Abstract

Very wealthy people influence political and societal processes by wielding their economic power through foundations, lobbying groups, media campaigns, as investors and employers. Because personality shapes goals, attitudes, and behaviour, it is important to understand the personality traits that characterize the rich. We used representative survey data to construct two large samples, one from the general population and one consisting of individuals with at least 1 million euros in individual net wealth, to analyse what personality traits characterize the wealthy and why their traits differ from those of the general population. High wealth was associated with higher Risk tolerance, Emotional Stability, Openness, Extraversion, and Conscientiousness. This “rich” personality profile was more prominent among individuals who had accumulated wealth through their own efforts (“self-mades”) than among individuals who had been born into wealth (“inheritors”). Thus, our evidence is suggestive of a unique configuration of personality traits contributing to self-made millionaires’ economic success.

Similar content being viewed by others

Introduction

Previous research has shown that the wealthiest individuals in society (referred to in the following as “the rich”) use their substantial economic power to influence political and societal processes. They have the ear of politicians and policy makers, and their beliefs about the way our society should be shaped filter down to everyone because they can market their ideas through their foundations, lobbying groups, media campaigns, and as investors and employers (Andreoni and Payne, 2013; Andres, 2008; Bartels, 2009; Bertrand et al., 2018; Fuentes-Nieva and Galasso, 2014; Manning, 2013). Interest in this influential group is widespread, as reflected in the popularity of books on how to get rich, the extensive media coverage of “the top one percent,” and the growing body of scholarly research on wealth and inequalities. Because goals, attitudes, and behaviour are shaped by personality (Gerber et al., 2010), it is important to learn more about who these individuals are and how their personality traits may differ from those of the general population. This is especially vital in light of rising inequality (Atkinson et al., 2011) and its polarizing impact on social comparisons (Cheung and Lucas, 2016).

Even more contested than the question of how the personality traits of the wealthy may differ from others is the question of why this might be the case. Put simply: Is the specific personality of the rich a consequence of or a factor contributing to their wealth? More specifically, it is currently unknown whether inheriting money and growing up rich leads to the development of a prototypical “rich” personality profile, or whether a specific personality profile promotes self-made economic success.

Despite the evident importance of understanding how and why rich individuals differ from the general population, there has been little investigation into the personality profiles of the very wealthy. This is not due to a lack of interest or relevance but because the rich make up a tiny fraction of the population that is especially hard to reach (Kennickell and Woodburn, 1999). As a result, they form a very small and difficult-to-analyse minority in existing population-representative surveys. The few existing analyses (Leckelt et al., 2019) were based on small convenience samples of the rich, thus raising questions about the generalizability of the results. Moreover, due to limitations on sample size and representativeness, previous research has not been able to address the question of why the personality profile of the wealthy differs from that of the general population.

There is a longstanding debate on how wealth and related constructs (e.g., social class and social status) shape people’s personality traits, goals, beliefs, and behaviours. Even laypeople often distinguish between “different types” of wealthy people who allegedly have different personality traits: those who were born into their wealth (“inheritors”) versus those who accumulated their wealth through their own efforts (“self-mades”). Similarly, scholarly work has often focused on the idea that being born into or inheriting wealth may shape personality through status and class-related characteristics. Such socialization effects have been proposed in sociology (e.g., Bourdieu’s concept of habitus; Bourdieu, 1984, 1990) and social psychology (Fiske and Markus, 2012). Other research has pointed toward personality’s role in promoting self-made wealth accumulation through entrepreneurship. Previous studies (Leckelt et al., 2019; Smeets et al., 2015) have indicated that a substantial percentage of wealthy individuals own a business, suggesting that a large proportion of their wealth may be self-made. Entrepreneurship has also been linked to a specific personality profile (Obschonka et al., 2010, 2013). It therefore appears possible that rich individuals are rich because they possess entrepreneurial personality traits that helped them accumulate their wealth.

With regard to personality, the Big Five personality traits (Neuroticism, the tendency to be worried/nervous; Extraversion, the tendency to be active/sociable; Openness to experience, the tendency to be inventive/curious; Agreeableness, the tendency to be friendly/compassionate; and Conscientiousness, the tendency to be organized/persistent), based on the Five-Factor-Model of personality (John et al., 2008; McCrae and Costa, 1997), and risk-taking propensity have been linked to a multitude of life outcomes and financial behaviours. Several studies have highlighted the roles of Conscientiousness and Emotional Stability in job performance, wages, and money management behaviours and attitudes (Almlund et al., 2011; Borghans et al., 2008; G. Donnelly et al., 2012). Other studies have highlighted the role of personality in attaining status and compensating for background disadvantages (Damian et al., 2015; Grosz et al., 2020), in creditworthiness and credit eligibility (Arráiz et al., 2017; Klinger et al., 2013), and in the likelihood that individuals will experience certain types of life events (Denissen et al., 2019). Risk-taking has been shown to be another important, independent predictor of various economic behaviours, such as investing (Mata et al., 2018), self-employment and entrepreneurship (Caliendo et al., 2009, 2014), and company performance (Sanders and Hambrick, 2007).

In the absence of a more direct measure, previous studies investigating wealthy individuals often relied on using income as proxy variable of wealth (Blanchflower and Oswald, 2004; Di Tella et al., 2010; Diener and Diener, 2009; Kahneman and Deaton, 2010). However, using individual-level net wealth, which provides a direct measure of an individual’s material resources, has several comparative advantages. First, while income may fluctuate substantially from year to year, especially in high-paying occupations (Betermier et al., 2012), wealth, which is accumulated over the course of a lifetime, comes closer to measuring lifetime material resources. This is in part because income has a more restricted, less right-skewed distribution than individual-level net wealth (G. E. Donnelly et al., 2018). The more right-skewed distribution of wealth implies larger differences in wealth than in income between, for instance, the top ten percent and the top one percent. These larger differences may come with significant distinctions in personality. Second, wealthy individuals can often forego personal income in lieu of non-realized capital gains (possibly to retain or invest profits in their business and collect the capital gains later, when they will be taxed at a more favourable rate (Kopczuk and Zwick, 2020). This makes individual net wealth a more accurate measure than current income to describe material resources, especially at the top.

In this study, we used two unique, large samples, from the general population (N = 23,721) and rich individuals holding at least €1 million individual net wealth, which represents the top 1.6% of the wealth distribution in Germany (N = 1125). We sought to (1) answer the questions of how the general population and the rich differ in their personality profiles, and (2) explore whether these differences can be attributed to individuals having been born into wealth or having acquired wealth through their own efforts. To provide initial empirical evidence regarding the second question of why the rich might have a different personality profile, we investigated two fundamentally different explanations: (1) because they were born into wealth and consequently developed different personality traits, and (2) because their personality traits promoted their economic success and accumulation of self-made wealth. See Table S1 for an overview of the characteristics of the rich.

Methods

The data used in this study met four central requirements to meaningfully address the questions of how and why rich individuals differ from the general population: (1) both samples use well-validated survey instruments and the same measures for the general population and the rich sample, (2) data on personality and wealth portfolios are collected at the individual level, (3) the number of rich people is substantially higher than in previous studies, and (4) the samples are population representative and come from surveys randomly drawn within their respective populations.

Data sources

The sample of rich individuals used in this study is largely comprised of a new top-wealth subsample (SOEP-P) in the German Socio-Economic Panel (SOEP). The SOEP measures not only personality but also wealth at the individual level; basically, all other surveys collect wealth data only at the household level. The SOEP-P, which was first surveyed in 2019 (Schröder et al., 2020), is thus unique in fulfilling the data requirements mentioned above.

The SOEP study began in 1984 and now surveys about 15,000 households and about 30,000 individuals every year (Giesselmann et al., 2019; Goebel et al., 2019). The target population is Germany’s resident population. New samples have been added over time to compensate for panel attrition, to maintain cross-sectional representativeness in the presence of influx to the underlying target population, and to oversample subpopulations like the wealthy (Kroh et al., 2018). Direct comparisons between different subsamples are possible thanks to the use of identical questionnaires and data-preparation procedures in the SOEP.

The SOEP scientific data infrastructure undertakes comprehensive measures to ensure data quality and consistency. Beyond the usual test routines to check data plausibility and consistency after data collection, the SOEP has put in place institutional safeguards to ensure data quality include monitoring mechanisms to verify the correct work of the interviewers, generation of user-friendly variables (including inter-temporal harmonization and statistical imputation), and external validations of SOEP statistics with external data sources (Schröder et al., 2020).

Population of interest

Our population of interest consists of adult individuals living in Germany. We distinguish these individuals according to whether or not they are rich, as measured by individual net wealth. In order to make the two groups sufficiently distinct from one another, we exclude individuals with individual net wealth levels between 800,000 and 1 million euros. Observations in this range of wealth are likely to contaminate salient differences between the general non-rich population and our sample of rich individuals. We label the individuals with lower individual wealth “non-rich” and those with higher wealth “rich”.

The working sample contains 23,721 individuals. Of these, 1125 individuals have individual net wealth of at least 1 million euros, 190 of at least 5 million euros, and 61 of at least 10 million euros. The richest five respondents have net wealth between 100 and 131 million euros.

Figure 1 shows the distribution of net wealth for the regular SOEP and SOEP-P samples, with the shaded area indicating the rich population (N = 1125), as well as the fraction of the relevant millionaire subpopulations: rich self-mades (millionaires for whom entrepreneurship and self-employment had the prime influence on their wealth, N = 517), and rich inheritors (N = 136, millionaires for whom gifts, inheritances, or marriage had the prime influence on their wealth). See Table S2 for percentiles of wealth for the combined sample and the rich sample. The data provide sufficient statistical power to analyse the personality traits of millionaires in Germany. Note that our data also overlap with the 2019 Manager Magazin “rich list” of the wealthiest 1000 individuals in Germany (according to expert estimates), who made up the top 0.00144 percent of the adult population in Germany in 2019 (Federal Statistical Office of Germany, n.d.). Last place (number 1000) in the Manager Magazin rich list is held by an individual with 90 million euros. The richest individual surveyed in our study comes in at number 821 in the Manager Magazin list. Note, however, that rich lists are prone to overestimating net wealth: as Raub et al. (2010) document, net wealth from inheritance tax records is on average about 50 percent of what is recorded in the Forbes 400 list.

On the left is a kernel density plot of net wealth for SOEP and SOEP-P and on the right is the composition of the rich population with respect to both relevant subgroups of millionaires (inheritors and self-mades) as well as a remaining group of rich individuals with mixed or unspecified factors influencing their wealth (mixed/unspecified). Data based on SOEP v36 (10.5684/soep-core.v36eu).

Focal variables

Our analyses require information on individual’s net wealth, personality traits (specifically the Big Five and risk-taking), and basic socio-demographic variables. An overview of all variables used in this study can be found in Table S3.

Individual net wealth

The SOEP survey includes a wealth module to collect data on owner-occupied housing, rental property, financial assets, building loan contracts, life and private pension insurance, tangible assets, vehicles, and privately owned businesses (market value). In case an asset is owned by multiple individuals such as spouses or business partners, respondents are asked to state how many shares they personally own. SOEP also collects information on individual liabilities: mortgages on owner-occupied housing, mortgages on rental property, consumer debt, and student loans. Individual net assets, used here to distinguish rich and non-rich individuals, is the sum of the eight asset components minus the four liability components. Measurement of wealth at the individual level is a special feature of the SOEP survey and essential for our analyses, since the use of household wealth would not take into account how many people in the household share the wealth in what proportions.

Personality

The Big Five personality traits are derived from SOEP’s short Big Five inventory (BFI-S), measuring each of the five traits with three items. Participants are asked to rate their agreement with statements starting with “I am …” on a scale from 1 (strongly disagree) to 7 (strongly agree). An example for the dimension of Conscientiousness would be “I am a thorough worker.” The BFI-S generally showed acceptable levels of: (1) internal consistency, (2) stability over a period of 18 months, (3) convergent validity in relation to the NEO-PI-R measuring the Big Five with 240 items and in relation to the BFI measuring the Big Five with 44 items, and (4) discriminant validity (Ackerman et al., 2016; Hahn et al., 2012). Evidence for the validity of this short version is provided by Gerlitz and Schupp (2005). A factor analysis clearly revealed the expected five-factor structure. Internal consistency was comparable to other short scales in which heterogeneous items are selected to maximize validity, ranging from 0.49 (Agreeableness) to 0.69 (Extraversion). For an overview of the correlation between the personality traits, see Table S4.

We use risk-taking as an additional personality trait for several reasons. Risk-taking is an important explanatory variable for entrepreneurship (Cagetti and De Nardi, 2006, 2008; De Nardi and Fella, 2017) and an important factor in wealth creation (Quadrini, 1999), investing (Mata et al., 2018), and company performance (Sanders and Hambrick, 2007). SOEP respondents are asked to rate their willingness to take risks on a scale from 0 to 10, where 0 means “not at all willing to take risks” and 10 means “very willing to take risks.” A comparison of this self-rated risk measure with an alternative measure of risk-taking from an incentivized lottery experiment in the field shows that the self-rating predicts actual risk-taking behaviour very well (Dohmen et al., 2011), and the self-rated risk measure has even outperformed incentivized lottery experiments in predicting real-world risk-taking across different domains (Hertwig et al., 2019). Recently, Arslan et al. (2020), analysed the self-perceptions behind stated Risk tolerance. They showed that people recount diagnostic behaviours and experiences, focusing on voluntary, consequential acts and experiences when inferring their risk preference.

Socio-demographic variables

The SOEP collects a wide range of sociodemographic information. In this study we used gender (0 = female, 1 = male) as well as the self-created variables age category (1 = younger than 40, 2 = between 40 and 60, 3 = older than 60) and high education (1 = 12 or more years of schooling; 0 = else) as control variables for our analyses.

Group definitions

We subdivided the general and the rich population into “inheritors,” “self-mades,” and individuals who cannot be assigned to the two other groups, i.e., the “mixed/unspecified group.” The latter group served as a benchmark for the personalities of the two former groups, as it consists of individuals who can be considered a convex combination of inheritors and self-mades. For this grouping, we relied on a battery of questions that ask respondents about the factors that have reduced, not influenced, or increased the amount of wealth they currently hold as individuals. These factors are: (1) entrepreneurship or self-employment, (2) dependent employment, (3) earnings from financial transactions, (4) real estate, (5) gifts, (6) inheritances, (7) marriage, and (8) lottery winnings. Respondents rated each of these factors on an 11-point Likert scale from –5 (reduced assets significantly) to 5 (increased assets significantly). Inheritors fulfilled the following criteria: (1) They rated the importance of either gifts or inheritances or marriage in increasing their individual wealth higher than 3. (2) They rated the importance of entrepreneurship and self-employment in increasing their individual wealth 3 or lower. Self-mades fulfilled the following criteria: (1) They rated the importance of entrepreneurship and self-employment in increasing their individual wealth higher than 3. (2) They rated the importance of either gifts and inheritance and marriage in increasing their individual wealth 3 or lower.Footnote 1 The groups based on self-ratings stratify well across many objective measures. The Supplementary Materials (Tables S11 and S12) show that the self-made scored high on objective measures of self-made economic success (such as self-employment and business wealth) and low on measures of being born into wealth (such as inheritances and the ratio of capitalized inheritances to current net wealth), while for inheritors the inverse is true.Footnote 2 The choice of the cut-offs ensures selectivity of the group while securing a reasonable size of the group, as can be seen from Table 1. Note that the share of rich self-mades is large (45%), which is congruent with evidence in Scheuer and Slemrod (2020) for the United States. Means and standard deviations for several socio-demographic variables as well as the personality items for each group among the rich and non-rich are shown in Table S5. Figure S2 in the Supplementary Materials shows histograms for each of the factors split across the rich and non-rich, while Fig. S3 shows these histograms for self-mades and inheritors, and Table S6 shows rank correlations of the influence factors.

Construction of a prototypical personality profile of the rich

The construction of the prototypical personality profile of the rich regarding the Big Five and risk-taking was informed by previous research that found wealthy individuals to score higher on Extraversion, Conscientiousness, Openness, and Narcissism, as well as scoring lower on Neuroticism and Agreeableness (Leckelt et al., 2019). There also exists initial indirect evidence that risk-taking is related to wealth (Cass and Stiglitz, 1972; Iglesias et al., 2004; King, 1974; Paravisini et al., 2017) and household income (Barsky et al., 1997; Dohmen et al., 2011). Moreover, narcissism, one of the traits that is somewhat more pronounced in wealthy individuals is linked to increased risk-taking (Buyl et al., 2019; Wales et al., 2013). Finally, a substantial number of wealthy individuals own businesses (Leckelt et al., 2019; Smeets et al., 2015) and entrepreneurship has been linked to a personality profile consisting of high values “[…] in extraversion, conscientiousness, and openness” and low levels of “[…] agreeableness and neuroticism” (Obschonka et al., 2013, p. 107). Thus, the prototypical profile of rich individuals can reasonably be assumed to consist of (limiting on the personality characteristics assessed in the present study): the highest possible values in Extraversion, Openness, Conscientiousness, and risk-taking as well as the lowest possible values in Neuroticism and Agreeableness.

Following previous studies that have successfully used a personality profile approach, linking personality profiles to entrepreneurial activity (Obschonka et al., 2013), to investigate personality types in adolescents (Asendorpf and van Aken, 1999; Robins et al., 1996), or person-environment-fit (Götz et al., 2018), we calculated a difference score to the prototypical profile of the rich for each person in the samples based on (Cronbach and Gleser, 1953) as follows:

Subscript j indicates a specific personality trait and the indices 1 and 2 represent a prototypical and a person’s actual score on trait j, respectively. Thus, the larger this difference, the more dissimilar is a person’s personality profile from the prototypical profile of the rich.

Results

Result 1: The rich are more risk tolerant, open, extraverted, and conscientious, but less neurotic than the general population

Regarding the first research question of how the rich differ from the general population, we first compared individuals from the rich and non-rich populations on each of the six personality traits (Big Five and risk-taking) using Welch’s t-tests and additionally report Cohen’ D. Results indicated that the rich were substantially more risk tolerant (t(1252) = 21.97, p < 0.001; D = 0.63), open (t(1241) = 10.99, p < 0.001; D = 0.33), extraverted (t(1239) = 7.29, p < 0.001; D = 0.22), and conscientious (t(1242) = 5.97, p < 0.001; D = 0.18) as well as less neurotic (t(1239) = −16.72, p < 0.001; D = −0.50) and less agreeable (t(1226) = −2.14, p = 0.032; D = −0.06) than the general population. Figure 2 shows the kernel density plots for each of the personality traits, for both the rich and non-rich, illustrating and underscoring the findings from the mean comparisons.

Data based on SOEP v36 (10.5684/soep-core.v36eu).

To evaluate the robustness of these results, we estimated separate OLS regression models with robust standard errors and each of the six personality traits as dependent variables as well as a dummy variable indicating sample membership (rich vs. non-rich), socio-demographic controls (age, gender, education), and interaction terms (age × gender) as explanatory variables. Results from the regression analyses (Table 2) confirmed the mean comparisons, such that only the difference in Agreeableness was not statistically significant.

Result 2: Self-made and inherited millionaires differ in their personality profiles. Self-mades show a more pronounced personality profile of high Risk tolerance, low Neuroticism, and high Openness, Extraversion, and Conscientiousness. While less pronounced, non-rich self-mades display a similarly shaped personality profile

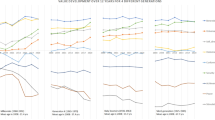

Millionaires distinguish themselves from the rest of the population by their unique profile of personality traits. This profile of higher Risk tolerance, Openness, Extraversion, and Conscientiousness, as well as lower Neuroticism and Agreeableness is illustrated in Fig. 3A, showing the average of the standardized trait scales after controlling for socio-demographics in an OLS regression (for details, see Table 2; socio-demographic controls used in these analyses are age, gender, education, and interaction terms for age and gender).

A The mean of the standardized personality traits for rich and non-rich, B mean of traits for rich self-mades, inheritors, and the mixed/unspecified group, and C means for non-rich self-mades, inheritors, and the mixed/unspecified group. Results are based on OLS regressions (see Table 3). Data based on SOEP v36 (10.5684/soep-core.v36eu).

Our group definitions enabled us to investigate two competing hypotheses. Under the first hypothesis, which posits that the unique personality profile of the rich is a consequence of being born rich or becoming rich without effort, one would expect that individuals who inherited their wealth or married into it (inheritors) (1) would show the most pronounced pattern of high Risk tolerance, low in Neuroticism, and high in Openness, Extraversion, and Conscientiousness, and, thus, (2) would show a personality profile that resembles the prototypical profile of rich individuals, that being the most pronounced realizations of traits among millionaires (i.e., maximum values for Risk tolerance, Openness, Extraversion, and Conscientiousness; minimum values for Neuroticism and Agreeableness). Under the competing hypothesis, which posits that the unique personality profile of the rich drives wealth accumulation, one would expect that the group of rich individuals who became wealthy through their own efforts (self-mades) would show the most pronounced trait pattern and would be prototypical for the rich personality profile.

Figure 3B shows, for the rich, the trait-by-trait personality profile of the inheritors, self-mades, and the mixed/unspecified group, derived from predictive margins based on OLS regressions after controlling for socio-demographic factors (see Table 3; socio-demographic controls used in the analyses are age, gender, education, and interaction terms for age and gender). Results showed that among the rich, all subgroups tracked the average profile of the rich, but to varying degrees. Self-mades showed the highest values for risk-tolerance, Openness, Extraversion, and Conscientiousness and the lowest for Neuroticism. Inheritors showed the lowest values for risk-tolerance, Openness, Extraversion, and Conscientiousness and the highest for Neuroticism. The confidence intervals for the self-mades did not overlap the point estimates for the inheritors for Risk tolerance, Neuroticism, Openness, Extraversion, and Conscientiousness, indicating that the groups are different with respect to these traits. The mixed/unspecified group’s profile fell in between the profiles of self-mades and inheritors.

As an additional test of our competing hypotheses, we reduced the dimensionality of differences in personality traits and measured the distance from the prototypical personality profile of millionaires for all subgroups of the rich and non-rich samples. We calculated a quadratic distance from this prototypical personality profile for every individual in the sample (see Supplementary Materials for details and Table S8 for descriptive statistics). This approach allowed us to study personality differences holistically to complement the trait-by-trait comparisons. Fig. 4A shows the kernel densities of the distances from the prototypical profile for all three groups split for the rich. The densities support the trait-by-trait analysis. Among the rich, the distributions for the mixed/unspecified group and the self-mades were fairly similar, while the distribution for rich inheritors indicate was furthest from the prototypical profile (see Table S9 for regression results with socio-demographic controls described above).

Panel A shows the kernel density of distance to prototypical personality profile for inheritors, self-mades, and the mixed/unspecified group split among the rich, while panel B shows these kernel densities among the non-rich population. Data for the “non-rich” sample are from the SOEP, data for the “rich” sample are based on the SOEP-P. Data based on SOEP v36 (10.5684/soep-core.v36eu).

We also took a closer look at the non-rich subgroups. Figure 3C shows, for the non-rich, that the profiles of the inheritors and the mixed/unspecified group were generally flat, that is, they did not track the personality profile of the rich. However, the group of non-rich self-mades did track the profile of the rich: They were high in risk-tolerance, Openness, Extraversion, and Conscientiousness and low in Neuroticism. Indeed, Table 3 shows that the 95 percent confidence intervals for non-rich self-mades did not overlap with the point estimates for non-rich inheritors for Risk tolerance, Neuroticism, Openness, Extraversion, or Conscientiousness. In Fig. 4B, non-rich self-mades also showed lower distances to the prototypical rich personality profile than the other non-rich groups. This was also confirmed by the regression coefficients shown in Table S9. Interestingly, the non-rich self-mades also did not differ from rich inheritors regarding the prototypical rich profile as the OLS regression indicated: Rich inheritors’ distance from the profile was lower compared to non-rich inheritors or the non-rich mixed/unspecified group, but this was not statistically significant (B = 3.678, p = 0.179), while non-rich self-mades’ distance was lower compared to non-rich inheritors and the non-rich mixed/unspecified group (B = 11.471, p < 0.001). However, the non-rich self-mades’ profile was not as pronounced as the profile of rich self-mades, as both the OLS and the median regression in Table S9 indicate. Further, a comparison of rich self-mades’ confidence intervals with the point estimates for non-rich self-mades in Table 3 shows that self-mades who became rich are even more risk-tolerant and less neurotic than non-rich self-mades.

Finally, we analysed whether the degree to which individuals possessed the unique rich personality profile predicted wealth even within the group of rich self-mades. We regressed wealth on the distance from the prototypical profile and each trait. Indeed, the richer the self-mades were, the more they resembled the prototypical profile, a result that was driven particularly by their higher Risk tolerance (see Table S10). In other words, the more individuals had a self-made, risk-tolerant personality, the higher their wealth.Footnote 3

We conclude that it is the unique personality profile of rich self-mades that is primarily responsible for personality differences between the rich and non-rich. They showed the most pronounced profile of high Risk tolerance, Openness, Extraversion, and Conscientiousness as well as low Neuroticism, and differed in each of these individual traits from rich inheritors. Conversely, rich inheritors conformed least to the prototypical profile of the rich. In addition, the profile of the non-rich self-mades resembled the prototypical personality of the rich, but their personality profile was still not as pronounced as that of rich self-mades. Compared to the rich population, self-mades made up a smaller portion of the non-rich population (see Table 1), which also contributed to the differences in personality profiles between the rich and non-rich (Fig. 3A). Finally, personality even predicted wealth within the highly selective group of rich self-mades: Rich self-mades with a more pronounced and particularly risk-tolerant personality profile were even richer than rich self-mades with a less pronounced profile.

The above evidence provides sorely needed descriptive information about the personality of the rich. In addition, it is also suggestive of the theory that the unique personality profile of millionaires results from individuals with the trait profile of self-made millionaires (particularly individuals in which this profile is more pronounced) having a higher chance of becoming rich.

Discussion

Our findings extend previous research and have several important implications, both for general interest and research, but also for the evaluation of the relevance of political influence groups on democratic processes.

First, we provide the (to date) best available robust evidence for a unique personality profile of the rich. Using (a) a large representative dataset with strong oversampling of millionaires, (b) established personality frameworks, and (c) well-validated measures that allow direct comparisons to the general population, we show that the rich are higher in Risk tolerance, Openness, Extraversion, and Conscientiousness, and that they are lower in Neuroticism. These findings extend and complement existing research on millionaires that has looked at giving behaviour (Smeets et al., 2015; Whillans and Dunn, 2018), time use (Smeets et al., 2019), and happiness (G. E. Donnelly et al., 2018), and provide a consistent and robust picture of the personality traits that characterize the rich.

Second, we provide suggestive evidence that personality may be a driving force in the accumulation of wealth rather than a consequence thereof. We show that rich self-mades conform most closely to the prototypical rich personality profile. Rich inheritors, in contrast, do not conform to the prototypical rich personality profile: They are far less willing to take risks and more neurotic. Thus, it appears that being born into wealth does not automatically lead to the development of the prototypical rich personality profile. We also find the prototypical profile among the non-rich self-mades, although to a lesser extent. This personality profile therefore does not automatically lead to economic success. Many other factors contribute to an individual’s position in the wealth distribution, such as initial capital, education, and abilities. However, the evidence we have gathered conforms to the idea that the unique personality of millionaires is driven by individuals with a self-made personality having a higher chance of becoming rich.

Third, our findings have important implications beyond the group of the rich. Because the rich influence many aspects of politics and society, the personality differences described above create externalities. The personality traits of the rich and their influence on rich individuals’ decision-making have direct impacts on the general population in the areas of work and politics as well as culture and society. Importantly, the rich have many of the same personality traits as entrepreneurs, and as exemplified here, this is certainly beneficial for economic success. However, this does not mean that such a trait constellation is necessarily also beneficial in other, more communal areas of social life. For instance, when an important decision-maker with a high Risk tolerance implements plans that may be beneficial but are very risky, this risk-prone decision making may end up being to the detriment of the more risk-averse rest of the population. Risk tolerance seems to be particularly important regarding both the positive and potentially negative consequences of rich individuals’ personality traits. Risk tolerance differs most between the rich and the non-rich and is predictive of behaviours such as entrepreneurship (Caliendo et al., 2009) and stock holding (Dohmen et al., 2011), but also overly optimistic decision making (Hvide and Panos, 2014) and collective losses, for example, due to corruption (Jain, 2001).

Naturally, our study does not come without limitations. Although our samples are large and representative, they only contain data from one country (Germany). While Germany is a highly developed nation with a wide dispersion in wealth, it may not necessarily represent all high-wealth countries, such as the United States, where the wealth distribution is even more unequal. Further, societal and cultural differences that shape personalities in Germany may also not be generalizable to other countries such as the United States, which is generally considered to be more individualistic than other countries (Miller et al., 2015). What we can say, however, is that the sample of rich individuals is comparable on socio-demographics to the samples in other studies (Smeets et al., 2015).

Next, the self-made and inheritor groups are constructed based on self-report data, which, to some degree, involve subjective judgments by the respondents and may even be subject to tendencies of emphasizing one’s own hard work instead of inherited advantages. However, since being a “hard worker” is a characteristic that is seen positively in many cultures and contexts, this self-report tendency should apply equally to all respondents, not just the wealthy. Nonetheless, ideally one would be able to objectively assess the contribution of an individual’s own hard work as well as inherited advantages. As this would involve having access to individuals’ bank accounts, assets, type of employment, consumption, etc. over a long period of time, this is out of scope for most academic research.

Additionally, it could be argued that because inheriting money is often associated with the loss of loved one (e.g., family member, spouse), which is a significant life event (Bratt et al., 2018), inheritance may be a source of personality differences. Research indicates, however, that widowhood or spousal bereavement (Chopik, 2018; Denissen et al., 2019) does not have long-lasting effects on personality traits such as the Big Five. With regard to personality-related constructs such as life satisfaction, well-being, and affect, the literature documents consistent drops around the loss of a loved one (see, however, Anusic et al., 2014), but these effects tend not to be long-lasting, with individuals returning to their baseline after a few years (Clark and Georgellis, 2013; Infurna and Luthar, 2017; Leopold and Lechner, 2015). Thus, it seems that the documented personality differences cannot be attributed to the fact that inheritance is associated with a significant negative life event.

Finally, we cannot formally answer the questions of whether the prototypical personality profile of the rich is the cause of their economic success and how their distinct personality profile may contribute to increasing their wealth through money management. Conscientiousness, for example, a trait on which the rich and especially self-made millionaires score significantly higher, has been linked to more positive financial attitudes, a stronger future orientation, and better money management (G. Donnelly et al., 2012).

Because of the cross-sectional and self-report nature of our data, we can only treat the evidence for the unique personality profile of the rich being a driver of their economic success as suggestive. While the results presented here are consistent with the hypothesis that the prototypical personality profile of the rich supports or even enables their economic success, longitudinal data would be very valuable in working toward a more conclusive answer.

In an ideal setting, we would be able to randomly vary the personality traits of a treatment group to conform to the prototypical personality profile of the rich and longitudinally track their economic success against that of the control group over time. This is a high bar to clear because finding a setting in which such variation exists as a quasi-experiment is difficult, and changing a person’s personality profile through intervention appears unfeasible (Roberts et al., 2017).

Conclusion

In this paper, we have shown that the rich differ from the rest of the population not only with respect to their wealth but also with respect to their personality traits. The prototypical personality profile of the rich is marked by higher Risk tolerance, Openness, Extraversion, and Conscientiousness, and lower Neuroticism. Further, we provide initial suggestive evidence that this unique personality profile may contribute to wealth accumulation. In our data, self-made millionaires most closely tracked the personality profile of the rich, and the more they did, the richer they were. A promising avenue for future research would be to analyse these personality differences as a means to better understand how the rich shape society.

Data availability

Data are available from the German Socio-Economic Panel (SOEP) study due to third-party restrictions (for requests, please contact soepmail@diw.de). The scientific use file of the SOEP with anonymous microdata is made available free of charge to universities and research institutes for research and teaching purposes. The direct use of SOEP data is subject to the strict provisions of German data protection law. Therefore, signing a data distribution contract is a precondition for working with SOEP data. The data distribution contract can be requested by submitting the form: https://www.diw.de/en/diw_01.c.601584.en/data_access.html. For further information, contact the SOEP hotline at soepmail@diw.de or +49-30-89789-292.

Notes

Our approach to defining millionaire subtypes is preferable to the use of objective indicators, such as inheritances (especially the type, timing, and amount thereof) and employment biographies. Even if such information were fully available, an accurate and detailed modelling of wealth accumulation over the life cycle would be necessary. This is because if we want to assess the role of an inheritance or self-made success for an individual’s wealth situation today, one would have to compare the actual situation with a counterfactual situation with these factors absent. This counterfactual is unobserved and would have to be modelled under untestable assumptions (König et al., 2020).

To check robustness of the self-rating scales, we tightened the group definition, increasing the critical values for group membership from 3 to 4. Table S7 shows the share of observations in each of the categories under the different definitions. The Supplementary Materials show (a) that all our main results are robust to the change of the critical values; (b) that the tight definition, following our expectations, makes self-mades’ personality profile more similar to the prototypical personality profile of the rich, while it does the inverse for inheritors.

Tables S11 and S12 in the Supplementary Materials provide additional information and detailed descriptive statistics on the share of heirs, capitalized inheritance, and inheritance ratios among the different groups (Table S11) as well as the share of self-employed individuals among the different groups (Table S12).

References

Ackerman RA, Donnellan MB, Roberts BW, Fraley RC (2016) The effect of response format on the psychometric properties of the Narcissistic Personality Inventory: consequences for item meaning and factor structure. Assessment 23(2):203–220. https://doi.org/10.1177/1073191114568113

Almlund M, Duckworth AL, Heckman J, Kautz T (2011) Personality psychology and economics. In: Hanushek, Machin and Woessmann (ed) Handbook of the economics of education, vol 4. Elsevier, pp. 1–181

Andreoni J, Payne AA (2013) Charitable giving. In: Auerbach, Chetty, Feldstein, and Saez (ed) Handbook of public economics, vol 5. North-Holland, pp. 1–50

Andres C (2008) Large shareholders and firm performance—an empirical examination of founding-family ownership. J Corporate Finance 14(4):431–445. https://doi.org/10.1016/j.jcorpfin.2008.05.003

Anusic I, Yap SCY, Lucas RE (2014) Does personality moderate reaction and adaptation to major life events? Analysis of life satisfaction and affect in an Australian national sample. J Res Personality 51:69–77. https://doi.org/10.1016/j.jrp.2014.04.009

Arráiz I, Bruhn M, Stucchi R (2017) Psychometrics as a tool to improve credit information. World Bank Econ Rev 30(Supplement 1):S67–S76

Arslan RC, Brümmer M, Dohmen T, Drewelies J, Hertwig R, Wagner GG (2020) How people know their risk preference. Sci Rep 10(1):15365. https://doi.org/10.1038/s41598-020-72077-5

Asendorpf JB, van Aken MAG (1999) Resilient, overcontrolled, and undercontrolled personality prototypes in childhood: replicability, predictive power, and the trait-type issue. J Personal Soc Psychol 77(4):815–832. https://doi.org/10.1037/0022-3514.77.4.815

Atkinson AB, Piketty T, Saez E (2011) Top incomes in the long run of history. J Econ Lit 49(1):3–71. https://doi.org/10.1257/jel.49.1.3

Barsky RB, Juster FT, Kimball MS, Shapiro MD (1997) Preference parameters and behavioral heterogeneity: an experimental approach in the health and retirement study. Q J Econ 112(2):537–579. https://doi.org/10.1162/003355397555280

Bartels LM (2009) Economic inequality and political representation. In: Jacobs L, King D (Eds.) The unsustainable American state. Oxford University Press, 167–196

Bertrand M, Bombardini M, Fisman R, Trebbi F (2018) Tax-exempt lobbying: corporate philanthropy as a tool for political influence. National Bureau of Economic Research Working Paper Series, No. 24451. https://doi.org/10.3386/w24451

Betermier S, Jansson T, Parlour C, Walden J (2012) Hedging labor income risk. J Fin Econ 105(3):622–639. https://doi.org/10.1016/j.jfineco.2012.05.001

Blanchflower DG, Oswald AJ (2004) Money, sex and happiness: an Empirical Study. Scand J Econ 106(3):393–415. https://doi.org/10.1111/j.0347-0520.2004.00369.x

Borghans L, Duckworth AL, Heckman JJ, Ter Weel B (2008) The economics and psychology of personality traits. J Hum Resour 43(4):972–1059. https://doi.org/10.3368/jhr.43.4.972

Bourdieu P (1984) Distinction: a social critique of the judgment of taste. Harvard University Press.

Bourdieu P (1990) The logic of practice. Stanford University Press.

Bratt AS, Stenström U, Rennemark M (2018) Exploring the most important negative life events in older adults bereaved of child, spouse, or both. OMEGA 76(3):227–236. https://doi.org/10.1177/0030222816642453

Buyl T, Boone C, Wade JB (2019) CEO narcissism, risk-taking, and resilience: an empirical analysis in US commercial banks. J Manag 45(4):1372–1400. https://doi.org/10.1177/0149206317699521

Cagetti M, De Nardi M (2006) Entrepreneurship, frictions, and wealth. J Polit Econ 114(5):835–870. https://doi.org/10.1086/508032

Cagetti M, De Nardi M (2008) Wealth inequality: data and models. Macroecon Dyn 12(S2):285–313. https://doi.org/10.1017/S1365100507070150

Caliendo M, Fossen F, Kritikos AS (2014) Personality characteristics and the decisions to become and stay self-employed. Small Bus Econ 42(4):787–814. https://doi.org/10.1007/s11187-013-9514-8

Caliendo M, Fossen FM, Kritikos AS (2009) Risk attitudes of nascent entrepreneurs—new evidence from an experimentally validated survey. Small Bus Econ 32(2):153–167. https://doi.org/10.1007/s11187-007-9078-6

Cass D, Stiglitz JE (1972) Risk aversion and wealth effects on portfolios with many assets. Rev Econ Stud 39(3):331. https://doi.org/10.2307/2296363

Cheung F, Lucas RE (2016) Income inequality is associated with stronger social comparison effects: the effect of relative income on life satisfaction. J Personal Soc Psychol 110(2):332–341. https://doi.org/10.1037/pspp0000059

Chopik WJ (2018) Does personality change following spousal bereavement? J Res Personal 72:10–21. https://doi.org/10.1016/j.jrp.2016.08.010

Clark AE, Georgellis Y (2013) Back to baseline in Britain: adaptation in the British Household Panel Survey. Economica 80(319):496–512. https://doi.org/10.1111/ecca.12007

Cronbach LJ, Gleser GC (1953) Assessing similarity between profiles. Psychol Bull 50(6):456–473. https://doi.org/10.1037/h0057173

Damian RI, Su R, Shanahan M, Trautwein U, Roberts BW (2015) Can personality traits and intelligence compensate for background disadvantage? Predicting status attainment in adulthood. J Personal Soc Psychol 109(3):473–489. https://doi.org/10.1037/pspp0000024

De Nardi M, Fella G (2017) Saving and wealth inequality. Rev Econ Dyn 26:280–300. https://doi.org/10.1016/j.red.2017.06.002

Denissen JJA, Luhmann M, Chung JM, Bleidorn W (2019) Transactions between life events and personality traits across the adult lifespan. J Personal Soc Psychol 116(4):612–633. https://doi.org/10.1037/pspp0000196

Di Tella R, Haisken-De New J, MacCulloch R (2010) Happiness adaptation to income and to status in an individual panel. J Econ Behav Organ 76(3):834–852. https://doi.org/10.1016/j.jebo.2010.09.016

Diener E, Diener M (2009) Cross-cultural correlates of life satisfaction and self-esteem. In: Diener E (Ed.) Culture and well-being, vol 3810. Springer, Netherlands, pp. 71–91

Dohmen T, Falk A, Huffman D, Sunde U, Schupp J, Wagner GG (2011) Individual risk attitudes: measurement, determinants, and behavioral consequences. J Eur Econ Assoc 9(3):522–550. https://doi.org/10.1111/j.1542-4774.2011.01015.x

Donnelly GE, Zheng T, Haisley E, Norton MI (2018) The amount and source of millionaires’ wealth (moderately) predict their happiness. Personal Soc Psychol Bull 44(5):684–699. https://doi.org/10.1177/0146167217744766

Donnelly G, Iyer R, Howell RT (2012) The Big Five personality traits, material values, and financial well-being of self-described money managers. J Econ Psychol 33(6):1129–1142. https://doi.org/10.1016/j.joep.2012.08.001

Federal Statistical Office of Germany (n.d.) Bevölkerung nach Altersgruppen (ab 2011) Bevölkerung nach Altersgruppen (ab 2011)—Statistisches Bundesamt. https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Bevoelkerung/Bevoelkerungsstand/Tabellen/liste-altersgruppen.html. Accessed 23 Nov 2021

Fiske ST, Markus HR (2012) Facing social class: How societal rank influences interaction. Russell Sage Foundation.

Fuentes-Nieva R, Galasso N (2014) Working for the few: political capture and economic inequality, No. 178. Oxfam. https://oxf.am/2FKRUWh

Gerber AS, Huber GA, Doherty D, Dowling CM, Ha SE (2010) Personality and political attitudes: relationships across issue domains and political contexts. Am Political Sci Rev 104(1):111–133. https://doi.org/10.1017/S0003055410000031

Gerlitz J-Y, Schupp J (2005) Zur Erhebung der Big-Five-basierten Persönlichkeitsmerkmale im SOEP. DIW Berlin.

Giesselmann M, Bohmann S, Goebel J, Krause P, Liebau E, Richter D, Schacht D, Schröder C, Schupp J, Liebig S (2019) The individual in context(s): research potentials of the Socio-Economic Panel Study (SOEP) in sociology. Eur Sociol Rev 35(5):738–755. https://doi.org/10.1093/esr/jcz029

Goebel J, Grabka MM, Liebig S, Kroh M, Richter D, Schröder C, Schupp J(2019) The German Socio-Economic Panel (SOEP) Jahrb Nationalökon Stat 239(2):345–360. https://doi.org/10.1515/jbnst-2018-0022

Götz FM, Ebert T, Rentfrow, PJ (2018) Regional cultures and the psychological geography of switzerland: person–environment–fit in personality predicts subjective wellbeing. Front Psychol 9. https://doi.org/10.3389/fpsyg.2018.00517

Grosz MP, Leckelt M, Back MD (2020) Personality predictors of social status attainment. Curr Opin Psychol 33:52–56. https://doi.org/10.1016/j.copsyc.2019.07.023

Hahn E, Gottschling J, Spinath FM (2012) Short measurements of personality—validity and reliability of the GSOEP Big Five Inventory (BFI-S). J Res Personal 46(3):355–359. https://doi.org/10.1016/j.jrp.2012.03.008

Hertwig R, Wulff DU, Mata R (2019) Three gaps and what they may mean for risk preference. Philos Trans R Soc B: Biol Sci 374(1766):20180140. https://doi.org/10.1098/rstb.2018.0140

Hvide HK, Panos GA (2014) Risk tolerance and entrepreneurship. J Fin Econ 111(1):200–223. https://doi.org/10.1016/j.jfineco.2013.06.001

Iglesias JR, Gonçalves S, Abramson G, Vega JL (2004) Correlation between risk aversion and wealth distribution. Physica A 342(1–2):186–192. https://doi.org/10.1016/j.physa.2004.04.077

Infurna FJ, Luthar SS (2017) The multidimensional nature of resilience to spousal loss. J Personal Soc Psychol 112(6):926–947. https://doi.org/10.1037/pspp0000095

Jain AK (2001) Corruption: a review. J Econ Surv 15(1):71–121. https://doi.org/10.1111/1467-6419.00133

John OP, Naumann LP, Soto CJ (2008) Paradigm shift to the integrative big five trait taxonomy. Handb Personal: Theory Res 3(2):114–158

Kahneman D, Deaton A (2010) High income improves evaluation of life but not emotional well-being. Proc Natl Acad Sci USA 107(38):16489–16493. https://doi.org/10.1073/pnas.1011492107

Kennickell AB, Woodburn RL (1999) Consistent weights design for the 1989, 1992 and1995 SCFs, and the distribution of wealth. Rev Income Wealth 45(2):193–215. https://doi.org/10.1111/j.1475-4991.1999.tb00328.x

King AG (1974) Occupational choice, risk aversion, and wealth. ILR Rev 27(4):586–596. https://doi.org/10.1177/001979397402700407

Klinger B, Khwaja AI, Del Carpio C (2013) Enterprising psychometrics and poverty reduction, vol 860. Springer.

König J, Schröder C, Wolff EN (2020) Wealth Inequalities. In: Zimmermann KF (ed) Handbook of labor, human resources and population economics. Springer International Publishing, pp. 1–38

Kopczuk W, Zwick E (2020) Business incomes at the top. J Econ Perspect 34(4):27–51. https://doi.org/10.1257/jep.34.4.27

Kroh M, Kühne S, Siegers R, Belcheva V (2018) Documentation of sample sizes and panel attrition of SOEP-core (1984 until 2016), No. 480; SOEP Survey Paper. DIW Berlin.

Leckelt M, Richter D, Schröder C, Küfner ACP, Grabka MM, Back MD (2019) The rich are different: unravelling the perceived and self‐reported personality profiles of high‐net‐worth individuals. Br J Psychol 110(4):769–789. https://doi.org/10.1111/bjop.12360

Leopold T, Lechner CM (2015) Parents’ death and adult well-being: gender, age, and adaptation to filial bereavement. J Marriage Fam 77(3):747–760. https://doi.org/10.1111/jomf.12186

Manning A (2013) Monopsony in motion: imperfect competition in labor markets. Princeton University Press.

Mata R, Frey R, Richter D, Schupp J, Hertwig R (2018) Risk preference: a view from psychology. J Econ Perspect 32(2):155–172. https://doi.org/10.1257/jep.32.2.155

McCrae RR, Costa PT (1997) Personality trait structure as a human universal. Am Psychol 52(5):509–516. https://doi.org/10.1037/0003-066X.52.5.509

Miller JD, Maples JL, Buffardi L, Cai H, Gentile B, Kisbu-Sakarya Y, Kwan VSY, LoPilato A, Pendry LF, Sedikides C, Siedor L, Campbell WK (2015) Narcissism and United States’ culture: the view from home and around the world. J Personal Soc Psychol 109(6):1068–1089. https://doi.org/10.1037/a0039543

Obschonka M, Schmitt-Rodermund E, Silbereisen RK, Gosling SD, Potter J (2013) The regional distribution and correlates of an entrepreneurship-prone personality profile in the United States, Germany, and the United Kingdom: a socioecological perspective. J Personal Soc Psychol 105(1):104–122. https://doi.org/10.1037/a0032275

Obschonka M, Silbereisen RK, Schmitt-Rodermund E (2010) Entrepreneurial intention as developmental outcome. J Vocat Behav 77(1):63–72. https://doi.org/10.1016/j.jvb.2010.02.008

Paravisini D, Rappoport V, Ravina E (2017) Risk aversion and wealth: evidence from person-to-person lending portfolios. Manag Sci 63(2):279–297. https://doi.org/10.1287/mnsc.2015.2317

Quadrini V (1999) The importance of entrepreneurship for wealth concentration and mobility. Rev Income Wealth 45(1):1–19. https://doi.org/10.1111/j.1475-4991.1999.tb00309.x

Raub B, Johnson B, Newcomb J (2010) A comparison of wealth estimates for America’s wealthiest descendants using tax data and data from the Forbes 400. In: Kopczuk and Scholz (ed)Proceedings of the annual conference on taxation and minutes of the annual meeting of the National Tax Association, vol 103. pp. 128–135. National Tax Association

Roberts BW, Luo J, Briley DA, Chow PI, Su R, Hill PL (2017) A systematic review of personality trait change through intervention. Psychol Bull 143(2):117–141. https://doi.org/10.1037/bul0000088

Robins RW, John OP, Caspi A, Moffitt TE, Stouthamer-Loeber M (1996) Resilient, overcontrolled, and undercontrolled boys: three replicable personality types. J Personal Soc Psychol 70(1):157–171. https://doi.org/10.1037/0022-3514.70.1.157

Sanders WMG, Hambrick DC (2007) Swinging for the fences: the effects of CEO stock options on company risk taking and performance. Acad Manag J 50(5):1055–1078. https://doi.org/10.5465/amj.2007.27156438

Scheuer F, Slemrod J (2020) Taxation and the superrich. Annu Rev Econ 12(1):189–211. https://doi.org/10.1146/annurev-economics-081919-115106

Schröder C, Bartels C, Grabka MM, König J, Kroh M, Siegers R (2020) A novel sampling strategy for surveying high net‐worth individuals—a pretest application using the socio‐economic panel. Rev Income Wealth 66(4):825–849. https://doi.org/10.1111/roiw.12452

Schröder C, König J, Fedorets A, Goebel J, Grabka MM, Lüthen H, Metzing M, Schikora F, Liebig S (2020) The economic research potentials of the German Socio-Economic Panel study. German Econ Rev 21(3):335–371. https://doi.org/10.1515/ger-2020-0033

Smeets P, Bauer R, Gneezy U (2015) Giving behavior of millionaires. Proc Natl Acad of Sci USA 112(34):10641–10644. https://doi.org/10.1073/pnas.1507949112

Smeets P, Whillans A, Bekkers R, Norton MI (2019) Time use and happiness of millionaires: evidence from the Netherlands. Soc Psychol Personal Sci https://doi.org/10.1177/1948550619854751

Wales WJ, Patel PC, Lumpkin GT (2013) In Pursuit of Greatness: CEO narcissism, entrepreneurial orientation, and firm performance variance. J Manag Stud 50(6):1041–1069. https://doi.org/10.1111/joms.12034

Whillans AV, Dunn EW (2018) Agentic appeals increase charitable giving in an affluent sample of donors. PLoS ONE 13(12):e0208392. https://doi.org/10.1371/journal.pone.0208392

Acknowledgements

We would like to thank Jasmin Leckelt for her help in creating Fig. 1 as well as Deborah Anne Bowen for her support with copy-editing. Support came from the German Federal Ministry of Education and Research and the German Federal Ministry of Labour and Social Affairs through grants for initiating and continuing SOEP-P. Further support came from the German Research Foundation (DFG) through Project #430972113.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Ethical approval

As this study involved only secondary analysis of anonymised data, ethical approval was not required.

Informed consent

Informed consent was obtained from all participants.

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Leckelt, M., König, J., Richter, D. et al. The personality traits of self-made and inherited millionaires. Humanit Soc Sci Commun 9, 94 (2022). https://doi.org/10.1057/s41599-022-01099-3

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-022-01099-3