand shock (dashed orange line). The sum of allowances and CROs issued equals net emissions. Abated emissions equal the difference between baseline emissions (green) and net emissions and consist of emission reductions and/or carbon removal.

Extended Data Fig. 2 Abatement costs and carbon debt of 1.5 °C (RCP 1.9) scenarios for six different MACCs of DACS and interest rates on carbon debt rd = 0 and rd = 0.08.

A definition of D is provided in the Methods. Abatement costs are discounted and expressed as a percentage of the GDP. Abatement costs are exclusive of interest costs. For each rate rd, 78 scenarios (13 scenarios as for the RCP 2.6 analysis times 6 DACS parameters) are grouped by DACS costs (low to high, that is, ‘LoCost’, ‘MedCost’ and ‘HiCost’) and DACS capacity limits (10% and 30% of baseline emissions, that is, ‘LoCap’ and ‘HiCap’). a, b, Median abatement costs as a function of median carbon debt D for rd = 0 (a) and rd = 0.08 (b). For rd = 0, we observe an inverse relation between the level of carbon debt and abatement costs; and the capacity limit is a stronger determinant of abatement costs than DACS deployment costs. This ‘discounting effect’ is reversed when rd = 0.08 and high levels of \(D\) are penalized. In this case, lower abatement costs are realized by lower carbon debt (and vice versa). For both rates rd ‘LoCost_HiCap’ DACS scenarios are characterized by the lowest abatement costs, however, at very different levels of D. When interest is invoked, DACS deployments costs become an increasingly important determinant of total abatement costs. c, d, Distribution of total carbon debt D (c) and abatement costs (d) for the median values shown in a, b. Boxes indicate the 25–75% interquartile ranges around medians (bold solid line), whiskers indicate minimum to maximum ranges, black dots mark outliers.

Extended Data Fig. 3 The 1.5 °C (RCP 1.9) pathways under a conventional ETS or a CRO-ETS.

a, b, A conventional ETS is used. c, d, A CRO-ETS is used. The underlying set of scenarios was filtered for those scenarios that achieved at least a 5% reduction in total carbon debt compared with their baselines (see Methods). a, c, Geometric median net emissions (solid line) and gross emissions from FFI, BECCS, LUC and DACS. Net emissions from a are also displayed in c (dashed line) and vice versa. The total carbon debt D is shown as a box-and-whiskers plot. Boxes indicate the 25–75% interquartile range around the median values (bold line), whiskers indicate minimum to maximum ranges, points mark the outliers. b, d, Annual mitigation costs as a percentage of GDP, including the share of average abatement costs attributed to emission reductions (ABM), to the compensation of residual emissions by CDR (RES) and to net-negative emissions (NNE) as well as expenditures for allowances (ETS) and interest costs (INT). Total mitigation costs (that is, ABM + RES + NNE + ETS + INT) from d are also displayed in b (dashed line) and vice versa. Box-and-whiskers plots show the total discounted abatement costs (that is, ABM + RES + NNE) as a percentage of GDP, the number above the chart indicates out-of-range outliers. Pie charts in d summarize the properties of the underlying set of scenarios (see Methods). The distribution of rd in CRO-ETS scenarios is depicted in c.

Extended Data Fig. 4 The 1.5 °C (RCP 1.9) pathways under a conventional ETS or a CRO-ETS.

a, b, A conventional ETS is used. c, d, A CRO-ETS is used. The underlying set of scenarios was filtered for those scenarios that achieve at least a 15% reduction in total carbon debt compared with their baselines (see Methods). a, c, Geometric median net emissions (solid line) and gross emissions from FFI, BECCS, LUC and DACS. Net emissions from a are also displayed in c (dashed line) and vice versa. The total carbon debt D is shown as a box-and-whiskers plot. Boxes indicate the 25–75% interquartile range around the median values (bold line), whiskers indicate minimum to maximum ranges, points mark the outliers. b, d, Annual mitigation costs as a percentage of GDP, including the share of average abatement costs attributed to emission reductions (ABM), to the compensation of residual emissions by CDR (RES) and to net-negative emissions (NNE) as well as expenditures for allowances (ETS) and interest costs (INT). Total mitigation costs (that is, ABM + RES + NNE + ETS + INT) from d are also displayed in b (dashed line) and vice versa. Box-and-whiskers plots show the total discounted abatement costs (that is, ABM + RES + NNE) as a percentage of GDP, the number above the chart indicates out-of-range outliers. Pie charts in d summarize the properties of the underlying set of scenarios (see Methods). The distribution of rd in CRO-ETS scenarios is depicted in c.

Extended Data Fig. 5 The 1.5 °C (RCP1.9) pathways under a conventional ETS or a CRO-ETS.

a, b, A conventional ETS is used. c, d, A CRO-ETS is used. The underlying set of scenarios was filtered for those scenarios that achieve at least a 45% reduction in total carbon debt compared with their baselines (see Methods). a, c, Geometric median net emissions (solid line) and gross emissions from FFI, BECCS, LUC and DACS. Net emissions from a are also displayed in c (dashed line) and vice versa. The total carbon debt D is shown as a box-and-whiskers plot. Boxes indicate the 25–75% interquartile range around the median values (bold line), whiskers indicate minimum to maximum ranges, points mark the outliers. b, d, Annual mitigation costs as a percentage of GDP, including the share of average abatement costs attributed to emission reductions (ABM), to the compensation of residual emissions by CDR (RES) and to net-negative emissions (NNE) as well as expenditures for allowances (ETS) and interest costs (INT). Total mitigation costs (that is, ABM + RES + NNE + ETS + INT) from d are also displayed in b (dashed line) and vice versa. Box-and-whiskers plots show the total discounted abatement costs (that is, ABM + RES + NNE) as a percentage of GDP, the number above the chart indicates out-of-range outliers. Pie charts in d summarize the properties of the underlying set of scenarios (see Methods). The distribution of rd in CRO-ETS scenarios is depicted in c.

Extended Data Fig. 6 The abatement costs and interest costs of the 1.5 °C (RCP 1.9) scenarios as function of the percentage of carbon debt reduction compared with the baseline scenario.

a, b, The abatement costs (a) and interest costs (b) of the 1.5 °C (RCP 1.9) scenarios is compared with the baseline scenario (in which rd = 0) for all 468 RCP 1.9 scenarios, grouped by the carbon debt interest rate (rd) and the cost and capacity parameters of DACS. DACS cost parameters range from low to high (that is, LoCost, MedCost and HiCost); capacity limits include 10% and 30% of baseline emissions (that is, LoCap and HiCap). a, Total discounted abatement costs excluding interest costs (that is, ABM + RES + NNE as in Fig. 4 and Extended Data Figs. 3–5). b, Total discounted interest costs (that is, INT as in Fig. 4 and Extended Data Figs. 3–5).

Extended Data Fig. 7 Schematic overview and illustrative repayment terms of RCP 1.9 scenarios.

a, Schematic overview of the CRO-ETS. The physical overshoot of a cumulative emission target, potentially amplified by outgassing of CO2 from the Earth’s stocks, subsequently necessitates carbon sequestration for returning to the target. For accrued carbon debt, CROs are issued, obliging emitters to compensate for a tonne of CO2 before a specified maturity—for example, by physically removing atmospheric CO2 or by acquiring an adequate quantity of allowances in the future. Similar to financial debt, CROs require debtors to pay interest to hedge physical and financial risks associated with carbon debt. Three earmarked financial resources are created under a CRO-ETS. (1) Revenues from auctioning allowances are recycled into the economy to the benefit of society. (2) Revenues from interest on carbon debt are targeted at managing risks—that is, by enabling additional carbon sequestration when Earth system risks (for example, permafrost thaw) and financial risks (for example, default risk of debtors) materialize. (3) Funds for repayment of the carbon debt are individually managed by debtors. b–e, The repayment term function TR(t) for the scenarios illustrated in Extended Data Fig. 3 (b), Extended Data Fig. 4 (c), Fig. 4 (d) and Extended Data Fig. 5 (e). Interest on carbon debt rd reflects the mean values of the distributions shown in Fig. 4c and Extended Data Figs. 3c, 4c, 5c. Bold lines indicate geometric median repayment terms derived from the scenarios presented in Fig. 4 and Extended Data Figs. 3–5. TR(t) maps the timing of carbon debt accrual to the time of its compensation (see Methods). For instance, in c, the carbon debt accrued in 2020 is compensated approximately 40 years later in scenarios with interest (rd = 0.058, yellow lines) and roughly 50 years later in scenarios for which rd = 0 (turquoise lines). As rd is increased, the net-zero year moves closer, indicating that carbon debt in 2020 is compensated earlier, whereas, in general, TR extends over longer periods. The increasingly flat net-negative emissions profile (when rd is increased) suggests that TR increases more rapidly in the beginning than when rd = 0 because the cumulative carbon debt at t grows faster than the cumulative net-negative emissions at t + TR(t). The point of inflection indicates where cumulative carbon debt begins to grow more slowly than cumulative net-negative emissions that compensate for that carbon debt. For instance, in d (yellow line), the cumulative carbon debt from 2030 onwards grows at a slower pace than the cumulative net-negative emissions approximately 63 years later.

Extended Data Fig. 8 MACCs.

a, The functional form of MACs,\(\,{\rm{MAC}}(a)=b[\tfrac{1}{\nu }((\tfrac{L-A}{a-A}{)}^{\nu }-1){]}^{c}\), is derived from the inverse generalized logistic function. It is relatively flexible with respect to replicating a wide range of MACCs derived from the SSP database. Here A = 1 and L = 0 are upper and lower asymptotes along the y axis. Notably, MAC(a = A) = ∞; therefore, A is a maximum abatement rate built into the MAC curve. b defines the y position of the pivot point. The x position of the pivot point is determined by ν and for ν = 1 it is exactly the middle of the interval (L, A), (L + A)/2. c defines the level of rotation with respect to the pivot point. b, Six stylized MACCs for DACS covering the literature range for costs from US$20 to US$1,000 per t CO2 (orange area). Low-cost MACCs (dotted lines) start at approximately US$50 per t CO2 and reach US$1,000 per t CO2 at abatement rates aDACS = 0.07 (low capacity, blue line) and aDACS = 0.27 (high capacity, red line) equivalent to approximately 3 and 12 Gt CO2 yr−1 at current emission levels, respectively. Medium-cost MACCs (dashed lines) start at US$250 per t CO2 and reach US$1,000 t CO2 at aDACS = 0.05 (low capacity, blue line) and aDACS = 0.22 (high capacity, red line), that is, roughly 2 and 10 Gt CO2 yr−1 at current emission levels, respectively. High-cost MACCs (solid lines) start at approximately US$500 per t CO2 and reach US$1,000 per t CO2 at aDACS = 0.03 (low capacity, blue line) and aDACS = 0.12 (high capacity, red line), amounting to roughly 1 and 5 Gt CO2 yr−1 at current emission levels, respectively.

Supplementary information

Supplementary Information

This file contains a graphical representation of all 2 °C (RCP2.6) emission pathways discussed in the Results (specifically in Figure 3).

Supplementary Data

This file contains the data of all 2 °C (RCP2.6) pathways discussed in the Results as an Excel sheet.

Supplementary Information

SI1.3 contains a graphical representation of all 1.5 °C (RCP1.9) emission pathways discussed in the Results (specifically in Figure 4 and Extended Data Figures 7–9).

Supplementary Data

This file contains the data of all 1.5 °C (RCP1.9) pathways discussed in the Results as an Excel sheet.

Supplementary Information

This file contains a graphical representation of the marginal abatement cost (MAC) curves used in the numerical model of this study. The parameters of the MAC curves can be retrieved with the R package provided for using the numerical model.

Supplementary Information

This file illustrates carbon prices from the SSP scenarios compared to carbon prices and MAC from the numerical model of this study.

Supplementary Information

This file illustrates consumption loss and GDP loss from the SSP scenarios compared to abatement costs from the numerical model of this study.

Supplementary Information

This file illustrates net emissions from the SSP scenarios compared to net emissions from the numerical model of this study.

Supplementary Information

This file contains the analytical methods necessary to derive equation [16] in the Methods section.

Rights and permissions

About this article

Cite this article

Bednar, J., Obersteiner, M., Baklanov, A. et al. Operationalizing the net-negative carbon economy. Nature 596, 377–383 (2021). https://doi.org/10.1038/s41586-021-03723-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41586-021-03723-9

This article is cited by

-

Inequality repercussions of financing negative emissions

Nature Climate Change (2024)

-

How rising temperatures affect electricity consumption and economic development in Mexico

Environment, Development and Sustainability (2024)

-

Realistic fault detection of li-ion battery via dynamical deep learning

Nature Communications (2023)

-

The social value of offsets

Nature (2023)

-

Modeling the city-level synergistic effect of low-carbon economic development in China’s Yangtze River Delta

Environmental Science and Pollution Research (2023)

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.