Abstract

Are Climate Change Champions favorable to investors? This is the first study of portfolio performance of a fourth generation SRI screening strategy based on United Nations Global Compact firms who are Climate Change Champions. The operational changes made by UNGC firms are real and disproves the notion that UNGC firms are merely green-washing. We find that after firms join UNGC, there is a positive effect on long term portfolio performance. UNGC firms have lower volatility and so less risk than their competitors. We find an apparent mispricing of lower risk in market returns as standard asset pricing models may not be pricing investors’ aversion to climate change risk and preference for firms actively combating climate change. This lends support to Fama and Frenchs’ theory that says that these “tastes” are valid factors to provide a more complete asset pricing model. Our study encourages investment in UNGC-CCC firms as we find there is no underperformance penalty against a conventional portfolio because the lower return reflects lower risk. Thus, our evidence suggests that “doing good for society is also good for business.”

Similar content being viewed by others

Introduction

Are investors rewarded when their firms adopt climate change as their corporate social responsibility (CSR) mission? The existential threat posed by climate change leads to many technological innovations impacting how we live and use resources. For example, zero-energy buildings consume as much energy as they generate by renewable energy sources. Climate change influences many organizations to implement saving the environment as their CSR mission. However, industries with direct inputs and products related to climate change, like the petroleum industry, face a dilemma; to adapt to climate change or not. Indeed, the petroleum and fossil fuels industry risk losing to renewable power industries. “Renewable power is increasingly cheaper than any new electricity capacity based on fossil fuels”, according to a new report by the International Renewable Energy Agency (The International Renewable Energy Agency, 2020). This report states that more than half of the renewable capacity added in 2019 achieved lower power costs than the cheapest new coal plants.

The most prominent organization by which these corporations can visibly demonstrate their CSR commitment is by joining the United Nations Global Compact. Founded in 2000, the United Nations Global Compact (UNGC) is the largest and most recognized voluntary CSR initiative with more than 10,000 members from 162 countries. Firms join for both ethical and economic reasons (Cetindamar and Husoy, 2007). Members of UNGC agree to integrate the ten UNGC principles, including human rights, labor, and the environment, into their strategies, policies, and operations, and report on these activities. In the UNGC Corporate Sustainability report (United Nations Global Compact, 2013), “companies indicate that they see the big picture of how addressing sustainability issue is good for business and the societies in which they have a presence.”

In the first literature review on studies of UNGC member firms, Rasche et al. (2012) note that researchers so far examine the historical, operational, and governance aspects of UNGC. These few studies only examine the case, country, and industry-specific impacts of UNGC firms. There is a gap in the literature on the performance impact of joining UNGC membership. We contribute to the broader SRI literature as reviewed by Renneboog et al. (2008). Our study is among the first study on the portfolio performance of fourth generation SRI screening firms. Indeed, it is the first study on United Nations Climate Change Champions, firms who chose to be pro-active leaders for fighting climate change.

UNGC created a set of specialized causes or initiatives for its members to join. One of these is the Climate Change Champions initiative. UNGC has adopted three principles under climate change; (1) “businesses should support a precautionary approach to environmental challenges; (2) undertake initiatives to promote greater environmental responsibility, and (3) encourage the development and diffusion of environmentally friendly technologies.” The Climate Change Champions (CCC) initiative is governed by the UN Global Compact (United Nations Global Compact, 2016), the UN Environment Program (United Nations Environment Programme, 2016), and the secretariat of the UN Framework Convention on Climate Change (United Nations Framework Convention on Climate Change, 2016).

Few studies exist on environmentally responsible corporate policies and their impacts on financial performance. Ng and Zheng (2018) conclude there is no penalty for investment performance for green energy companies. This conclusion counters the traditional view that CSR orientations in firms tend to compromise profit objectives. Rather, these firms are attracting investors and succeeding with their strong growth records. Nevertheless, climate change potentially affects investors’ returns because it threatens the economic value of assets (Covington and Thamotheram, 2014). The next two decades might see large systemic risks resulting in volatile investment values along with large potential returns. For example, the ski industry cannot operate under warm weather conditions in many traditional locations in the world (Nikolaou et al., 2015). Lee et al. (2015) find a negative impact of climate change on firm value. Studies on market performance of portfolios that divested fossil fuels and utilities firms are based on this first generation of negative screening SRI strategy (Dordi and Weber, 2019; Henriques and Sadorsky, 2018; Plantinga and Scholtens, 2021; Trinks et al., 2018). Generally, these studies show no decrease in risk adjusted return performance. Studies based on the second-generation strategy show that markets penalize firms’ negative environmental performance more consistently than reward its positive performance (Lee et al., 2015) and (Liesen, 2014).

Our study contributes to the SRI and climate finance literature because it is a first study of asset pricing of a third and fourth generation SRI portfolio. The companies in our study have proactively volunteered to join the United Nations Global Compact, the world’s gold standard for firms to be the best in practice in corporate social responsibility. Indeed, our Climate Change Champions are not only UNGC members, but are a special subset of firms choosing to be leaders of climate change intervention, which is a significantly greater commitment to social responsibility.

Our study of a UNGC-CCC portfolio is like a natural experimental study of a population of firms who have chosen to be Climate Change Champions. These firms have superior CSR standards across the ten principles of the United Nations Global Compact, which cover labor, human rights, environment, and corruption. Therefore, UNGC-CCC firms exceeds the second-generation criteria of positive SRI screening and the third-generation criteria of the “triple bottom line”. UNGC-CCC firms most accurately belong to the fourth-generation SRI strategy, which combines sustainability and shareholder activism. The UNGC institution has direct governing influence in granting the UNGC membership. This membership and its commitments do shape UNGC members corporate CSR objectives and shareholder value interests. For example, UNGC members are committed to reporting every year their progress in advancing the ten principles of the Global Compact. Unlike many studies in the CSR literature, our study utilizes a natural experiment over which the researchers have no control: the choice some companies make to join UNGC and further to make a commitment to being a Climate Change Champion, while some of their competitors choose not to make this commitment.

In line with the findings of the divestment of fossil fuels firms and SRI literature (Dordi and Weber, 2019; Henriques and Sadorsky, 2018; Plantinga and Scholtens, 2021; Trinks et al., 2018), we find that UNGC-CCC firms in of themselves do not reward or penalize investor’s performance. However, after joining UNGC, these firms show a positive effect. We provide evidence of causality of UNGC-CCC after joining UNGC, which shows positive impacts on portfolio performance.

We research whether a firm’s choice of climate change policies impacts its value. Two studies have examined climate change policies on a firm’s operating profitability (Gallego-Alvarez et al., 2014, 2015). In addition to profitability, we study the market performance of firms who voluntarily join the UNGC-Climate Change Champions (CCC) initiative. These CCC firms have direct stakes and influence on climate change. Their chief executives agree to set goals, develop and expand strategies and practices, and publicly disclose emissions. They also act as advocates for a global climate change agreement in global and local policy discussions. Furthermore, CCC firms encourage integrating carbon pricing into long-term corporate strategies and investment decisions, advocating for carbon pricing, and communicating their progress (Guide to Corporate Sustainability: Shaping a sustainable future, 2015). Climate Change Champions have a great role in leading the current and critical global dialog on adapting their businesses to contribute to the climate change crisis. We find that UNGC-CCC firms have higher financial performance than their non-UNGC competitors. Moreover, we find that these firms have significant financial operating performance changes. Our result implies that they have made real changes to their operations and that they are not green-washing.

We contribute to the crucial question of whether Climate Change Champions, who adopt and lead climate change policies, can do so without sacrificing financial performance. We find that UNGC-CCC portfolio risk-adjusted returns are lower than their matched competitor portfolio. Hence, our conclusion suggests that standard asset pricing models are under-pricing returns in our UNGC portfolio because these models do not account for investor preferences of disagreement and tastes as pricing factors.

Background

In theory, there has been a long-standing debate over whether businesses suffer costs to the profit objective for being environmentally responsible. The “Disagreement, tastes, and asset pricing” theory of Fama and French’s (2007) explains that consumer tastes and their disagreement over payoffs are valid factors of asset pricing. Consumer preferences drive the growth of socially responsible investing (Wallis and Klein, 2015). This theory suggests that corporate social responsibility can give value to firms. Indeed, Ng and Zheng (2018) find that green energy portfolios perform even better than a matching non-green portfolio and the industry S&P 500 Energy benchmark in the last 24 years. They find significantly positive alphas in green firms. In theory, firms also achieve maximizing shareholder wealth by maximizing the present value of future cash flows. Socially responsible initiatives (SRI) can accomplish this by lowering costs (e.g., reducing waste and regulatory fines), by increasing market power (by appealing to socially conscious buyers), or by lowering the cost of finance (by appealing to socially conscious investors) (Mackey et al., 2007). Socially responsible investments demonstrate a positive financial impact (Wallis and Klein, 2015). Revelli and Viviani (2014) conclude from their meta-analysis study that there is neither cost nor benefit to SRI. Ethical investors have existed as early as 1972 (Simon et al., 1972) who demonstrate loyalty traits in the face of losses compared to investors motivated purely by wealth maximization (Benson and Humphrey, 2008; Renneboog et al., 2011; and Peifer, 2014). News announcements from firms on eco-friendly behavior yield positive abnormal returns over a two-day event window; whereas, announcements of eco-harmful behavior lead to negative abnormal returns (Flammer, 2013). Firms who volunteer to report to the Carbon Disclosure Program (a consortium of over 300 institutional investors with $41 trillion in assets) suffer immediate negative effects on their market returns. Thus, investors view carbon information disclosures as negative news (Lee et al., 2013).

Renneboog et al. (2008) identify four generations of Socially responsible investing (SRI). The first generation is negative screening excluding specific industries or stocks based on social, environmental, and ethical criteria. For example, tobacco, gambling, and fossil fuel companies are filtered out of an SRI portfolio. The second generation of SRI strategy is positive screening for specific industries or stocks based on corporate governance, labor relations, cultural diversity criteria. For example, firms involved with renewable energy usage companies are selected. The third generation SRI strategy is an “integrated approach of selecting companies based on the economic, environmental and social criteria comprised by both negative and positive screens. This approach is often called “sustainability” or “triple bottom line” (due to its focus on People, Planet and Profit).” The fourth generation of SRI strategy combines the sustainability approach to SRI in the third generation together with shareholder activism. Here, portfolio managers or the organizations who grant the ethical labels work to influence the managers of these companies.

Hypothesis, methodology, and sample

Financial performance of Climate Change Champions

Climate Change Champions do achieve their economic goal of growing shareholder wealth by maximizing the present value of future cash flows. Environmentally responsible investments into renewable power can maximize cash flows by the cheaper investment into efficient assets, which lower the costs of producing energy. For example, the cost of producing electricity through solar panels is cheaper than coal plants. Indeed, International Renewable Energy Agency (The International Renewable Energy Agency, 2020) reports that renewable power is increasingly cheaper than fossil fuels in producing electricity. This report highlights that:

New renewable power generation projects now increasingly undercut existing coal-fired plants. On average, new solar photovoltaic (PV) and onshore wind power cost less than keeping many existing coal plants in operation, and auction results show this trend accelerating—reinforcing the case to phase-out coal entirely.

Renewable project investments can maximize firm value by lowering costs by reducing waste and regulatory fines. On the revenue side of cash flows, these renewable energy firms increase market power by appealing to socially conscious buyers. For some time, consumer preferences have been driving the growth of socially responsible investing (Wallis and Klein, 2015). Thus, renewable energy firms create value by getting lower finance costs by again appealing to socially conscious investors (Mackey et al., 2007). The overall benefits of sustainable business are the firm’s better alignment with society’s expectations, regulations and realizing new revenue from innovative products and untapped markets.

Few studies examine the impacts of UNGC membership on financial performance. Coulmont and Berthelot (2015) find that UNGC firms listed on the Paris Stock Exchange show improved market to book value and earnings financial performance. Ortas et al. (2015) show that UNGC firms in France and Spain have a positive relationship between their ESG (environmental, social, governance) performance and five-year financial performance (using yearly ROA and Tobin’s Q). Again, few studies examine the financial impact of changes in climate change policy made by firms. Gallego-Alvarez et al. (2015a, 2015b) and Delmas et al. (2015) find that firms who have reduced their greenhouse gas emissions, realize positive ROE and ROA financial performance in the long term.

In sum, UNGC Climate Change Champions can prove the theoretical benefits of pro-environmental industries with renewable power technologies. Empirical studies on UNGC firms’ financial performance and studies on socially responsible firms and environmentally friendly firms support positive financial performance. Therefore, we propose that UNGC Climate Change Champions perform comparably with their competitors who do not join UNGC in this hypothesis:

H1: UNGC-CCC firms have no difference in financial operating performance compared to their non-UNGC competitors.

Do Climate Change Champions reward their investors?

Fama and French (2007) explain in “Disagreement, tastes, and asset pricing” that investors are like consumers. Their consumer tastes (for example, socially responsible investing) and their disagreement over payoffs are valid factors of asset pricing and firm performance. Indeed, empirically Ng and Zheng (2018) affirm this theory. They show that investors’ “tastes” and the payoff uncertainty of green energy investments have asset pricing effects. Green energy portfolios perform comparably or better than a matching non-green portfolio and the industry S&P 500 Energy benchmark in the last 24 years. Investors are rewarded with sound financial performance to pursue environmentally responsible objectives because there are significantly positive alphas in green firms.

This theory of disagreement, tastes and asset pricing suitably applies to UNGC Climate Change Champions. By virtue of their cause to fight climate change, these firms exemplify the consumer taste of environmentalism to investors. Moreover, Climate Change Champions can have a higher disagreement over return payoffs because these firms are tackling the new climate policy initiative, which comes with higher risk than their conventional competitors. Therefore, this theory implies that they can have comparable value with their non-UNGC competitors.

Given our theoretical explanation that investor’s taste in fighting climate change and higher disagreement in payoffs, as well as supportive empirical studies, we hypothesize Climate Change Champions have comparable investment performance with non-UNGC competitors.

H2: UNGC-CCC firms have no difference in abnormal return performance than their matched non-UNGC competitors.

We further examine whether being a UNGC member could explain investment performance because this membership strongly signals the firm’s social responsibility orientation to the financial markets. Thus, we propose:

H3: UNGC-CCC membership affects long-term abnormal return performance after controlling for the firms’ financial, governance, region, and governance factors.

Our study is a modified portfolio study that uses an event study approach. Here, we use the UNGC joining year as a reference year to line up comparable performance over time to: (1) to study the long-term effects of UNGC on performance; (2) to discern when a firm changed from a conventional non-UNGC firm to a UNGC firm, and (3) to compare our UNGC-CCC sample against a control sample of matched competitors, which remained as non-UNGC firms with a matching time frame. This approach allows us to isolate the effect of joining UNGC from UNGC membership itself.

Our modified portfolio approach to study performance of UNGC firms using panel regression tests is done over the long term of 15 years. As a long-term study, we do not expect other firm-specific events to impact our results because our UNGC (133 firms) and competitor portfolios are relatively diversified by country and industry. Second, portfolio studies are marginally concerned with firm-specific events. Third, both portfolios have the same time windows whose yearly performance is matched up by the year of joining to control for the effects after a firm has joined UNGC and not before. Therefore, business cycle conditions are the same for both the UNGC-CCC and its competitor portfolio. This conditional model is expressed as follows in Eq. (1) below:

Our main variable of interest is the UNGC-CCC member, a binary identification variable. One represents that the firm is a UNGC-CCC member each year, and 0 represents a non-UNGC member or its competitor. The variables above are explained and defined in Table 1.

Second, this research design allows us to compare performance between the UNGC portfolio and its non-UNGC competitor counterpart using a difference in difference panel regression analysis. Hence, our approach works to study these questions:

-

1.

Does UNGC membership have any effect on CARs?

-

2.

Does the effect on CARs occur after joining UNGC?

-

3.

Is there a difference in portfolio performance between UNGC versus its competitor portfolio?

Here, we include a variable, AFTER PARTICIPATION DATE, which is zero before a company joins UNGC and one after, and its interaction with the UNGC membership variable, UNGC OR COMPETITOR. This interaction term is labeled: DIFF AND DIFF. The AFTER PARTICIPATION DATE dummy variable is the same for a UNGC company’s competitor. This model specification isolates for the effect on long term performance arising from the decision to join UNGC from the impact of UNGC membership itself. This regression model is specified in Eq. (2) below:

We collected our firms from the year 2000 because this is the earliest year a firm can join UNGC. The UNGC was launched officially at the United Nations headquarters in New York city on July 26th, 2000. 2015 is the latest data in which we were able to collect at the onset of our study. All financial data, including these variables, are obtained from (Capital IQ, 2015–2021) published by Standard and Poors. We collected the population of UNGC firms from the United Nations Global Compact website (www.unglobalcompact.org/participants). The UNGC website provides a list of all organizations, including publicly traded corporations, as well as: date of membership, industry, country, and active status.

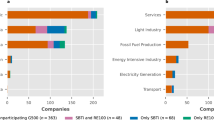

Table 2 presents distribution by country and industry (Standard Industrial Classification) of our Climate Change Champion firms. There are 117 unique publicly traded UNGC firms in the climate change initiative. Of these firms, 115 are active, and two are inactive. The majority of firms (60 firms) are in Europe and Asia/Pacific, having the second-highest (34 firms). The United States and Canada have 14 Climate Change Champion members; Africa and the Middle East have 5; lastly, Latin America and Caribbean countries have only two members. Climate Change Champion firms come from ten industrial sectors including: consumer discretionary, consumer staples, energy, financials, healthcare, industrials, information technology, materials, real estate and utilities.

The competitor firms used in our study are non-UNGC publicly listed companies from the same five regions. (Capital IQ, 2015–2021) identifies competitors through self-reported surveys by company, competitor, and third-party firms, as well as similarities in finances and operations. We collected a matched competitor firm sample from (Capital IQ, 2015–2021). The first listed competitor was selected from the list of competitors provided for each UNGC firm. The sample size of UNGC firms falls to 54 firms after accounting for UNGC CCC firms that have got competitors on a one-to-one match basis. Our matching efforts are working. We compare the characteristics of UNGC-CCC firms and their competitors (explanatory variables descriptive statistics—table is available upon request). Most of these variables are quantitatively similar between UNGC firms and their competitors, which attest to our matched sample’s validity. However, we note a few differences. UNGC-CCCs have a larger percentage of external directors (81 percent) compared to their competitor’s (23 percent). Also, UNGC-CCCs have greater leverage, larger debt to equity ratios (66 versus 54%) and higher profit (gross margins are 41% compared to 29%) than their competitors.

Dependent variable: performance

We perform the above panel regression models to see UNGC-CCC effects on financial performance using Cumulative Abnormal Returns (CAR) as the dependant variable. We collect monthly share price data from (Capital IQ, 2015–2021) to get monthly returns adjusted for dividends. We start our monthly share price data five years (60 months) before the year 2000, in which the first firms join the UNGC. The share price data is collected through December 2015.

We used four different asset pricing models to estimate CAR using CAPM, Fama French 3 factor, and Fama French 5 (2016) and operating performance ROA. For each firm, we determine an estimation period starting at −60 months and ends at −24 months relative to the UNGC joining date (t = 0) to estimate alphas and betas, and then use a rolling 36-month estimation window. The event period starts 24 months before the event month (t = 0) and ends 36 months after. Also, we calculate abnormal returns for up to 120 months after inception to see if there is a reversion to the mean or eventual recovery of the stock value. We use the value-weighted MSCI World Index as the market return benchmark.

We also employ three models for measuring relative returns over time. That is, using the UNGC membership joining date as the event of interest, we measure performance using event time relative to UNGC joining year, event time in blocks, and lastly, calendar time. With calendar time, we measure the abnormal return performance of UNGC firms and their competitors regardless of the UNGC membership joining event date. We calculate abnormal returns in relative time 24 months before a firm joins UNGC and 60 months after. Here, we can see how joining UNGC-CCC has effects both in short-and long-term performance. Calendar time returns are calculated from the time the firm joins the UNGC Climate Change Champion initiative from 2000 to December 2015. As firms join the initiative, they are added to this portfolio, and their risk-adjusted performance is compiled.

Following Brown and Warner (1980), the normal return is defined as the expected return without conditioning on the events taking place. For firm i and event date t the abnormal return is

where ARiτ, Riτ, and \(E\left( {R_{i\tau }\left| {X_{i\tau }} \right.} \right)\) are the abnormal, actual, and expected returns, respectively, for time τ. The abnormal return observations are aggregated into an equally weighted portfolio to draw overall inferences for the event of interest (Bernard, 1987). The abnormal return for the portfolio will be

The expected return on the firm is determined by regressing the excess firm return on the excess market risk premium and estimating the parameters:

for CAPM, and

for the Fama-French three-factor model where SMB and HML are factors for firm size and book-to-market value of equity, respectively, are obtained from Fama and French Global Factors in Kenneth French’s data library: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html. The abnormal return compares the return on the firm with the expected return given these parameters:

for the CAPM, and

for the Fama-French three-factor model. The Cumulative Abnormal Return for the portfolio is:

Lastly, we employ the latest asset pricing model, the Fama and French (2016) five-factor model. This model includes two additional factors: RMW (Robust Minus Weak) and CMA (Conservative Minus Aggressive).

We employ the following test statistics for the event period [t1,t2] to test the null hypothesis, H0: CAAR = 0, where (CAAR) is the computed cross-sectional average of a firm’s CAR.

Results

Operating performance: Climate Change Champions and Competitors

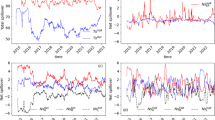

We compare the financial operating performance of UNGC Climate Change Champions (green line) against their non-UNGC competitors (red line) relative to the year of joining UNGC (Year 0), as shown in Fig. 1. This figure shows the mean and median financial performance in the relative time of joining UNGC (from year −3 to year +5) using two measures, Return on Assets (ROA) and Return on Capital (ROC). Clearly, the graph shows that Climate Change Champions have greater ROC and ROA performance (the lines are higher) versus their competitors. Also, their performance is less volatile or risky than their competitors.

Operating performance is the annual return on capital ROC, and the return on assets, ROA.

Table 3 presents our comparative analyses of financial operating performance between Climate Change Champions and their matched competitors. We present long-term performance results in relative time (−3 to +5 years) to joining UNGC in the top section of the table. Here, we discuss the results based on mean values. Median values are shown in the table but not discussed for brevity unless there are significant differences in the results for the median values. We show that UNGC-CCC firms have a 4.87% ROA, which is significantly (p < 0.01) greater than their non-UNGC firms’ 2.34% ROA by +2.53%. Moreover, UNGC-CCC firms have a ROC (8.13%), which is significantly (p < 0.01) greater than their non-UNGC firms’ ROC (4.09%) by 4.04 percentage points. However, looking at Gross Margins, UNGC-CCC firms have Return on Sales (ROS) (33.20%), which is significantly (p < 0.01) lower than their competitors’ ROS (40.43%) by −7.24 percentage points. In addition, market performance is presented here using the return premium (stock return less the risk free rate) and the Sharpe Ratio (which is used for comparing investment return to risk performance of undiversified portfolios). Here, UNGC-CCC firms have a mean Risk Premium (13.63%), which is significantly (p < 0.05) lower than their competitors’ risk premium (22.09%) by −8.46 percentage points. However, the Sharpe Ratio for UNGC-CCC firms is practically the same as their competitors (0.282 versus 0.289). This Sharpe ratio finding demonstrates that there is no real investment performance difference between them after accounting for their market risk.

Second, the middle panel of Table 3 shows performance in calendar time for the entire period of 16 years. Here, we show that UNGC-CCC firms have a 3.14% ROA, which is significantly (p < 0.05) greater than their competitors 1.62% ROA by +2.53 percentage points. The ROA median values show no significant difference. Moreover, although there is lower ROC performance (−2.29%) of UNGC-CCC firms, this difference is not statistically significant. UNGC-CCC firms have ROS of 39.68%, which is significantly (p < 0.01) higher than their non-UNGC firms’ ROS (33.37%) by 6.90 percentage points. For market performance, UNGC-CCC firms have a mean risk premium (11.61%), which is not significantly lower (−3.50%) at the (p < 0.05) level than their competitors’ risk premium (15.11%). However, the Sharpe Ratio for UNGC-CCC firms is higher than their competitors (0.236 versus 0.220).

In sum, we show that Climate Change Champions perform better on accounting returns (ROA and ROC) than their non-UNGC competitors. Renneboog et al. (2008) reports that across the existing studies, CSR is positively related to financial performance. Moreover, Renneboog et al. (2008) notes that CSR seems more highly correlated with backward-looking measures of accounting returns.

We expect that Climate Champion firms to have increased capital costs because of the real commitments they must make to comply with their UNGC commitments. Such investment should pay off in lower operating costs, through lower energy consumption and potential savings on litigation, for example. Figure 2 confirms this: operating expense ratio shows decreasing trends. Table 3 Panel B presents the standard statistics of their Operating Expense to Sales ratio around the time they join UNGC. The decrease in operating costs (−0.01) is significant (p < 0.01) between years −3 to 0 and similarly between years −3 to year +3 as well. These falling costs are meaningful. Therefore, becoming a Climate Champion member is associated with lower operating costs. These results suggest that Climate Champion firms have committed to real changes in operations and in their strategy. Thus, our evidence counters the “fake CSR” or “green-washing” criticism in the literature.

This figure shows that the operating expense ratio shows a decreasing trend.

Market return performance

We present the investment performance of Climate Champion firms and their matched competitors using Fama-French 5-factor risk adjusted cumulative abnormal returns (CARs) plotted over time. Figure 3 shows the UNGC performance (green line) against its competitors (dashed gray line), which are matched based on Capital IQ’s (Capital IQ, 2015–2021) standard criteria. Climate Change Champions show positive CARs 24 months before joining, with a peak return of about ten percent. Ten to 36 months after joining UNGC, CAR performance falls to about five percent. Thereafter, positive abnormal returns remain for four years. After 60 months from joining UNGC, performance diminishes to −6.0 percent. Overall, there appears to be diminishing abnormal returns after joining UNGC.

Investment performance measured as Cumulative Abnormal Returns (CARs) are presented 24 months before and 60 months after joining UNGC.

Table 4 presents Fama-French 5-factor risk adjusted CARs for UNGC-CCCs firms matched one to one with their non-UNGC competitors in relative time on the left and calendar time on the right. After joining UNGC, Climate Champion firms show neither significant positive CARs (about 7 percent at month zero) nor show significant negative CARs, (about −6 percent at +60 months). Similarly, their competitors also show non-significant CARs, ranging from −2 to 12.6 percent. Thus, Climate Change Champions do not suffer abnormal losses or gains compared with their competitors on a risk adjusted basis. Indeed, both groups of firms are earning their appropriate risk-adjusted returns. The calendar time (right side of the panel) portfolio shows non-significant losses of up to −32 percent at 84 months (7 years). Climate Champion firms appear to earn appropriate risk-adjusted returns performing on par with their non-UNGC competitors.

UNGC-CCC conditional results

We test our hypothesis conditionally on whether UNGC membership affects firm performance. Table 5 presents panel regression results using four asset pricing models for Climate Champion firms and their non-UNGC competitors for the aggregate sample. Here we show that UNGC membership has non-significant effects of +0.091 using the Capital Asset Pricing Model. With the Fama-French 3 factor model, there is a non-significant effect of −0.054 on risk adjusted stock performance. The Fama-French 5 factor results show that being a UNGC-CCC member does not have a significant effect (−0.250) on risk adjusted returns. UNGC also has no significant effect on an operating performance measure, ROA, at −2.636.

We further test this conclusion more robustly in Table 6. This time, we perform the same conditional analyses on a one-to-one matched sample of UNGC-CCC firms and their competitors. UNGC-CCC firms do not suffer any negative performance after controlling for firm characteristics, governance, region factors using the same four estimation models (CAPM, FFM 3, FFM 5, and ROA). Our robustness testing affirms the same conclusion that UNGC membership in itself has no negative effect on performance.

We offer deeper conditional testing of same hypothesis on whether UNGC membership affects firm performance in Table 5. We find again that UNGC membership has non-significant effects in calendar time and relative time models. We have controlled for sample bias selection for firms before they join UNGC from their non-UNGC competitors. Interestingly, after controlling for UNGC membership, we find that after a firm joins UNGC, there is a positive effect on portfolio performance. AFTER PARTICIPATION shows a significant (p < 0.01) and positive effect on abnormal returns of 23.6 to 35.4 percent in 15 years after joining UNGC. Hence, there is a causal effect over and above UNGC membership. Renneboog et al. (2011) highlight another issue in asset pricing; there is no convincing evidence on the direction of causality over CSR’s relations with higher shareholder value. We find that after joining UNGC, there is a significantly positive relationship with portfolio performance. Therefore, we show evidence on the direction of causality between UNGC-CCC and higher shareholder value.

Intriguingly, the DIFF AND DIFF variable (difference in difference) shows a significant (p < 0.01) and negative effect on abnormal returns. This finding indicates that after joining UNGC, Climate Change Champions significantly underperformed against their non-UNGC competitors by 16.8 to 37.4 percent (−1.10 to −2.35% per year). We did not expect to find UNGC-CCC portfolio underperformance against their competitor portfolio. This puzzling result suggests that there is mis-pricing of the UNGC portfolio. Indeed, Derwall et al. (2019) are puzzled by their results of finding superior risk-returns on their eco-efficient portfolio. They explain “the fact that common risk factors fail to account fully for the observed results raises the possibility of a mispricing story.”

Discussion

Renneboog et al. (2008) conclude from the SRI literature that among the great issues and puzzles to be solved is asset pricing. The question is whether CSR is incorporated in their share prices.

We can explain why this asset mispricing puzzle exists in the SRI literature with Fama and French’s (2007) theory on disagreement and tastes on asset pricing. Here, disagreement and tastes are incorporated into share prices. Standard asset pricing models assume that: (i) there is complete agreement among investors about probability distributions of future payoffs on assets; and (ii) investors choose asset holdings based solely on anticipated payoffs; that is, investment assets are not also consumption goods. Both assumptions are unrealistic. Indeed, these two assumptions are equally unrealistic for UNGC-CCC firms. Investors in UNGC-CCC firms are unlikely to have complete agreement about distributions of future payoffs on assets. These firms are the first to adopt a global standard of CSR that is best in practice with unknown payoffs. Second, UNGC-CCC investors are unlikely to invest based solely on anticipated payoffs. Rather, they chose to invest in UNGC-CCC as consumption goods because they see value in them as “Climate Change Champions.” Therefore, we deduce from this theory that there would be mis-pricing of UNGC firms. We find under-pricing of our UNGC-CCC portfolio because standard asset pricing models ignores investor behavior of disagreement over payoffs and tastes. The good news is that the Popular Asset Pricing model, recently developed by Idzorek, Kapan and Ibbotson (2020), address this mispricing by including disagreement and tastes into asset pricing.

Lastly, Renneboog et al. (2008) point to an important implication that SRI has for asset pricing:

For example, if investors exhibit preferences of “aversion to unethical/asocial corporate behavior” in addition to the standard risk aversion, investors may require a lower rate of return from ethical firms than that suggested by the standard asset pricing models. However, the existing studies at the portfolio level hint but do not univocally demonstrate that SRI investment funds perform worse than conventional funds…. Further research remains to be conducted to investigate the anomaly.

Investors of Climate Change Champions are likely to have preferences of aversion to unethical/asocial behavior of fossil fuel related firms in the non-UNGC competitor portfolio. These preferences of aversion in addition to the standard risk aversion, implies that investors would require a lower rate of return from UNGC-CCC firms than that suggested by standard asset pricing models. Indeed, we show that UNGC-CCC portfolio performs worse than its competitors by up to 2%. Investors are willing to accept lower returns from UNGC-CCC firms than their conventional competitors. This conclusion is in-line with our result for UNGC firms in which the Sharpe ratio is lower than the non-UNGC portfolio because the UNGC portfolio has lower risk with lower returns. Thus, our contribution to the SRI literature is finding mispricing of fourth generation SRI screened firms.

Conclusion

Firms join the United Nations Global Compact for economic and ethical reasons (Cetindamar and Husoy, 2007). Whether it is beneficial for a firm to commit to a universal code of ethics and social responsibility is a vital question for the UNGC and the global business community. As an implication to renewable energy, UNGC-CCC are corporate leaders who support renewable energy, production and consumption, which implies a positive relationship to sustainable economic growth as Gozgor (2018) concluded. Moreover, UNGC Climate Change Champions have “best in practice” in corporate social responsibility who are improving institutional quality of the corporation, improving human capital and improving skill, and R&D expenditures. These CSR improvements contributes to economic complexity, which Gozgor (2018) found to positively relate to sustainable economic growth.

Renewable energy consumption can have a unit root process as found in Brazil or a stationary process as found in China and India (Gozgor, 2016). A unit root process implies that policy implications will persistently affect renewable energy use. That permanent policy changes such as renewable portfolio standard will be a more appropriate tool versus “temporary policy stances” such as tax or investment incentive. UNGC Climate Change Champions represent a renewable portfolio standard; therefore, they would have positive persistent effects on renewable energy consumption in some of the countries where our firms come from.

Our study is a first study of portfolio performance of a fourth generation SRI screening strategy of United Nations Global Compact firms who are Climate Change Champions. The operational changes made by UNGC firms are real as we have shown substantial changes in financial operating performance. This disproves the notion that UNGC firms are merely green-washing.

We find that after firms join UNGC, there is a positive effect on long term portfolio performance, but not before joining. Firms that join the UNGC have lower volatility and so less risk versus their competitors. There appears to be mispricing of lower risk in market returns because standard asset pricing models may not be pricing investors’ aversion to climate change risk and preference for firms actively combating climate change. Fama and Frenchs’ theory (2007) says that these “tastes” are valid factors to provide a more complete asset pricing model. The Popular Asset Pricing model (Idzorek et al., 2020) can resolve this puzzle because it includes both disagreement and tastes into the CAPM. Our study encourages investors to invest in UNGC-CCC firms as we find there is no penalty of underperformance against a conventional portfolio because the lower return reflects lower risk.

Ultimately, whether firms should adopt climate change policy will depend on the moral force of the argument that firms have the imperative to save the planet from the impending threat of climate change. More firms should consider joining UNGC, especially fossil fuel-related firms facing divestment. Becoming a UNGC-CCC can improve their financial performance and their ability to grow their shareholder value. We hope our study contributes to this moral force by showing that doing good for climate change and society is neither costly nor penalizing returns for Climate Change Champions. They earn normal risk-adjusted returns, which is what investors rationally and normally want.

Data availability

The datasets generated during and/or analyzed during the current study are not publicly available due as they are based on proprietary data provided under subscription by S&P Capital IQ but are available from the corresponding author on reasonable request.

Change history

14 January 2022

A Correction to this paper has been published: https://doi.org/10.1057/s41599-022-01033-7

References

Benson KL, Humphrey JE (2008) Socially responsible investment funds: Investor reaction to current and past returns. J Bank Finan 32(9):1850–1859. https://doi.org/10.1016/j.jbankfin.2007.12.013

Bernard VL (1987) Cross-sectional dependence and problems in inference in market-based accounting research. J Account Res 25(1):1–10. https://doi.org/10.2307/2491257

Brown SJ, Warner JB (1980) Measuring security price performance. J Finan Econ 8:205–258

Capital IQ (2015-2021) Capital IQ: A division of S&P Global Market Intelligence, LLC. Retrieved from http://www.capitaliq.com/

Cetindamar D, Husoy K (2007) Corporate social responsibility pratices and environmentally responsible behavior: the case of The United Nations Global Compact. J Bus Ethics 76:163–176. https://doi.org/10.1007/s10051-006-9265-4

Cetindamar D, Husoy B (2007) Corporate social responsibility practices and environmentally responsible behaviour: the case of the United Nations Global Compact. J Bus Ethics 163–176. https://doi.org/10.1007/s10551-006-9265-4

Coulmont M, Berthelot S (2015) The financial benefits of a firm’s affiliation with the UN Global Compact. Bus Ethics: Eur Rev 24:150–155.

Covington H, Thamotheram R (2014) How should investors manage climate-change risk? Rotman Int J Pension Manag 7(2):42–47. https://doi.org/10.3138/ripjm.7.2.42.

Delmas MA, Nairn-Birch N, Lim J (2015) Dynamics of environmental and financial performance_the case of greenhouse gas emissions. Organ Environ 28:374–393. https://doi.org/10.1177/1086026615620238.

Derwall J, Guenster N, Bauer R, Koedijk K (2019) The eco-efficiency premium puzzle. Financ Anal J 61(2):51–63. https://doi.org/10.2469/faj.v61.n2.2716

Dordi T, Weber O (2019) The impact of divestment announcements on the share price of fossil fuel stocks. Sustainability 11(11):3122. https://doi.org/10.3390/su11113122

Fama EF, French KR (1992) The cross-section of expected stock returns. J Financ 47(2):427. https://doi.org/10.2307/2329112

Fama EF, French KR (2015) (2016) Dissecting anomalies with a Five-Factor Model. Rev Financ Stud 29(1):69–103. https://doi.org/10.1093/rfs/hhv043

Fama EF, French KR (2007) Disagreement tastes and asset prices. J Financ Econ 83(3):667–689. https://doi.org/10.1016/j.jfineco.2006.01.003

Flammer C (2013) Corporate social responsibility and shareholder reaction: the environmental awareness of investors. Acad Manag J 56(3):758–781.

Gallego-Alvarez I, Segura L, Martinez-Ferrero J (2015) Carbon emission reduction: the impact on the financial and operational performance of international companies. J Clean Prod 103:149–159

Gallego-Alvarez I, Garcia-Sanchez I, da Silva Viera C (2014) Climate change and financial performance in times of crisis. Bus strateg Environ 361–374. https://doi.org/10.1002/bse.1786.

Gozgor G (2016) Are shocks to renewable energy consumption permanent or transitory? An empirical investigation for Brazil China and India. Renew Sustain Energy Rev 66:913–919. https://doi.org/10.1016/j.rser.2016.08.055

Gozgor G (2018) A new approach to the renewable energy-growth nexus: evidence from the USA. Environ Sci Pollut Res 25(17):16590–16600. https://doi.org/10.1007/s11356-018-1858-9

Guide to Corporate Sustainability | UN Global Compact. (n.d.) Retrieved November 24, 2021, from https://www.unglobalcompact.org/library/1151

Henriques I, Sadorsky P (2018) Investor implications of divesting from fossil fuels. Global Financ J 3830–3844. https://doi.org/10.1016/j.gfj.2017.10.004

Idzorek TM, Kaplan PD, Ibbotson RG (2021) The PAPM with Heterogeneous Preferences and Expectations. SSRN Electronic J. https://doi.org/10.2139/ssrn.3451554

Lee K-H, Min B, Yook K-H(2015) The impacts of carbon (CO2) emissions and environmental research and development (R&D) investment on firm performance. Int J Prod Econ 167:1–11

Lee S-Y, Park YS, Klassen RD (2013) Market responses to firms’ voluntary climate change information disclosure and carbon communication. Corp Soc Responsib Environ Manag 22:1–12. https://doi.org/10.1002/csr.1321.

Liesen A (2014) Climate change and financial market efficiency. Bus Soc 54:511–539. https://doi.org/10.1177/0007650314558392.

Mackey A, Tyson BM, Jay BB (2007) Corporate social responsibility and firm performance: Investor preference and corporate strategies. Acad Manag Rev 32(3):817–35. https://doi.org/10.5465/AMR.2007.25275676.

Ng A, Zheng D (2018) Let’s agree to disagree! On payoffs and green tastes in green energy investments. Energy Econ 69:155–169. https://doi.org/10.1016/j.eneco.2017.10.023

Nikolaou I, Evangelinos K, Filho WL (2015) A system dynamic approach for exploring the effects of climate change risks on firms’ economic performance. J Clean Prod 103:499–506.

Ortas E, Alvarez I, Garayar A (2015) The environmental, social, governance and financial performance effects on companies that adopt the United Nations Global Compact. Sustainability 1932–1956. https://doi.org/10.3390/su7021932.

Peifer J (2014) Fund loyalty among socially responsible investors: The importance of economic and ethical domains. J Bus Ethics 121(4):635–49. https://doi.org/10.1007/s10551-013-1746-7.

Plantinga A, Scholtens B (2021) The financial impact of fossil fuel divestment. Clim Polic 21(1):107–119. https://doi.org/10.1080/14693062.2020.1806020

Rasche A, Wwaddock S, McIntosh M (2012) The United Nations Global Compact: restrospect and prospect. Bus Soc 51(I):6–30. https://doi.org/10.1177/0007650312459999.

Renneboog L, Horst JT, Zhang C (2008) Socially responsible investments: Institutional aspects performance and investor behavior. J Bank Financ 32:1723–1742. https://doi.org/10.1016/j.jbankfin.2007.12.039

Renneboog L, Horst JT, Zhang C (2011) Is ethical money financiall smart? Nonfinancial attributes and money flows of socially responsible investment funds. J Finan Intermed 20(4):562–88. https://doi.org/10.1016/j.jfi.2010.12.003.

Rivelli C, Viviani J-L (2014) Financial performance of socially responsible investing: what have we learned? A meta-analysis. Bus Ethics: Eur Rev 24(2):159–178

Simon JG, Powers CW, Gunnemann JP (1972) The Ethical Investor: Universities and Corporate Responsibility. Yale University Press

The International Renewable Energy Agency (2020) Retrieved from The International Renewable Energy Agency. https://www.irena.org/newsroom/pressreleases/2020/Jun/Renewables-Increasingly-Beat-Even-Cheapest-Coal-Competitors-on-Cost

Trinks A, Scholtens B, Mulder M, Dam L (2018) Fossil fuel divestment and portfolio performance. Ecol Econ 146:740–748. https://doi.org/10.1016/j.ecolecon.2017.11.036

United Nations Environment Programme (2016) United Nations Environment Programme. Retrieved from https://www.unep.org/.

United Nations Framework Convention on Climate Change (2016) Retrieved from United Nations Climate Change: https://unfccc.int/.

United Nations Global Compact (2013) Global Corporate Sustainability Report 2013. United Nations Global Compact Office, New York, NY

United Nations Global Compact. (2016). Retrieved from https://www.unglobalcompact.org/what-is-gc/mission/principles.

Wallis MV, Klein C (2015) Ethical requirement and financial interest: a literature review on socially responsible investing. Bus Res 8:61–98. https://doi.org/10.1007/s40685-014-0015-7

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The author(s) declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Msiska, M., Ng, A. & Kimmel, R.K. Doing well by doing good with the performance of United Nations Global Compact Climate Change Champions. Humanit Soc Sci Commun 8, 321 (2021). https://doi.org/10.1057/s41599-021-00989-2

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-021-00989-2