Abstract

Countries such as China are facing a bottleneck in their paths to carbon neutrality: abating emissions in heavy industries and heavy-duty transport. There are few in-depth studies of the prospective role for clean hydrogen in these ‘hard-to-abate’ (HTA) sectors. Here we carry out an integrated dynamic least-cost modelling analysis. Results show that, first, clean hydrogen can be both a major energy carrier and feedstock that can significantly reduce carbon emissions of heavy industry. It can also fuel up to 50% of China’s heavy-duty truck and bus fleets by 2060 and significant shares of shipping. Second, a realistic clean hydrogen scenario that reaches 65.7 Mt of production in 2060 could avoid US$1.72 trillion of new investment compared with a no-hydrogen scenario. This study provides evidence of the value of clean hydrogen in HTA sectors for China and countries facing similar challenges in reducing emissions to achieve net-zero goals.

Similar content being viewed by others

Main

Achieving carbon neutrality is an urgent global mission, but there is no ‘one-size-fits-all’ pathway for major emitting nations to meet this objective1,2. Most developed nations, such as the United States and those in Europe, are pursuing decarbonization strategies focused especially on large light-duty vehicle (LDV) fleets, electric power generation, manufacturing and commercial and residential buildings, four sectors that together account for vast majorities of their carbon emissions3,4. Major developing-country emitters, such as China, by contrast, have very different economies and energy structures, requiring different decarbonization priorities not only in sectoral terms but also in strategic deployment of emerging zero-carbon technologies.

Key distinctions of China’s carbon emissions profile compared with those of western economies are much larger emission shares for heavy industries and much smaller fractions for LDVs and energy use in buildings (Fig. 1). China ranks first in the world, by far, in terms of production of cement, iron and steel, chemicals and building materials, consuming huge amounts of coal for industrial heat and production of coke. Heavy industry contributes 31% of China’s current total emissions, a share that is 8% higher than the world average (23%), 17% greater than that of the United States (14%) and 13% higher than that of the European Union (18%) (ref. 5).

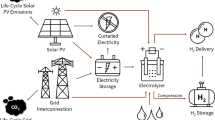

a, China’s carbon emissions in 2019 compared with the United States, Europe, Japan and India, by fuel. In 2019, coal combustion took the largest share of the carbon emissions in China (79.62%) and India (70.52%), and oil combustion contributed most to the carbon emissions in the United States (41.98%) and Europe (41.27%). b, China’s carbon emissions in 2019 compared with the United States, Europe, Japan and India, by sector. Emissions are displayed on the left and proportion on the right in a and b. The proportion of carbon emissions from industry in China (28.10%) and India (24.75%) was much higher than that of the United States (9.26%) and Europe (13.91%) in 2019. c, Technical pathway with hydrogen technologies applied in the HTA sectors. SMR, steam methane reforming; PEM electrolysis, polymer electrolyte membrane electrolysis; PEC process, photoelectrochemical process.

China has pledged to peak its carbon emissions before 2030 and achieve carbon neutrality before 2060. These climate pledges earned widespread praise but also raised questions about their feasibility6, in part because of the major role of ‘hard-to-abate’ (HTA) processes in China’s economy. These processes notably include energy use in heavy industry and heavy-duty transport that will be difficult to electrify (and thus to transition directly to renewable power) and industrial processes now dependent on fossil fuels for chemical feedstocks.

There have been a few recent studies1,2,3 investigating decarbonization pathways towards carbon neutrality for China’s overall energy system planning but with limited analyses of HTA sectors. Internationally, potential mitigation solutions for HTA sectors have begun to draw attention in recent years7,8,9,10,11,12,13,14. The decarbonization of HTA sectors is challenging because they are difficult to electrify fully and/or cost effectively7,8. Åhman emphasized that path dependency is the key problem for HTA sectors and that vision and long-term planning for advanced technologies are needed to ‘unlock’ the HTA sectors, especially heavy industries, from fossil dependency9. Studies have explored new materials and mitigation solutions related to carbon capture, use and/or storage (CCUS) and negative emission technologies (NETs)10,11. However, clean hydrogen options are often not included; the authors of at least one study acknowledge that they should also be considered in long-term planning11. In the recently released Sixth Assessment Report of the Intergovernmental Panel on Climate Change, the use of ‘low-emission’ hydrogen was recognized as one of the key mitigation solutions for multiple sectors towards achieving a net-zero emissions future12.

The existing literature on clean hydrogen is focused largely on production technology options with analyses of supply-side costs15. (‘Clean’ hydrogen in this paper includes both ‘green’ and ‘blue’ hydrogen, the former produced by water electrolysis using renewable power, the latter sourced from fossil fuels but decarbonized with CCUS.) Discussion of hydrogen demand is focused largely on the transportation sector in developed countries—hydrogen fuel cell vehicles in particular16,17. Pressures for decarbonization of heavy industries have lagged compared with those for road transport, reflecting conventional assumptions that heavy industry will remain particularly hard to abate until new technological innovations emerge. Studies of clean (especially green) hydrogen have demonstrated its technological maturity and declining costs17, but further studies are needed that focus on the size of potential markets and technological requirements of industries to exploit prospective growth of the clean hydrogen supply16. Understanding the potential of clean hydrogen to advance global carbon neutrality will be inherently biased if analyses are limited mainly to the costs of its production, its consumption by favoured sectors only and its application in developed economies.

Evaluating opportunities for clean hydrogen depends on reassessing its prospective demands as an alternative fuel and chemical feedstock across the entire energy system and economy, including consideration of differing national circumstances. There is no such comprehensive study to date on the role of clean hydrogen in China’s net-zero future. Filling this research gap will help draw a clearer roadmap for China’s CO2 emissions reduction, allow evaluation of the feasibility of its 2030 and 2060 decarbonization pledges and provide guidance for other growing developing economies with large heavy-industrial sectors.

This study seeks to answer three key inquiries. First, what are the key challenges for decarbonization of HTA sectors in developing countries such as China, as distinguished from those of developed countries? Are current mitigation technologies in HTA sectors (especially heavy industry) effective enough to achieve China’s carbon neutrality by 2060? Second, what are the prospective roles for clean hydrogen as both an energy carrier and feedstock in HTA sectors, especially in China and other developing countries that have just begun to access its prospective production and use? Finally, based on dynamic optimization of China’s entire energy system, would widespread application of clean hydrogen in HTA sectors be cost effective compared with other options?

Here we build a model of an integrated energy system including both supply and demand across sectors to analyse the prospective cost effectiveness and roles of clean hydrogen in China’s entire economy, with emphasis on the under-researched HTA sectors (Fig. 1c). Results of the analysis show that reliance on improvement of energy efficiency combined with CCUS and NETs alone is unlikely to be a cost-effective path for deep decarbonization of China’s HTA sectors, especially heavy industries. More specifically, widespread application of clean hydrogen in HTA sectors can help China achieve carbon neutrality cost effectively compared with a scenario without clean hydrogen production and use. The results provide strong guidance for China’s HTA decarbonization pathway and a valuable reference for other countries facing similar challenges.

Decarbonizing HTA industrial sectors with clean hydrogen

We carry out an integrated least-cost optimization of mitigation pathways to carbon neutrality for China in 2060. Four modelling scenarios are defined in Table 1: business as usual (BAU), China’s Nationally Determined Contributions under the Paris Agreement (NDC), net-zero emissions with no-hydrogen applications (ZERO-NH) and net-zero emissions with clean hydrogen (ZERO-H). HTA sectors in this study include industrial production of cement, iron and steel and key chemicals (including ammonia, soda and caustic soda) and heavy-duty transport, including trucking and domestic shipping. Full details are provided in the Methods section and Supplementary Notes 1–5.

Regarding the iron and steel sector, the dominant share of existing production in China (89.6%) is by the basic oxygen-blast furnace process, a key challenge for deep decarbonization of this industry. The electric arc furnace process comprised only 10.4% of total production in China in 2019, which is 17.5% less than the world average share and 59.3% less than that for the United States18. We analysed 60 key steelmaking emissions mitigation technologies in the model and classified them into six categories (Fig. 2a): improvement of material efficiency, advanced technology performance, electrification, CCUS, green hydrogen and blue hydrogen (Supplementary Table 1).

a, Six categories of 60 key steelmaking emissions mitigation technologies. b, Six categories of 47 key cement emissions mitigation technologies. The technologies are listed by number, with corresponding definitions included in Supplementary Table 1 for a and Supplementary Table 2 for b. The technology readiness levels (TRLs) of each technology are marked: TRL3, concept; TRL4, small prototype; TRL5, large prototype; TRL6, full prototype at scale; TRL7, pre-commercial demonstration; TRL8, demonstration; TRL10, early adoption; TRL11, mature.

Comparing the system cost optimizations of ZERO-H with NDC and ZERO-NH scenarios shows that inclusion of clean hydrogen options would yield notable carbon reduction due to introduction of hydrogen-direct reduction of iron (hydrogen-DRI) processes. Note that hydrogen can serve not only as an energy source in steelmaking but also as a carbon-abating reducing agent on a supplementary basis in the Blast Furnance-Basic Oxygen Furnance (BF-BOF) process and 100% in the hydrogen-DRI route. Under ZERO-H, the share of BF-BOF would be reduced to 34% in 2060, with 45% electric arc furnace and 21% hydrogen-DRI, and clean hydrogen would supply 29% of total final energy demand in the sector. With the grid price for solar and wind power expected to decline to US$38–40 MWh−1 in 205019, the cost of green hydrogen will also decline, and the 100% hydrogen-DRI route may play a more important role than previously recognized.

Regarding cement production, the model includes 47 key mitigation technologies across the production processes classified into six categories (Supplementary Tables 2 and 3): energy efficiency, alternative fuels, reducing the clinker-to-cement ratio, CCUS, green hydrogen and blue hydrogen (Fig. 2b). Results show that improved energy efficiency technologies can reduce only 8–10% of the total CO2 emissions in the cement sector, and waste-heat cogeneration and oxy-fuel technologies will have limited mitigation effect (4–8%). Technologies to reduce the clinker-to-cement ratio can yield relatively high carbon mitigation (50–70%), mainly including decarbonized raw materials for clinker production using granulated blast furnace slag, although critics question if the resulting cement will retain its essential qualities. But current results indicate that utilization of hydrogen together with CCUS could help the cement sector achieve near-zero CO2 emissions in 2060.

In the ZERO-H scenario, 20 hydrogen-based technologies (out of the 47 mitigation technologies) come into play in cement production. We find that the average carbon abatement cost of hydrogen technologies is lower than typical CCUS and fuel switching approaches (Fig. 2b). Furthermore, green hydrogen is expected to be cheaper than blue hydrogen after 2030 as discussed in detail below, at around US$0.7–US$1.6 kg−1 H2 (ref. 20), bringing significant CO2 reductions in the provision of industrial heat in cement making. Current results show that it can reduce 89–95% of the CO2 from the heating process in China’s industry (Fig. 2b, technologies 28–47), which is consistent with the Hydrogen Council’s estimate of 84–92% (ref. 21). Clinker process emissions of CO2 must be abated by CCUS in both ZERO-H and ZERO-NH.

We also simulate use of hydrogen as a feedstock in production of ammonia, methane, methanol and other chemicals listed in the model description. In the ZERO-H scenario, gas-based ammonia production with hydrogen heat will gain a 20% share of total production in 2060 (Fig. 3 and Supplementary Table 4). The model includes four kinds of methanol production technologies: coal to methanol (CTM), coke gas to methanol (CGTM), natural gas to methanol (NTM) and CGTM/NTM with hydrogen heat. In the ZERO-H scenario, CGTM/NTM with hydrogen heat can achieve a 21% production share in 2060 (Fig. 3). Chemicals are also potential energy carriers of hydrogen. On the basis of our integrated analysis, hydrogen can comprise 17% of final energy consumption for heat provision in the chemical industry by 2060. Along with bioenergy (18%) and electricity (32%), hydrogen has a major role to play in decarbonization of China’s HTA chemical industry (Fig. 4a).

Results under BAU, NDC, ZERO-NH and ZERO-H scenarios (2020–2060). In each milestone year, the specific technology penetration in different sectors is shown by the coloured bars, where each bar is a percentage of penetration up to 100% (for a fully shaded lattice). The technologies are further classified by different types (shown in the legends). CNG, compressed natural gas; LPG, liquid petroleum gas; LNG, liquid natural gas; w/wo, with or without; EAF, electric arc furnace; NSP, new suspension preheater dry process; WHR, waste heat recovery.

a, CO2 trajectory in BAU, NDC and ZERO-NH (2020–2060). b, CO2 trajectory in BAU, NDC and ZERO-H (2020–2060). The ranges in green show the INDC (Intended Nationally Determined Contributions) mitigation range. The ranges in blue are the negative emissions needed to offset the total emission to achieve net-zero, the amount in ZERO-NH in a is larger than in ZERO-H in b (1.09 billion tons larger in 2030 and 1.23 billion tons larger in 2060). c, Carbon mitigation costs in 2060, compared with BAU scenario. GDP is the gross domestic product. d, Total final energy consumption in BAU, NDC, ZERO-NH, ZERO-H scenarios (2020–2060). The green arrow shows the amount of hydrogen consumption in 2060 in ZERO-H which is 56.7 Mt. e, Primary energy mix in BAU, NDC, ZERO-NH, ZERO-H scenarios (2030–2060).

Decarbonizing HTA transportation modes with clean hydrogen

On the basis of the modelling results, hydrogen also has large potential to decarbonize China’s transport sector, although it will take time. In addition to LDVs, other transport modes analysed in the model include fleet buses, trucks (light/small/medium/heavy), domestic shipping and railways, covering most transportation in China. For LDVs, electric vehicles look to remain cost competitive in the future. In ZERO-H, hydrogen fuel cell (HFC) penetration of the LDV market will reach only 5% in 2060 (Fig. 3). For fleet buses, however, HFC buses will be more cost competitive than electric alternatives in 2045 and comprise 61% of the total fleet in 2060 in the ZERO-H scenario, with the remainder electric (Fig. 3). As for trucks, the results vary by load rate. Electric propulsion will drive more than half of the total light-duty truck fleet by 2035 in ZERO-NH. But in ZERO-H, HFC light-duty trucks will be more competitive than electric light-duty trucks by 2035 and comprise 53% of the market by 2060. Regarding heavy-duty trucks, HFC heavy-duty trucks would reach 66% of the market in 2060 in the ZERO-H scenario. Diesel/bio-diesel/CNG (compressed natural gas) HDVs (heavy-duty vehicles) will quit the market after 2050 in both ZERO-NH and ZERO-H scenarios (Fig. 3). HFC vehicles have an additional advantage over electric vehicles in their better performance in cold conditions, important in northern and western China.

Beyond road transport, the model shows widespread adoption of hydrogen technologies in shipping in the ZERO-H scenario. China’s domestic shipping is very energy intensive and an especially difficult decarbonization challenge. Clean hydrogen, especially as a feedstock for ammonia, provides an option for shipping decarbonization. The least-cost solution in the ZERO-H scenario results in 65% penetration of ammonia-fuelled and 12% of hydrogen-fuelled ships in 2060 (Fig. 3). In this scenario, hydrogen will account for an average of 56% of the final energy consumption of the entire transport sector in 2060. We also modelled hydrogen use in residential heating (Supplementary Note 6), but its adoption is negligible and this paper focuses on hydrogen use in HTA industries and heavy-duty transport.

Cost savings of carbon neutrality using clean hydrogen

China’s carbon-neutral future will be characterized by renewable energy dominance, with a phasing out of coal in its primary energy consumption (Fig. 4). Non-fossil fuels comprise 88% of the primary energy mix in 2050 and 93% in 2060 under ZERO-H. Wind and solar will supply half of primary energy consumption in 2060. On average, nationally, the clean hydrogen share of total final energy consumption (TFEC) could reach 13% in 2060. Considering regional heterogeneity of production capacities in key industries by region (Supplementary Table 7), there are ten provinces with hydrogen shares of TFEC higher than the national average, including Inner Mongolia, Fujian, Shandong and Guangdong, driven by rich solar and onshore and offshore wind resources and/or multiple industrial demands for hydrogen.

In the ZERO-NH scenario, the cumulative investment cost to achieve carbon neutrality up to 2060 would be $20.63 trillion, or 1.58% of the aggregate gross domestic product (GDP) for 2020–2060. The average additional investment on an annual basis would be around US$516 billion per year. This result is consistent with China’s US$15 trillion mitigation plan up to 2050, an average annual new investment of US$500 billion (ref. 22). However, introducing clean hydrogen options into China’s energy system and industrial feedstocks in the ZERO-H scenario results in a significantly lower cumulative investment of US$18.91 trillion by 2060 and the annual investment would be reduced to less than 1% of GDP in 2060 (Fig. 4). Regarding the HTA sectors, the annual investment cost in those sectors would be around US$392 billion per year in the ZERO-NH scenario, which is consistent with the projection of the Energy Transition Commission (US$400 billion) (ref. 23). However, if clean hydrogen is incorporated into the energy system and chemical feedstocks, the ZERO-H scenario indicates the annual investment cost in HTA sectors could be reduced to US$359 billion, chiefly by reducing reliance on costly CCUS or NETs. Our results suggest that the use of clean hydrogen can save US$1.72 trillion in investment cost and avoid a 0.13% loss in the aggregate GDP (2020–2060) compared with a pathway without hydrogen up to 2060.

In the least-cost pathway of ZERO-H, consumption of hydrogen increases continually to 12.8% of the TFEC in 2060. For comparison, the projection of the China Hydrogen Energy Alliance is that hydrogen (of all types, fossil-derived and clean) will account for 10% of energy consumption in 205024. Our analysis shows that in 2050, around 9.8% of the TFEC would be supplied by clean hydrogen alone. We believe this target in 2050 is achievable as renewable energy costs continue their decline, possibly accelerated further by government subsidies.

The hydrogen proportions in final energy consumptions of end-use sectors are shown in Fig. 5a, and key hydrogen production modes up to 2060 are shown in Fig. 5b. Note that hydrogen is currently produced as a by-product of chemical processes, especially steam cracking (mainly of ethane and naphtha) and chlor-alkali and styrene production. Under ZERO-H, by-product hydrogen will increase from 0.78 Mt in 2030 to 14.50 Mt in 2060. In this scenario, clean hydrogen production is dominated by blue hydrogen from coal or methane gasification with CCUS (in large-scale, centralized facilities) until 2040. Green hydrogen will grow significantly after 2030 with increasing cost effectiveness. In this scenario, alkaline electrolysis cells (AEC) will play a dominant role until 2050, based on cost assumptions from the International Renewable Energy Agency (IRENA) and Danish Energy Agency25,26 (Supplementary Table 5). Nevertheless, declining costs and higher efficiencies will make hydrogen production from solid oxide electrolysis cells (SOEC) and proton exchange membrane electrolysis cells increasingly competitive over time, especially in large centralized installations, and their production will increase to 19.36 Mt and 18.10 Mt, respectively, in 2060 (Fig. 5b), comprising more than half of total hydrogen production (56.9%).

a, Final energy mix in the least-cost hydrogen-inclusive net-zero CO2 (ZERO-H) scenario (2060). b, Key hydrogen production technologies in the ZERO-H scenario (2020–2060). PEFC is the polymer electrolyte fuel cell. In a, hydrogen will take notable shares in the final energy mix of 2060 in the sectors of steel (29%), cement (21%), fleet buses (56%), light trucks (53%), mid-size trucks (55%), heavy trucks (66%) and shipping (a sum up of 77% for hydrogen and ammonia). In b, hydrogen production based on large-scale centralized alkaline electrolyzers will increase from 72 PJ in 2020 to 1,197 PJ in 2060, and the hydrogen production based on SOEC and PEFC will increase faster than alkaline electrolyzers and achieve up to 2,322 PJ and 2,171 PJ in 2060.

Green hydrogen advantages over blue hydrogen

If clean hydrogen is valuable for decarbonizing the HTA sectors, a question then is which type of hydrogen is most cost competitive for a fossil fuel-dominated country such as China? Our results and those of other sources indicate that green hydrogen can be cost competitive with blue hydrogen before 2040, even in fossil fuel-dominated China. Studies by IRENA and ITM Power are similarly optimistic about green hydrogen, with cost estimates of US$1.6–3.3 kg−1 of H2 in 205025,27. Bloomberg New Energy Finance projects that the cost of green hydrogen will reach even lower levels (US$0.7–1.6 kg−1). The US Department of Energy estimates that green hydrogen will be economically competitive only when it costs less than US$2 kg−1 H2 (ref. 28). Our results indicate that the average cost of China’s green hydrogen can be reduced to US$2 kg−1 H2 by 2037 and US$1.2 kg−1 by 2050, when it will be much more cost effective than blue hydrogen (US$1.9 kg−1). China has rich untapped resources of solar and wind energy (both onshore and offshore)29,30, giving it significant advantages in production of green hydrogen.

We further evaluate the effects if only green or blue hydrogen is allowed in the ZERO-H scenario. If only blue hydrogen is permitted, the aggregate investment cost will be around US$19.54 trillion, US$0.63 trillion higher than a clean hydrogen (green hydrogen and blue hydrogen) scenario. Several factors favour green hydrogen in the market. First, the costs of renewables in China are increasingly competitive. If electrolysers use otherwise-curtailed (that is, effectively costless) wind and solar power instead of grid electricity, the total cost will be even lower. Second, China’s renewable sources are geographically concentrated, with onshore wind and solar concentrated in the north and northwest, while offshore wind is concentrated along the southeast coast. Green hydrogen production, storage and transport is advantaged when the needed infrastructure can also be concentrated, that is, co-located in renewable-rich areas, further bringing the total costs down compared with a more distributed hydrogen production system. This result is a rejoinder to concerns that lower costs of blue hydrogen could lock China into another round of fossil fuel investments if it pursues clean hydrogen. From the perspectives of both emissions reduction potentials and costs, green hydrogen appears to be China’s strongest option as a centrepiece of a long-term clean hydrogen strategy for decarbonization.

Sensitivity analysis

We assess the sensitivity of results to assumptions by varying key factors of the hydrogen production cost on the supply side, and GDP growth on the demand side. Key assumptions are summarized in Supplementary Table 6 and Supplementary Note 7, with results shown in Fig. 6.

a, CO2 emissions and sectoral contribution in high- and low-GDP scenarios compared with the central case. b, Changes of hydrogen penetration in TFEC compared with the central case. The bars in purple show the decrease of hydrogen proportion in TFEC and the bars in gold show the increase of hydrogen proportion in TFEC. c, Hydrogen penetration in key HTA sectors in 2060 considering changes of hydrogen production costs. d, Technology penetration in iron and steel, cement, ammonia and residential heating sectors in 2060 considering changes of hydrogen production costs. EAF, electric arc furnace; NSP, new suspension preheater dry process; WHR, waste heat recovery. e, Technology penetrations in LDV, bus, heavy truck and shipping transport modes in 2060 considering changes of hydrogen production costs. LNG, liquid natural gas; HDT, heavy-duty truck. f, Aggregate investment changes of the energy system considering changes of hydrogen costs. The green lines are scenarios tested with incremental 1% rates of cost increase between 50% (hydrogen share 10.04% in 2060 TFEC with an aggregate investment of US$19.47 trillion) and 100% (hydrogen share 7.09% in 2060 TFEC with an aggregate investment of US$22.18 trillion) to identify at which rate the ZERO-H scenario would require the same aggregate investment as the ZERO-NH scenario. The result, +87%, helps to reconfirm the considerable cost-competitiveness of clean hydrogen use demonstrated by the current analysis unless its production cost projections are significantly underestimated (Supplementary Note 7).

Higher GDP growth rates may increase the sectoral carbon emissions contributions from HTA sectors in 2050 (Fig. 6a). With efforts towards green recovery in the post-COVID-19 period, China may be more likely to face increasing carbon emissions from HTA sectors and larger challenges to abate them.

Although there is consensus that clean hydrogen production costs will continue to decline, notably according to IRENA, IEA (International Energy Agency) and Bloomberg New Energy Finance17,25, uncertainties remain. First, the hydrogen penetration rate in the TFEC would remain above 10% in 2060 even if hydrogen production costs increases 50% (Fig. 6b). If this cost declines by 30% compared with current levels (Supplementary Table 5), clean hydrogen will contribute 15.4% of TFEC, and a 50% decline would increase the TFEC share to 17.6% in 2060, compared with 12.8% in the central case (Fig. 6b). A more detailed discussion of the results of the sensitivity analysis at the sector and sub-sector levels is presented in Fig. 6c–f and Supplementary Note 8.

Discussion

On the basis of an integrated modelling analysis, this study makes the case that clean hydrogen could provide a basis for cost-effective decarbonization of a wide array of HTA applications in China, helping the country meet its 2060 carbon neutrality target. We also consider the effects of including clean hydrogen options on the aggregate costs of an entire energy system that achieves national carbon goals. Applying clean hydrogen widely in HTA sectors yields a decarbonization pathway in China that is cost effective compared to ones without.

Some caveats of the analysis should be recognized. First, while we evaluated clean hydrogen production technologies carefully, including future efficiency improvements and cost reductions of electrolysis, our treatment of hydrogen transport and storage is simplified, assuming use of trailer trucks and tanks. We do not consider a role for hydrogen pipelines, which raises uncertainties of network effects, metal embrittlement and the feasibility of retrofitting existing gas pipelines31. Second, we do not consider possible indirect effects of widespread hydrogen use, notably the potential of high leak rates to affect air quality and radiative forcing through secondary atmospheric chemistry processes32. Third, we do not consider the short-term (for example, hourly) dynamic complexities of renewable power balancing, which could affect short-term costs of electricity and green hydrogen production. Fourth, the full impacts on society of a clean hydrogen pathway, including on employment, social welfare and public acceptance, could be widespread and significant but are beyond the scope of the study.

While feasible, capitalizing on clean hydrogen in HTA sectors to help achieve carbon neutrality in China by 2060 will require effective policy implementation at both national and sectoral levels. China has historically relied heavily on a priori targets to motivate emissions reductions of both carbon dioxide and air pollutants. Detailed policies to achieve those reductions are typically developed after the aggregate quantitative targets have been set. If China continues this policymaking practice, a clean hydrogen strategy for HTA sectors would first require near- and mid-term emissions reduction targets consistent with its 2060 net-zero commitment. To correct what the Chinese central government considers ineffective ‘campaign-style decarbonization’ at the local level, it has emphasized that its energy transition must be based not on speculative strategies but on proven new energy forms. This study’s systematic and objective evaluation of potential benefits of clean hydrogen, including timelines for its deployment, is consistent with these aims.

Incorporating clean hydrogen into conventional energy planning should recognize that the sizable ongoing curtailment of wind and solar energy across China (due to constraints of power balancing, transmission and other factors) represents a nearly costless renewable energy resource available for green hydrogen production, especially in regions with the highest rates of curtailment. Exploitation of curtailed renewable power for green hydrogen production could improve returns on investment in renewable generation, encouraging higher capacity shares than when left to serve conventional electricity demands alone.

While incorporating clean hydrogen solutions into target-driven national planning for decarbonization may be the conventional and perhaps most likely primary Chinese policy strategy, aggressive use of market-based instruments could strengthen the economic efficiency of such a transition and determine the sequencing of industrial fuel switching to hydrogen based not on top-down planning but on lowest marginal cost of abatement. The most obvious mechanism for achieving this is China’s carbon emission trading system (ETS), which formally came into operation in 2021. Initially covering the power sector alone33, plans for the ETS include expansion to more industries in its next phase, including HTA sectors such as iron and steel and cement. Indeed, HTA heavy industries may be better suited than the power sector for effective implementation of China’s ETS, because pricing of iron and steel, cement and most other industrial commodities, unlike electricity, is not regulated but set by the market. With the cost of carbon passed on to consumers, the market will favour enterprises adopting least-cost decarbonization, which our analysis suggests will often be achieved with clean hydrogen.

Over the longer term, the pace and/or costs of China’s decarbonization of HTA sectors through greater use of clean hydrogen could be influenced by new technology innovations now in early development or unforeseen entirely. One sector-specific example is Sweden’s Hydrogen Breakthrough Ironmaking Technology project, advancing hydrogen-DRI application34. A more general example is the US Advanced Research Projects Agency-Energy, which emphasizes high-impact clean energy innovations that may be too early and high risk to rely solely on private sector investment, sometimes extending support to bridge the ‘valley of death’ to commercialization35. Another example is the climate change programme of the European Commission’s Horizon Project, which similarly funds innovation of ‘next-generation’ technologies at earliest stages36. Should analogous programmes in China lead to technology breakthroughs in clean hydrogen production and use beyond those implied by the learning-curve assumptions of our model, the cost results of our zero-carbon scenarios could conceivably be surpassed.

This dynamic study, focusing on the energy transition in HTA sectors between now and 2060 for China, adds to other studies of China and the world in building a long-term perspective on how mid-century carbon neutrality might be achieved. In a net-zero future, the energy system will be dominated by renewable sources. Green hydrogen offers an opportunity to indirectly extend the benefits of renewable power and accelerate the growth of its capacity share37. China has abundant renewable resources, sufficient to provide for ambitious green hydrogen development in addition to decarbonized conventional electricity supply and demand29,30. China, like other countries, could potentially evolve from a fossil fuel importer into a green hydrogen exporter. Countries should be ready for the emerging new opportunities and challenges of clean hydrogen and rethink its relationship to HTA sectors in their long-term aspirations for a net-zero world.

Methods

Energy system optimization model

The energy system optimization model used in this study is based on a dynamic linear planning programming model featuring algorithms developed by IEA-ETSAP (International Energy Agency-Energy Technology System Analysis Program, https://iea-etsap.org/index.php/etsap-tools). The improvements are based on an in-depth full system modelling exercise conducted for the European Union-funded ‘PARIS REINFORCE’ project of Horizon 2020 (https://paris-reinforce.eu/), for which representative models were selected at the global and national levels to explore a set of new scenarios (https://www.i2am-paris.eu/detailed_model_doc). The specific model used in this study is the China-MAPLE model (Multi-Abatement Planning and Long-term Energy system optimization in China). This model is based on the TIMES (The Integrated MARKAL-EFOM System) modelling framework developed by IEA-ETSAP featuring the TIMES-VEDA tool (https://veda-documentation.readthedocs.io/en/latest/pages/introduction.html).

The MAPLE model provides a technology-rich basis for estimating how an energy system operates from 2015 to 2060, which is consistent with China’s target year for carbon neutrality. It is a dynamic linear programming energy system optimization model with a five-year time step, aligned with China’s system of official national five-year plans. The basic functions and evaluation principles are consistent with IEA-ETSAP and TIMES-VEDA (https://iea-etsap.org/docs/Documentation_for_the_TIMES_Model-Part-I.pdf).

Compared with other models, the one applied in this study has notable improvements. Version 4.0 has better coverage of HTA sectors in China, especially heavy industry. There are over 780 technological processes, of which 579 used in HTA sectors are described in this version. In industry, the key specific industries included are ferrous metal (that is, the iron and steel industry, including coking, sintering, pelleting, furnace and forging processes), non-ferrous metals (copper, aluminium, zinc and lead products, with multiple processes), cement (wet and dry processes and mitigation technologies38), non-metallic commodities (glass, paper and brick), chemicals (Haber–Bosch-processed ammonia, methanol, ethylene, soda, caustic soda, yellow phosphorus and other chemicals) and petroleum-based chemical products. The scenarios of this study are defined in Table 1.

Hydrogen consumption

Unlike electricity, hydrogen is consumed in final-demand sectors both as a feedstock and an energy carrier, introducing complexities. The hydrogen demand in this paper includes its consumption in industries, transport and other sectors. Among industries, hydrogen consumption in key industrial sectors such as iron and steel, cement and ammonia are listed in equations (1–3). In the transport sector, hydrogen is applied in both heavy-freight transport (trucks, railways, shipping) and passenger transport (light-duty vehicles, fleet buses, railways). Equation (4) determines the demand for hydrogen (DH) in the heavy-freight transport.

where t denotes the year; p represents a given technological process within a sector; DMt represents energy service demand in year t; ACT in industrial sectors (1)–(3) denotes industrial production activity, whereas in the heavy-freight transport sector (4), it refers to vehicle stock; EFFp, heat represents the heat efficiency of technological process p; and EFFHt,p is the hydrogen combustion efficiency of technological process p in year t.

Specifically, in the iron & steel sector (STE) (1), hydrogen is not only a combustion fuel to supply heat but also an important reducing agent in the hydrogen-DRI process and a supplemental one in the BF-BOF process; SHt,HYD is the share of processes using hydrogen as reducing agent by the energy system optimization based on the cost analysis; and DMt,STE denotes crude steel demand in year t. Demand for hydrogen in the cement sector (CEM) is determined analogously in equation (2), with hydrogen used as heat supply. In equation (3) for the ammonia sector (AMO), representative of the chemical industry, hydrogen is consumed both as feedstock and combustion fuel for heat, with FEEDHAMO representing the hydrogen consumed as feedstock. Hydrogen consumption in the production of methanol, ethylene, soda, caustic soda, yellow phosphorous and oil refining sectors follow the same structure as that for the ammonia sector. In the transport sector, the heavy-freight transport (HTRU) can serve as an example. In equation (4), SHt,TRU refers to the share of hydrogen fuel cell trucks; SHt,RAI refers to the share of railways that using hydrogen; SHt,SHI refers to the share of shipping that uses hydrogen; DISp,t is the distance travelled in year t by vehicle type p; LOADp,t is the load rate for vehicle type p in year t (that is, tons of freight per vehicle). All heavy-freight transport modes in operation in year t should meet the freight transport service demand in year t, which is represented as DMt,F. Hydrogen demand of passenger transportation modes is determined analogously. A detailed document that includes a full description of the sets, attributes, variables and equations for all the energy demand can be found at https://iea-etsap.org/docs/Documentation_for_the_TIMES_Model-PartII.pdf.

Hydrogen production

In this study, multiple hydrogen production technologies are considered (Supplementary Table 5), including both hydrogen production from fossil fuels and electrolysis. The hydrogen production from fossil fuels includes coal or biomass gasification and natural gas reformation, with and without CCUS. Steam reforming of methane accounts for the largest proportion of this production, mainly due to its low investment cost and high efficiency (up to 76%). Gasification of coal to produce hydrogen, which is also common in China, has lower efficiency (55%) and higher cost (US$2,670 kW−1). For the electrolytic production of green hydrogen from water, three kinds of electrolyser technologies are analysed in the model: AEC, SOEC and proton exchange membrane electrolysis cells. The current efficiency of AEC can be as much as 61%, and SOEC reaches 68%, with both expected to improve further in the long term. With carbon emissions constraints present in the model, electrolytic green hydrogen has obvious advantages. When taking the curtailment of wind and solar power into account, the cost of green hydrogen may be further reduced with higher renewable penetration. China’s national wind power curtailment rate reached as high as 21% in 201639, and while curtailment rates have declined since then, this is partly due to policies slowing needed investment in renewable power in affected regions until curtailment can be addressed40,41,42. Additional discussion on the cost of hydrogen can be found in Supplementary Note 9. Recent studies have estimated that renewable energy will serve a large share of China’s total final energy demand up to 205022,23,43. AEC and SOEC are identified as the most cost-effective electrolysing technologies for 2020 and 2030, respectively.

Note that many models simulate only green hydrogen production and ignore the considerable potential for blue hydrogen, likely derived from coal combined with CCUS in China (compared to natural gas with CCUS in the United States). Therefore, we consider fossil fuel-based hydrogen production technologies of varying efficiencies and scales, including natural gas reforming and coal gasification with CCUS in this study (Supplementary Table 5). Regarding hydrogen delivery, some existing model studies assume that the delivery cost is zero, while in this study, we consider both gaseous and liquid road transport. We consider transportation of hydrogen mainly by trailer trucks with efficiencies of 75–85% and average delivery costs around US$0.65–1.73 kg−1 H2 (gas) and US$3.87–6.70 kg−1 H2 (liquid)20. To simplify the analysis, all hydrogen storage is assumed to occur in tanks at an average cost of US$0.4–0.5 kg−1 (ref. 44). Long-distance transoceanic transportation of clean hydrogen or ammonia is not considered in this study.

Data availability

The data generated during and/or analysed during the current study are available in the main text and supplementary materials. Additional data are available from the corresponding authors on reasonable request. Source data are provided with this paper.

Code availability

The analysis is based on the IEA-ETSAP model tool VEDA-TIMES with its official introduction for model tools and algorithm shown at https://iea-etsap.org/index.php/documentation and https://iea-etsap.org/docs/Documentation_for_the_TIMES_Model-PartIII.pdf.

References

Hanna, R. & Victor, D. G. Marking the decarbonization revolutions. Nat. Energy 6, 568–571 (2021).

Figueres, C. et al. Emissions are still rising: ramp up the cuts. Nature 564, 27–30 (2018).

Larson, E. et al. Net-Zero America: Potential Pathways, Infrastructure, and Impacts, Final Report (Princeton Univ., 2021); https://netzeroamerica.princeton.edu/the-report

Davis, S. J. et al. Net-zero emissions energy systems. Science 360, eaas9793 (2018).

IEA Data and Statistics—Data Tools (International Energy Agency, 2022); https://www.iea.org/data-and-statistics

Normile, D. China’s bold climate pledge earns praise—but is it feasible? Science 370, 17–18 (2020).

Prasad, N. in Green, Reliable and Viable: Perspectives on India’s Shift Toward Low-Carbon Energy. Chapter: Tackling the Hard-To-Abate Sectors in India’s Energy Transition. pp.75-79. (eds Mathur, A. et al.) (CRC Press, 2018).

Energy Technology Perspectives 2020 (International Energy Agency, 2020); https://www.iea.org/reports/energy-technology-perspectives-2020

Åhman, M. Unlocking the ‘Hard to Abate’ Sectors (World Resources Institute, 2022); https://www.wri.org/climate/expert-perspective/unlocking-hard-abate-sectors

Santos, D. A., Dixit, M. K., Kumar, P. P. & Banerjee, S. Assessing the role of vanadium technologies in decarbonizing hard-to-abate sectors and enabling the energy transition. iScience 24, 103277 (2021).

Paltsev, S., Morris, J., Kheshgi, H. & Herzog, H. Hard-to-abate sectors: the role of industrial carbon capture and storage (CCS) in emission mitigation. Appl. Energy 300, 117322 (2021).

IPCC Summary for Policymakers. In Climate Change 2022: Mitigation of Climate Change (eds Shukla, P.R. et al.) (Cambridge Univ. Press, 2022).

Shen, J., Zhang, Q., Xu, L., Tian, S. & Wang, P. Future CO2 emission trends and radical decarbonization path of iron and steel industry in China. J. Clean. Prod. 326, 129354 (2021).

Fan, Z. & Friedmann, S. J. Low-carbon production of iron and steel: technology options, economic assessment, and policy. Joule 5, 829–862 (2021).

Olabi, A. G. et al. Large-scale hydrogen production and storage technologies: current status and future directions. Int. J. Hydrogen Energy 46, 23498–23528 (2021).

Larsson, M., Mohseni, F., Wallmark, C., Grönkvist, S. & Alvfors, P. Energy system analysis of the implications of hydrogen fuel cell vehicles in the Swedish road transport system. Int. J. Hydrogen Energy 40, 11722–11729 (2015).

The Future of Hydrogen (International Energy Agency, 2019); https://www.iea.org/reports/the-future-of-hydrogen#

Iron and Steel Technology Roadmap (International Energy Agency, 2020); https://www.iea.org/reports/iron-and-steel-technology-roadmap

Global Renewables Outlook: Energy Transformation 2050 (International Renewable Energy Agency, 2020); https://www.irena.org/publications/2020/Apr/Global-Renewables-Outlook-2020

Hydrogen Economy Outlook (Bloomberg New Energy Finance, 2020); https://data.bloomberglp.com/professional/sites/24/BNEF-Hydrogen-Economy-Outlook-Key-Messages-30-Mar-2020.pdf

Hydrogen Decarbonization Pathways: Part 1—A Life-cycle Assessment (Hydrogen Council, 2021); https://hydrogencouncil.com/en/hydrogen-decarbonization-pathways/

Institute of Climate Change and Sustainable Development, Tsinghua Univ. China’s long-term low-carbon development strategy and transformation path. Chin. J. Popul. Resour. Environ. 30, 1–25 (2020).

China 2050: A Fully Developed Rich Zero-Carbon Economy (Rocky Mountain Institute aad Energy Transitions Commission, 2019); https://www.energy-transitions.org/publications/china-2050-a-fully-developed-rich-zero-carbon-economy/

White Paper on China’s Hydrogen Energy and Fuel Cell Industry (China Hydrogen Energy Alliance, 2019)

Hydrogen From Renewable Power: Technology Outlook for the Energy Transition (International Renewable Energy Agency, 2018); https://www.irena.org/publications/2018/Sep/Hydrogen-from-renewable-power

Technology Data for Renewable Fuels (Danish Energy Agency, 2018); https://ens.dk/en/our-services/projections-and-models/technology-data/technology-data-renewable-fuels

Newborough, M. & Cooley, G. Developments in the global hydrogen market: the spectrum of hydrogen colours. Fuel Cells Bull. 2020, 16–22 (2020).

DOE Technical Targets for Hydrogen Production from Electrolysis (Office of Efficiency and Renewable Energy, US Department of Energy, 2020); https://www.energy.gov/eere/fuelcells/doe-technical-targets-hydrogen-production-electrolysis

Sherman, P., Chen, X. & McElroy, M. Offshore wind: an opportunity for cost-competitive decarbonization of China’s energy economy. Sci. Adv. 6, eaax9571 (2020).

Chen, S. et al. The potential of photovoltaics to power the belt and road initiative. Joule 3, 1895–1912 (2019).

Global Hydrogen Review 2021 (International Energy Agency, 2021; https://iea.blob.core.windows.net/assets/5bd46d7b-906a-4429-abda-e9c507a62341/GlobalHydrogenReview2021.pdf

Atmospheric Implications of Increased Hydrogen Use (Department for Business and Energy and Industrial Strategy, 2022); https://www.gov.uk/government/publications/atmospheric-implications-of-increased-hydrogen-use

The Role of China’s ETS in Power Sector Decarbonisation (International Energy Agency and Tsinghua Univ., 2021); https://iea.blob.core.windows.net/assets/61d5f58d-4702-42bd-a6b6-59be3008ecc9/The_Role_of_China_ETS_in_Power_Sector_Decarbonisation.pdf

HYBRIT—Fossil-Free Steel (Swedish Steel AB, Luossavaara-Kiirunavaara AB and Vattenfall, 2022); https://www.hybritdevelopment.se/en/

Advanced Research Projects Agency-Energy (US Department of Energy, 2022); https://arpa-e.energy.gov/

Horizon Europe (European Commission, 2022); https://ec.europa.eu/info/research-and-innovation/funding/funding-opportunities/funding-programmes-and-open-calls/horizon-europe_en

Hydrogen Roadmap Europe—A Sustainable Pathway for the European Energy Transition (Fuel Cells and Hydrogen Joint Undertaking, 2019); https://www.fch.europa.eu/sites/default/files/Hydrogen%20Roadmap%20Europe_Report.pdf

Yang, X., Teng, F. & Wang, G. Incorporating environmental co-benefits into climate policies: a regional study of the cement industry in China. Appl. Energy 112, 1446–1453 (2013).

Luo, G., Dan, E., Zhang, X. & Guo, Y. Why the wind curtailment of Northwest China remains high. Sustainability 10, 1–26 (2018).

He, G. & Kammen, D. M. Where, when and how much wind is available? A provincial-scale wind resource assessment for China. Energy Policy 74, 116–122 (2014).

He, G. & Kammen, D. M. Where, when and how much solar is available? A provincial-scale solar resource assessment for China. Renew. Energy 85, 74–82 (2016).

He, G. et al. Enabling a rapid and just transition away from coal in China. One Earth 3, 187–194 (2020).

Duan, H. et al. Assessing China’s efforts to pursue the 1.5 °C warming limit. Science 372, 378–385 (2021).

Sgobbi, A. et al. How far away is hydrogen? Its role in the medium and long-term decarbonisation of the European energy system. Int. J. Hydrogen Energy 41, 19–35 (2016).

Acknowledgements

This work was supported by the European Commission Horizon 2020 Project, the Harvard President’s Office and Energy Foundation China. X.Y. acknowledges the European Commission Horizon 2020 Project ‘PARIS REINFORCE’ (grant number 820846). X.Y., C.P.N. and M.B.M. acknowledge the funding support from Energy Foundation Project ‘Advanced Technologies for Decarbonization of China’s Iron and Steel Sector’ (grant number 2206-33971). X.Y., C.P.N., S.S. and M.B.M. acknowledge the Energy Foundation Project ‘Technology Systems for Carbon Neutrality’ (grant number G-2008-32164) and the Harvard President’s Office.

Author information

Authors and Affiliations

Contributions

X.Y. conceived and designed the work, contributed to data collection, performed data analysis and wrote the paper. C.P.N. contributed to verification, investigation and in-depth review and editing of the manuscript. S.S. contributed to data verification, investigation and editing the Supplementary Information. M.B.M. supervised this work and contributed to verification, review and editing the manuscript. All authors contributed to the discussion of the results and approved the manuscript.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Energy thanks Panagiotis Fragkos, Yanfei Li and the other, anonymous, reviewer(s) for their contribution to the peer review of this work.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Supplementary Information

Supplementary Tables 1–7 and Notes 1–9.

Source data

Source Data Fig. 1

Carbon emissions of key countries.

Source Data Fig. 2

Carbon mitigation potential and abatement costs of key mitigation technologies in the iron and steel industry and cement industry.

Source Data Fig. 3

Technology penetration in typical HTA sectors (2020–2060).

Source Data Fig. 4

China’s net-zero carbon emissions future. a, CO2 trajectory in BAU, NDC and ZERO-NH (2020–2060). b, CO2 trajectory in BAU, NDC and ZERO-H (2020–2060). c, Carbon mitigation costs in 2060, compared with BAU scenario. d, Total final energy consumption in BAU, NDC, ZERO-NH, ZERO-H scenarios (2020–2060). e, Primary energy mix in BAU, NDC, ZERO-NH, ZERO-H scenarios (2030–2060).

Source Data Fig. 5

Penetration of hydrogen in key HTA sectors (2060) and key regions considering multiple production technologies applied (2020–2060).

Source Data Fig. 6

Sensitivity analysis of key results. a, CO2 emissions and sectoral contribution in high- and low-GDP scenarios compared with the central case. b, Changes of hydrogen penetration in TFEC compared with the central case. c, Hydrogen penetration in key HTA sectors in 2060 considering changes of hydrogen production costs. d, Technology penetration in iron and steel, cement, ammonia and residential heating sectors in 2060 considering changes of hydrogen production costs. e, Technology penetrations in LDV, bus, heavy truck and shipping transport modes in 2060 considering changes of hydrogen production costs. f, Aggregate investment changes of the energy system considering changes in hydrogen costs.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Yang, X., Nielsen, C.P., Song, S. et al. Breaking the hard-to-abate bottleneck in China’s path to carbon neutrality with clean hydrogen. Nat Energy 7, 955–965 (2022). https://doi.org/10.1038/s41560-022-01114-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41560-022-01114-6

This article is cited by

-

Decreasing resilience of China’s coupled nitrogen–phosphorus cycling network requires urgent action

Nature Food (2024)

-

Decarbonising road freight transport: The role of zero-emission trucks and intangible costs

Scientific Reports (2024)

-

Natural resource development, economic policy uncertainty and urban residents’ consumption in China: a nonlinear ARDL and time-varying parameter vector autoregressive with stochastic volatility approach

Stochastic Environmental Research and Risk Assessment (2024)

-

Nonredox trivalent nickel catalyzing nucleophilic electrooxidation of organics

Nature Communications (2023)

-

Recent advances in efficient and scalable solar hydrogen production through water splitting

Carbon Neutrality (2023)