Abstract

Research has made clear that neighbourhood conditions affect racial inequality. We examine how living in minority neighbourhoods affects ease of access to conventional banks versus alternative financial institutions (AFIs) such as check cashers and payday lenders, which some have called predatory. Based on more than 6 million queries, we compute the difference in the time required to walk, drive or take public transport to the nearest bank versus AFI from the middle of every block in each of 19 of the largest cities in the United States. The results suggest that race is strikingly more important than class: even after numerous conditions are accounted for, the AFI is more often closer than the bank in low-poverty racial/ethnic minority neighbourhoods than in high-poverty white ones. Results are driven not by the absence of banks but by the prevalence of AFIs in minority areas. Gaps appear too large to reflect simple differences in preferences.

This is a preview of subscription content, access via your institution

Access options

Access Nature and 54 other Nature Portfolio journals

Get Nature+, our best-value online-access subscription

$29.99 / 30 days

cancel any time

Subscribe to this journal

Receive 12 digital issues and online access to articles

$119.00 per year

only $9.92 per issue

Buy this article

- Purchase on Springer Link

- Instant access to full article PDF

Prices may be subject to local taxes which are calculated during checkout

Similar content being viewed by others

Data availability

The Google Places establishment data were collected using a Google Maps API Premium Plan. The licence precludes publicly sharing the Places location data. Instead, we provide the travel times by foot, car and public transport from the centroid of each block, aggregated to the block group. These travel times are available at https://github.com/urbaninformaticsandresiliencelab/bnk_afi_si/tree/master/_all_data. The 2015 American Community Survey 5-year data files were collected from Census Bureau file transfer protocol (FTP) server (https://www.census.gov/data/developers/data-sets/acs-5year.2015.html). Full details on the variables used are included in Supplementary Discussion, Section 4. The street grid and associated variables were obtained from OpenStreetMap data (https://www.openstreetmap.org). The public transport schedules and associated data were obtained from each city’s General Transit Feed Specification, via the Transitland platform (https://www.transit.land/). The minimum dataset needed for replicating our full set of results is available at https://github.com/urbaninformaticsandresiliencelab/bnk_afi_si/tree/master/modeling_data_cleaned. Source data are provided with this paper.

Code availability

The travel times were calculated with the open-source GraphHopper routing engine and OpenTripPlanner, using OpenStreetMap data. The main results were produced using STATA. The replication code for processing travel times is available at https://github.com/urbaninformaticsandresiliencelab/bnk_afi_si/tree/master/scripts/python. The replication code for the empirical analysis is available at https://github.com/urbaninformaticsandresiliencelab/bnk_afi_si/tree/master/scripts/stata. Source data are provided with this paper.

References

Wilson, W. J. The Truly Disadvantaged: The Inner City, the Underclass, and Public Policy (Univ. Chicago Press, 1987).

Sampson, R. J. Great American City: Chicago and the Enduring Neighborhood Effect (Univ. Chicago Press, 2012).

Chetty, R. & Hendren, N. The impacts of neighborhoods on intergenerational mobility II: county-level estimates. Q. J. Econ. 133, 1163–1228 (2018).

Ludwig, J. et al. Neighborhood effects on the long-term well-being of low-income adults. Science 337, 1505–1510 (2012).

Goering, J. & Feins, J. D. Choosing a Better Life? Evaluating the Moving to Opportunity Social Experiment (Urban Institute Press, 2003).

Small, M. L. & Newman, K. Urban poverty after The Truly Disadvantaged: the rediscovery of the family, the neighborhood, and culture. Annu. Rev. Sociol. 27, 23–45 (2001).

Sharkey, P. & Faber, J. W. Where, when, why, and for whom do residential contexts matter? Moving away from the dichotomous understanding of neighborhood effects. Annu. Rev. Sociol. 40, 559–579 (2014).

Small, M. L. & McDermott, M. The presence of organizational resources in poor urban neighborhoods: an analysis of average and contextual effects. Soc. Forces 84, 1697–1724 (2006).

Faber, J. W. Segregation and the cost of money: race, poverty, and the prevalence of alternative financial institutions. Soc. Forces 98, 819–848 (2019).

Hegerty, S. W. Commercial bank locations and “banking deserts”: a statistical analysis of Milwaukee and Buffalo. Ann. Reg. Sci. 56, 253–271 (2016).

Walker, R. E., Keane, C. R. & Burke, J. G. Disparities and access to healthy food in the United States: a review of food deserts literature. Health Place 16, 876–884 (2010).

Moore, L. & Roux, A. V. D. Association of neighborhood characteristics with the location and type of food stores. Am. J. Public Health 96, 325–331 (2006).

Goodstein, R. M. & Rhine, S. L. W. The effects of bank and nonbank provider locations on household use of financial transaction services. J. Bank Financ. 78, 91–107 (2017).

Hogarth, J. M., Anguelov, C. E. & Lee, J. Who has a bank account? Exploring changes over time, 1989-2001. J. Fam. Econ. Issues 26, 7–30 (2005).

FDIC 2019 Summary of deposits highlights. FDIC Q. 14, 31–43 (2020).

Results from survey of consumer finance. Federal Reserve Board https://www.federalreserve.gov/econresdata/scf/files/scf2013_tables_internal_real.xls (2013).

Consumers and mobile financial services. Federal Reserve Board https://www.federalreserve.gov/econresdata/consumers-and-mobile-financial-services-report-201603.pdf (2016).

FDIC. Brick-and-mortar banking remains prevalent in an increasingly virtual world. FDIC Q. 9, 37–51 (2015).

Burhouse, S., et al. 2013 FDIC national survey of unbanked and underbanked households. Federal Deposit Insurance Corporation https://www.fdic.gov/householdsurvey/2013report.pdf (2014).

Wilson, W. J. When Work Disappears: The World of the New Urban Poor (Knopf, 1996).

Anderson, E. Code of the Street: Decency, Violence, and the Moral Life of the Inner City (WW Norton, 1999).

Venkatesh, S. A. Gang Leader for a Day: A Rogue Sociologist Takes to the Streets (Penguin, 2008).

Caskey, J. P. Bank representation in low-income and minority urban communities. Urban Aff. Q. 29, 617–638 (1994).

Simpson, W. & Buckland, J. Dynamics of the location of financial institutions: who is serving the inner city? Econ. Dev. Q. 30, 358–370 (2016).

Faber, J. W. Cashing in on distress: the expansion of fringe financial institutions during the Great Recession. Urban Aff. Rev. 54, 663–696 (2018).

Friedline, T. & Kepple, N. Does community access to alternative financial services relate to individuals’ use of these services? Beyond individual explanations. J. Consum. Policy 40, 51–79 (2017).

Caskey, J. Fringe Banking: Check-Cashing Outlets, Pawnshops, and the Poor (Russell Sage Foundation, 1994).

Carter, S. P., Skiba, P. M. & Tobacman, J. in Financial Literacy: Implications for Retirement Security and the Financial Marketplace (eds Mitchell, O. S. & Lusardi, A) 145–157 (Oxford Univ. Press, 2010).

Agarwal, S., Skiba, P. M. & Tobacman, J. Payday loans and credit cards: new liquidity and credit scoring puzzles? Am. Econ. Rev. Pap. Proc. 99, 412–417 (2009).

Baradaran, M. How the poor got cut out of banking. Emory Law J. 62, 483–548 (2013).

Melzer, B. T. The real costs of credit access: evidence from the payday lending market. Q. J. Econ. 126, 517–555 (2011).

Laraia, B. A., Siega-Riz, A. M., Kaufman, J. S. & Jones, S. J. Proximity of supermarkets is positively associated with diet quality index for pregnancy. Prev. Med. 39, 869–875 (2004).

Langford, M., Higgs, G. & Dallimore, D. J. Investigating spatial variations in access to childcare provision using network-based geographic information system models. Soc. Policy Admin. 53, 661–677 (2018).

Macdonald, L. Associations between spatial access to physical activity facilities and frequency of physical activity; how do home and workplace neighbourhoods in West Central Scotland compare? Int J. Health Geogr. 18, 2 (2019).

Gross, M. B., Hogarth, J. M., Manohar, A. & Gallegos, S. Who uses alternative financial services, and why? Consum. Interests Annu. 58, 1–13 (2012).

Stegman, M. A. & Faris, R. Payday lending: a business model that encourages chronic borrowing. Econ. Dev. Q. 17, 8–32 (2003).

Payday lending zoning laws and legislation, Appendix 1: list of payday lender ordinances. Consumer Federation of America (2020); https://consumerfed.org/pdfs/PDL_ZONING_LAWS_chart_11-11.pdf

Small, M. L. & Adler, L. The role of space in the formation of social ties. Annu. Rev. Sociol. 45, 111–132 (2019).

Smith, T. E., Smith, M. M. & Wackes, J. Alternative financial service providers and the spatial void hypothesis. Reg. Sci. Urban Econ. 38, 205–227 (2008).

Baradaran, M. How the Other Half Banks: Exclusion, Exploitation, and the Threat to Democracy (Harvard Univ. Press, 2015).

Taylor, K.-Y. Race for Profit: How Banks and the Real Estate Industry Undermined Black Homeownership (Univ. of North Carolina Press, 2019).

Friedline, T. & Chen, Z. Digital redlining and the fintech marketplace: evidence from U.S. zip codes. J. Consum. Aff. https://doi.org/10.1111/joca.12297 (2020).

Goodstein, R., Lloro, A., Rhine, S. L. W. & Weinstein, J. What accounts for racial and ethnic differences in credit use? FDIC Division of Depositor and Consumer Protection working paper no. 2018-01 (Federal Deposit Insurance Corporation, 2018).

Aliprantis, D., Carroll, D. R. & Young, E. R. What explains neighborhood sorting by income and race? Working paper no. 18-08 R. Federal Reserve Bank of Cleveland https://doi.org/10.26509/frbc-wp-201808r (2019).

Pattillo, M. Black middle-class neighborhoods. Annu. Rev. Sociol. 31, 305–329 (2005).

Pattillo, M. Black on the Block: The Politics of Race and Class in the City (Univ. Chicago Press, 2007).

Massey, D., & Denton, N. American Apartheid: Segregation and the Making of the Underclass (Harvard Univ. Press, 1993).

Pattillo-McCoy, M. Black Picket Fences: Privilege and Peril among the Black Middle Class (Univ. Chicago Press, 1999).

Charles, C. Z. The dynamics of racial residential segregation. Annu. Rev. Sociol. 29, 167–207 (2003).

Tienda, M. & Fuentes, N. Hispanics in metropolitan America: new realities and old debates. Annu. Rev. Sociol. 40, 499–520 (2014).

Galster, G. C. & Santiago, A. Neighborhood ethnic composition and outcomes for low-income Latino and African American children. Urban Stud. 54, 482–500 (2017).

Small, M. L. & Pager, D. Sociological perspectives on racial discrimination. J. Econ. Perspect. 34, 49–67 (2020).

Acknowledgements

The authors thank J. Beshears, T. García Mathewson and R. Sampson for comments, and M. Mobius for helpful early conversations. M.L.S. received funding from Harvard University and the Harvard Project on Race, Class and Cumulative Adversity, at the Hutchins Center, to support this project. The funders had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript.

Author information

Authors and Affiliations

Contributions

M.L.S. designed research, performed research, analysed data and drafted paper. A.A. created dataset and visualizations, analysed data, produced replication package and edited paper. M.T. performed research and edited paper. Q.W. co-created dataset, performed research and edited paper.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Peer review information Nature Human Behaviour thanks Megan Doherty Bea, George Galster and the other, anonymous, reviewer(s) for their contribution to the peer review of this work.

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Supplementary information

Supplementary Discussion and Supplementary Tables 1–3.

Source data

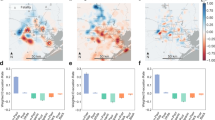

Source Data Fig. 1

Data for Fig. 1. AFI easier to get to as proportion minority in neighbourhood increases, regardless of whether neighbourhood is poor or non-poor. Adjusted and unadjusted included probability that AFI establishment is faster to get to.

Source Data Fig. 2

Data for Fig. 2. Could race differences in demand account for the pattern? Banks still harder to get to in low-poverty, college-educated, minority homeowner neighbourhoods than high-poverty, low-education, white renter neighbourhoods.

Rights and permissions

About this article

Cite this article

Small, M.L., Akhavan, A., Torres, M. et al. Banks, alternative institutions and the spatial–temporal ecology of racial inequality in US cities. Nat Hum Behav 5, 1622–1628 (2021). https://doi.org/10.1038/s41562-021-01153-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41562-021-01153-1

This article is cited by

-

An environmental justice analysis of air pollution emissions in the United States from 1970 to 2010

Nature Communications (2024)

-

7-day patterns in Black-White segregation in 49 metropolitan areas

Scientific Reports (2024)

-

A Life Course Perspective of Community (Non)Investment: Historical Financial Service Trajectories and Community Outcomes

Journal of Family and Economic Issues (2023)

-

The data revolution in social science needs qualitative research

Nature Human Behaviour (2022)