Abstract

On the path to climate neutrality, global production locations and trade patterns of basic materials might change due to the heterogeneous availability of renewable electricity. Here we estimate the ‘renewables pull’, that is, the energy-cost savings, for varying depths of relocation for three key tradable energy-intensive industrial commodities: steel, urea and ethylene. For an electricity-price difference of €40 MWh−1, we find respective relocation savings of 18%, 32% and 38%, which might, despite soft factors in the private sector, lead to green relocation. Conserving today’s production patterns by shipping hydrogen is substantially costlier, whereas trading intermediate products could save costs while keeping substantial value creation in renewable-scarce importing regions. In renewable-scarce regions, a societal debate on macroeconomic, industrial and geopolitical implications is needed, potentially resulting in selective policies of green-relocation protection.

Similar content being viewed by others

Main

A promising option for the climate-change mitigation of the production of energy-intensive basic materials, such as steel and chemicals, is a switch to renewable electricity (RE) and green hydrogen (H2)1,2. Owing to varying RE availability and cost across the globe, the transition to net-zero greenhouse-gas (GHG) emissions might result in a relocation of industrial production and hence a shift of trade patterns for the respective emerging green value chains (Fig. 1).

Defossilizing the value chains of energy-intensive basic materials necessitates the emergence of new green value chains that rely on low-carbon feedstocks produced from RE. The displayed value chains start with water electrolysis and, in the cases of urea and ethylene, with DAC, which yields the basic building blocks green H2 and atmospheric CO2. Combining these two together (with iron and nitrogen) yields DRI, NH3 and basic carbonaceous feedstocks, which we refer to as intermediates. These are finally converted into (semi)finished products which are widely used in industry, such as semifinished steel, cast iron, fertilizer and HVCs. While the share of energy in the production cost decreases along the value chain, the long-distance transportability of intermediate products increases.

Energy prices are a major factor for production costs of basic materials3 and will probably continue to be so for future green value chains. While trade with fossils has so far dampened effects of the heterogeneous availability of primary energy, long-distance transport of electricity and H2 is much costlier. Thus, energy-cost savings resulting from substantial geographical differences in RE prices will create an incentive (so-called ‘renewables pull’4,5), which may lead to a relocation of low-carbon production (so-called ‘green relocation’).

Prominent candidates for RE-scarce importers are the European Union (EU), South Korea or Japan, which, respectively, import 55% (ref. 6), 84% (ref. 7) and 96% (ref. 8) of their current energy demand. Producing sufficient RE to replace these mostly fossil imports will be challenging, as land and RE potentials are limited. While these countries have declared ambitious H2 import strategies, their openness about basic-material imports is unclear, especially given current global trends towards protecting critical supply chains. This work aims to inform both strategies: those seeking to protect against green relocation and those seeking to exploit energy-cost savings through relocation.

Obvious candidates for RE-rich exporters include industrialized countries, such as Australia, the United States and Canada but also countries located in Africa, the Middle East and Latin America, most of which are classified as low-income economies. Intraregional effects are also conceivable, such as within the EU (for example, Germany to Spain) or the United States (for example, north to south). While the renewables pull is a region-specific effect, our work presents a generic framework based on electricity-price assumptions.

Previous works include case studies of steel exports from Australia9 and South Africa10, searches for globally optimal steel-production sites11,12, as well as studies of global trade with ammonia (NH3) (refs. 13,14), e-fuels and e-chemicals15, which all conclude to varying extent that exporting basic materials from regions with high RE availability can be desirable due to improved cost-competitiveness with fossils and with alternative green production sites. Others5 analysed announcements from the private sector, showcasing how the renewables pull influences investment decisions today (Supplementary Table 5).

While many public and academic debates rightfully focus on the green-versus-fossil competitiveness2,16,17,18, our assessment looks at the understudied green-versus-green regional competitiveness for basic materials. Also note that there exist several other basic materials not considered in this work, such as aluminium, copper, cement, glass, paper or silicon. While many aspects discussed here also apply to these products, their green value chains do not rely on H2, contain fewer intermediate steps and are responsible for a smaller share of industrial GHG emissions.

Here, we present quantitative insights into the renewables pull by estimating the energy-cost savings and competing effects (transport and financing penalties) for the green value chains of three primary basic materials: steel, urea and ethylene. We conduct our techno-economic analysis for varying depth of relocation and thereby study the role of individual production steps in these value chains. This approach allows comparisons of competing options for splitting value chains between the importer and exporter side across industrial subsectors. Moreover, we integrate the renewables pull into a holistic perspective that includes difficult-to-quantify private factors, societal implications and optional regulatory intervention. Finally, we apply our generic approach to a case study of energy-intensive imports to Germany and estimate potential ‘green-relocation protection’, which we define as the public subsidies required to avoid relocation.

A broader picture of the renewables pull and green relocation

The effect we ultimately aim to study is green relocation, which we define as the relocation of industrial production owing to the renewables pull (that is, the incentive to relocate due to energy-cost savings). The renewables pull is only one of many factors determining private investment decisions, which jointly may or may not lead to green relocation. We therefore start our work by embedding the renewables pull into a broader conceptual framework, which will allow for a structured analysis, before we present quantitative estimates in the next two sections.

We arrange competing factors that influence green relocation in three layers corresponding to different perspectives (Fig. 2): (1) a private investors’ perspective, (2) a policy-makers’ perspective and (3) a societal perspective. As a result, our analysis is structured around the following three questions. First, when considering companies in free markets, will the renewables pull and other factors from the private sector alone result in green relocation? Second, are there existing, announced or conceivable forms of policy-making that could influence private investment decisions in addition to factors from the private sector? And third, what future policy-making can be expected to arise from conflicting societal goals and how these are weighed up by societies and policy-makers?

Investments into new green production facilities can occur in two ways. Option 1: plants are constructed in RE-scarce regions, where (grey) industrial production is located today, hence reinforcing the status quo (left circle). Option 2: plants are constructed in new RE-rich regions, where no or little industrial production takes place today, hence resulting in green relocation (right circle). The construction of such facilities is determined by private investment decisions, which are influenced by several incentivizing and inhibiting soft and hard factors. The renewables pull is only one of these factors and we estimate it quantitatively together with transport and financing penalties. Green relocation also comes with societal risks and opportunities, which however only translate into factors influencing private investment decisions via regulatory intervention.

First, the occurrence of green relocation is determined by investment decisions of the private sector, which are influenced by incentivizing or inhibiting factors. These factors can broadly be split up into hard factors (those easy to express as changes in the production cost) and soft factors (those that are not). Hard factors that our generic study is able to capture can be summarized in the following simple relation

where we define the term ‘relocation savings’ to refer to the overall production-cost savings resulting from production relocation. Financing penalty here refers to higher financing cost due to higher weighted average cost of capital (WACC) in RE-rich exporting countries.

Soft factors may also influence production cost, increase consumers’ readiness-to-pay for short and reliable supply chains, otherwise affect private revenues or strictly prohibit production. Such soft factors may be inhibiting, incentivizing or with undecided/case-specific effect for green relocation. Inhibiting factors include proximity to customers (for example, benefits of short supply chains, just-in-time production, lean manufacturing, close customer relationships and reliability of supply), proximity to other producers (for example, benefits of heat integration, process integration, coproduction, joint industrial infrastructure and economies of scope), infrastructure availability in established locations of industrial production (for example, roads, ports, electricity grids and water supply), general know-how (industry expertise), political and economic stability of countries and certification (which can be easier to obtain when producing in the country where products are demanded). Incentivizing factors include the availability of space for construction (often ample in RE-rich regions), the complexity of plant integration (challenging in complex arrangements of existing industrial sites), reduced labour cost and proximity to non-energy resources (for example, iron ore). Factors that are undecided or case specific include the market structure and resulting prices of future green products, the complexity of planning and approval procedures and the availability of skilled labour.

In summary, conserving current production patterns allows using many advantages of established production sites in RE-scarce regions, which can only partly be compensated for by the absence of obstructing brownfield integration and potentially lower wages. Moreover, revenues will ultimately depend on future supply and demand curves and hence market prices of energy carriers, feedstocks, intermediates and products, which are all uncertain. Whether soft factors will suffice to compensate the renewables pull will be highly case specific and constitute its own subject of research. (See Supplementary Table 1 for a comprehensive list of private-sector factors.)

Second in our list of perspectives to account for is the one of policy-makers. Many of today’s existing or announced policies targeting energy-intensive industries will influence private investment decisions connected to green relocation, as discussed in more detail in the ʻDiscussion and conclusionsʼ. Moreover, policy-makers could try to introduce more regulatory interventions specifically targeted at steering green relocation, such as subsidies (for example, a potential green-relocation protection scheme) or trade tariffs.

Third, whether such interventions are necessary or how these should be designed will depend on the perception of risks and opportunities of green relocation in the respective countries. On the RE-scarce side, opportunities are low-cost imports of basic materials, reduced system and transformation cost, lower domestic energy prices and an accelerated transition to net-zero emissions. Risks include reduced security of supply and geopolitical dependencies, a potential deferment of climate mitigation and losses of employment and productivity. The last, that is value creation relocated, is the greatest opportunity of RE-rich regions alongside energy-system development, while risks could be introducing neocolonial structures and using RE potentials only for exports instead of domestic climate mitigation (so-called resource shuffling). (See Supplementary Table 2 for a comprehensive list of risks and opportunities.) All risks and opportunities need to be assessed and weighed up by affected countries, potentially resulting in new policies aiming to steer green relocation in one way or the other.

Analysing each layer and answering each question will be the topic of future research and societal debate, especially across regional cases and industrial sectors. In the next section, we start by addressing the first question (what the private sector would decide in the absence of policy intervention) through a generic quantification of the renewables pull.

Quantifying the renewables pull for key energy-intensive value chains

We estimate the renewables pull for the emerging green value chains of three commodities, which are chosen to be broadly representative of key existing industrial value chains (compare Fig. 1):

-

(1)

Hot rolled coil (HRC)—the most traded semifinished steel product at a global market share of 18% in 202219

-

(2)

Urea—an intermediate product of the chemical industry and a key component of nitrogen fertilizers with ~50% global market share in 201820

-

(3)

Ethylene—a precursor to polymer plastics (polyethylene and polyethylene-terephthalate)

All are produced using green H2 and their value chains consist of three main processing steps, resulting in four possible import cases of varying degrees of relocation (Fig. 3). Notably, today’s value chains in resource-constrained countries best compare with case 1, given that these value chains rely on imports of fossil primary energy (coal, oil and gas). Therefore, the base case may even be considered a case of onshoring, since fossil imports are replaced by domestic RE generation. When discussing the role of green relocation, we mainly refer to the industrial processes part of the studied value chains and not their energy supply.

a–c, All studied value chains start with producing green hydrogen (H2) via water electrolysis. They use this H2 as a feedstock to produce intermediate products: DRI from direct reduction (DR) of iron ore (a), NH3 from Haber–Bosch synthesis with nitrogen from an air-separation unit (HB-ASU) (b) and MeOH from synthesis of H2 with CO2 from DAC (c). They convert these intermediate products into (semi)finished industrial products: semifinished steel from an EAF (a), urea from the synthesis of NH3 and CO2 (b) and ethylene from an MtO process (c). Trade may occur in between these three production steps, resulting in four import cases (base case and cases 1–3).

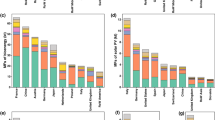

We estimate the production cost for these commodities for each import case, with results presented in Figs. 4 and 5 and Table 1, and with the assumed electricity prices also listed in Table 1. We distinguish case 1 into case 1A, showing high H2 transportation cost of €50 MWh−1 and case 1B, showing moderate cost of €15 MWh−1, corresponding to, respectively, shipping-based and pipeline-based imports.

a–f, Low-carbon production of steel (a,d), urea (b,e) and ethylene (c,f). The top row shows the relocation savings expressed as total cost of production relative to the base case (a–c), whereas the bottom row shows competition between energy-cost savings on the lower and other cost changes on the upper axis (d–f). Results are reported for different electricity-price differences (€20, €40 and €70 MWh−1) according to Table 1. a–c, Production cost relative to base case for the import cases from Fig. 3 (including subcases A/B for case 1). d–f, Comparison between energy-cost savings on the lower axis and transport and financing penalties on the upper axis, with the heatmap showing the resulting relocation savings relative to the base case. Case 1A is shown separately from the other cases and not included in the corridor of values on the top row to highlight its saliency and contrast it with the otherwise monotonous decrease of production cost with increasing depth of relocation. Markers for the same case represent different electricity-price cases and the shaded band on the top row is a simple spline interpolation serving as visual support.

Naturally, the magnitude of the renewables pull is most strongly influenced by regional differences in electricity prices, which are inherently uncertain, complex and dependent on regional context. Here, we aim to provide a generic framework and thus vary electricity-price differences between €20 and €70 MWh−1 without assuming specific regional cases. While levelized cost of electricity (LCOE) estimates indicate only price differences of €20 MWh−1 between RE-rich and RE-scarce regions, we identify five more layers of complexity that can drive differences up to €40–70 MWh−1: marginal renewables costs, temporal price profiles, the role of electricity grids, barriers for high renewables deployment and general infrastructure availability (see section on future electricity prices in Supplementary Information for an in-depth discussion).

Technology parameters are chosen to represent the year 2040, hence including learning effects resulting from wide deployment of technologies with a low readiness level today. We choose a relocation-induced increase of the WACC from 5% to 8%, which affects results only lightly (Fig. 5). Note that we choose optimistic assumptions for the energy demand of direct air capture (DAC), for which we present sensitivity analysis below.

a–c, Low-carbon production of steel (a), urea (b) and ethylene (c). Results are again shown for the four import cases illustrated in Fig. 3 and assume an electricity-price difference of €40 MWh−1 (medium-pull case from Table 1). The levelized costs visualize how the relocation savings in the steel value chain are smaller in comparison to the other value chains as a result of the high feedstock cost. Moreover, annualized CAPEX assumes a higher WACC of 8% in the RE-rich region compared to 5% in the RE-scarce region over a lifetime of 18 years, resulting in higher levelized capital cost, yet this effect appears to be small compared to the renewables pull. For a detailed composition, we encourage readers to view this figure in the online webapp or download the accompanying spreadsheet file (see ʻData availabilityʼ).

The full relocation savings (from base case to case 3) spread across a broad range of 9–60% and vary strongly, depending on assumed electricity-price differences and between commodities (Table 1). Savings are lower for steel, where raw-material costs (iron ore and so on) are high. An electricity-price difference of €40 MWh−1 (medium-pull case) yields substantial relocation savings of 18%, 32% and 38% for, respectively, steel, urea and ethylene, whereas savings reach up to 32%, 55% and 60% for €70 MWh−1 (strong-pull case).

By splitting up the value chains into three steps and considering the resulting four import cases, we can demonstrate how production costs decrease with every step relocated (except case 1A and electricity-price difference ≤€35 MWh−1) and which share of savings occurs with the relocation of each step. A large share of energy-cost savings is associated with relocating electrolysis, the most energy-intensive process. Yet, in case 1A the energy-cost savings translate into only minor relocation savings of, respectively, 1%, 2% and 2% (medium-pull case), due to high transport costs of different H2 shipping technologies. Lower H2 transport cost in case 1B substantially increase the gained relocation savings to 9%, 19% and 19%. Moreover, resorting to imports of intermediates (directly reduced iron (DRI), NH3 and methanol (MeOH)) would cover almost all relocation savings at 13%, 25% and 37%. Therefore, there is comparably little cost incentive for further relocation beyond import of intermediates across the studied commodities, which is because the energy demand of the third step is comparably low and transport costs for (semi)finished products are similar or even higher than for intermediates.

Sensitivity analysis shows that our results are mostly robust, yet relocation savings shrink notably for drastic increases in the WACC on the RE-rich exporter side, in the overall CAPEX or in specific H2 transport cost (Extended Data Fig. 1).

Before applying these results to a specific case study and concluding with interpretation and policy recommendations, it is important to once more understand the meaning of these estimates, appreciate their limitations and connect them to the wider framework from the previous section. It should be noted that we have so far only estimated quantifiable hard factors and neglected difficult-to-quantify soft factors, such as the readiness-to-pay for short and reliable supply chains, various advantages of reusing established production sites and the role of market prices. In summary, our estimations are only able to provide insights based on technologies and RE prices, yet analyses of soft factors and political implications remain an important subject of further research.

Estimating potential green-relocation protection for Germany

We proceed by applying our generic framework to a specific case study on future German imports of H2 and basic materials, which will allow us to estimate potential policy cost of regulatory intervention aiming to prevent green relocation. Specifically, we estimate the total potential relocation savings for the annual German demand of the considered products (steel, urea and ethylene), which may also be interpreted as the annual subsidy required to protect these industrial subsectors against green relocation. As argued before, there are limitations to our approach and the actual subsidy needed could deviate from our estimations either way, depending on the magnitude of the soft factors. Yet, our estimates are helpful for gaining a first impression of the societal impact of green relocation and implications for regulatory intervention.

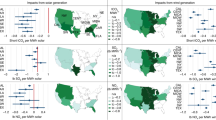

We assume two scenarios of varying degree of green relocation, corresponding to policy interventions following competing strategies (Table 2). Scenario 1 (focus H2) assumes basic materials to be produced domestically with a mix of domestic H2 (base case) and imported H2 (via pipeline and ship; cases 1A/B) at an equal share. Scenario 2 (focus intermediates) assumes full domestic production (base case) and shipping-based H2 imports (case 1A) to be reduced to 15% each and pipeline-based H2 (case 1B) imports to be replaced by 50% imported intermediates (case 2) and 20% imported (semi)finished products (case 3). This means we can take the perspective of the German government aiming to (1) conserve industrial production patterns as today (while reducing the share of imported energy through domestic RE expansion) or (2) establish a mixed solution, in which security of supply is realized by retaining a third of industrial production, while for the remaining share relying on imports of intermediates from global markets (and/or selected exporters). Potential exporting countries listed in Table 2 are selected on the basis of RE potentials, existing fossil production, green project announcements and availability of raw materials.

Projections for the German basic-material demand in 2040 are taken from two studies on German industry decarbonization21,22. Projections for NH3 demand of ~3 Mt would translate into ~5 Mt of urea demand if all NH3 were to be converted into urea only. For reasons of simplicity, we assume a urea demand of 4 Mt to represent the full fertilizer sector and other industrial NH3 uses (excluding potential future applications as a fuel). For steel, the share of retained industry production in scenario 2 corresponds roughly to the steel-production capacity which private companies and policy-makers envisage to transform until around 2030 (based on instruments such as EU Important Projects of Common European Interest (IPCEIs) and Carbon Contracts for Differences (CCfDs)).

Depending on the strength of the renewables pull (which in turns depends on electricity-price differences), the total potential annual relocation savings (compared to direct imports of the final good) and hence the required green-relocation protection span a range of €6–18 billion yr−1 for scenario 1 and €3–9 billion yr−1 for scenario 2 (Fig. 6 and Supplementary Fig. 4). These numbers can be interpreted as an indication for subsidies or other policy costs which Germany would have to pay as a green-relocation protection to prevent private companies from relocating the production of the considered commodities. It is worth comparing these subsidies to the planned spending from the provisional German federal budget for 202323 and the federal Climate and Transition Fund24, which indicates that such subsidies would result in a substantial additional expense.

a–c, Annual volumes for a potential green-relocation scheme for two scenarios defined in Table 2: scenario 1 focussing on imported and domestically produced H2 and scenario 2 focussing on importing intermediate industrial products. The presented numbers are derived on the basis of our generic framework for production-cost estimates outlined in the previous section. These assume the three electricity-price differences cases, weak (a), medium (b) and strong pull (c), as defined in Table 1. d, Comparison of these numbers against planned federal fiscal spending, represented by the regular budgets of selected federal ministries in the provisional German budget for 202323 and the two main special budgets from the federal Climate and Transition Fund24.

Discussion and conclusions

Access to cheap energy has always shaped the locations of energy-intensive industries. On the path to climate neutrality, the heterogeneous distribution of renewable energy resources might change global patterns of industrial production and trade of basic materials. More specifically, relocating low-carbon industrial production away from RE-scarce and towards RE-rich regions would result in energy-cost savings which provide an incentive (so-called renewables pull4,5) for such relocation (so-called green relocation).

Here, we find substantial overall relocation savings of roughly 18%, 32% and 38% for steel, urea and ethylene for a full relocation of the considered production steps. These estimates assume an electricity-price difference of €40 MWh−1 in 2040, which we find conceivable based on estimations of renewable LCOEs, infrastructure cost and barriers arising for high deployment rates for renewables in RE-scarce regions (with details in a section on future electricity prices in Supplementary Information), although we also vary this crucial assumption across €20–70 MWh−1 in our analysis.

Soft factors counteracting the renewables pull will probably only have a dampening effect, given the magnitude of energy-cost savings derived here and thus will be insufficient to prevent green relocation entirely. However, further sector-specific research is needed to understand locational factors, such as proximity to customers, proximity to other producers, infrastructure, general know-how, skilled labour, certification and approval schemes and market prices.

By analysing cases of varying ‘depth’ of relocation, we assess different options of splitting value chains between the importer and exporter side and estimate associated relocation savings. This yields two main conclusions as follows. First, although locating only electrolysis (the first step in each considered value chain) in RE-rich regions and importing green H2 could shift a large share of energy demand to where it is cheap, the resulting overall relocation savings are small for shipping-based imports (1–2%) because of high H2 transportation cost. Therefore, trying to conserve production patterns through H2 imports is a potentially expensive and risky strategy. Importing H2 via pipeline instead could weaken the renewables pull, yet they may be infeasible (Japan and South Korea) or take time to construct (Europe). These findings challenge the H2 import strategies of some RE-scarce regions, in which basic-material production is considered a domestic no-regret H2 application and hence a key component of future H2 demand. Second, importing intermediate products (DRI, NH3 and MeOH) effectively harnesses a large share of the relocation savings (13%, 25% and 37%), while potentially retaining a substantial share of value creation. Since these intermediate products are rather homogeneous goods, security of supply in RE-scarce regions could be established via diverse global markets. This suggests the import of these intermediate goods as a ‘sweet spot’ of relocation.

Policy-makers across the globe are tasked with shaping the transition of their basic-material industries against the backdrop of geopolitical tensions, protectionist trends and—as we establish here—decreasing competitiveness of energy-intensive industries in RE-scarce countries due to the renewables pull. However, policy-makers have thus far not addressed the renewables pull but instead focussed on a range of other goals. Specifically, existing policies and strategies aim to do the following. (1) Stimulate domestic industry decarbonization through investments into new infrastructure (especially H2 and CO2) and low-carbon industrial processes, however without considering the future competitiveness of these industries. Examples are the IPCEIs on hydrogen and industry, the Net-Zero Industry Act in the EU, the European Hydrogen Backbone project or the German CCfDs. (2) Secure supply chains of green technologies, however focussing only on critical minerals (such as lithium and cobalt) or technological supply chains (such as mineral refining, manufacturing, batteries and electrolysers) and not on basic materials. Examples are the Critical Raw Materials Act in the EU or the Inflation Reduction Act in the United States. (3) Compensate for high energy prices during the transition but without considering the need for sustained long-term subsidies to counteract the renewables pull (so-called green-relocation protection). An example is the recently proposed German industrial electricity-price subsidy, which is, however, only considered as a transitional measure. (4) Foster global imports of H2 and derivatives but without considering the trade of energy-intensive basic materials. Examples are the H2 import strategies announced by Japan in 2020 and by the EU in 2022, including respective H2 import targets for 2030 of 10 TWh (ref. 25) and 333 TWh (ref. 26) (assuming lower heating value (LHV)), as well as the German H2Global project27.

This mix of policies and strategies represents a set of explicit or implicit choices on future locations of industrial production. The result will probably be both domestic production of and global trade with low-carbon basic materials. Contradictions between individual policy instruments across these two opposing goals are conceivable. For example, the German H2Global project tries to stimulate imports of green NH3, whereas the German CCfDs may contribute to the domestic transformation of the German fertilizer industry. Such contradicting approaches can be interpreted as the outcome of a mindset which seeks to conserve industrial production and trade patterns. This mindset is characterized by the expectation that fossil imports can be replaced with H2 imports in basic-material value chains and that derivatives (especially NH3) will be imported via ships, cracked into H2 at harbours and distributed inland via pipelines. Such a strategy is challenged by high costs. As soon as RE-rich exporting countries seek to secure more parts of future basic-material value chains, diminishing competitiveness in RE-scarce regions would lead to green relocation and stranded assets or require expensive public compensation schemes. In public debates, it is sometimes raised that green relocation might result in a widespread de-industrialization. Again, this belief may be challenged given that intermediate products (especially NH3 or MeOH) will probably become basic energy carriers in future decarbonized energy systems and that the greatest share of industrial value creation is associated with production steps much further downstream from basic-material production. In conclusion, a long-term strategy accounting for the renewables pull and a consistent short-term policy mix can avoid frictions between individual instruments and path dependencies that otherwise would lead to disruptive changes and high costs.

To arrive at such a harmonized strategy, RE-scarce countries first need to assess how they would be impacted by green relocation and how this would align with overarching societal goals. The following three considerations appear to be key. (1) Security of supply is typically easier to establish for energy carriers and, more generally, for rather homogeneous goods with high supplier substitutability which can be produced low-tech, with a global market likely to emerge. Notably, this is particularly true for shipping-based trade, whereas pipelines might induce strong bilateral dependencies. This suggests that security of supply will generally be possible to achieve through importing hydrogen or intermediates, however, this has to be assessed case by case across sectors and depth of relocation. For DRI, the emergence of a global market is unclear, yet existent dependencies on iron-ore imports raise the question whether switching to DRI imports would create much difference. For green NH3, the emergence of a liquid and diversified market seems likely, given (i) today’s global trade volumes for grey NH3 and (ii) announcements of green NH3 production and terminal capacity28. Markets for green carbonaceous feedstocks such as MeOH are currently more uncertain than for green NH3, hence relying on imports in the short- to mid-term might also entail supply risks, while fossil methanol can serve as a backup during the transition. Finally, trade dependencies need to be determined on a country-specific level, as for example relocation within the EU entails less risk than relocation from the EU to other global regions. (2) Economic productivity and jobs are concerns often raised in public debates. Typically, the number of jobs and added value directly affected by relocation of basic-materials production is comparably low in industrialized countries, yet more research is needed to understand potential knock-on effects for downstream industries (for example, machinery produced from steel and plastics produced from ethylene). Generally, structural change may allow for more efficient use of production factors, such as human capital and scarce renewable energy; however, this may be met by strong opposition among affected societal groups and actors with vested interests. (3) Every energy-intensive process relocated away from RE-scarce regions will also reduce domestic electricity demand, probably resulting in reduced prices for electricity for all consumers. Allowing some energy-intensive processes to relocate to locations with more favourable RE availability could ease pressure on RE expansion targets in RE-scarce countries.

On the basis of the impact assessment above, policy-makers need to decide if and how to intervene in potential relocation of industrial production. The following approaches may be used to address green relocation. (1) In spite of current global onshoring and nearshoring trends, future supply of energy-intensive basic materials could be secured via global imports. Strategies pursuing this solution would aim to foster liquid and diverse markets through collaboration with and technology diffusion across a broad range of potential exporting countries. This may be accompanied by retaining a small level of domestic production capacity and building up strategic reserves (for example, fertilizers). (2) Subsidy-based schemes of green-relocation protection are possible but could become costly and are not economically efficient. However, some policy-makers have recently voiced their willingness to secure domestic supply chains through subsidies despite the high cost, albeit only as a temporary measure during the transition (for example, the proposed German industrial electricity-price subsidy29). Such a proposal must be informed about the necessity of sustained policy support beyond early stages of the green transition needed to avoid future green relocation due to the renewables pull. If governments decide to protect against green relocation via subsidies, they probably need to strike a balance between affordability and securing value chains by being selective about industrial sectors, the share of production retained domestically and the depth of relocation allowed. Specifically, subsidies could be used to steer towards the above-mentioned sweet spots of relocation, resulting in green value chains being split such that only the most energy-intensive parts are located in RE-rich regions. (3) Another complementing strategy for dampening the renewables pull might be a focus on an efficient use of scarce energy resources through material efficiency, circularity and demand-side flexibility (see also the section on flexibility, circularity and demand reduction in Supplementary Information). Increased mechanical and chemical recycling of plastics or secondary steel from scrap would reduce the dependence on energy-intensive primary materials. Designing industrial plants capable of load following the hourly availability of RE could reduce energy cost30,31,32.

There is an urgent need for a broad societal debate on the role of a country in global industrial production informed by scientific assessments of pros, cons and trade-offs. The scientific community can support this debate in RE-scarce countries with further research on future market structures of green products, difficult-to-quantify soft factors determining private investment decisions, macroeconomic impacts, sector-specific details and policy assessment. Moreover, the assessment of green relocation presented here takes the perspective of RE-scarce countries. For a more comprehensive scientific debate, research on green relocation needs to include a diversity of perspectives in light of existing power dynamics between RE-scarce and RE-rich countries. Exporting and importing countries which occupy different positions might arrive at different evaluations of green relocation.

To better inform societal and policy debates on the energy transition, integrated-assessment and energy-system modelling may account for the renewables pull, green relocation and the associated geopolitical dimensions. Specifically, models may need to go beyond the trade of energy carriers (such as H2) and also model the trade of energy-intensive goods such as steel, fertilizers and higher-value chemicals (HVCs). Scenario analysis and energy-system modelling will allow for an improved understanding of the impacts of green relocation on the overall energy system and the net-zero transition.

Methods

Terminology

Supplementary Table 6 contains an overview of terminology used within this article. We stress again that we use the term renewables pull to refer to the energy-cost incentive, while green relocation is the potentially resulting effect, that is relocation of industrial production as a consequence of energy-cost incentives. We note that our definition of the renewables pull is slightly adjusted from an earlier one given by ref. 4, where the two concepts were both referred to by the term renewables pull only, which the authors however revised in a more recent publication5.

Moreover, another term sometimes used for green relocation is green leakage, in analogy to the term carbon leakage, in which case relocation is incentivized by the evasion of climate-abatement cost. While carbon leakage is predominantly considered as undesirable, as it undermines climate-mitigation efforts, green leakage comes with both risks and opportunities. We therefore prefer the term green relocation to enable an open and unbiased debate.

Quantitative estimations

An overview of how quantitative results are compiled is presented in Supplementary Fig. 4. Details on the individual steps and associated assumptions are presented below.

Technology data from literature review

Technology data required for the calculation of the levelized cost of production (LCOP) outlined below (that is, capital and operational expenditures and specific energy/feedstock demands, which we define below) are obtained from POSTED, the Potsdam Open-Source Techno-Economic Database v.0.2.3 (ref. 33). In doing so, we used 181 individual entries of techno-economic data from a total of 33 original data sources1,11,28,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63 to represent the following nine processes: alkaline water electrolysis, low-temperature DAC, industrial heat pumps (for delivering heat for DAC at 80–120 °C), direct-reduction furnaces, electric-arc furnaces (EAFs), NH3 synthesis via the Haber–Bosch (HB) process using nitrogen from an air-separation unit (ASU), urea synthesis, MeOH synthesis via the hydrogenation of CO2 and methanol-to-olefins (MtO). Where several sources are available for one entry type, we either take the average value or proceed with the more conservative assumption. Conservative in this case means assuming the set of parameters least supporting a renewables pull (high CAPEX and low energy demand). The main technology parameters resulting from this literature review are reported in Supplementary Table 7.

Technology assumptions

For our estimations, we consider green value chains based on RE for the three products steel, urea and ethylene. All three value chains start with the production of H2 via alkaline electrolysis. In the case of steel, H2 is used to reduce iron ore in a direct-reduction shaft to produce DRI, which is then melted in an EAF, cast and hot rolled into HRC. In the case of urea, H2 and atmospheric nitrogen from an ASU are reacted via the HB process to yield NH3, which is then combined with atmospheric CO2 from DAC to synthesize urea. In the case of ethylene, H2 and CO2 from DAC constitute the synthesis gas for MeOH production, which is then reacted to ethylene in an MtO process (note that the output of MtO is actually a mixture of ethylene, propylene and other byproducts but for simplicity we refer to it by just ethylene hereafter). When splitting these value chains into their three main processing steps, we associate the winning of CO2 from DAC to the process step consuming this as a feedstock, that is the final step in the urea and the second step in the ethylene value chain.

The heat for DAC can be provided by low-temperature industrial heat pumps with a coefficient of performance of around 3–3.5. This assumption is justified, as the required temperature T for low-temperature DAC is only T ≈ 80–120 °C and waste heat should typically be available from the processes consuming the CO2 (MeOH and urea synthesis). This means that the heat demand of DAC of ~1.68 MWh t−1 translates into only ~0.51 MWh t−1 of electricity demand for the heat pump, while adding CAPEX for the heat pump.

The heat required by all other processes, which require T ≳ 200 °C, is assumed to be provided by resistive (Ohmic), radiative, microwave or inductive heating64, for which we assume a constant efficiency of 100%. These assumptions are valid, as such electrified heating of industrial processes is piloted and the technology is straightforward and available, whereas high-temperature industrial heat pumps for T ≳ 200 °C are still in early development (TRL 4–5; ref. 65) and the efficiency and feasibility of heat pumps for T ≳ 400 °C (for most chemical processes) and T ≳ 800 °C (for steel processes) is unclear.

Importing intermediates (DRI, MeOH and NH3 in the specific cases estimated here) can reduce the potential for heat integration and hence increase energy demand. In the case of DRI, we account for this in electricity demand by adding 0.159 MWh t−1 (ref. 1). In the cases of urea and ethylene, we neglect this, mainly because of poor data availability. Most literature from the past assumes waste heat availability from upstream fossil processes such as steam methane reforming (SMR; needed to produce the required grey H2). That said, there are other ways to make use of waste heat and potential electricity generated from it, such as (1) selling electricity to the grid, (2) feeding heat into urban district heating, (3) recycling heat and electricity internally for preheating of precursors and operating the plant or (4) using waste heat for onsite DAC or high-temperature solid-oxide electrolysis (water to H2 or CO2 to CO). While options (1) and (2) are probably more relevant for RE-scarce importers with good grid infrastructure and remote urban areas, options (3) and (4) can be applied for both RE-scarce importers and RE-rich exporters.

The fresh-water demand for the production of green H2 can be a relevant factor for some RE-rich exporters with water scarcity. Our assumed price for water includes cost of water desalination, yet this leads only to a minor contribution to the overall production cost across all value chains. It should be noted that there may be countries/regions where water availability can pose a major obstruction to the development of green value chains. Here, for the steel value chain, case 1 (the import of H2) is the only case with implicit transportation of water from the RE-rich to the RE-scarce region. In all other cases, the water could be cycled between the electrolyser and the DR shaft for onsite H2 production1. This could add another reason for why importing DRI or importing semifinished steel could be cheaper compared to importing H2 but this constitutes only a minor point for most RE-rich exporters and we therefore neglect it in our estimations.

We assume the operational capacity factor (OCF) to be 95% for all plants except for the electrolyser, which we assume to have an OCF of 50%. A detailed discussion of flexible operation of plants is provided in Supplementary Information.

Transport costs

Depending on the considered import case, transport costs are added for the respective traded goods, representing international trade based on shipping (and pipelines for case 1B). Specifically, case 1 adds transport costs for H2, case 2 for intermediates (DRI, NH3 and MeOH) and case 3 for (semi)finished products (HRC, urea and ethylene). We assume that CO2 is not traded but produced from DAC at the point where it is needed. Moreover, we add transport costs for iron ore in the base case and case 1, as we assume the exporting country of DRI to be a producer of iron ore. This assumption is justified since the largest three iron-ore exporting countries (Australia, Brazil and South Africa) all have ample RE potentials.

Specific (that is, per mass) transport costs are researched and reported in Supplementary Table 8. In principle, specific transport costs are dependent on distance, yet in practice we can assume generic values independent of distance and specific cases. This is particularly the case for shipping (as confirmed by UNCTADstat data), where harbour dues, terminal costs and liquefaction (especially H2) make up a large share of the total transport cost.

For shipping-based H2 transport, specific costs are in the range US$2.0–2.6 per kgH2 in 2030, depending on distance and transport medium used (liquid H2, liquid organic H2 carriers or NH3)66. This corresponds to €55–72 MWh−1; hence we assume €50 MWh−1, which includes learning effects achieved by 2040. Pipeline-based imports are only feasible for short-distance transportation of ~1,000 km, which gives US$0.5–1.0 per kgH2 of transport cost, depending mainly on whether new pipelines are built or old ones are repurposed66. This corresponds to €14–28 MWh−1; hence we choose €15 MWh−1.

Commodities other than H2 are established in international trade and country-specific bilateral transport costs in 2016 are reported by ref. 67, which we analyse in Supplementary Information and report in Supplementary Table 8. While transport costs for iron ore were only €2.5 t−1 in 2016, these drastically increased in recent years, are in the range €5–40 t−1 now and are predicted to peak soon68,69. Others70 derive transport costs of €35 t−1 for NH3 and MeOH for today based on literature review. We conclude with the values reported in Supplementary Table 8, which are supposed to capture relative trends from the 2016 UNCTADstat data and also account for absolute trends in recent markets.

Retrofitting and repurposing of grey production capacity

When determining the required investment in our estimations, another question arises as to whether new green production plants will need to be built in both RE-scarce importing and RE-rich exporting regions or if the former can repurpose/retrofit existing capacities. Clearly, new electrolysis, DAC, DR, EAF, casting, MeOH synthesis and MtO plant capacity would need to be built to meet future demands of the respective green products. On the contrary, hot-rolling plants, HB plants and urea synthesis plants could, in principle, be repurposed/retrofitted. In the case of HB, this will probably require retrofitting the heat supply, which in today’s grey HB plants is satisfied through integrated SMR and which would need to be replaced with electrified heating. Urea synthesis capacity can probably be reused without the need for large investment. Regarding the production of green ethylene, it should be noted that a competing route would be via the cracking of green naphtha, which would repurpose existing steam-cracker capacity and hence make better use of fossil infrastructure yet at the expense of likely lower energy efficiency and whose study is beyond the scope of this work. More generally beyond technology-specific considerations, integration into existing infrastructure, the lack of free space for construction and the requirement of continued operation of other plants in an existing industrial park create obstacles for brownfield investments that are not existent for greenfield investments, potentially resulting in substantially higher cost. In summary, investment into new capacity is the same across both regions, whereas the option of repurposing hot-rolling, HB and urea plants is studied in the sensitivity analysis (Extended Data Fig. 1).

Financing assumptions

Many of the RE-rich exporting regions implicitly considered in this article have higher financing cost compared to the RE-scarce importing regions. This effect is captured by a higher WACC assumed to determine the annuity factor used in the calculation of the LCOP below. Clearly, such an increase in WACC is not universal, as for example Australia is a country with a high potential to become an RE-rich exporter, while profiting from an established economy with a low WACC. Nonetheless, we assume 5% for the RE-scarce and 8% for the RE-rich region in the results presented in Figs. 4 and 5 and we provide sensitivity analysis in Extended Data Fig. 1. For simplicity and to demonstrate the minor effect of capital and financing cost, we assume a low value of 18 years for the book lifetime of new green facilities independent of the technical lifetime of plants. Notably, while financing costs can also increase the cost of wind and solar capacities and hence electricity prices, our analysis treats electricity prices as an exogenous parameter independent of financing costs.

Calculating the levelized cost of production

On the basis of these assumptions and the curated techno-economic data (see below), we can calculate the LCOP as follows:

ANF is the annuity factor given as (i × (1 + i)n)/((1 + i)n − 1) with interest rate i ∈ [0, 1] and lifetime n in years, CAPEX is the total capital expenditure in units of annual production capacity, FOPEX is the annual fixed operational expenditures per annual production capacity, OCF ∈ [0, 1], VOPEX is the variable operational expenditure per output quantity (non-energy, non-feedstock), dk is the specific demand for feedstock or energy carrier k, pk is the associated price, dg is the specific demand of transported intermediate feedstock or energy carrier g and tcg is the associated specific transport cost.

Other assumptions

We note that our conceptual framework and our estimations assume electricity and heat supply from renewable sources, where the residual GHG intensity in both regions is negligible and roughly the same, such that no competitive advantage emerges from cleaner production in one or the other region (for example, carbon costs due to carbon pricing).

When estimating the potential green-relocation protection in Germany, we take the 2040 projections for steel demand from a study of long-term scenarios on German industry decarbonization21 and for NH3 and ethylene demand from a study of the green transformation of the German chemical industry22.

Potential exporting countries in the German case study

The conceptual framework and quantitative estimations presented in this work are kept generic and do not assume specific exporting countries. Yet, in our case study of German imports and potential green-relocation protection, we try to illustrate future export corridors and hence list potential exporting countries. To identify such candidates, we analyse countries with high RE potentials according to the following aspects: (1) whether a country produces and exports the respective commodity based on fossils today, (2) whether substantial green projects have been announced and, in the case of steel, (3) the availability of iron ore. This procedure results in a non-exhaustive list of potential candidates presented in Supplementary Table 9.

Data availability

A copy of input data and results is published on Zenodo at https://doi.org/10.5281/zenodo.10641486 (ref. 71). This includes (1) an Excel spreadsheet file reporting techno-economic assumptions obtained from POSTED, (2) several plain-text files containing other assumptions and data needed to reproduce all results, (3) the results reported in Figs. 4, 5 and 6 and (4) a Jupyter notebook showcasing how the results can be obtained with basic Python code. Moreover, results of our study can be reproduced with adjusted assumptions via an interactive webapp at https://doi.org/10.5880/pik.2024.002 (ref. 72), which also allows viewing individual cost components for every process in each value chain shown in Fig. 5.

Code availability

A permanent copy of the software code needed to reproduce all figures and run the interactive webapp is publicly available on Zenodo at https://doi.org/10.5281/zenodo.10869780 (ref. 73), which may also be viewed via GitHub at https://github.com/PhilippVerpoort/green-value-chains/. The software uses data and analysis tools from POSTED v.0.2.3 (ref. 33) and builds on the PIW (Potsdam Interactive Webapp) framework library v.0.8.2 (ref. 74).

References

Vogl, V., Åhman, M. & Nilsson, L. J. Assessment of hydrogen direct reduction for fossil-free steelmaking. J. Clean. Product. 203, 736–745 (2018).

Lopez, G., Keiner, D., Fasihi, M., Koiranen, T. & Breyer, C. From fossil to green chemicals: sustainable pathways and new carbon feedstocks for the global chemical industry. Energy Environ. Sci. 16, 2879–2909 (2023).

Boulamanti, A. & Moya, J. A. Production costs of the chemical industry in the EU and other countries: ammonia, methanol and light olefins. Renew. Sustain. Energy Rev. 68, 1205–1212 (2017).

Samadi, S., Lechtenböhmer, S., Viebahn, P. & Fischer, A. Renewables pull—Verlagerung industrieller Produktion aufgrund unterschiedlicher Kosten erneuerbarer Energien. Energiewirtschaftliche Tagesfragen 71, 10–13 (2021).

Samadi, S. The renewables pull effect: how regional differences in renewable energy costs may influence future locations of industrial production. Energy Res. Social Sci. 104, 103257 (2023).

Energy Statistics—An Overview (EUROSTAT, 2023); https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Energy_statistics_-_an_overview#Imports_and_exports

Korea 2020 Energy Policy Review (IEA, 2020); www.iea.org/reports/korea-2020

Zhu, D., Mortazavi, S. M., Maleki, A., Aslani, A. & Yousefi, H. Analysis of the robustness of energy supply in Japan: role of renewable energy. Energy Rep. 6, 378–391 (2020).

Gielen, D., Saygin, D., Taibi, E. & Birat, J. Renewables-based decarbonization and relocation of iron and steel making: a case study. J. Indust. Ecol. 24, 1113–1125 (2020).

Trollip, H., McCall, B. & Bataille, C. How green primary iron production in South Africa could help global decarbonization. Clim. Policy 22, 236–247 (2022).

Devlin, A. & Yang, A. Regional supply chains for decarbonising steel: energy efficiency and green premium mitigation. Energy Convers. Manag. 254, 115268 (2022).

Devlin, A., Kossen, J., Goldie-Jones, H. & Yang, A. Global green hydrogen-based steel opportunities surrounding high quality renewable energy and iron ore deposits. Nat. Commun. 14, 2578 (2023).

Salmon, N. & Bañares-Alcántara, R. Green ammonia as a spatial energy vector: a review. Sustain. Energy Fuels 5, 2814–2839 (2021).

Fasihi, M., Weiss, R., Savolainen, J. & Breyer, C. Global potential of green ammonia based on hybrid PV-wind power plants. Appl. Energy 294, 116170 (2021).

Galimova, T. et al. Global trading of renewable electricity-based fuels and chemicals to enhance the energy transition across all sectors towards sustainability. Renew. Sustain. Energy Rev. 183, 113420 (2023).

Longden, T., Beck, F. J., Jotzo, F., Andrews, R. & Prasad, M. ‘Clean’ hydrogen?—comparing the emissions and costs of fossil fuel versus renewable electricity based hydrogen. Appl. Energy 306, 118145 (2022).

Pye, S. et al. Regional uptake of direct reduction iron production using hydrogen under climate policy. Energy Clim. Change 3, 100087 (2022).

Richstein, J. C. & Neuhoff, K. Carbon contracts-for-difference: how to de-risk innovative investments for a low-carbon industry? iScience 25, 104700 (2022).

World Steel in Figures 2022 (World Steel Association, 2023); https://worldsteel.org/steel-topics/statistics/world-steel-in-figures-2023/

Fertilizer Industry Facts & Figures (Fertilizers Europe, 2022); www.fertilizerseurope.com/publications/industry-facts-and-figures-2022/

Fleiter, T. et al. Long-term Scenarios 3: Scientific Analyses on the Decarbonization of Germany, Industry Sector (Langfristszenarien, 2022); https://langfristszenarien.de/enertile-explorer-de/dokumente/

Wie die Transformation der Chemie gelingen kann (VCI & VDI, 2023); www.vci.de/services/publikationen/chemistry4climate-abschlussbericht-2023.jsp

Deutscher Bundeshaushalt Digital (German Federal Ministry of Finance, 2022); www.bundeshaushalt.de/DE/Bundeshaushalt-digital/bundeshaushalt-digital.html

Knopf, B. & Illenseer, N. Die Finanzierung der Transformation: Klimafonds, Klimageld und Kernhaushalt (MCC, 2023); www.mcc-berlin.net/en/research/publications/publications-detail/article/die-finanzierung-der-transformation-klimafonds-klimageld-und-kernhaushalt.html

Japan Aims to Set up Commercial Hydrogen Fuel Supply Chain by 2030 (Reuters, 2020); www.reuters.com/article/us-japan-energy-hydrogen-idUKKBN2700PM

REPowerEU: A Plan to Rapidly Reduce Dependence on Russian Fossil Fuels and Fast Forward the Green Transition (EUR-Lex, 2022).

Press Release: Federal Ministry for Economic Affairs and Climate Action Launches First Auction Procedure for H2Global—€900 Million for the Purchase of Green Hydrogen Derivatives (German Federal Ministry for Economic Affairs and Climate Action, 2022); www.bmwk.de/Redaktion/EN/Pressemitteilungen/2022/12/20221208-federal-ministry-for-economic-affairs-and-climate-action-launches-first-auction-procedure-for-h2global.html

Ammonia Technology Roadmap—Towards More Sustainable Nitrogen Fertiliser Production (IEA, 2021); www.iea.org/reports/ammonia-technology-roadmap

German Coalition Ministers Clash Over ‘Gamechanger’ Power Subsidy Plan (Reuters, 2023); www.reuters.com/business/energy/german-economy-ministry-proposes-industrial-power-price-6-cents-per-kwh-2023-05-05/

Toktarova, A., Walter, V., Göransson, L. & Johnsson, F. Interaction between electrified steel production and the north European electricity system. Appl. Energy 310, 118584 (2022).

Toktarova, A., Göransson, L., Thunman, H. & Johnsson, F. Thermochemical recycling of plastics—modeling the implications for the electricity system. J. Clean. Prod. 374, 133891 (2022).

Golmohamadi, H. Demand-side management in industrial sector: a review of heavy industries. Renew. Sustain. Energy Rev. 156, 111963 (2022).

Verpoort, P. C. et al. POSTED: Potsdam open-source techno-economic database. V.0.2.3. Zenodo https://doi.org/10.5281/zenodo.10640888 (2024).

Al-Qahtani, A., Parkinson, B., Hellgardt, K., Shah, N. & Guillen-Gosalbez, G. Uncovering the true cost of hydrogen production routes using life cycle monetisation. Appl. Energy 281, 115958 (2021).

Arnaiz del Pozo, C. & Cloete, S. Techno-economic assessment of blue and green ammonia as energy carriers in a low-carbon future. Energy Convers. Manag. 255, 115312 (2022).

Bazzanella, A. M. & Ausfelder, F. Low Carbon Energy and Feedstock for the European Chemical Industry (DECHEMA, 2017); https://dechema.de/en/Low_carbon_chemical_industry-path-123212,124930.html

Study on the Competitiveness of the European Steel Sector (EU, 2008); https://op.europa.eu/en/publication-detail/-/publication/7b6df831-0266-40a1-9ca2-13992d526bf7

Large Volume Inorganic Chemicals—Ammonia, Acids and Fertilisers (European Commission, 2007) https://eippcb.jrc.ec.europa.eu/reference/large-volume-inorganic-chemicals-ammonia-acids-and-fertilisers

Fasihi, M., Efimova, O. & Breyer, C. Techno-economic assessment of CO2 direct air capture plants. J. Clean. Product. 224, 957–980 (2019).

Fiamelda, L., Suprihatin & Purwoko Analysis of water and electricity consumption of urea fertilizer industry: case study PT. X. IOP Conf. Ser. Earth Environ. Sci. 472, 012034 (2020).

Hauser, P. D., Burmeister, H., Münnich, P. J., Witecka, W. K. & Mühlpointner, T. Klimaschutzverträge für die Industrietransformation (Agora Energiewende, 2021).

Hegemann, K.-R. & Guder, R. Stahlerzeugung (Springer, 2020).

Hölling, M., Weng, M. & Gellert, S. Bewertung der Herstellung von Eisenschwamm unter Verwendung von Wasserstoff. Stahl Eisen 137, 47–53 (2017).

Holst, M., Aschbrenner, S., Smolinka, T., Voglstätter, C. & Grimm, G. Cost Forecast for Low Temperature Electrolysis—Technology Driven Bottom-up Prognosis for PEM and Alkaline Water Electrolysis Systems (ISE, 2021); www.ise.fraunhofer.de/content/dam/ise/de/documents/publications/studies/cost-forecast-for-low-temperature-electrolysis.pdf

Direct Air Capture—A Key Technology for Net Zero (IEA, 2022); www.iea.org/reports/direct-air-capture-2022

Global Hydrogen Review (IEA, 2021); www.iea.org/reports/global-hydrogen-review-2021

Global Hydrogen Trade to Meet the 1.5 °C Climate Goal: Part III—Green Hydrogen Cost and Potential (IRENA, 2022); www.irena.org/publications/2022/May/Global-hydrogen-trade-Cost

Ikäheimo, J., Kiviluoma, J., Weiss, R. & Holttinen, H. Power-to-ammonia in future North European 100% renewable power and heat system. Int. J. Hydrog. Energy 43, 17295–17308 (2018).

Jacobasch, E. et al. Economic evaluation of low-carbon steelmaking via coupling of electrolysis and direct reduction. J. Clean. Product. 328, 129502 (2021).

Jarvis, S. M. & Samsatli, S. Technologies and infrastructures underpinning future CO2 value chains: a comprehensive review and comparative analysis. Renew. Sustain. Energy Rev. 85, 46–68 (2018).

Keith, D. W., Holmes, G., St. Angelo, D. & Heidel, K. A process for capturing CO2 from the atmosphere. Joule 2, 1573–1594 (2018).

Kent, J. A. Riegel’s Handbook of Industrial Chemistry (Springer, 1974).

Madhu, K., Pauliuk, S., Dhathri, S. & Creutzig, F. Understanding environmental trade-offs and resource demand of direct air capture technologies through comparative life-cycle assessment. Nat. Energy 6, 1035–1044 (2021).

Matzen, M. J., Alhajji, M. H. & Demirel, Y. Technoeconomics and sustainability of renewable methanol and ammonia productions using wind power-based hydrogen. J. Adv. Chem. Eng. https://doi.org/10.4172/2090-4568.1000128 (2015).

Oliveira, C. Advanced Methanol to Olefines Process (TNO, 2021); https://energy.nl/media/data/Technology-Factsheet-Advanced-methanol-to-olefins.pdf

Otto, A. et al. Power-to-steel: reducing CO2 through the integration of renewable energy and hydrogen into the German steel industry. Energies 10, 451 (2017).

Ozkan, M., Nayak, S. P., Ruiz, A. D. & Jiang, W. Current status and pillars of direct air capture technologies. iScience 25, 103990 (2022).

Pérez-Fortes, M., Schöneberger, J. C., Boulamanti, A. & Tzimas, E. Methanol synthesis using captured CO2 as raw material: techno-economic and environmental assessment. Appl. Energy 161, 718–732 (2016).

Rechberger, K., Spanlang, A., Sasiain Conde, A., Wolfmeir, H. & Harris, C. Green hydrogen-based direct reduction for low-carbon steelmaking. Steel Res. Int. 91, 2000110 (2020).

Sasiain, A. et al. Green hydrogen as decarbonization element for the steel industry. BHM Berg- und Hüttenmännische Monatshefte 165, 232–236 (2020).

Vartiainen, E. et al. True cost of solar hydrogen. Solar RRL 6, 2100487 (2021).

Worrell, E., Price, L., Neelis, M., Galitsky, C. & Zhou, N. World Best Practice Energy Intensity Values for Selected Industrial Sectors (Lawrence Berkeley National Laboratory, 2007); https://escholarship.org/uc/item/77n9d4sp

Wörtler, M. et al. Steel’s Contribution to a Low-Carbon Europe 2050 (Boston Consulting Group, 2013); www.bcg.com/publications/2013/metals-mining-environment-steels-contribution-low-carbon-europe-2050

Madeddu, S. et al. The CO2 reduction potential for the European industry via direct electrification of heat supply (power-to-heat). Environ. Res. Lett. 15, 124004 (2020).

The Future of Heat Pumps (IEA, 2022); www.iea.org/reports/the-future-of-heat-pumps

Global Hydrogen Review (IEA, 2022); www.iea.org/reports/global-hydrogen-review-2022

Hoffmeister, O. et al. Developing a Global Transport Costs Dataset for International Trade (UNCTAD, 2022); https://doi.org/10.18356/27082814-85

Sand, P. Iron ore spot freight rates spike 163% to lift capesize earnings. Hellenic Shipping News Worldwide (30 September 2021); www.hellenicshippingnews.com/bimco-iron-ore-spot-freight-rates-spike-163-to-lift-capesize-earnings/

Lee, D. Capesize regional tightness signals stronger freight rates in the short term but likely to peak soon. S&P Global Market Intelligence Website (4 October 2021); www.spglobal.com/marketintelligence/en/mi/research-analysis/capesize-freight-rates.html

Perner, J. & Unteutsch, M. Wirtschaftlichkeit von PtX-Produkten aus Nordafrika—Geschäftsmodelle für H2 und seine Derivate (Frontier Economics, 2021); www.frontier-economics.com/media/4979/frontier-ptx-business-cases-studie_teil-1-hauptstudie.pdf

Verpoort, P. C., Gast, L., Hofmann, A. & Ueckerdt, F. Research data supporting "Impact of global heterogeneity of renewable energy supply on heavy industrial production and green value chains". V. 4.1.0. Zenodo https://zenodo.org/records/10869959 (2024).

Verpoort, P. C., Gast, L., Hofmann, A. & Ueckerdt, F. Interactive webapp for techno-economic analysis of green value chains. V. 4.1.0. GFZ Data Services https://doi.org/10.5880/pik.2024.002 (2023).

Verpoort, P. C., Gast, L., Hofmann, A. & Ueckerdt, F. Research software used for techno-economic analysis of the impact of global heterogeneity of renewable energy supply on heavy industrial production and green value chains. V. 4.1.0. Zenodo https://doi.org/10.5281/zenodo.10869780 (2024).

Verpoort, P. C. Potsdam interactive webapp (PIW) framework library. V. 0.8.2. Zenodo https://doi.org/10.5281/zenodo.10640781 (2024).

Acknowledgements

We thank G. Luderer, T. Brown, J. Hampp, M. Schimmel, T. Sach, D. Bietenholz, S. Samadi, C. Schneider, K. Unverzagt and J. Müßel for valuable discussions and comments while preparing and revising the paper and C. Bachorz and P. Effing for help with curating techno-economic data and writing software code for POSTED. P.C.V. and F.U. received support for the research for this work by the Kopernikus-Ariadne project by the German Federal Ministry of Education and Research (grant nos. 03SFK5A, 03SFK5A0-2), the INTEGRATE project by the German Federal Ministry for Economic Affairs and Climate Action (grant no. 01LP1928C) and the HyValue project (grant no. 333151). F.U. and L.G. received support for the research for this work by the CCfD project by the German Federal Ministry for Economic Affairs and Climate Action (grant no. DE64B88F-54CC-4CFB-B802-7CEC1AA2E542).

Funding

Open access funding provided by Potsdam-Institut für Klimafolgenforschung (PIK) e.V.

Author information

Authors and Affiliations

Contributions

F.U. and P.C.V. suggested the research question. P.C.V. and F.U. jointly conceived and designed the study in consultation with A.H. and L.G. P.C.V., A.H. and L.G. curated the techno-economic data. P.C.V. wrote the code for performing the calculations and designed and created the figures. P.C.V. and F.U. wrote the paper with contributions from L.G.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Energy thanks Tobias Fleiter, Ric Hoefnagels and Mariesse van Sluisveld for their contribution to the peer review of this work.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Extended data

Extended Data Fig. 1 Sensitivity analysis.

Shown are the main results from Fig. 4 with electricity-price difference of 40 EUR/MWh, while varying the WACC on the RE-rich exporter between 5% and 20% (a–c), relative changes in CAPEX between -50% and +100% (d–f), transport cost for H2 between 5 EUR/MWh and 90 EUR/MWh (g–i), whether the heat for DAC is provided by a heat pump or not (j–k) and whether existing grey plants (hot rolling in steel, HB-ASU, urea synth.) can be repurposed (l–m).

Supplementary information

Supplementary Information

Supplementary Tables 1–9, Figs. 1–4 and Discussion.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Verpoort, P.C., Gast, L., Hofmann, A. et al. Impact of global heterogeneity of renewable energy supply on heavy industrial production and green value chains. Nat Energy 9, 491–503 (2024). https://doi.org/10.1038/s41560-024-01492-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41560-024-01492-z

This article is cited by

-

Impact of global heterogeneity of renewable energy supply on heavy industrial production and green value chains

Nature Energy (2024)

-

The role of border carbon adjustments and subsidies in incentivising investment: comparing equivalence in the context of steel recycling and decarbonisation

Discover Sustainability (2024)

-

Catalysis for Renewable Energy and Sustainable Development

Topics in Catalysis (2024)