Abstract

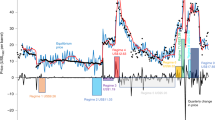

Exploration of tight oil and gas formations has significantly increased US oil and gas production in recent years. However, detailed economic analysis of this production, including identification of the break-even price (BEP), the measure of price used to plan exploration and development, a synergy between price volatility and the BEP, and a feedback effect of tight oil production on oil prices, has yet to be carried out. Here we show that the BEP for rigs used to drill oil wells is $20 (~$50 nominal), the effect of price volatility on rig activity declines as the price for crude oil or natural gas moves above or below this BEP, firms use futures prices (not spot prices) to plan exploration and development, and new rig productivity affects both drilling activity and oil prices. The latter indicates that increases in new rig productivity can account for much of the 2014 oil price decline.

This is a preview of subscription content, access via your institution

Access options

Access Nature and 54 other Nature Portfolio journals

Get Nature+, our best-value online-access subscription

$29.99 / 30 days

cancel any time

Subscribe to this journal

Receive 12 digital issues and online access to articles

$119.00 per year

only $9.92 per issue

Buy this article

- Purchase on Springer Link

- Instant access to full article PDF

Prices may be subject to local taxes which are calculated during checkout

Similar content being viewed by others

Data availability

The data and computer code are available on request from the authors.

References

Ansari, D. OPEC, Saudi Arabia, and the shale revolution: insights from equilibrium modelling and oil politics. Energy Policy 111, 166–178 (2017).

Behar, A. & Ritz, R. A. OPEC vs. US shale: analyzing the shift to a market-share strategy. Energy Econ. 63, 185–198 (2017).

Manescu, C. B. & Nuno, G. Quantitative effects of the shale oil revolution. Energy Policy 86, 866–866 (2015). 2015.

Drilling Productivity Report https://www.eia.gov/petroleum/drilling/ (EIA, December 2017); https://www.eia.gov/petroleum/drilling/

Kleinberg, R. L., Paltsev, S., Ebinger, C. K. E., Hobbs, D. A. & Boersma, T. Tight oil market dynamics: benchmarks, breakeven points, and inelasticities. Energy Econ. 70, 70–83 (2018).

Watchmeister, H., Lund, L., Aleklett, K. & Hook, M. Production decline curves of tight oil in Eagle Ford shale. Nat. Resour. Res. 26, 365–377 (2017).

Likvern, R. Is shale production from the Bakken headed for a run with “The Red Queen”? The Oil Drum http://www.theoildrum.com/node/9506 (2012).

Boyce, J. R. & Nøstbakken, L. Exploration and development of US oil and gas fields, 1955–2002. J. Econ. Dyn. Control 35, 891–908 (2011).

Khalifa, A., Caporin, M. & Hammoudeh, S. The relationship between oil prices and rig counts: the importance of lags. Energy Econ. 6, 213–226 (2012).

Henriques, I. & Sandorsky, P. The effect of oil price volatility on strategic investment. Energy Econ. 33, 79–87 (2011).

Kellogg, R. The effect of uncertainty on investment, evidence from Texas oil drilling. Am. Econ. Rev. 104, 1698–1744 (2014).

Compernolle, T., Welkenhuysen, K., Huisman, K., Piessens, K. & Kort, P. M. Offshore enhanced oil recovery in the North Sea: the impact of price uncertainty on the investment decisions. Energy Policy 101, 123–137 (2017).

Guedes, J. & Santos, P. Valuating an offshore oil exploration and production project through real options analysis. Energy Econ. 60, 377–386 (2016).

Trends in U.S. Oil and Gas Upstream Costs (EIA, 2015); https://www.eia.gov/analysis/studies/drilling/pdf/upstream.pdf

Juselius, K. The Cointegrated VAR Model: Methodology and Applications (Advanced Texts in Econometrics) (Oxford Univ. Press, 2006).

Ederington, L. & Lee, J. H. Who trades futures and how: evidence from the heating oil futures markets. J. Bus. 75, 353–373 (2002).

Buhami-Oskoopee, M. & Aftab, M. Malaysia–EU trade at the industry level: is there an asymmetric response to exchange rate volatility? Empirica 45, 425–455 (2018).

Granger, C. W. J. & Lee, T. H. Investigation of production, sales and inventory relationships using multicointegration and nonsymmetric error correction models. J. Appl. Econ. 4, S145–S159 (1989).

Bataa, E. & Park, C. Is the recent low oil price attributable to the shale revolution? Energy Econ. 67, 72–82 (2017).

Tokic, D. The 2014 oil bust: causes and consequences. Energy Policy 85, 162–169 (2014).

Baumeister, C. & Kilian, L. Understanding the decline in the price of oil since June 2014. J. Assoc. Environ. Res. Econ. 3, 131–158 (2016).

Akins, J. E. The oil crisis: this time the wolf is here. Foreign Aff. 51, 463–490 (1973).

Kaufmann, R. K., Dees, S., Karadeloglou, P. & Sanchez, M. Does OPEC matter? An econometric analysis of oil prices. Energy J. 25, 67–90 (2004).

Kaufmann, R. K., Dees, S., Gasteuil, A. & Mann, M. Oil prices, the role of refinery utilization, futures markets, and non-linearities. Energy Econ. 30, 2609–2622 (2008).

Chevillon, G. & Rifflart, C. Physical market determinants of the price of crude oil and the market premium. Energy Econ. 31, 537–549 (2009).

Sheiks vs shale. The Economist (6 December 2014).

The new winners and loser in America’s oil shale boom. Wall Street Journal (21 April 2014).

Sandrea, I. US Shale Gas and Tight Oil Industry Performance: Challenges and Opportunities Oxford Energy Comment (Oxford Institute for Energy Studies, 2014).

Domanski, D. & Kearns, J. & Lombardi, M. & Shin, H. S. Oil and debt. BIS Q. Rev. 55–65 (March 2015).

US oil companies closer to balancing capital investment with operating cash flow. EIA Today in Energy https://www.eia.gov/todayinenergy/detail.php?id=27112 (2016).

Bureau of Labor Statistics (December 2017); https://data.bls.gov/cgi-bin/surveymost?cu

Enders, W. Applied Time Series Econometrics (Wiley, 1995).

Juselius, K. The cointegrated VAR methodology. In Oxford Research Encyclopedia of Economics and Finance (Oxford Univ. Press, 2017).

Johansen, S. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models (Advanced Texts in Econometrics) (Oxford Univ. Press, 1996).

Hendry, D. F. &. Doornik, J. A. Empirical Model Discovery and Theory Evaluation: Automatic Selection Methods in Econometrics (MIT Press, 2014).

Castle, J. L., Doornik, J. A., Hendry, D. F. & Pretis, F. Detecting location shifts during model selection by step-indicator saturation. Econometrics 3, 240–264 (2015).

Doornik, J. A. in The Methodology and Practice of Econometrics: A Festschrift In Honour of David F. Hendry (eds Castle, J. & Shephard, N.) Ch. 4 (Oxford Univ. Press, 2009).

Acknowledgements

We thank A. Berman, A. Behar, C. A. S. Hall, L. Nogueira Hallack, M. Kah, A. Ali Khalifa, R. Kleinberg and R. Ritz for comments on preliminary versions of this work and J. Lieskovsky and F. Pretis for assistance in accessing data. Any errors that remain are our responsibility.

Author information

Authors and Affiliations

Contributions

Both authors played a role in collecting the data, estimating statistical models, analysing the results and writing the manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note: Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Supplementary Figures and Text

Supplementary Notes 1–6, Supplementary Figures 1–6, Supplementary Tables 1–4, Supplementary references.

Rights and permissions

About this article

Cite this article

Ansari, E., Kaufmann, R.K. The effect of oil and gas price and price volatility on rig activity in tight formations and OPEC strategy. Nat Energy 4, 321–328 (2019). https://doi.org/10.1038/s41560-019-0350-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41560-019-0350-1

This article is cited by

-

Price Responsiveness of Shale Oil: A Bakken Case Study

Natural Resources Research (2022)

-

Energy Price Jumps, Fat Tails and Climate Policy

Environmental Modeling & Assessment (2022)

-

Reply to: Why fossil fuel producer subsidies matter

Nature (2020)

-

Oil price regimes and their role in price diversions from market fundamentals

Nature Energy (2020)

-

Rigging economics

Nature Energy (2019)