Abstract

We describe a framework for understanding the factors that underpin economic resilience, and identify the basic tools for implementing it. This principally involves examining resilience by design, which promotes endogenous reorganization in the economy, and by intervention, which includes exogenous measures such as bailouts, stockpiles and building buffers. We link these ideas to comparable notions from physics, such as the rich and non-trivial phenomenology that arises in circumstances when a system is dynamic and out of equilibrium. We contend that a more nuanced understanding of the underlying structure of our economic system could lead to more enlightened policy decisions that promote resilience and result in better outcomes in the long run.

Similar content being viewed by others

Main

Awarding the 2021 Nobel Prize for physics to two climatologists, Klaus Hasselmann and Syukuro Manabe, and a physicist, Giorgio Parisi, sent an important message to all those concerned about the overall complex system in which we live. We should see the socioeconomic system as one part of the whole planetary system in which the very different components interact with each other and generate aggregate phenomena that could not be predicted from even the most detailed knowledge of the millions of individual parts in isolation.

This might seem to suggest that one cannot say much about the aggregate behaviour of such systems. However, we can hope that recognizable patterns will emerge, even if precise predictions as to what the state of the system will be at any point in time cannot be made. Physicists tend to be most familiar with the argument for emergence put forwards by Philip Anderson in his famous 1972 essay entitled ‘More is different’1, but this notion has also been explored in the economics domain2—a view that was perhaps most succinctly expressed by Friedrich Hayek when he argued3 that “there are no laws in economics, just patterns”.

Nevertheless, the idea that seemingly precise predictions for the behaviour of such complex systems can be made solely on the basis of deterministic models has become prevalent in many disciplines, and in economics we persist with the idea that each crack in the system’s structure can be independently addressed. This issue is especially pressing when it comes to establishing the resilience of economic systems to shocks, because our collective well-being depends on this being effective.

Two complementary approaches

As we have seen over the past two years, the SARS-CoV-2 pandemic exposed the brittleness of the global system and the fragility of the many systems that support the livelihoods of the global population4. To counter the pandemic’s potential to overwhelm public health systems, many socioeconomic activities were curtailed or prohibited, with some sectors suppressed throughout 2020.

Economic recovery has been, and will continue to be, heavily influenced by fiscal policy and central bank activity. Discussions about whether the economy can be brought back to ‘normal’ or structurally transformed to better face existing and future challenges, including climate change and structural inequality, are crucial to the underlying policy debates.

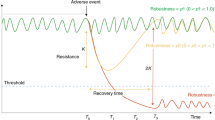

The conceptual answer we have proposed is to strengthen systemic resilience within our economies, by which we mean the capacity of a system to anticipate, absorb, recover from and adapt to a wide array of systemic threats (hereafter referred to as ‘systemic resilience’4. The processes of systemic resilience provide the means to pursue multiple objectives associated with economic output, as well as human and environmental health5.

But how is systemic resilience generated? Fundamentally, the processes are organized in two distinct, yet interrelated, ways. First, the capacity for systemic resilience may be driven by a need to protect the system against an exogenous shock; that is, one that originates outside the system. Resources can be used and transferred between entities, by interventions such as building up stockpiles, transferring resources to people, bailing out firms or building appropriate infrastructure. This approach sees a limited part of the system protecting itself against problems in other parts of the system. An alternative is to have a much broader view of the system as a whole and recognize that it will evolve and modify itself over time, and that the appropriate policy would be to guide or influence that process to achieve our desired goals. This means developing policies that will, by design, lead the system to self-organize itself so as to achieve the required goals.

However, the debate around economic recovery has so far largely focused on achieving resilience through intervention, with sizable capital outflows via government stimulus, such as those to preserve financial liquidity and backstop threatened economic sectors. Such interventions may offer considerable lasting benefits to national and international economic health, but they suffer from two limitations: the cost of intervention may rise above and beyond the political or market capacity or willingness to sustain the debts incurred; and the success of interventionist policies depends on impeccable timing and a precise identification of when and where to intervene. The latter is particularly concerning, as a misplaced financial intervention may yield poor stimulus returns or even inhibit long-term sustainability in job creation, sectoral growth and international trade.

One of the principal problems in trying to act on and improve one component of a complex system is that this will often have unexpected consequences for the rest of the system. And as important as it is, the economy is only one part of the whole system in which we exist. An effective pandemic recovery is therefore predicated not only on promoting systemic resilience in economies, but also on how we are able to promote systemic resilience in underlying subsystems and connected human and environmental systems. In this regard, it is equally important to find the appropriate and achievable balance between systemic resilience by design (RBD) and by intervention (RBI)6,7. Table 1 distinguishes the characteristics of these two types of resilience.

Efficiency of economic systems at equilibrium

Economists tend to conceptualize the macroeconomy on the basis of “equilibrium” thinking, whereby after a disturbance, the system will eventually return to its previous relatively steady state8. One of the basic theorems of welfare economics shows that economic systems are ‘efficient’ at equilibrium, but it is assumed that there is an ‘invisible hand’ (usually interpreted to mean ‘markets’) that brings an economy or market to equilibrium.

However, this is at the heart of a problem widely discussed in physics—out-of-equilibrium states and convergence. Unfortunately, economists have been unable to show, even in the simplest model, that starting from an out-of-equilibrium state, a market or an economy, even with frictions removed, will self-organize into such an efficient state. The effort to do so came to a halt in 1970s with the impossibility results of Sonnenschein9, Mantel10 and Debreu11, The reaction has been simply to assume that the economy was at equilibrium and to propose policies that would make the economy more like the idealized model.

Policies that enhance competition and flexibility are claimed to promote this objective. Efficiency and the global economy’s relatively smooth growth in the past hundred years12 is seen as a testament to the success of these policies. The limited volatility that member countries of the Organisation for Economic Co-operation and Development seem to have experienced from the mid-1980s onwards prompted some to call for an ‘end of economic history’13. This reinforced theories based on the idea that the economy is evolving along a stable path from which it only deviates as a result of technological, demographic and ‘societal’ changes.

Systemic resilience within the context of economic systems is an emerging discourse, but limited studies have examined how low-level market disturbances can escalate into sectoral disruption7,14; thus exogenous shocks are still responsible for the stochastic evolution of the economy, but they occur at the micro level and are amplified by the system. Another view is that the economy exhibits endogenous dynamics, which would cause volatile outputs even without the presence of noise in the system.

The economy can be thought of as a system of interconnected institutions and markets that is continuously correcting itself, but which eventually, but inevitably, reaches a critical state (that is, one in which small perturbations have large consequences for the whole). This may lead to cascade effects and, in the economic context, for example, a broader type of instability that impedes the flows of capital. This is the phenomenon generally defined as ‘self-organizing criticality’, part of the wider framework of critical phenomena and phase transitions. This term was introduced into economics by Bak et al.15 and Scheinkman and Woodford16. Again, the important point here is that the critical states that may occur are rare, but the systems in question tend to self-organize in such a way that they converge to these critical states. Guzman and Stiglitz17 pursued this line of thought and proposed a ‘dynamic disequilibrium’ macro framework based on the premise that “a better way to understand deep downturns is to think of the economy experiencing a constant evolution, marked by uncertainty, in which there is continual learning about the economic system”. In this regard, learning is a form of adaptive behaviour that is both exogenously and endogenously produced by intervention and by design.

Incorporating RBD

During the Great Depression (1929–1930s), the Financial Crisis (2007–2009) and thus far the SARS-CoV-2 Crisis (2019–present), localized catalysts provoked a chain reaction of systemic disruption across the globe, and within many facets of daily life. What had been individual problems led to a systemic collapse. At the onset of each event, the need for financial backstopping became a common problem linking the various disrupted systems together—from manufacturing and industry to employment, health, education and beyond.

When governments allocate vast amounts of capital to preserving everything from household mortgages to payroll and labour, food and utility assistance, and various other core essentials, the intention is to aid a failing system by conferring enough resources not only to stave off systemic collapse, but also to stimulate a more robust recovery—these are examples of RBI, which will certainly be needed to navigate future crises.

However, for RBI to be effective, future economic systems must incorporate RBD. Structuring systems in a manner that promotes their self-organization around post-disruption recovery will ultimately better position the financial system to minimize the resources required to rebuild affected systems, and simultaneously generate greater system stability.

If global society is to strive for RBD in the coming years, the financial system’s core stakeholders must lead the way. In 2015, the report ‘Completing Europe’s Economic and Monetary Union’ authored by the ‘five presidents’ Juncker, Tusk, Dijsselbloem, Draghi and Schulz18 called for a binding convergence process towards more resilient economic structures. The essence of the argument was that economies with ‘better’ structures were better able to withstand shocks. The call for resilience was, in fact, a call to make economies more ‘efficient and flexible’. At the same time, G20 members agreed to implement a range of measures to enhance systemic resilience among their respective economies.

This included facilitating the effective reallocation of labour, promoting labour market inclusion and designing efficient social security systems; promoting productivity growth and entrepreneurship; exercising prudent management of public finances; and reducing vulnerabilities in transactional and information systems. In finance, it included harnessing the benefits of capital flows; enhanced monitoring and surveillance of cross-border risks; addressing excessive external imbalances; and promoting international cooperation on economic policies. Sondermann19 claimed that economies that had facilitated such developments did, in fact, weather shocks better than those with weaker structures. In particular, he argued that rigidities in labour markets, limited competition in product markets, outdated business framework conditions and the quality of government services represent the main obstacles to mitigating shocks. All of this suggests that there was still a belief that removing the impediments to the freedom of action of the individuals and components of the system would automatically enhance its functioning.

Yet, paradoxically, this was in the aftermath of a major financial crisis that, in large part, resulted from moves to make financial markets less constrained and more flexible. The reaction to an internal upheaval caused by a removal of constraints in an important part of the economy was, counterintuitively, to progressively remove more constraints in other parts of the economy and to eliminate what were regarded as ‘frictions’ or ‘imperfections’ that led to ‘market failures’. However, both theory and the evidence from the recent past go against this sort of recommendation and suggest that the measures mentioned by the G20 actually diminish resilience.

Consider two examples. The first concerns labour markets. There has been a steady move towards an expansion of the ‘gig economy’ in which workers are independent contractors who are paid to take on tasks by those who require their services. In many countries, unemployment protection, healthcare cover and other benefits do not apply to these workers. This makes the market extremely flexible, but has left a considerable part of the workforce with precarious incomes and little or no access to financial services. As Weil20 argues, the result has been declining wages, eroding benefits, inadequate health and safety conditions and ever-widening income inequality for society as a whole. This is not evidence of resilience, which involves protecting all the components of a system and not a particular class of individuals. Indeed, the reaction has been, in some countries, to classify such workers as employees and to give them back access to the facilities that they had progressively lost. It would be prudent to understand how and why these frictions emerged before trying to remove them in the name of efficiency.

As a second example, consider financial markets. Their traditional role was to direct the money of those who wished to invest to the most gainful activities. Indicators such as stock market indices were supposed to provide a picture of the general health of the economy. The price of shares in the most productive and profitable activities would rise, while shares in activities that performed less well would stagnate or fall. Yet this is not what we have observed. As Shiller21 noted in his book on ‘rational exuberance’, financial market indices have become more and more detached from the performance of the ‘real economy’. The fact that the stock market has flourished during the pandemic does not mean that the majority of the population has benefited from this evolution.

Applying the best science and economics

The physical sciences provide evidence for the necessity of a by-design conferral of resilience. Systemic capacity for resilience is a recurring theme in complex systems: without the structural and material capacity for recovery and adaptation to disruption, then system collapse is likely to occur over a given period of time. The physical world is fundamentally dynamic, with systems constantly changing and adapting to shifting incentives and constraints. The laws of physics track the conservation of energy and matter through dynamic transitions, and interventions are constrained by the governing laws. In economics, considerations are usually static and financial interventions are often not constrained by any physical reality—especially recently.

Economic systems interact with a range of other systems in a network structure. The SARS-CoV-2 crisis is an illustration of how systems change each other. The 2020 health crisis was made far worse by the 2008 financial crisis, or more precisely, the austerity measures that left many health systems without the basic resources such as protective clothing needed to cope with a sudden, unexpected upsurge in the number of patients7. As socioeconomic activity waned following government orders for quarantine and self-isolation, systemic disruption spread beyond the public health domain and into economics and finance, and even the broader political systems of various states. The loss of functionality triggered by this single disruption requires robust recovery to minimize extensive and even permanent multisystem losses, but ensuring recovery in the economic system will be insufficient to help address a range of existing problems that were exacerbated by the COVID-19 crisis.

Resilience begins with understanding individuals and how the ways in which economies try to reallocate resources after shocks affect workers and citizens. Data from the World Health Organization (WHO) show how the pandemic provoked high levels of stress and anxiety owing to lockdowns, quarantines, loss of routine and loss of employment. Drug and alcohol abuse and gender-based violence have risen in lockstep with unemployment and lockdowns. Psychological resilience is key to absorbing and adapting to social and economic shocks. A McKinsey report confirmed how investing in public health is required to accelerate post-COVID-19 economic recovery22, while Smith et al.23 stated that investments in brain health and brain skills are critical for post-COVID-19 economic recovery and long-term economic resilience.

To return to the problem of climate change and its socioeconomic consequences, we have to focus on the whole system. Although we see the effects of global warming on the various components of the system and human activity in different areas of the world, these cannot be treated in isolation. The work of this year’s Nobel laureates in physics emphasizes the impact of the interlocking structure of the whole system. Ignoring the effects of the modifications to the climate system on different areas of the globe and the resultant dramatic effects on the populations of those areas explains why economists’ estimates of the damage involved are so much lower than those of climate scientists. Flooding following on from prolonged heatwaves and drought, and migration as a result of food shortages, are examples of the way in which the system as a whole is changing. Although precise predictions of the consequences of these changes are impossible, nevertheless certain patterns emerge and can be used to guide interventions to improve the resilience of the socioeconomic system.

Perhaps the greatest weakness of the models used by economists to evaluate the cost of phenomena such as climate warming has been the underestimation of the interdependence of the components of our systems and the networks that they form. As one of us said during the financial crisis24: “seizures in the electricity grid, degradation of eco-systems, the spread of epidemics and the disintegration of the financial system, each is essentially a different branch of the same network family tree”. Recent events have reinforced the necessity of emphasizing the network structure of our systems.

Conclusion

How then can such an interdependent set of networks be made more resilient to endogenous upheavals resulting from the system’s tendency to self-organize into a critical state, as well as disruptions from those parts of the system over which we have only limited or no control? RBD and RBI must be undertaken simultaneously, using resilience analysis to drive implementation design and estimate the efficiency/resilience trade-offs. Resilience analysis can be used to stress test network and system intricacies, complexities and interdependencies to evaluate necessary corrective actions, regulations and policy to prevent degradation of critical function post-disruption.

RBD and RBI, can, if implemented properly, enable internal and external actors to incorporate resilience into economic systems without compromising long-term efficiency or other economic goals25. But this will mean changing from a myopic fixation on extracting the maximum from each part of the system in the short term, developing a better understanding of the structure of the underlying links in the system and exploiting its capacity for self-organization to make it more resilient.

References

Anderson, P. W. More is different. Science 177, 393–396 (1972).

Föllmer, H. Random economies with many interacting agents. J. Math. Econ. 1, 51–62 (1974).

Kirman, A. in OECD Complexity and Policymaking (OECD, 2016).

Linkov, I., Keenan, J. & Trump, B. D. COVID-19: Systemic Risk and Resilience (Springer, 2021).

Trump, B. T., Hynes, W. & Linkov, I. Combine efficiency and resilience in post-COVID societies. Nature 588, 220 (2020).

Linkov, I., Trump, B. D., Golan, M. & Keisler, J. Enhancing resilience in post-COVID societies: by design or by intervention? Environ. Sci. Technol. 55, 4202–4204 (2021).

Kott, A. S., Golan, M. S., Trump, B. D. & Linkov, I. Cyber resilience: by design or by intervention? Computer 54, 112–117 (2021).

Simmie, J. & Martin, R. The economic resilience of regions: towards an evolutionary approach. Camb. J. Reg. Econ. Soc. 3, 27–43 (2010).

Sonnenschein, H. Market excess demand functions. Econometrica 40, 549–563 (1972).

Mantel, R. On the characterisation of aggregate excess demand. J. Econ. Theory 7, 348–353 (1974).

Debreu, G. Excess demand functions. J. Math. Econ. 1, 15–23 (1974).

Beaudry, P., Galizia, D. & Portier, F. Reviving the Limit Cycle View of Macroeconomic Fluctuations (NBER, 2015).

Portier, F. The instability of market economies. Rev. OFCE 157, 225–233 (2018).

Gabaix, X. The granular origins of aggregate fluctuations. Econometrica 79, 733–772 (2011).

Bak, P., Chen, K., Scheinkman, J. & Woodford, M. Aggregate fluctuations from independent sectoral shocks: self-organized criticality in a model of production and inventory dynamics. Ric. Econ. 47, 3–30 (1993).

Scheinkman, J. & Woodford, M. Self-organised criticality and economic fluctuations. Am. Econ. Rev. 84, 417–421 (1994).

Guzman, M. & Stiglitz, J. E. Towards a Dynamic Disequilibrium Theory with Randomness Working Paper No. w27453 (NBER, 2020).

Juncker, J.-C., Tusk, D., Dijsselbloem, J., Draghi, M. & Schulz, M. The Five Presidents’ Report: Completing Europe’s Economic and Monetary Union (European Commission, 2015); https://ec.europa.eu/info/publications/five-presidents-report-completing-europes-economic-and-monetary-union_en

Sondermann, D. Towards more resilient economies: the role of well-functioning economic structures. J. Policy Model. 40, 97–117 (2018).

Weil, D. The Fissured Workplace (Harvard Univ. Press, 2017).

Shiller, R. Irrational Exuberance (Princeton Univ. Press, 2000).

Pfeffer, J. & Williams, L. Mental health in the workplace: the coming revolution. McKinsey Quarterly (8 December 2020); https://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/mental-health-in-the-workplace-the-coming-revolution

Smith, E. et al. A brain capital grand strategy: toward economic re-imagination. Mol. Psychiatr. 26, 3–22 (2021).

Haldane, A. Rethinking the Financial Network (2009).

Hynes, W., Trump, B., Love, P. & Linkov, I. Bouncing forward: a resilience approach to dealing with COVID-19 and future systemic shocks. Environ. Syst. Decis. 25, 1–11 (2020).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Hynes, W., Trump, B.D., Kirman, A. et al. Systemic resilience in economics. Nat. Phys. 18, 381–384 (2022). https://doi.org/10.1038/s41567-022-01581-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41567-022-01581-4

This article is cited by

-

An index of static resilience in interindustry economics

Journal of Economic Structures (2024)

-

Resilience and lessons learned from COVID-19 emergency response

Environment Systems and Decisions (2022)